Two things are all but guaranteed for the rest of the week:

The Fed is going to hike 75 basis points (2.25%-2.50%) and signal that it remains vigilant about inflation. Their characterization of growth dynamics are likely to remain on the rosier side, and inflation expectations are probably the only area where they might signal comfort. Given the Fed's willingness to hike aggressively right now, the risks of a recession are elevated.

We will be debating whether Q1 and Q2 GDP releases could potentially count as a recession. To which my primary contribution is:

What I think of the 2022H1 "Is this officially a recession?" debate

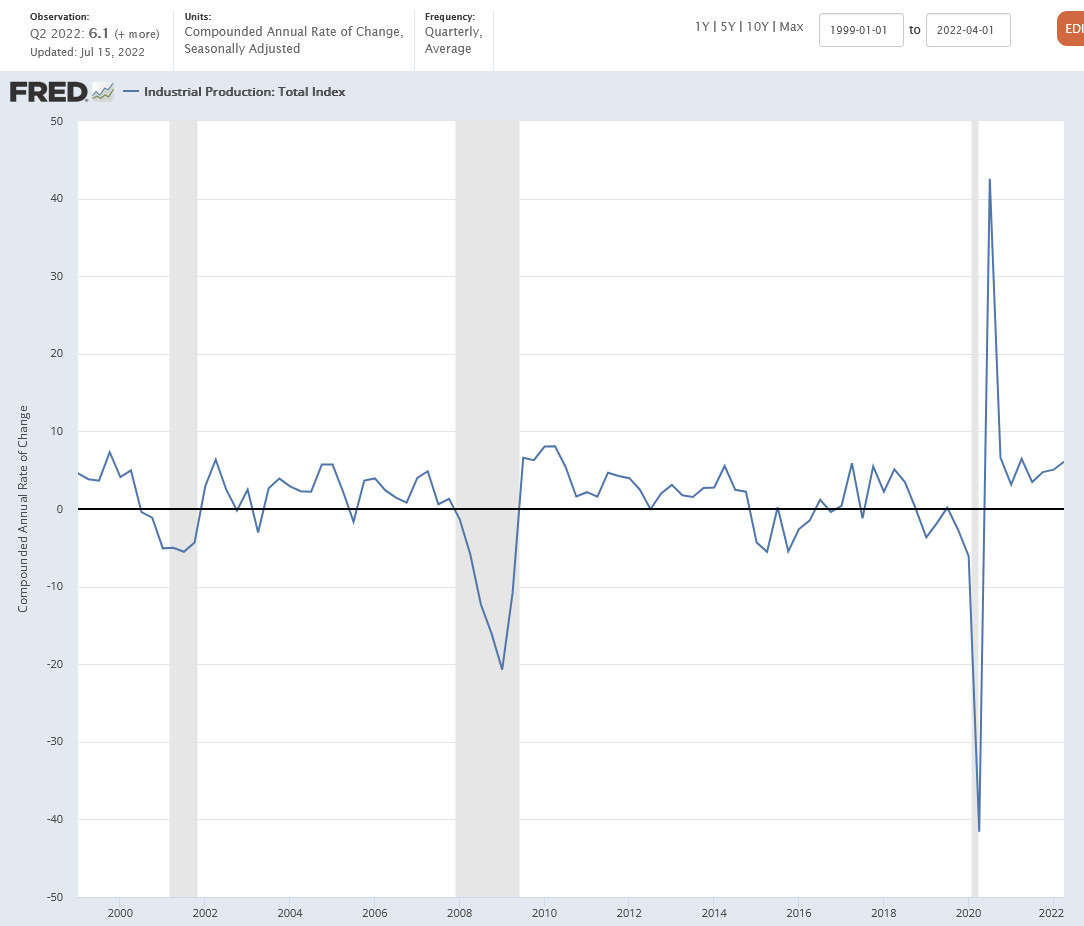

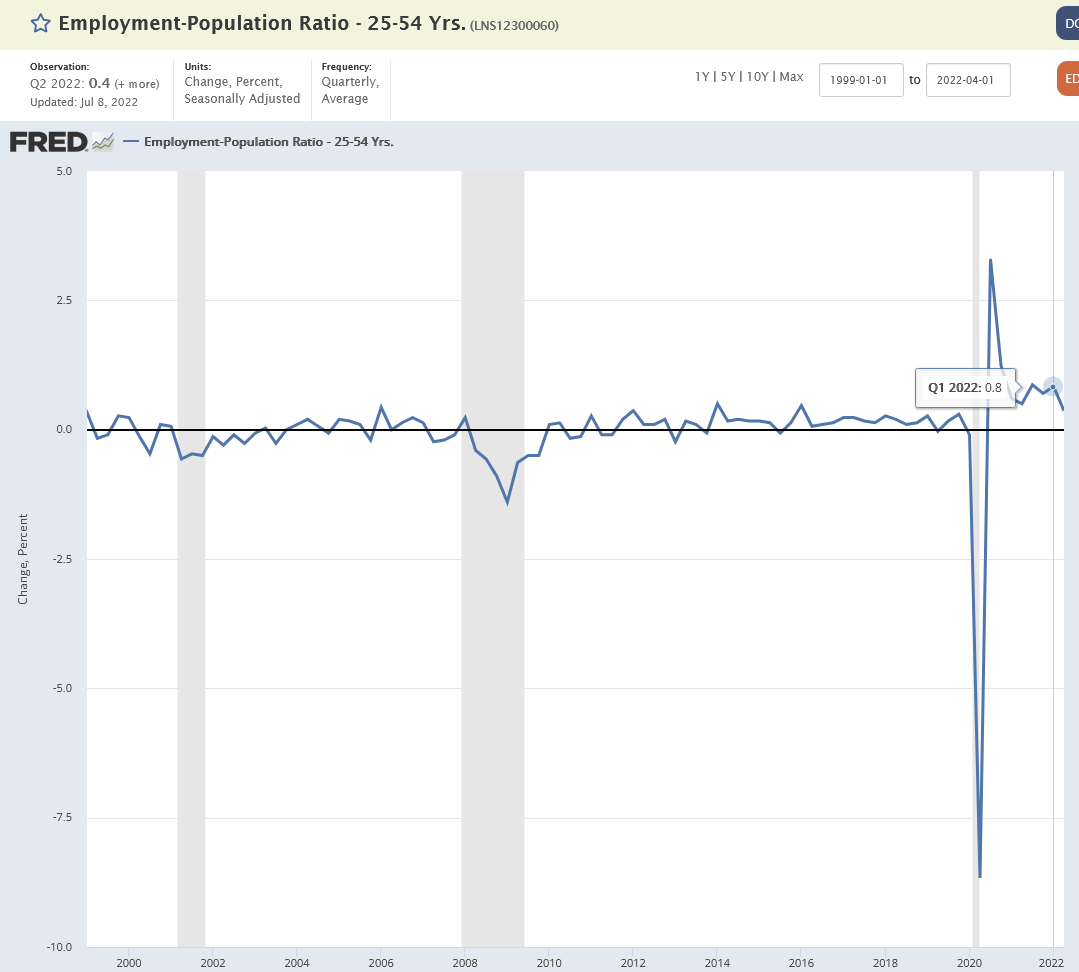

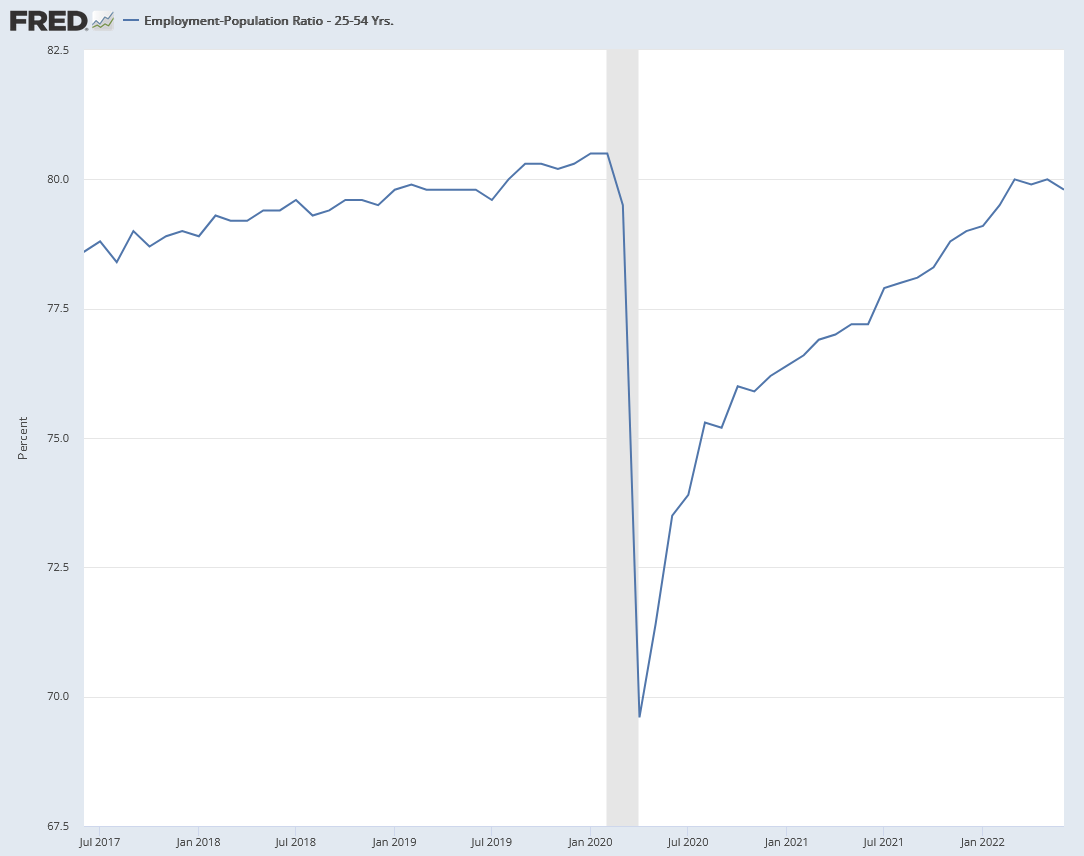

The downside risks to the growth outlook should be taken seriously, but they are primarily in the coming months and quarters, not in the recent past. 2022H1 saw historically strong gains in employment and industrial production, clearly at odds with the characterization of a recession. While a business cycle peak could have formed in May or June of 2022, it certainly did not materialize in December 2021.

The difficulty for describing the business cycle right now is that while 2022H1 GDP is not representative of what happened, communication of these dynamics can be conflated with a description of the economic outlook. Not all slowdowns lead to recessions, but all recessions begin with an economic slowdown. The risk of a recessionary policy mistake from the Fed looms large for four key reasons:

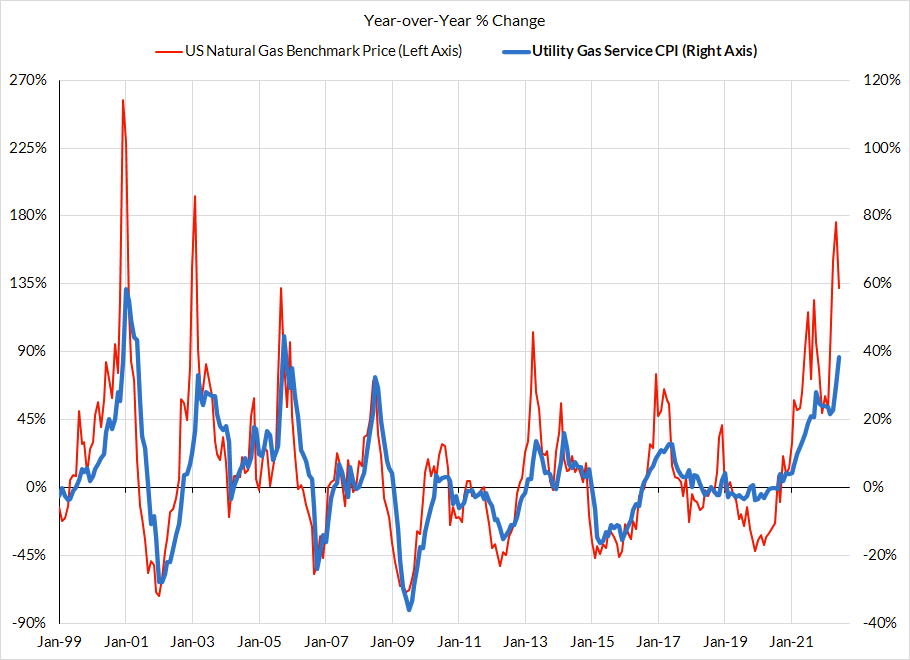

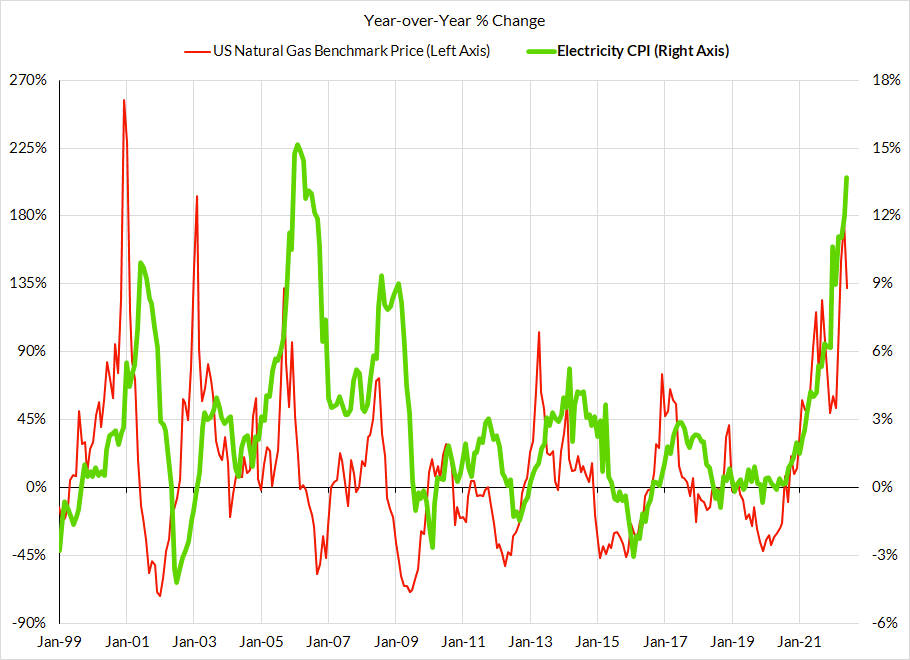

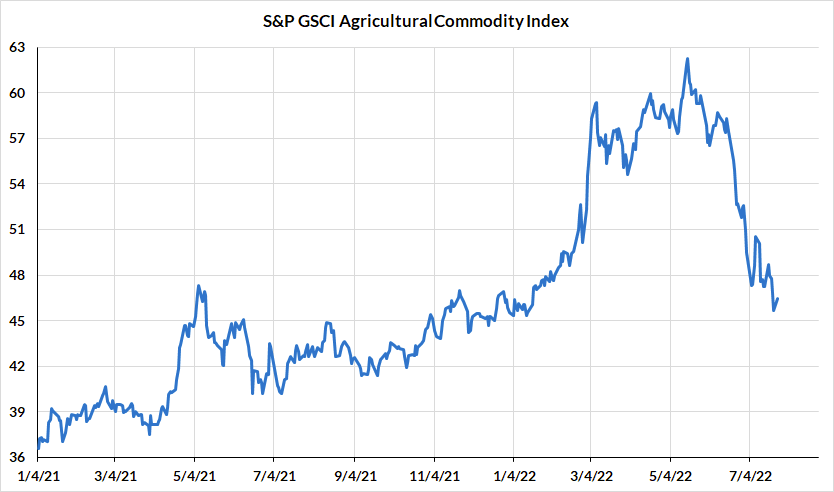

The Fed is fixated on a lagging indicator—inflation—at a time when commodity price dynamics could still put upward pressure on consumer prices simply through lagged passthrough effects. We already know that rental inflation will not provide substantial relief for at least a few more months. But if the economy otherwise slows down precipitously, many of these dynamics are not representative of what we are likely to see on a forward looking basis.

Commodity price shocks are already cramming the budgets of households and businesses. Luckily both have elevated liquidity buffers to weather some of the shock, but those buffers are ultimately finite. We are already seeing real consumption growth slow, though nominal spending patterns look less ominous.

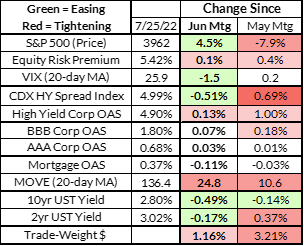

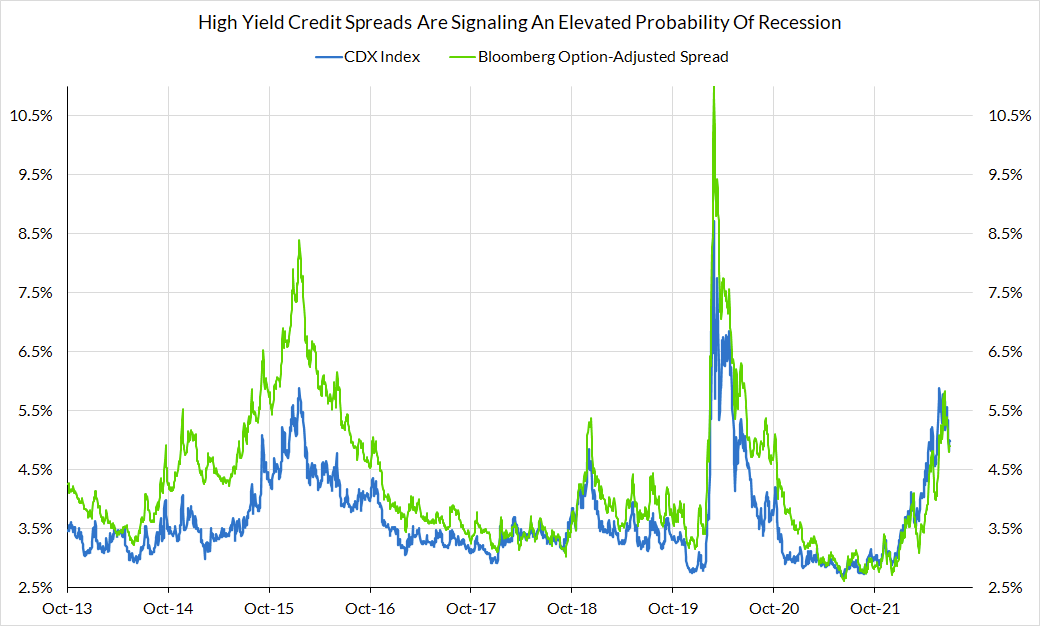

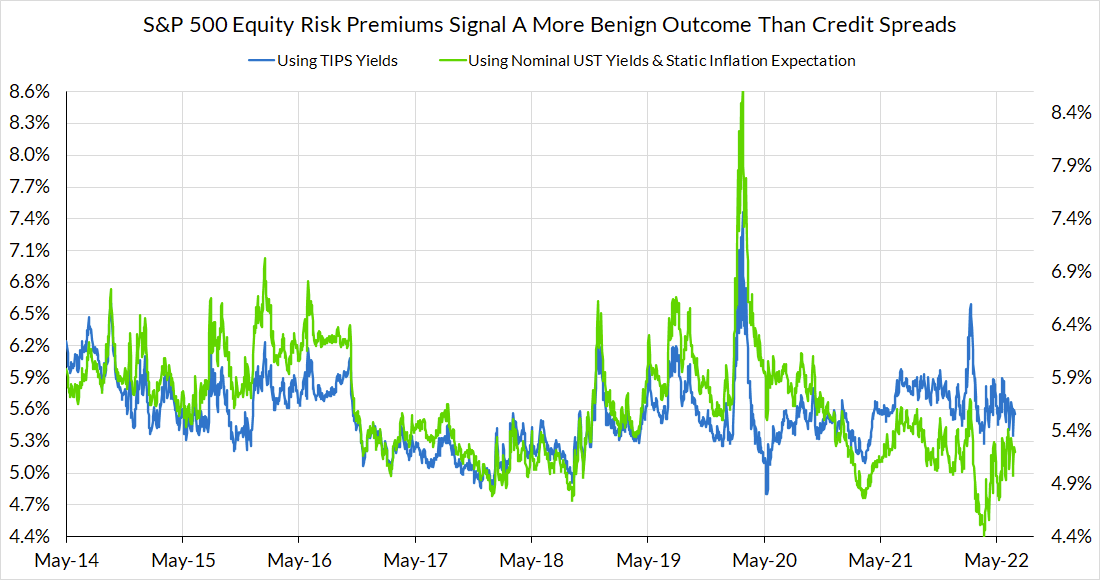

The Fed is underrating the effects of its rate hikes on financial conditions, which have tightened far more aggressively in 2022 than their 225 basis points of hikes otherwise suggests. Additional hikes are already baked into market expectations. Credit spreads have generally widened, suggesting that rate hike expectations are also inciting additional risk aversion for certain fixed income borrowers. Interest rate volatility is systematically, and in such a way that keeps mortgage rates higher.

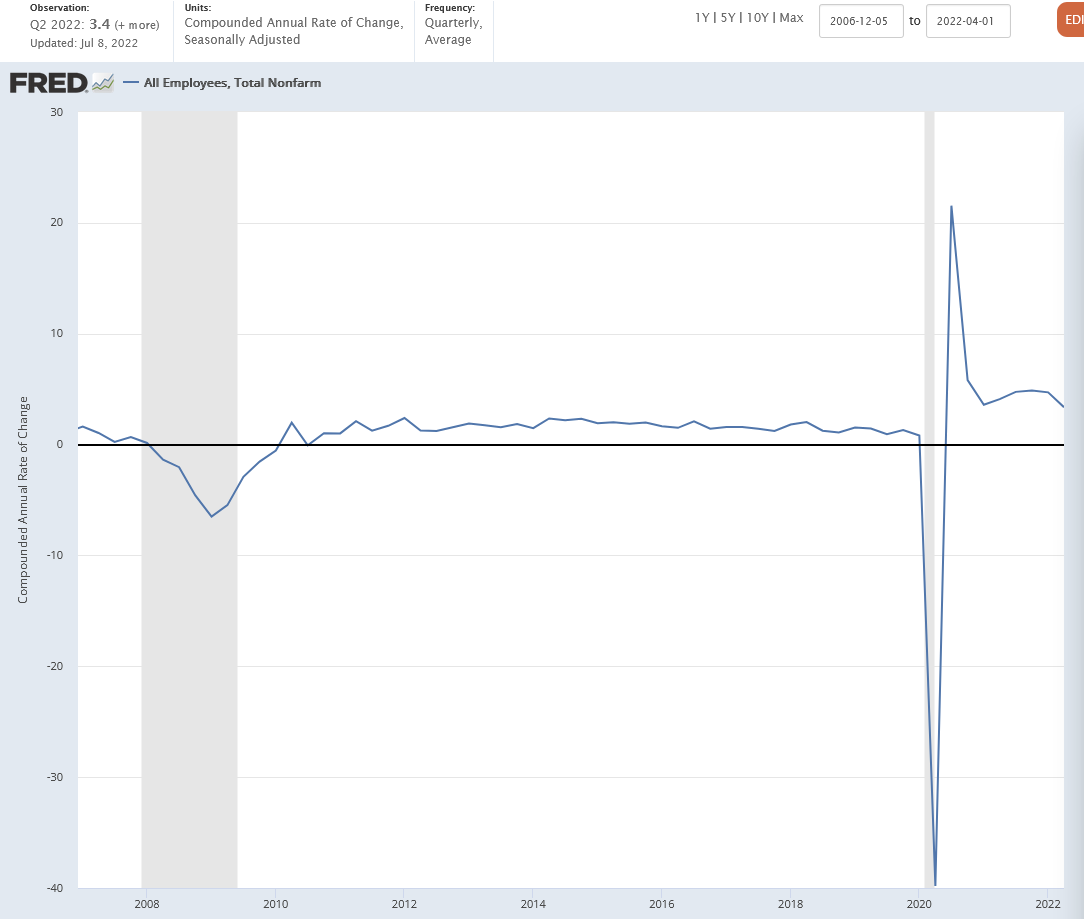

The economy is already slowing down and the pace of layoffs is starting to pick up. While seasonal adjustment effects might uniquely color some of the weekly data, it is clear at this point that initial jobless claims are on the rise. The scale of this rise need not be recessionary but the rise is substantial enough that recession probabilities should be elevated. Should the rise in layoffs continue, nominal consumer spending is also likely to slow, and with it, businesses' willingness to hire and invest (the recessionary feedback loop).

Fed officials claim it does not intend to induce a recession. But without clear ways to know "when enough is enough" the Fed's aggressive path runs the risk of overshooting of what is otherwise intended. In light of these risks, the Fed is going to need some kind of offramp to a more judicious and flexible tightening path. Chair Powell is unlikely to provide hints of any such offramp on the back of such a (predictably) hot June CPI print. But as we approach the September FOMC meeting, he and his colleagues should be more directly communicating how the following factors feed into their outlook of inflation (an indicator that otherwise tends to lag real and nominal spending dynamics):

Financial conditions tightening, which has generally proceeded at a faster pace than what Fed hikes otherwise indicate.

Slowing nominal spending and income growth (consumer spending components, employment and wage measures)

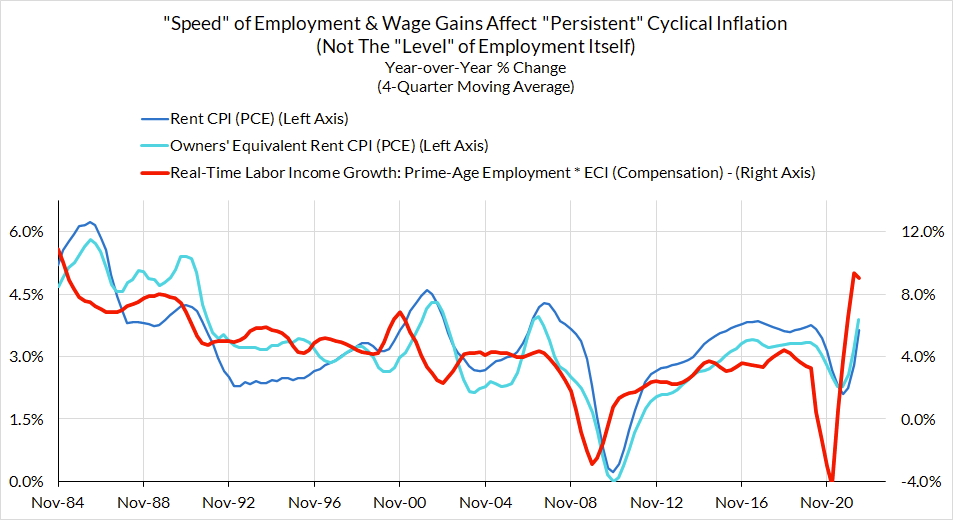

Lagged inflation dynamics that are functions of either 1) past/ongoing commodity price increases (e.g. the effect of natural gas prices on energy services) or 2) past labor market dynamics (e.g. the surging recovery in jobs and wages feeding into rent and OER)

Charts

Financial Conditions Have Shown More Stability Since The June FOMC Meeting But Still Much Tighter Than the FOMC Meeting

Consumer Price Inflation Is Still Vulnerable To Lagged Effects From Past Shocks And Dynamics

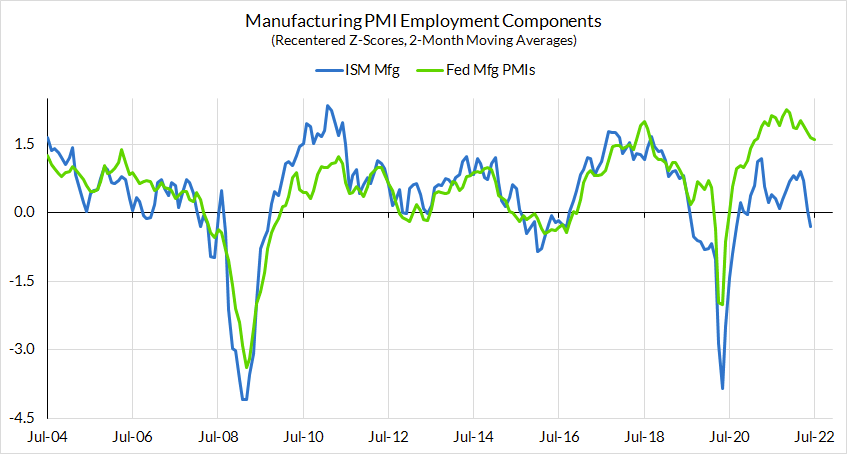

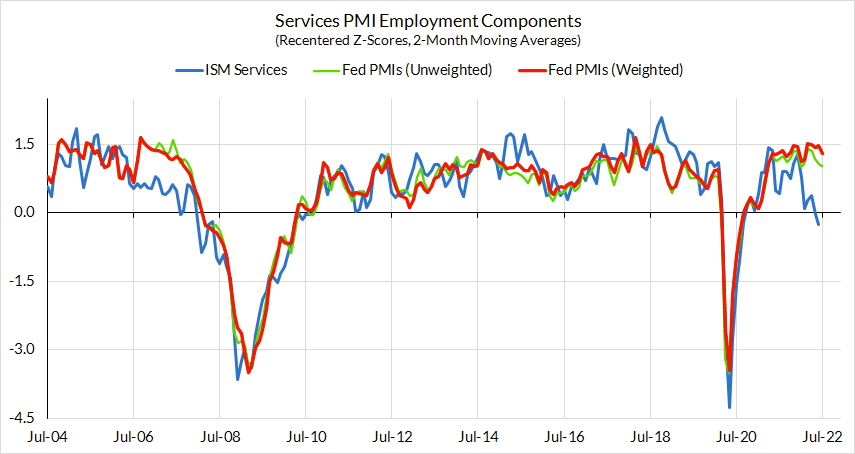

Job Growth Is Already Cooling Down And Layoffs Have Been Rising

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.