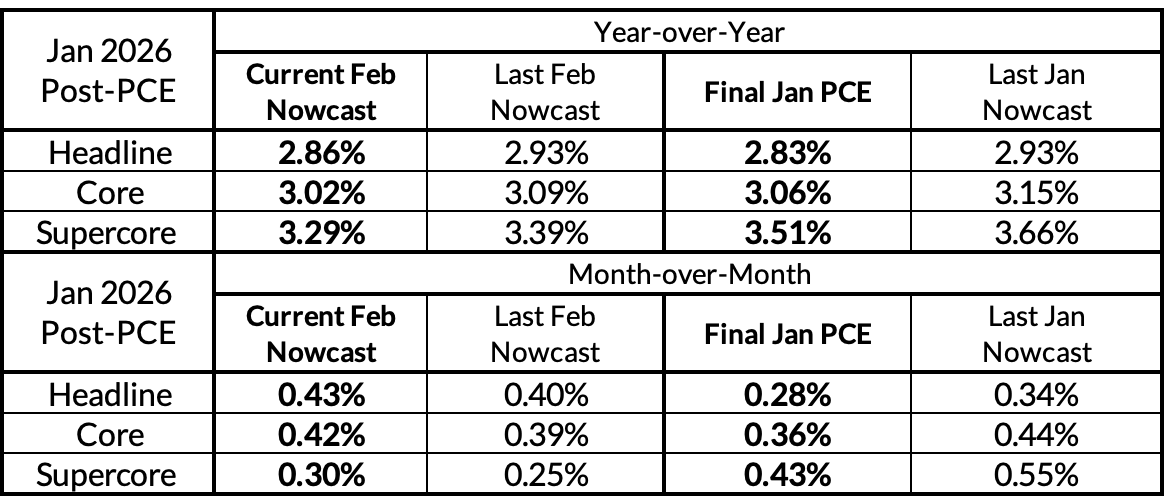

We pride ourselves on being among the closest in our forecasts / nowcasts of Core PCE, especially after receiving all of the relevant information from CPI, PPI, and import prices. January proved to be an uncharacteristic miss for us (8-9bps too high on Core PCE). We would be suspicious of those who nailed the final reading given what the Bureau of Economic Analysis (BEA) just engaged in, since there was no way to forecast the BEA's one-off methodology change for tracking legal service price changes. Inflation is still far too hot for the Fed's comfort, but it should have been hotter, had the BEA adhered to its standard practices for estimating PCE.

We would have been close to the final outcome if the methodology was fully stable, but some of the seasonal factors for CPI- and PPI-sourced NSA series also came in a bit softer than we expected, and this pushes up our nowcasts for February Core PCE at the margin. We expect the Fed to remain on hold indefinitely given the upward momentum in the inflation data, which is already 1% above target even before considering the shocks tied to the closure of the Strait of Hormuz. We will learn more on Wednesday about February Core PCE from the relevant PPI inputs.

BEA, We Have A Problem

The Bureau of Economic Analysis (BEA) appears to have engaged in an ad hoc methodology change, choosing on a one-off basis to ignore an upside surprise to the unpublished CPI legal services series. For the past several months and quarters, the CPI legal services series has gone unpublished from the BLS, but could nevertheless be backed out from the other available CPI data. We have been carefully calculating every possible unpublished series each month because they are direct inputs into specific PCE inflation components, and enhance our nowcast estimates.

Instead of using the CPI legal services series, the BEA decided, all of a sudden, to use legal services PPI data for January, and January alone. There is a time and a place to shift the source data and time series associated with PCE—that time is the annual benchmark revisions, not a random January.

It is true that the CPI legal services series is increasingly volatile and based on dubiously small sample, but here's a dirty secret: there are other components of PCE inflation that also suffer from this issue but are nevertheless included in the calculation. Inflation measurement is never universally robust. That a given series is exhibiting volatility and smaller samples is not, in and of itself, a reason to censor it or substitute to a different source. What the BEA has done amounts to a form of aysmmetric data censorship.

The most concerning aspect of the BEA's decision is the lack of transparency. To the extent the BEA felt the CPI legal services series was so uniquely unreliable to warrant a deviation in practice, such a change should have been communicated transparently to the public with corresponding reasoning. Instead, the public has had to rely on a series of private communications that were later shared through non-governmental outlets.

We do not allege or ascribe ill intent to the BEA. The Bureau is filled with diligent, thoughtful public servants who generally do an exceptional job. Statistical agencies must subject themselves to the highest of standards to retain legitimacy. The opaque, ad hoc, and asymmetric adjustment to the January PCE inflation fell substantially short of the top standards the BEA generally adheres to.

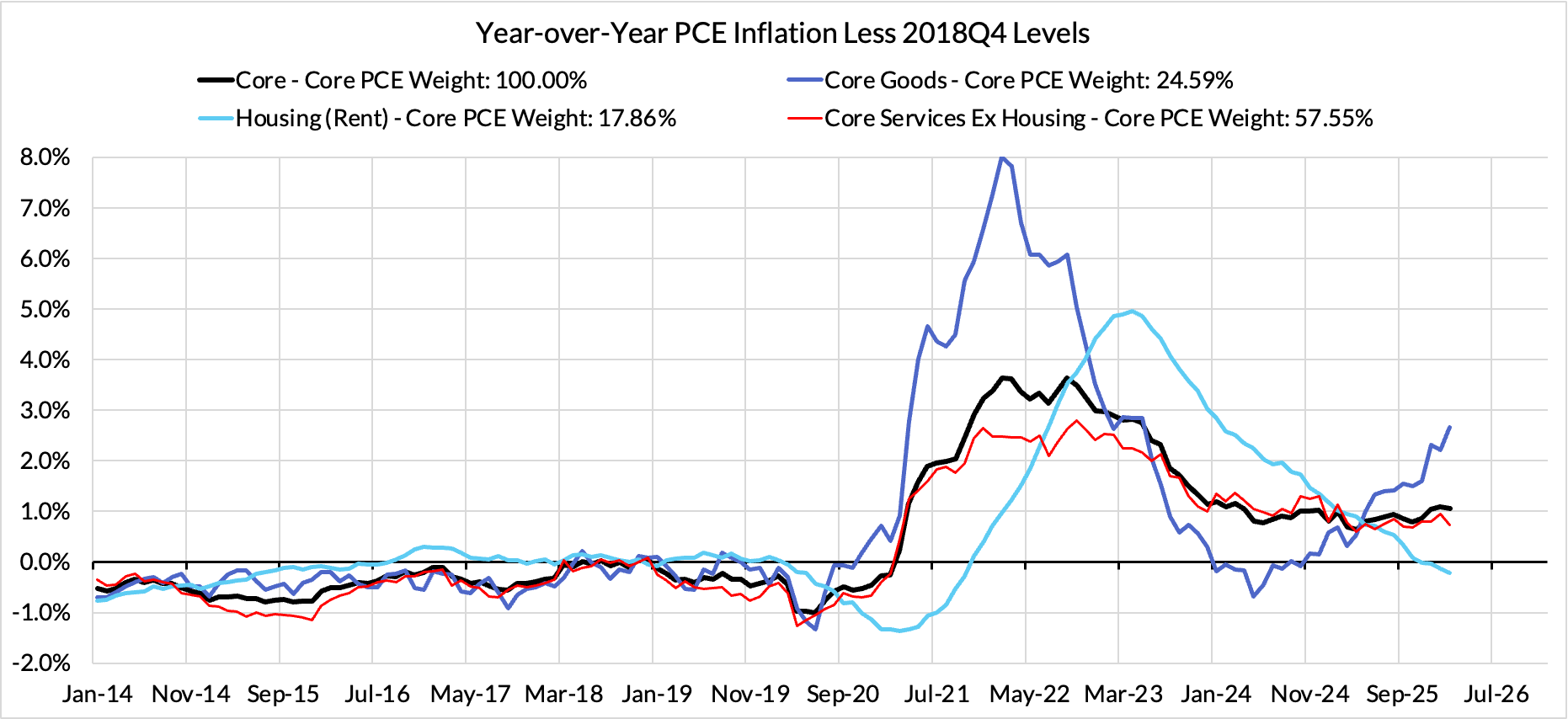

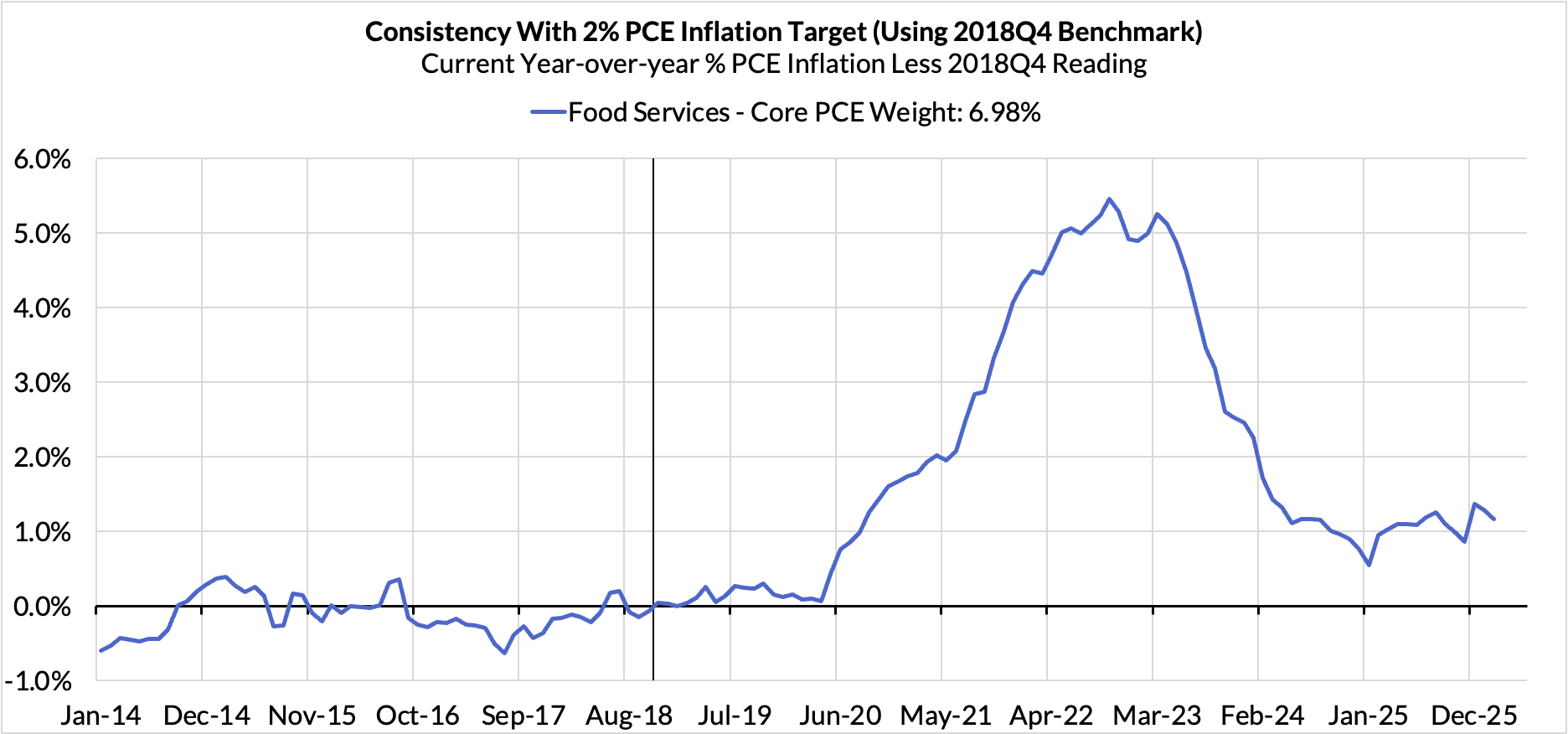

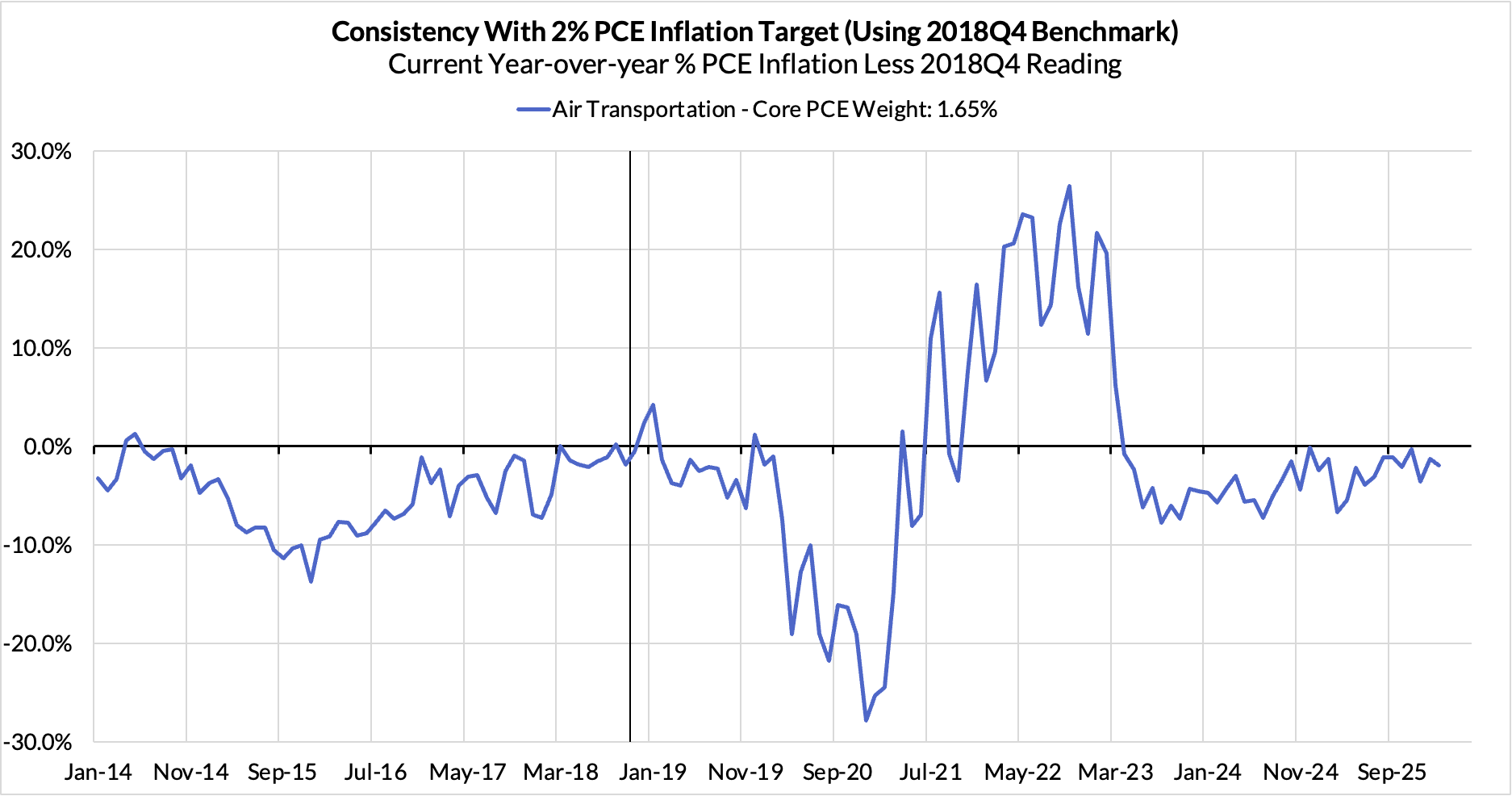

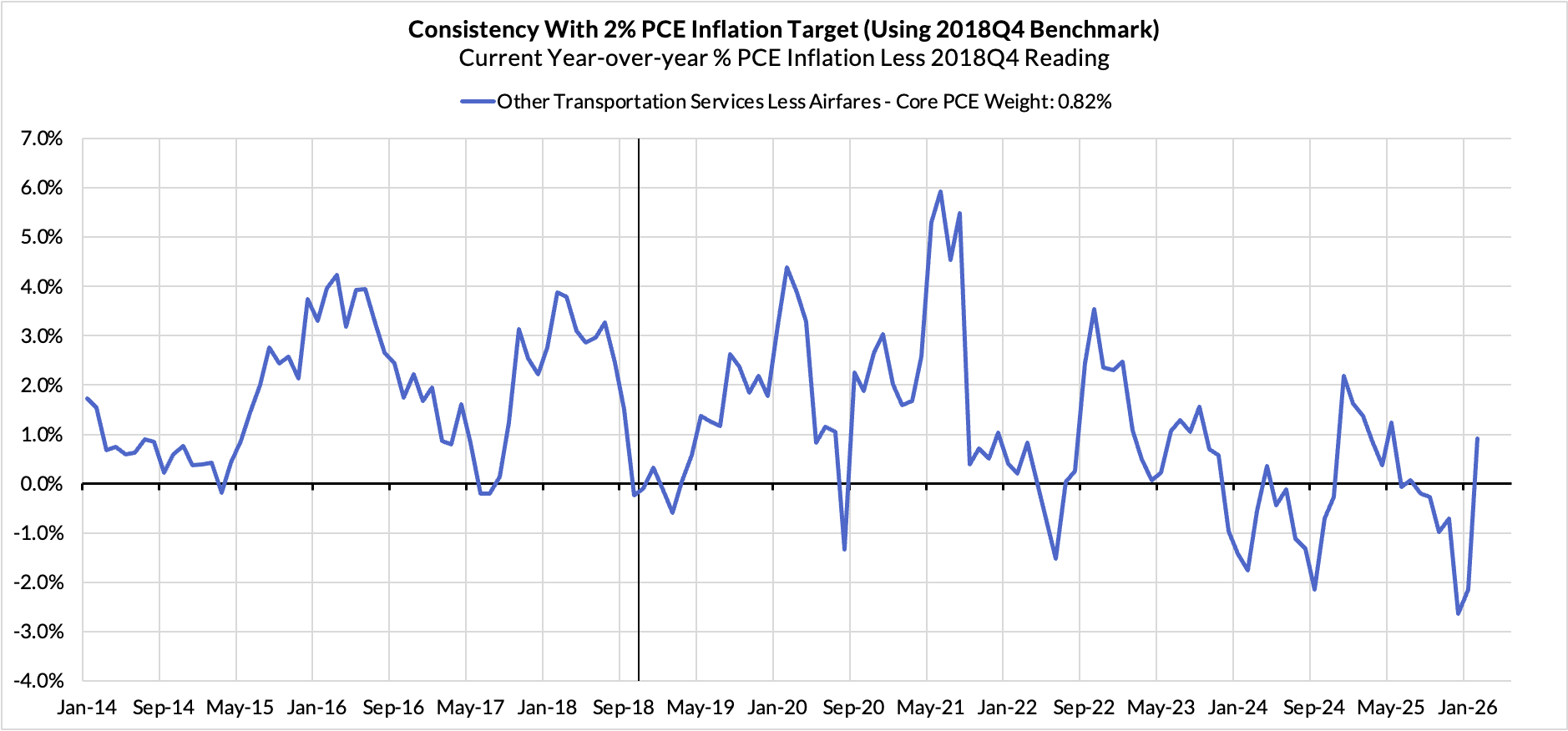

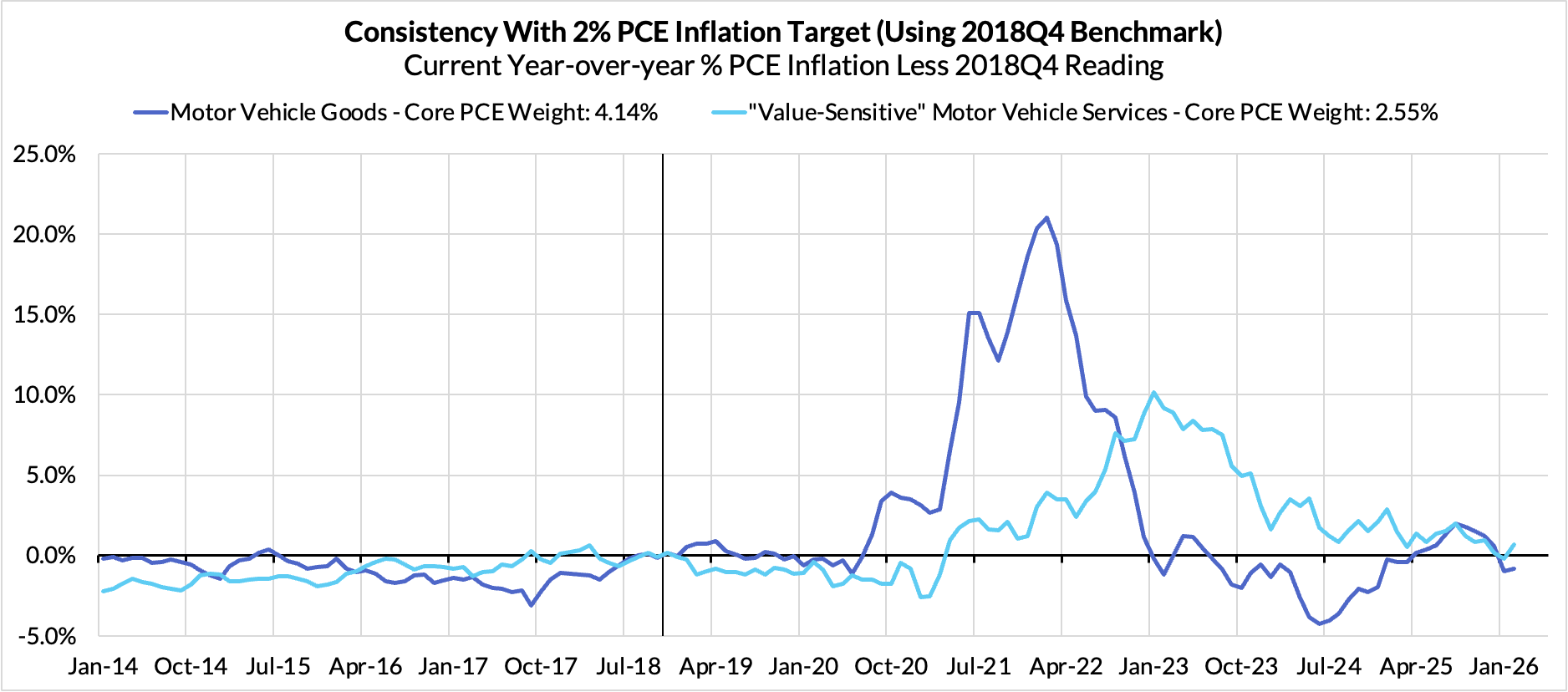

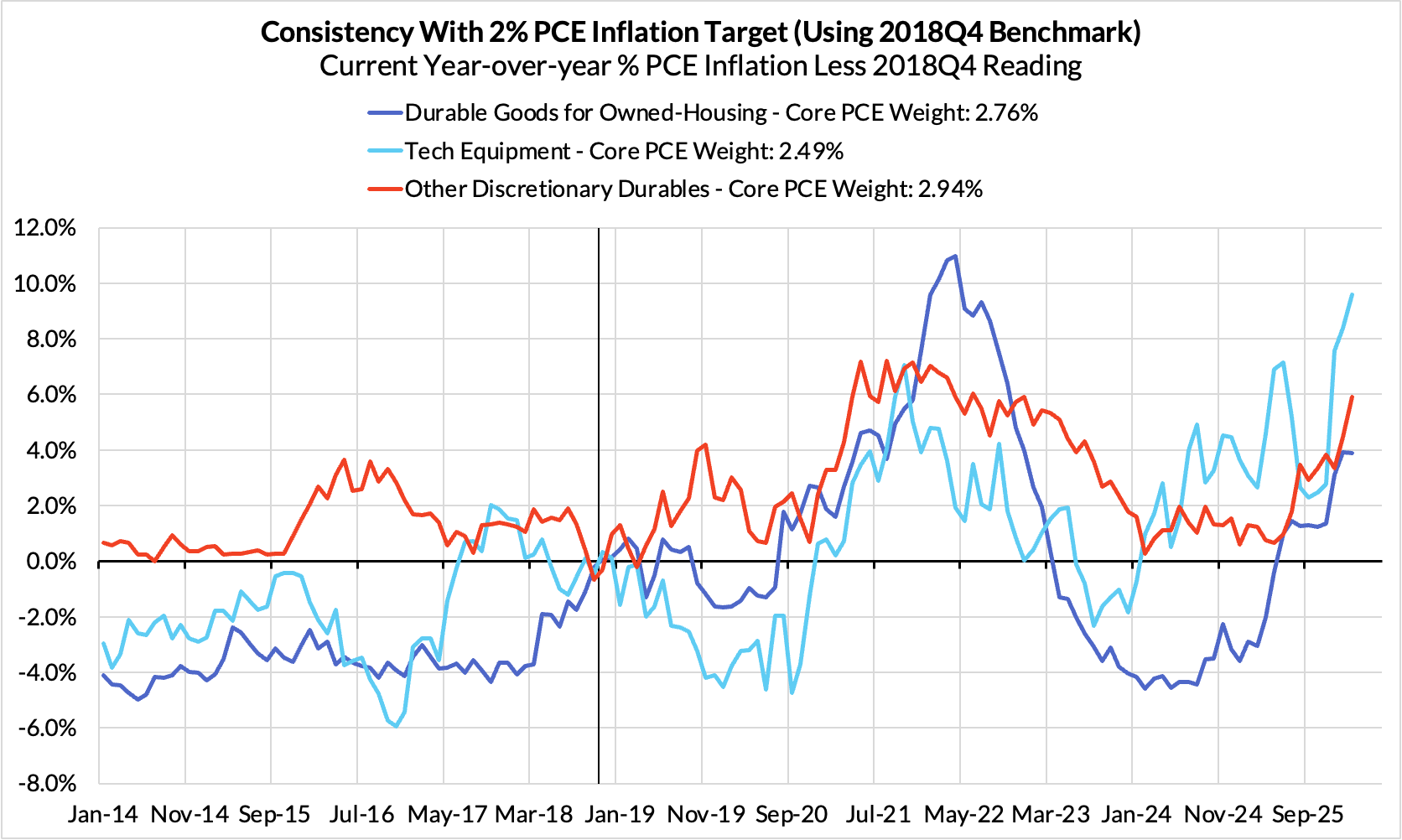

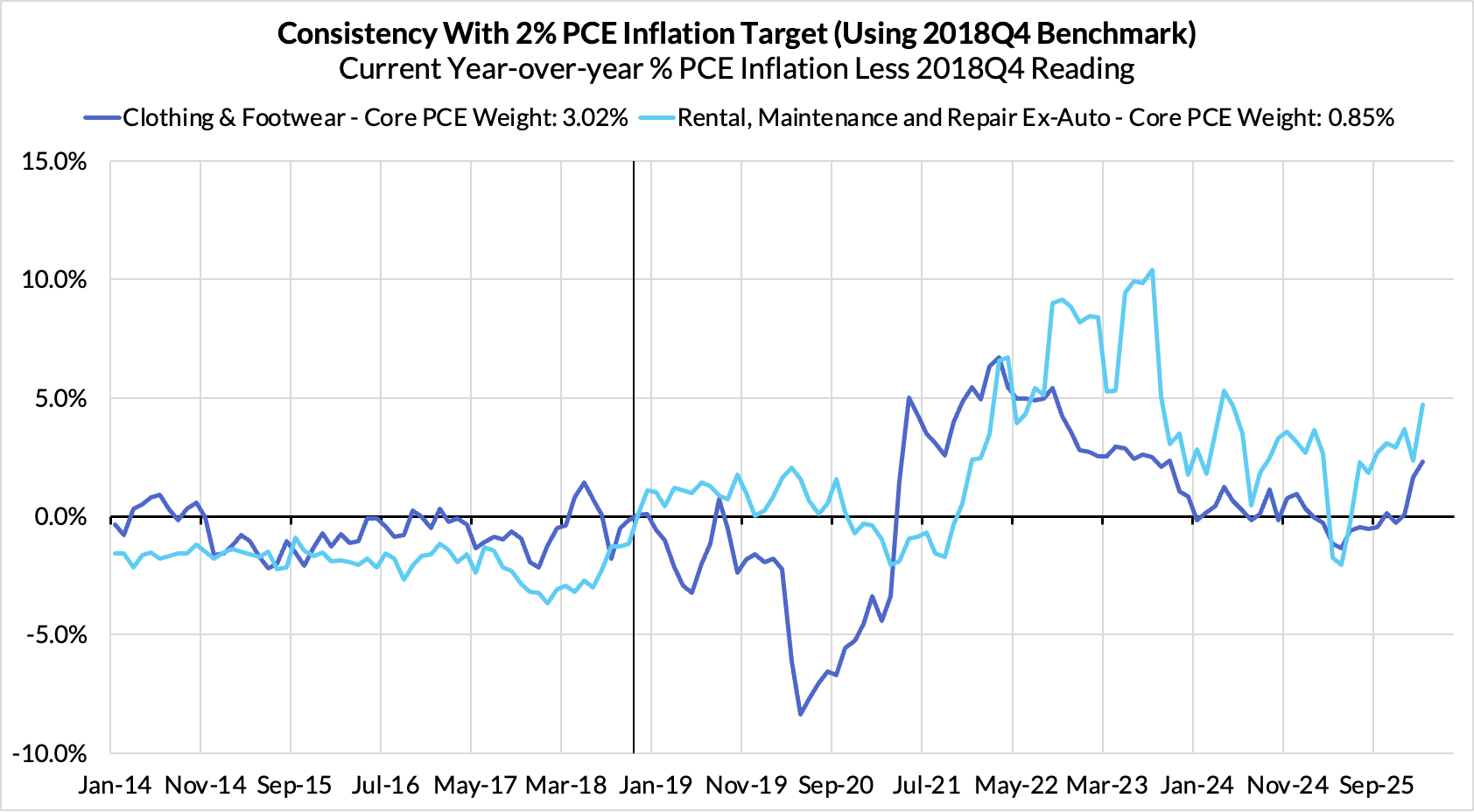

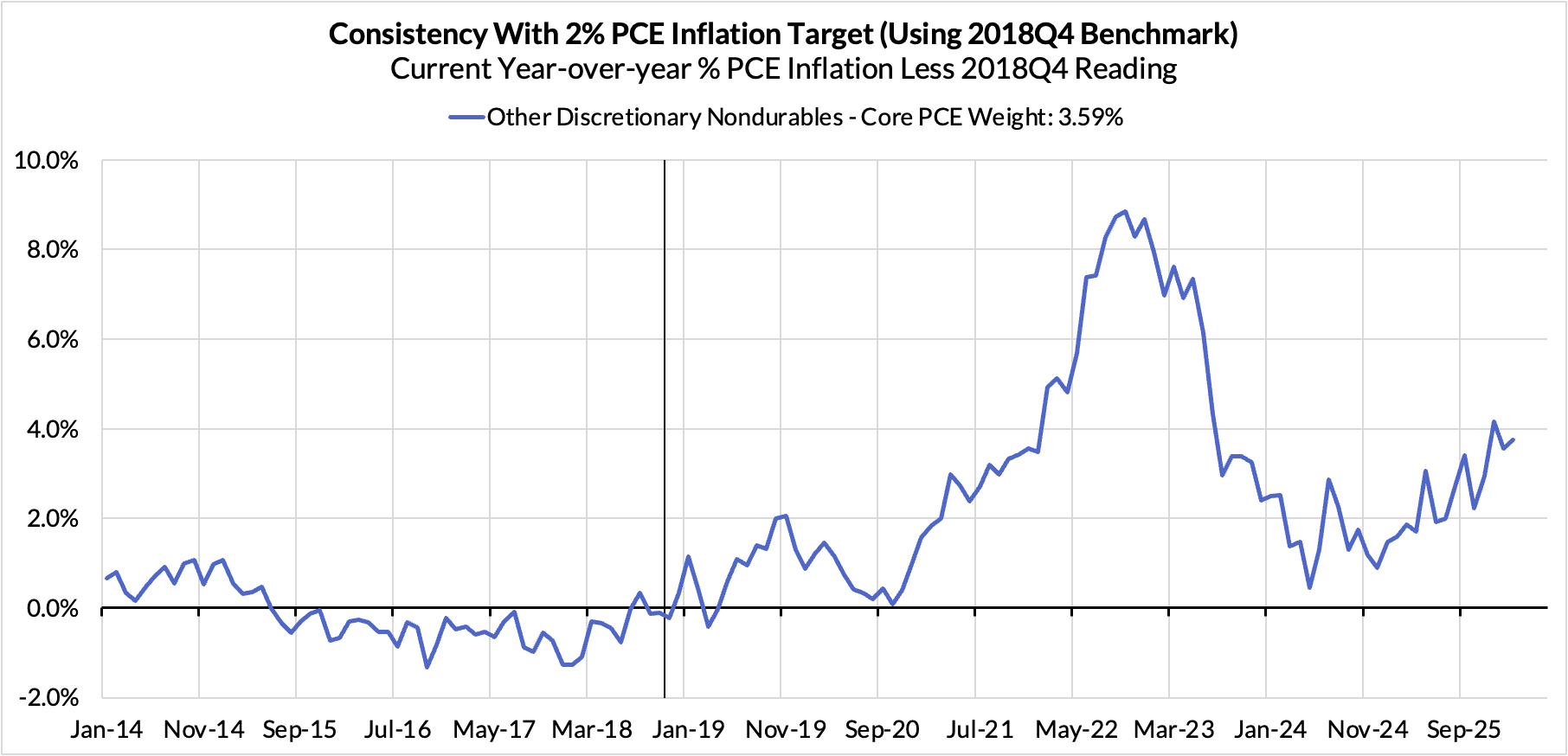

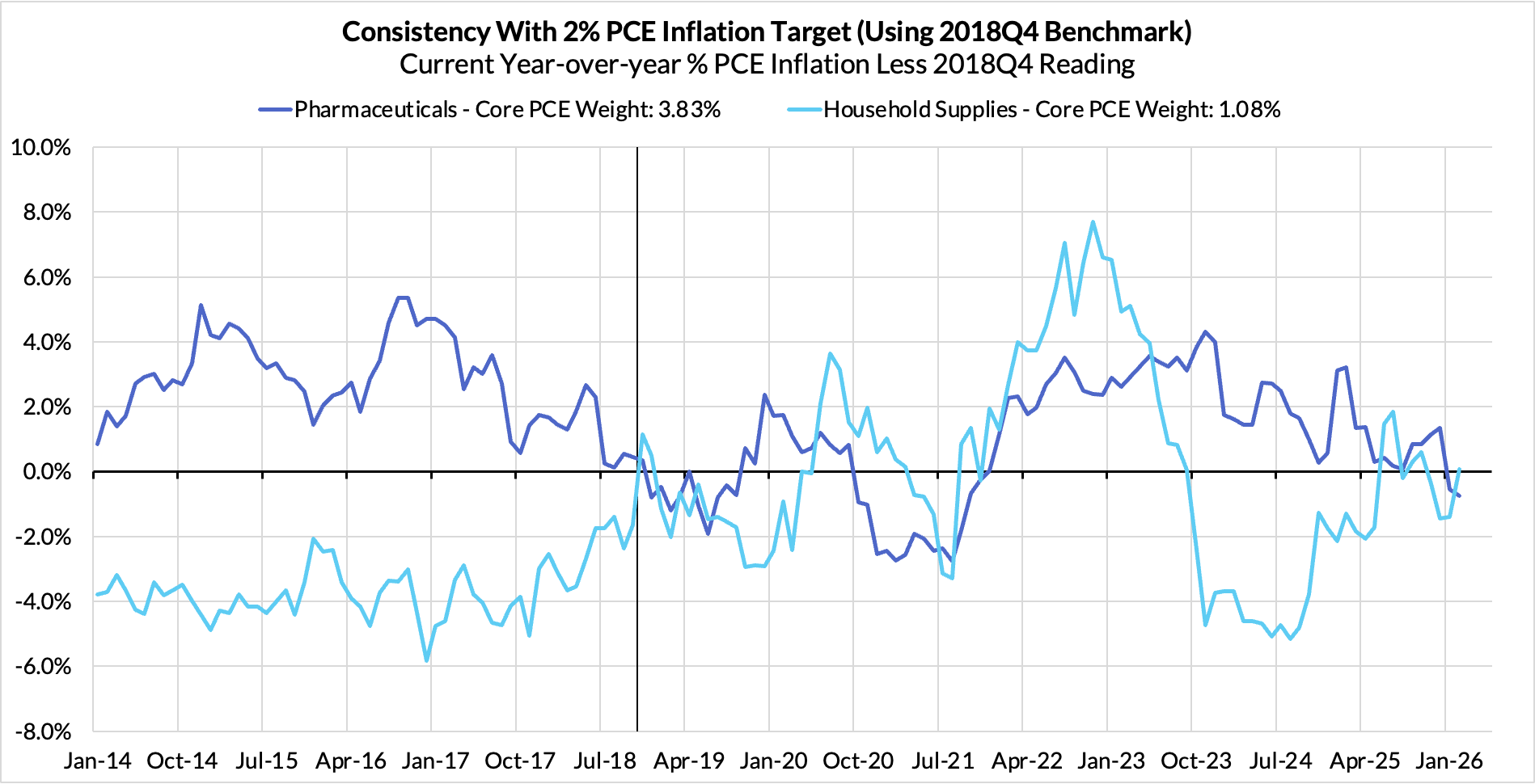

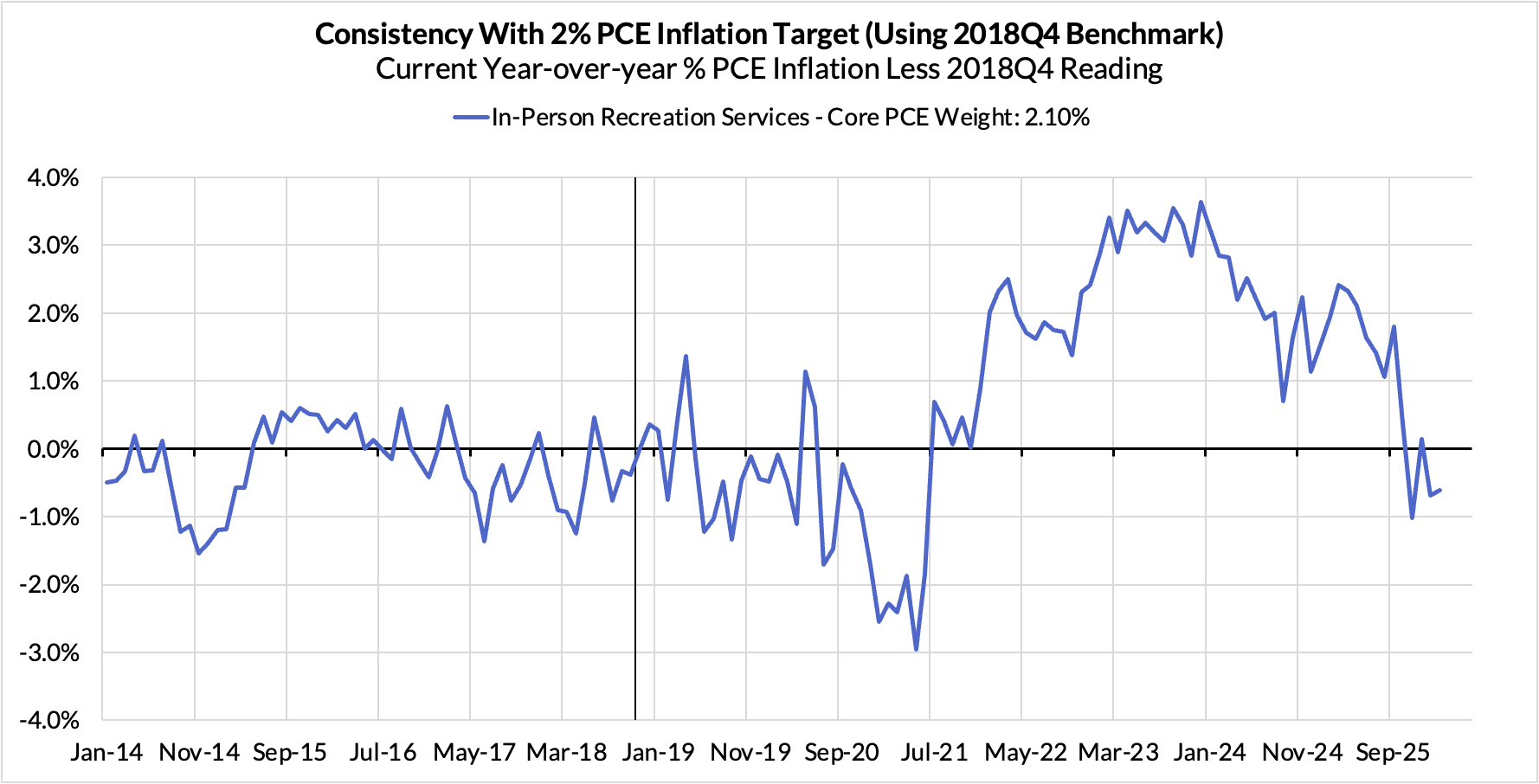

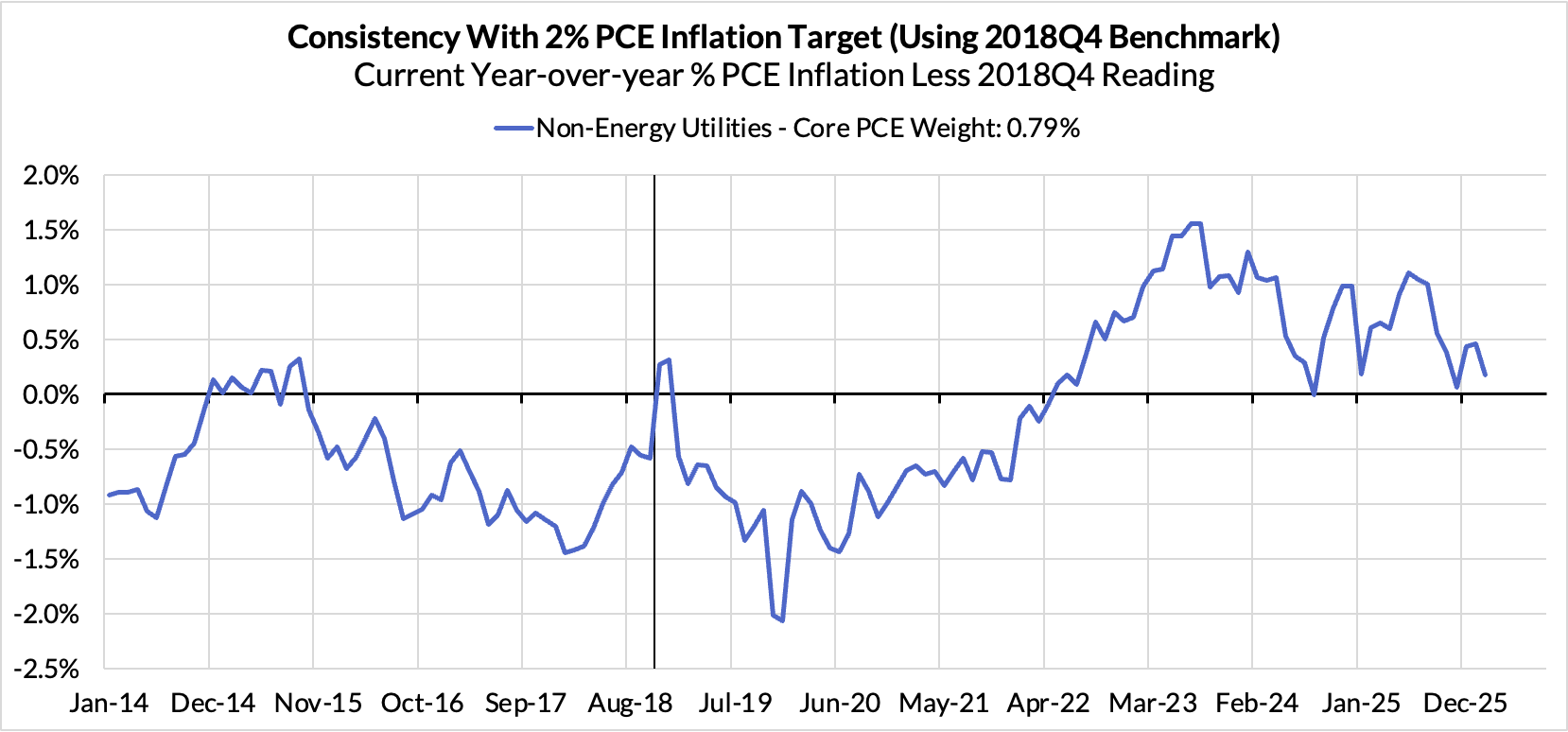

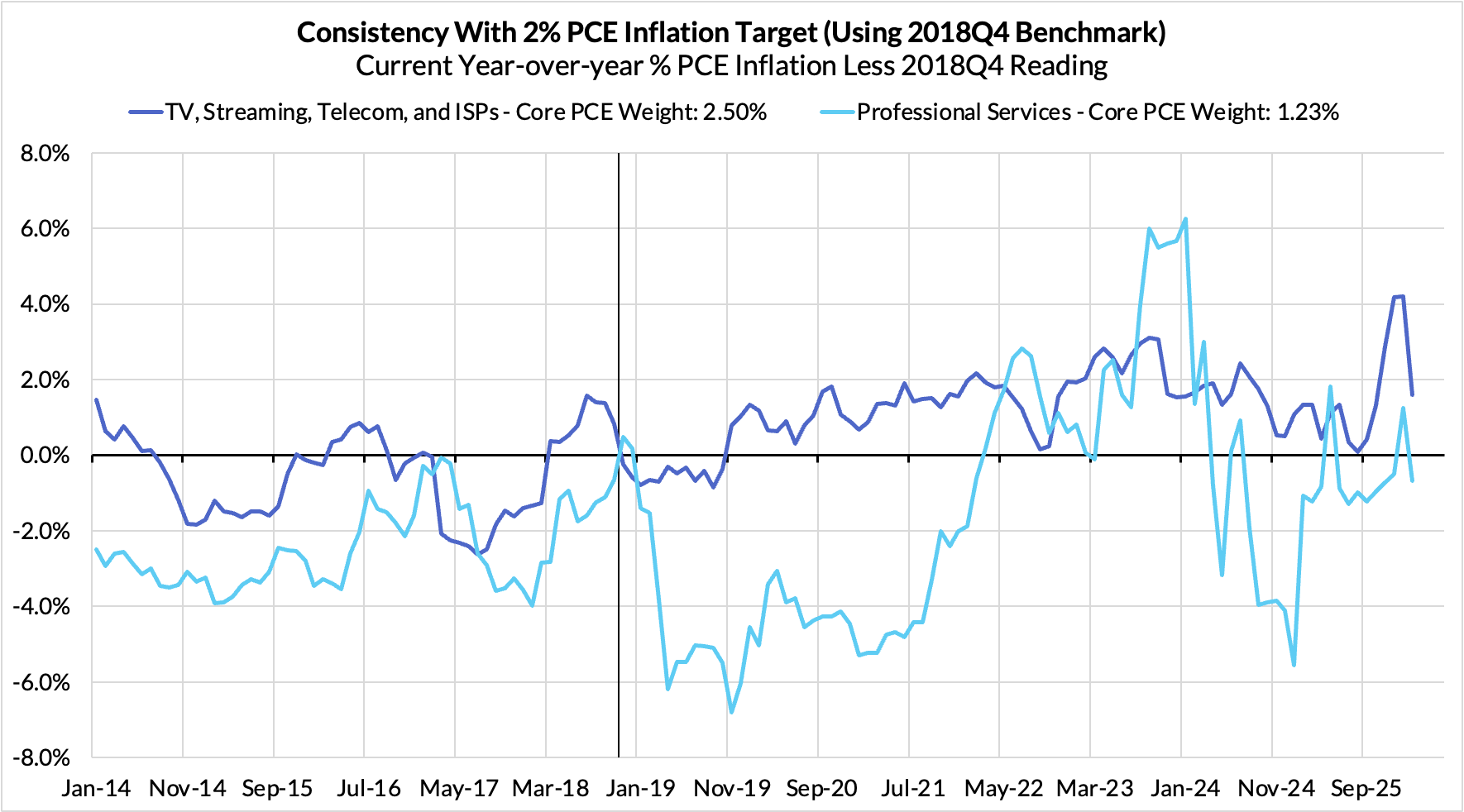

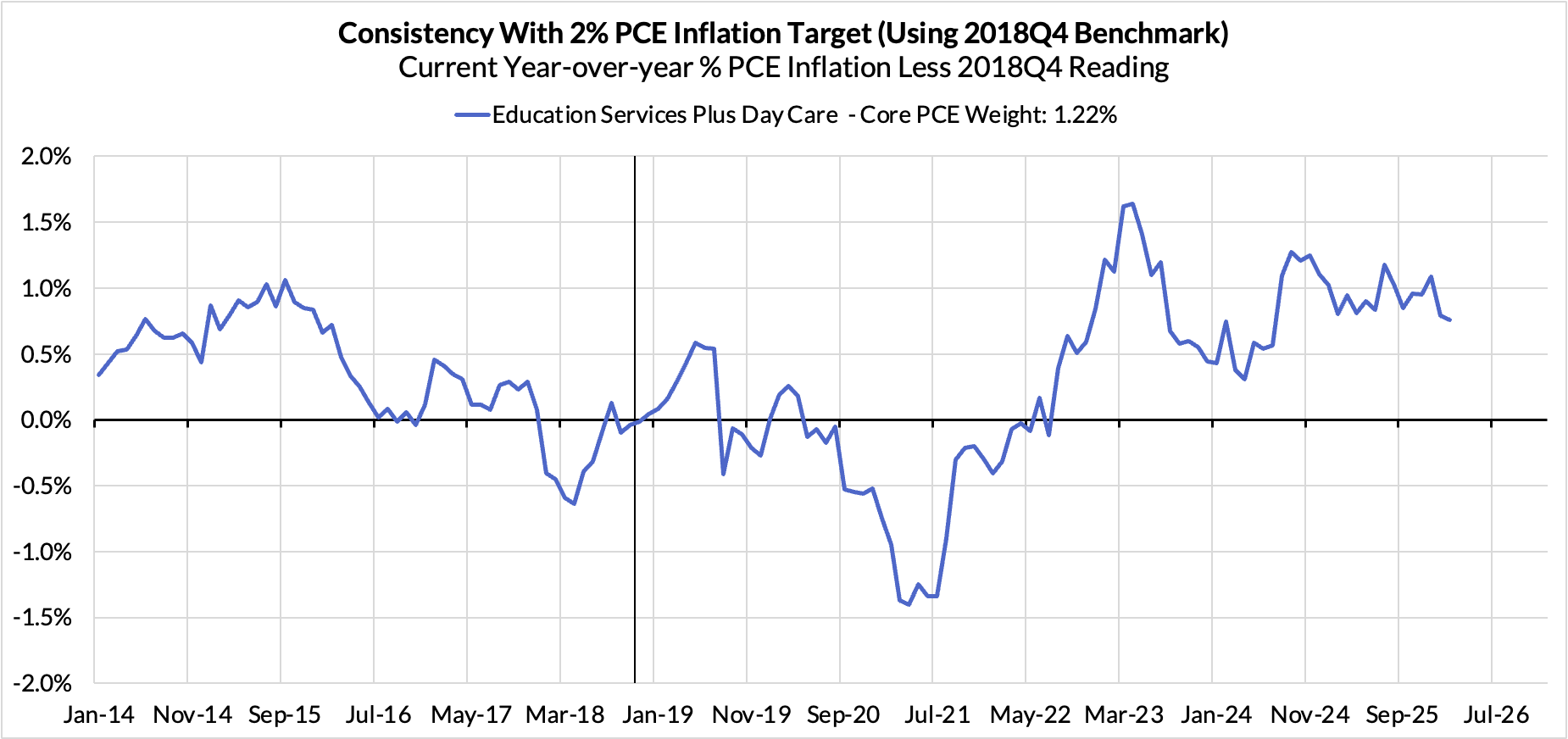

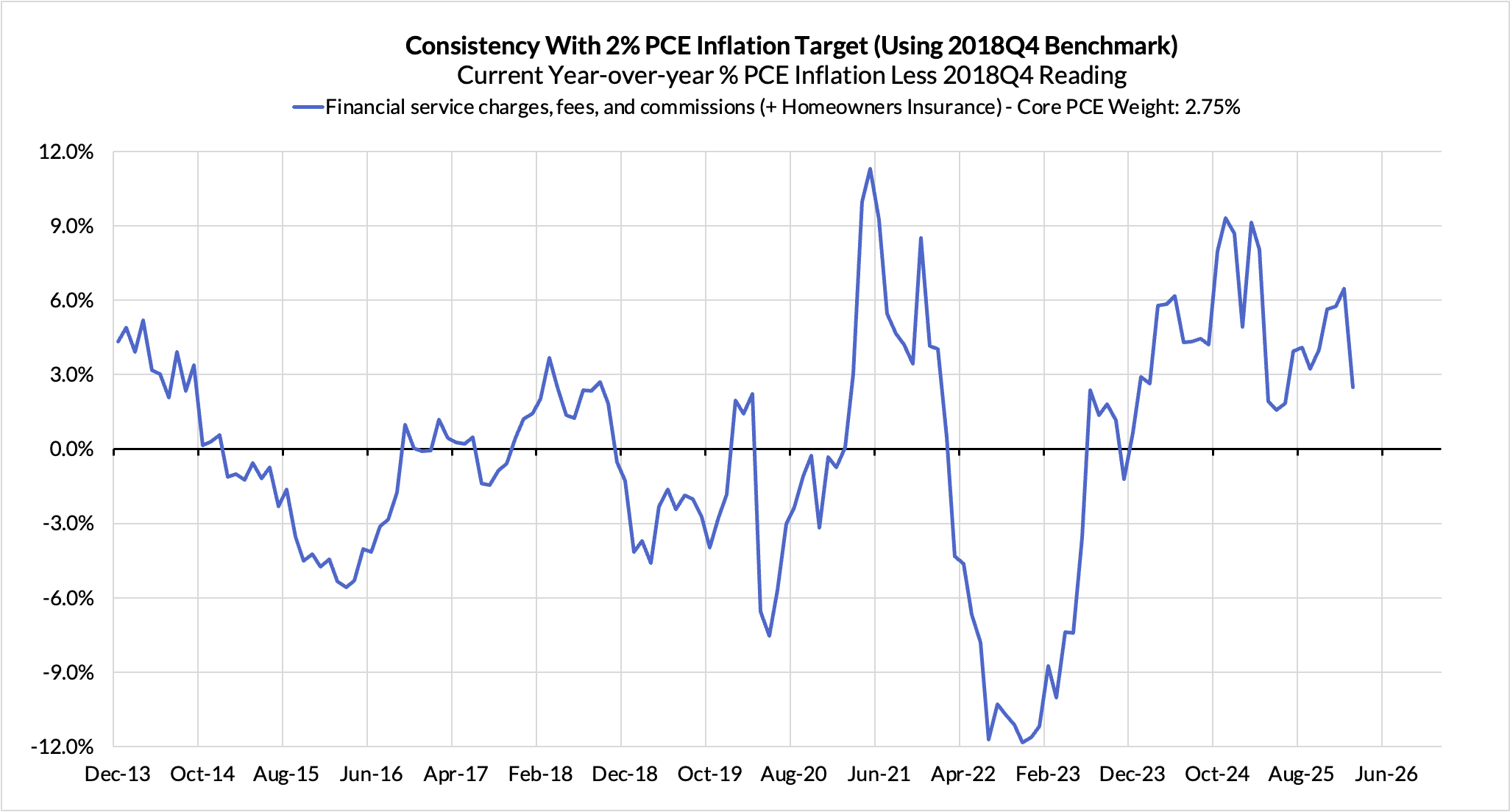

Inflation Overshoots At The Component Level

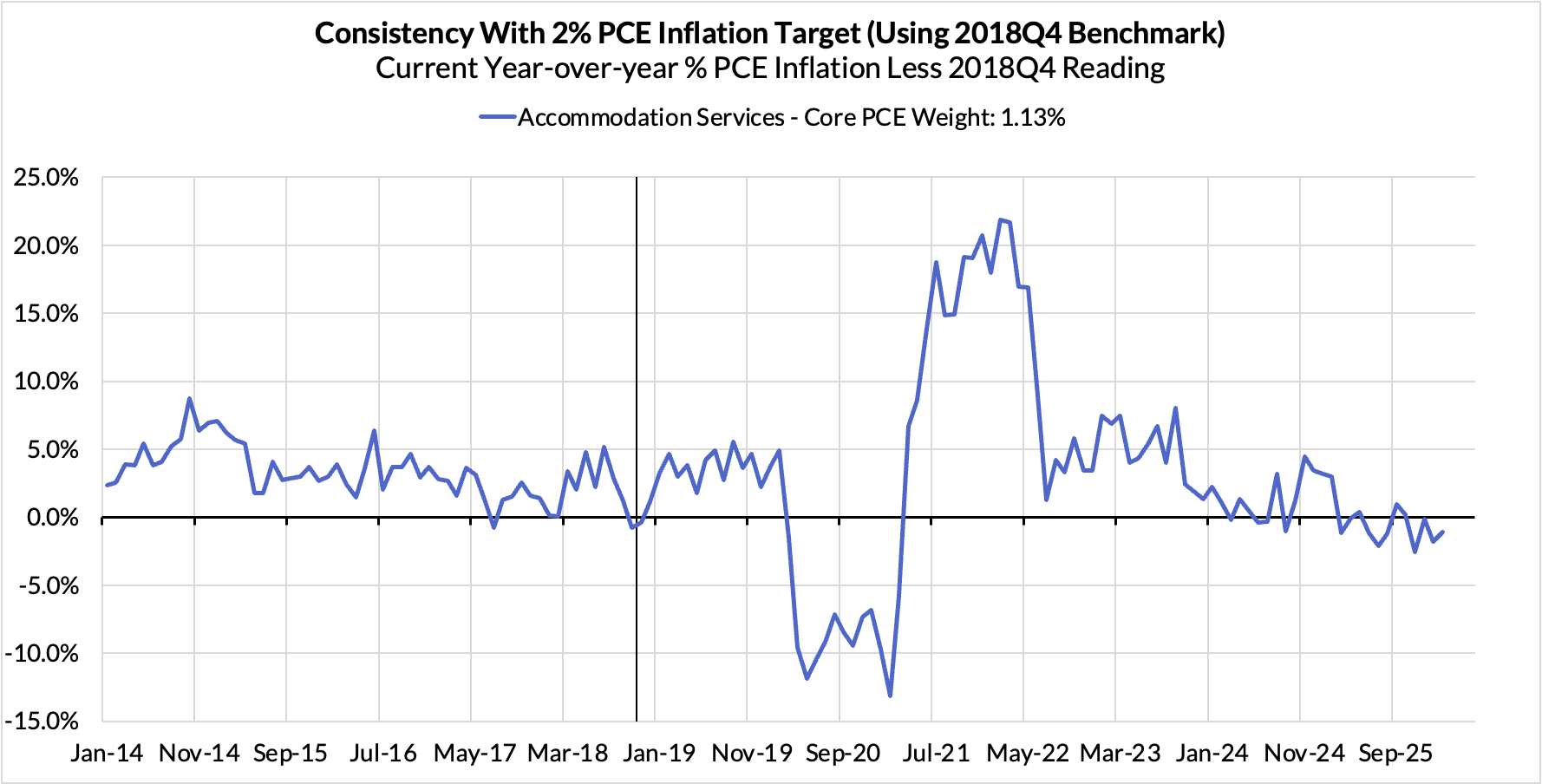

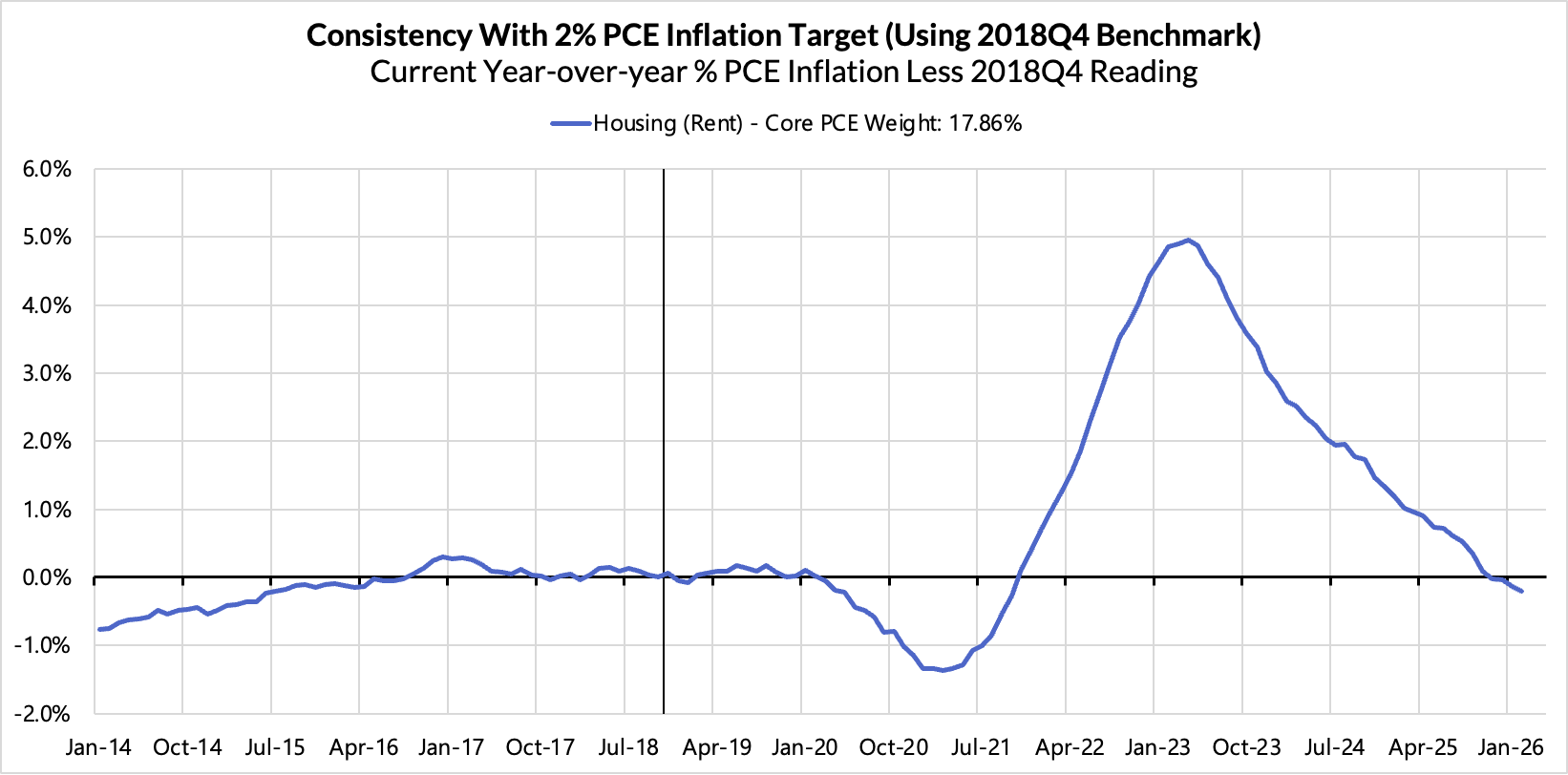

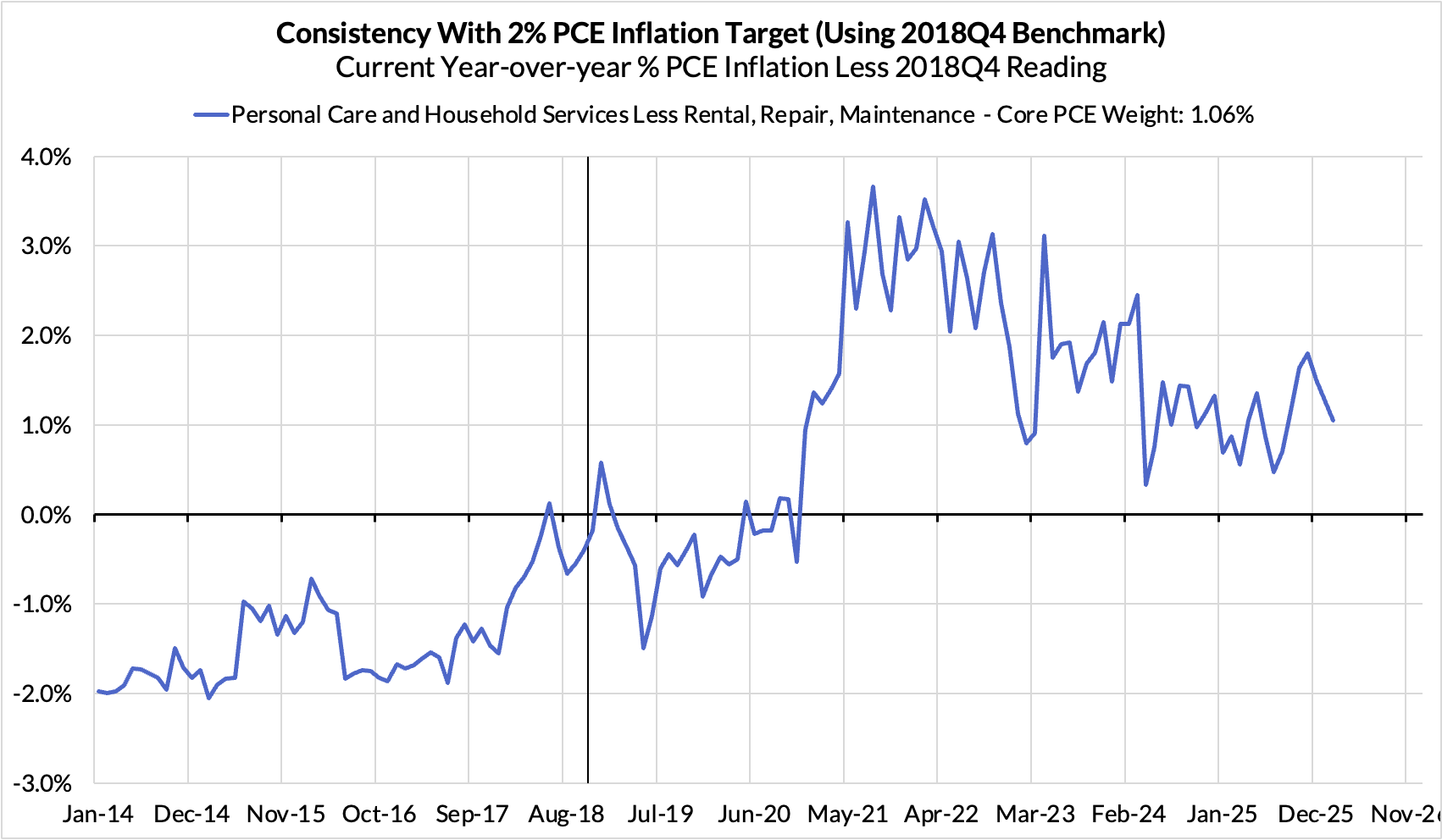

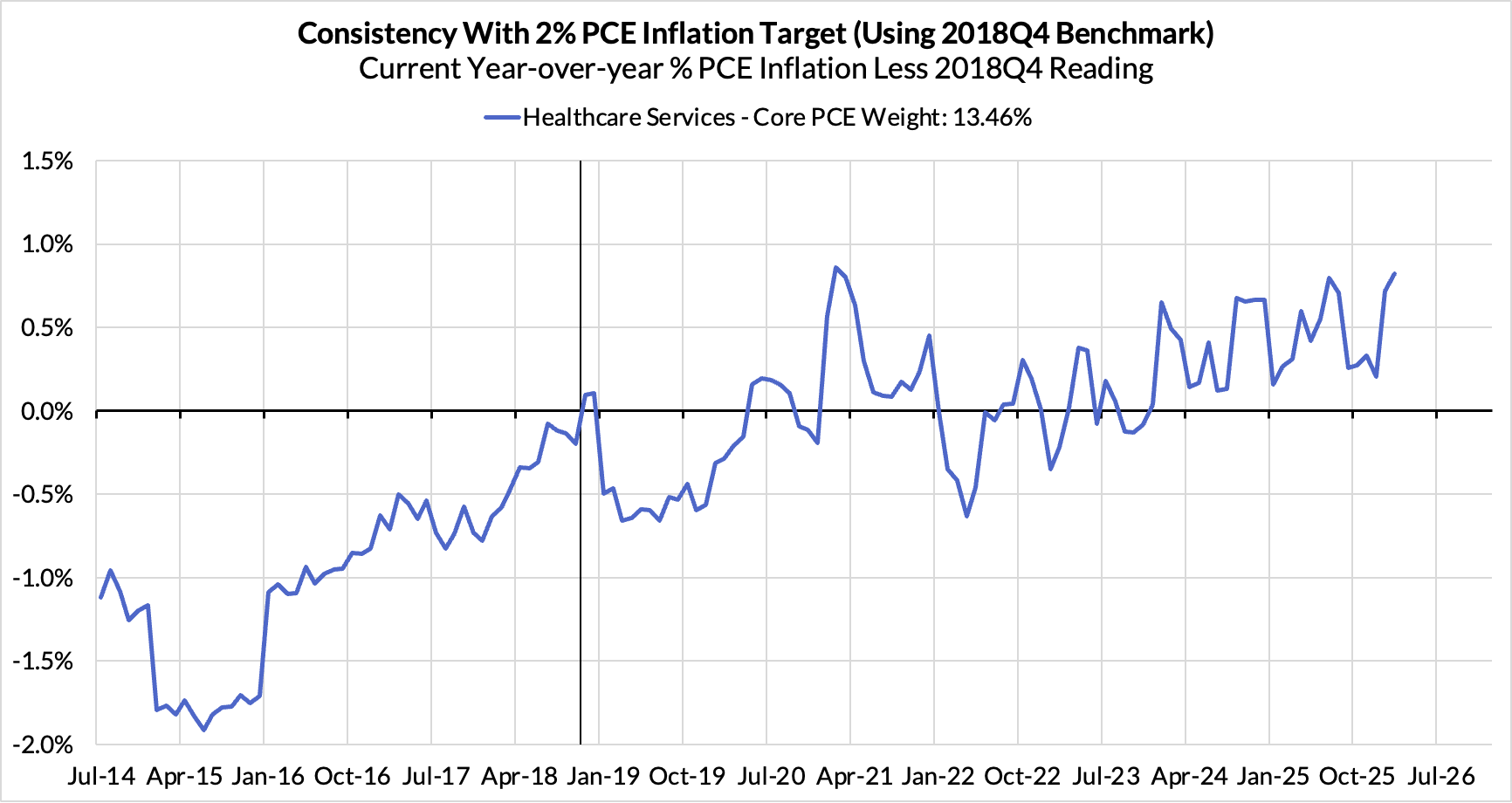

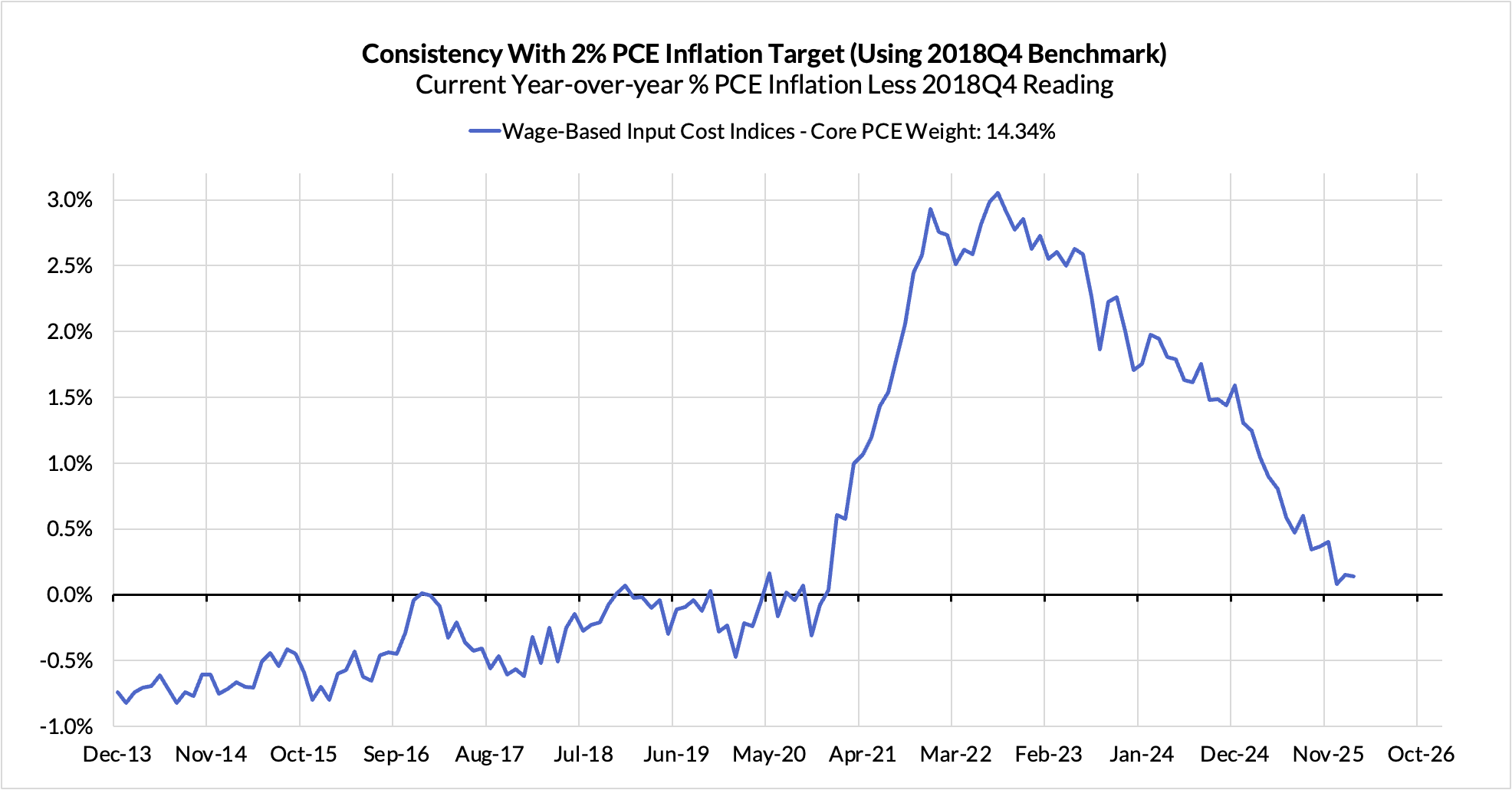

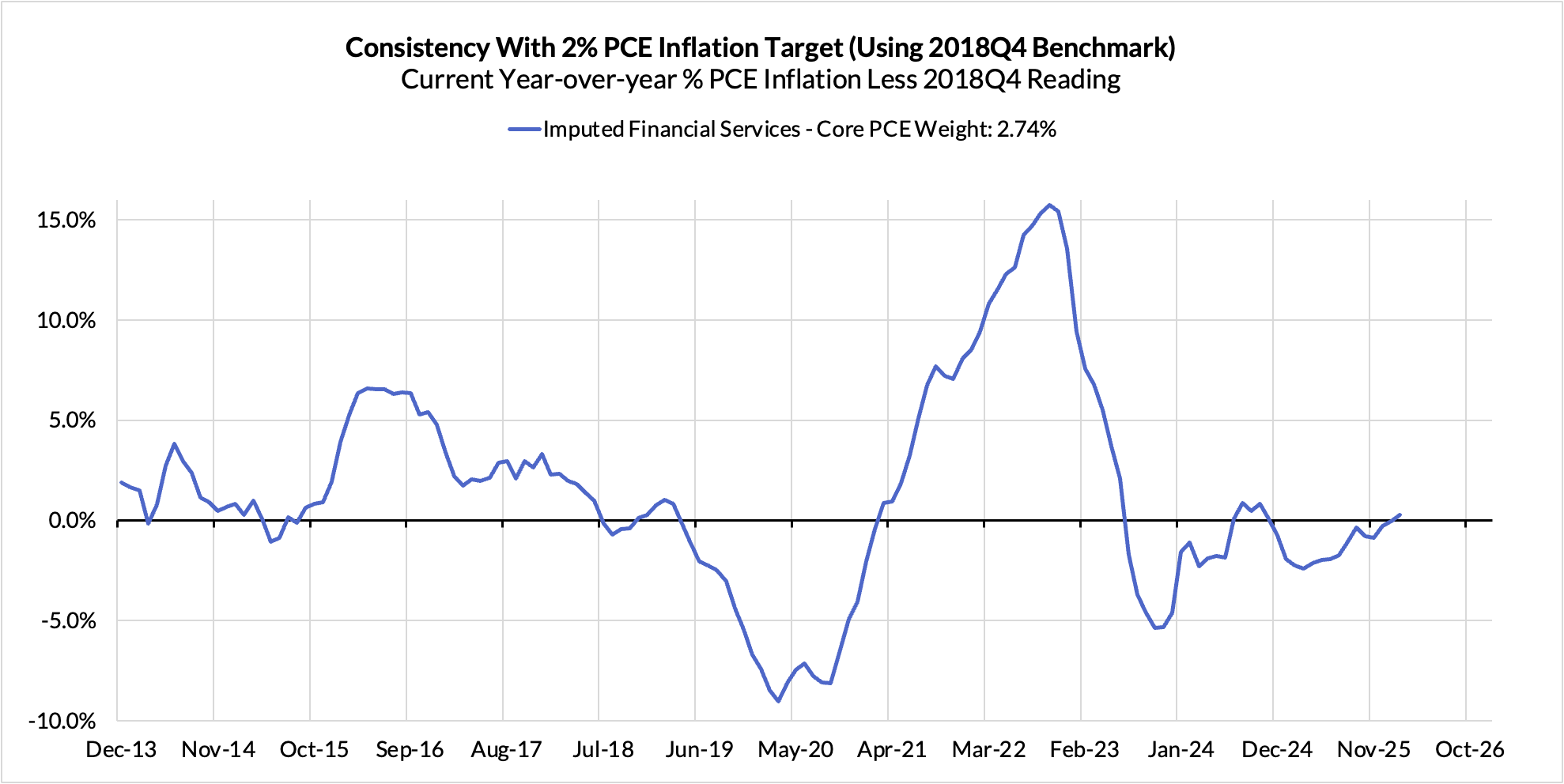

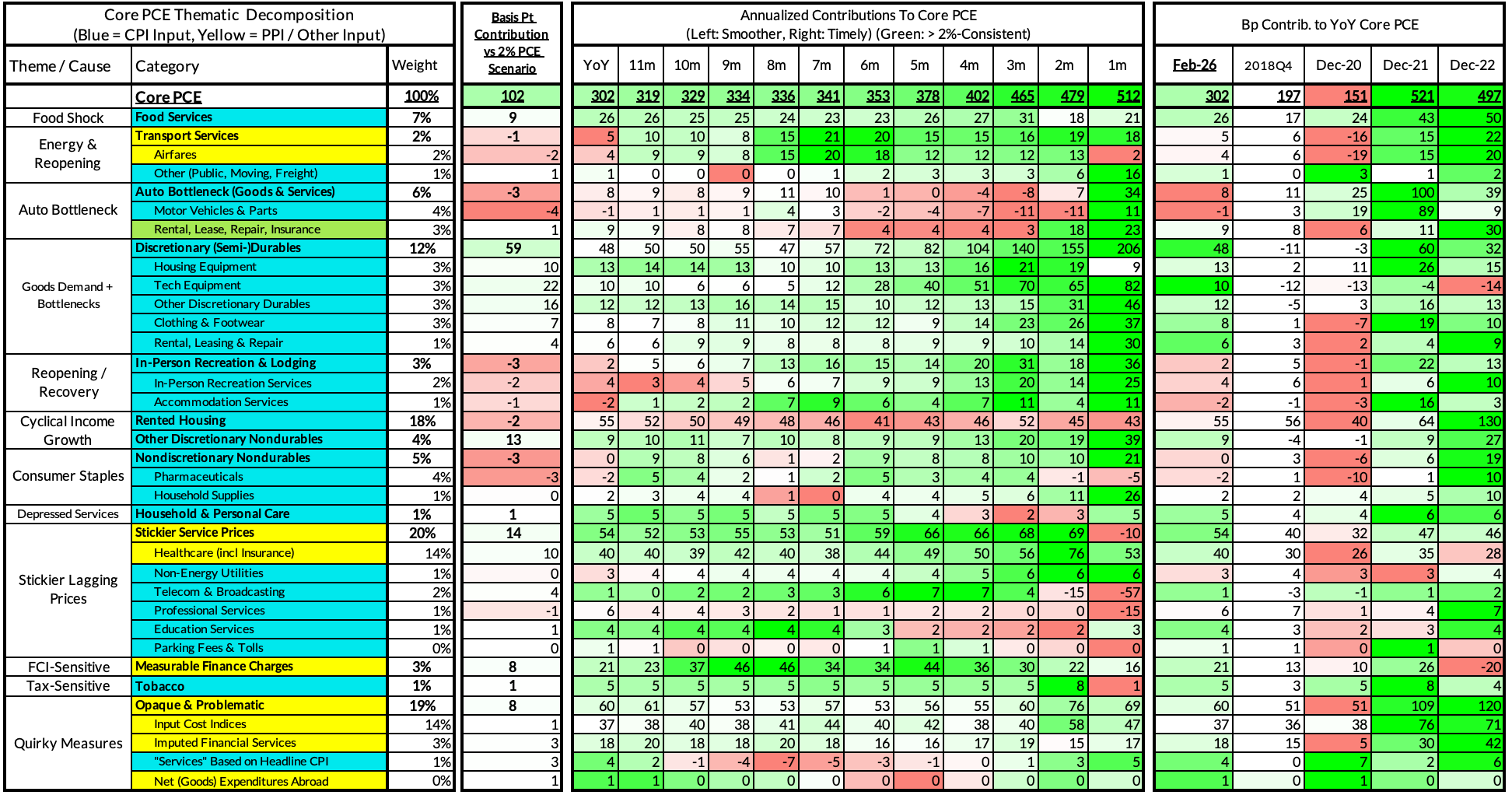

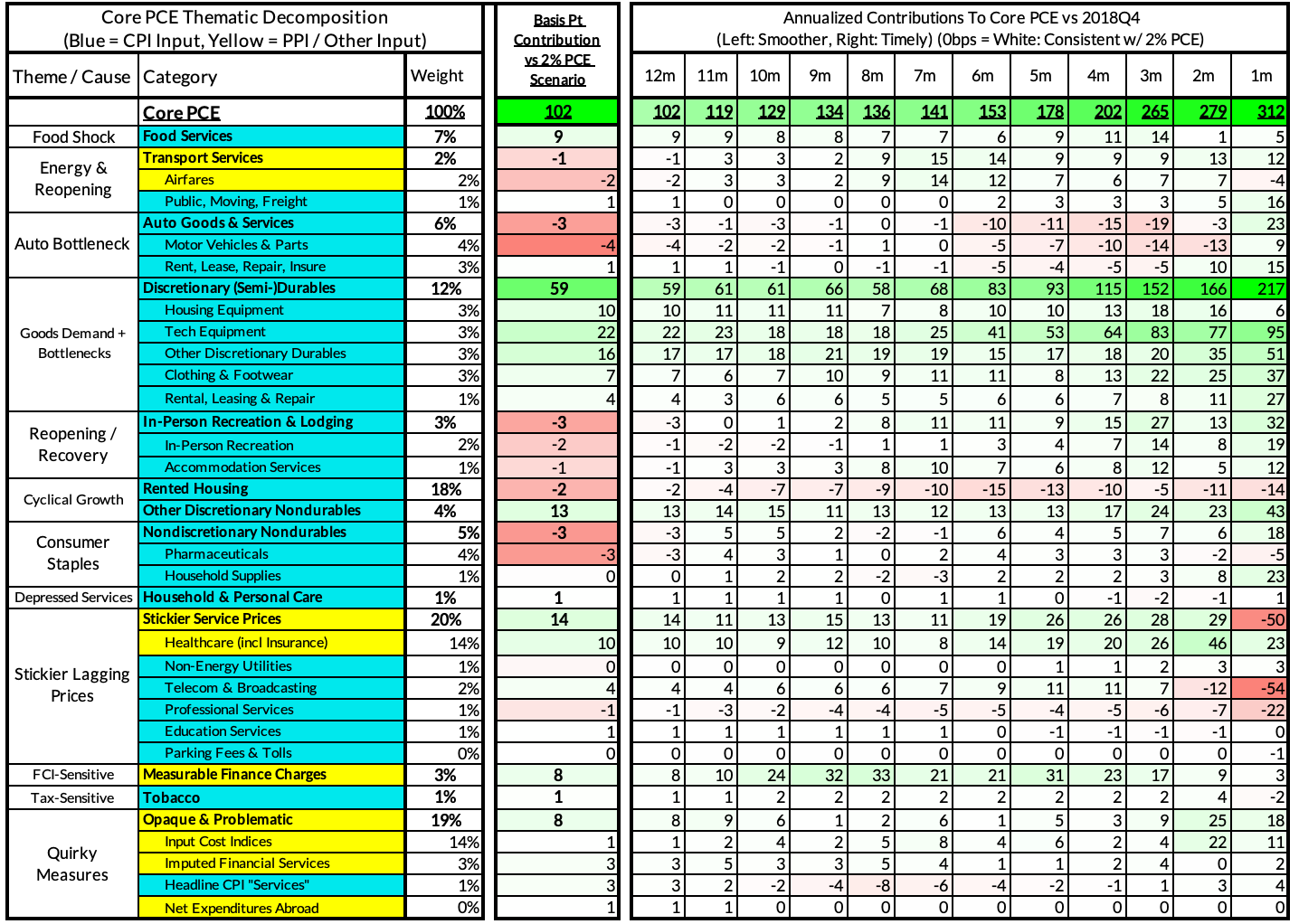

For the Detail-Oriented: Core PCE Heatmaps

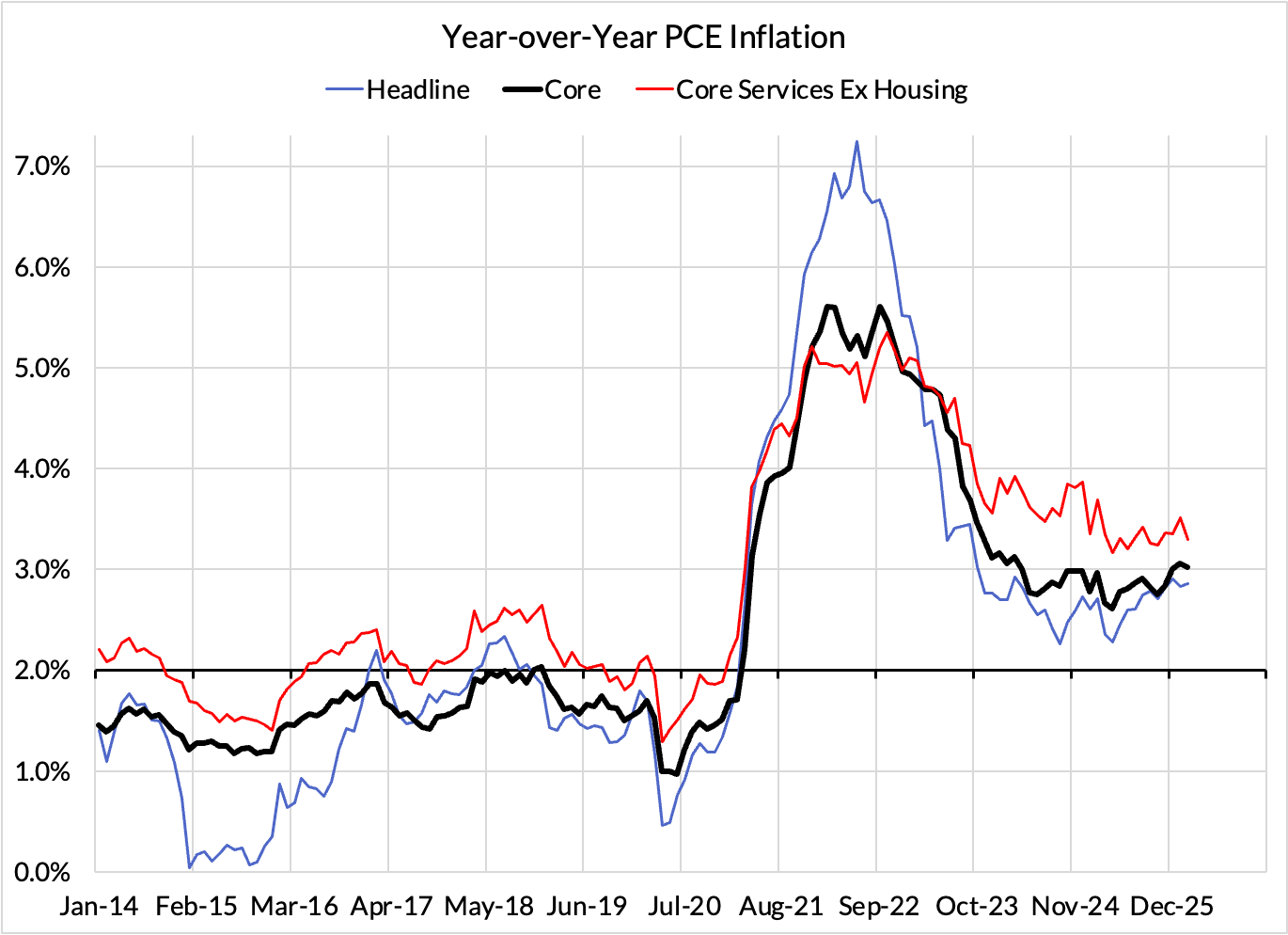

Right now Core PCE (PCE less food products and energy) is on track to run at a 3.02% year-over-year pace as of February, 102 basis points above the Fed's 2% inflation target for PCE.

Equity market effects are adding 8 basis points to the overshoot.

Food inputs likely adding 9 basis points to the overshoot.

Telecommunications and broadcasting are adding 4 basis points.

Healthcare services are adding 10 basis points.

The final heatmap below gives you a sense of the overshoot on shorter annualized run-rates. February monthly annualized Core PCE is on track to run at a 5.12% annualized pace, a 312 basis point overshoot vs 2% target inflation. These estimates are subject to some revision as more data gets released (PPI, IPI, GDP, PCE).

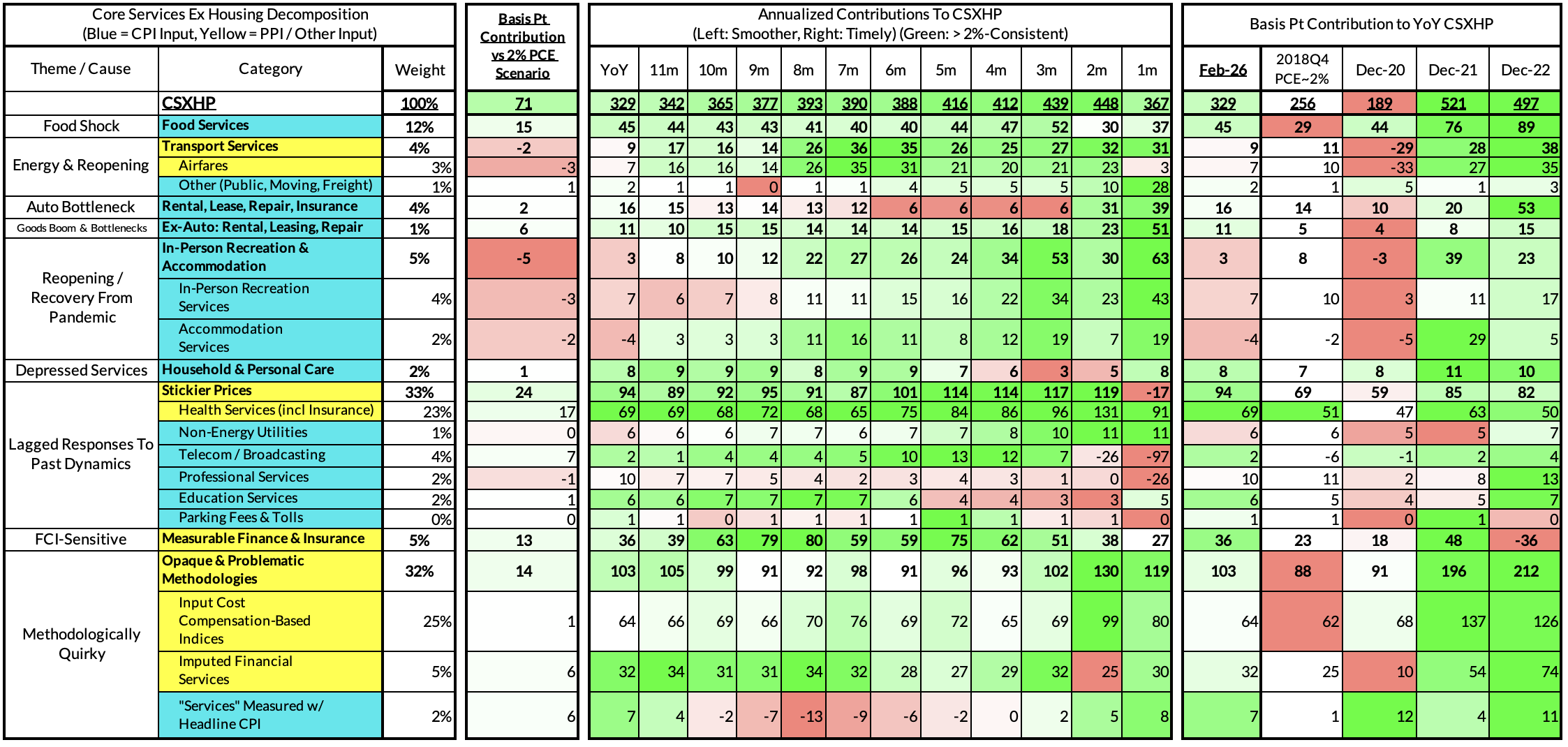

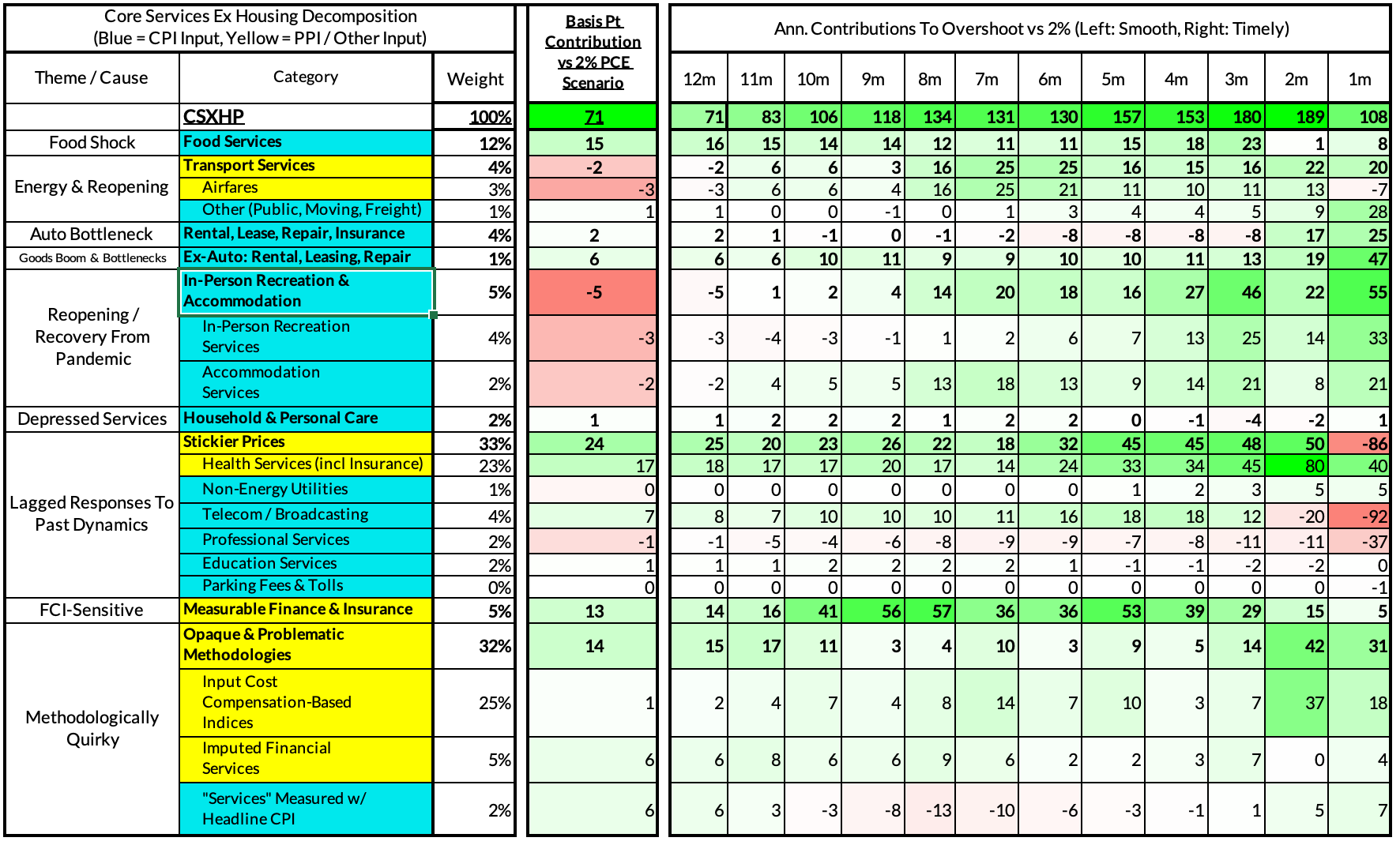

For the Detail-Oriented: Core Services Ex Housing PCE Heatmaps

The February growth rate in "Core Services Ex Housing" ('Supercore') PCE is on track to run at a 3.29% year-over-year pace, a 71 basis point overshoot versus the ~2.59% run rate that coincided with ~2% Headline and Core PCE inflation.

The February monthly supercore is on track to run at a 3.67% annualized rate, a 108 basis point annualized overshoot of what would be consistent with 2% Headline and Core PCE. These estimates are subject to revision as more data gets released (PPI, IPI, GDP, PCE).

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.