Summary

The Fed’s framework review and forward guidance from this past fall showed an encouraging willingness to center labor market outcomes over inflation in evaluating interest rate policy. However, the Fed has only partially clarified how they will evaluate real-time inflationary dynamics within their new flexible average inflation targeting regime. The end of the pandemic, alongside substantial stimulus spending, has created an environment where some commentators and policymakers are preemptively worried about inflation, much as they were in 2009 after the Great Financial Crisis. We present three possible scenarios to consider, when thinking about the path that interest rate policy should take through the end of the pandemic and beginning of the recovery.

The most important takeaway is that it is critical to distinguish between transitory and persistent inflation when thinking about interest rate policy, and that it should be the growth in wage incomes that drives the assessment of persistent inflationary dynamics. As the pandemic ends, the shift in consumption baskets is liable to create some one-off inflation, especially as capacity comes back online. If this inflation does not to show up in wage incomes, there would be far less reason for the Fed to respond.

Three Scenarios

The Fed’s framework review and forward guidance from this past fall showed an encouraging willingness to focus on labor market outcomes rather than inflation alone. Rather than previous efforts at forward guidance which guaranteed low rates until either inflation or employment rose, the most recent guidance ensures low rates until both inflation and employment rise sufficiently.

The Committee …expects it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.

Chair Jerome Powell took pains at the most recent FOMC press conference to emphasize that this guidance will not be changing anytime soon, indicating that low rates will continue until the labor market improves. Similarly, Lael Brainard’s most recent speech makes the case for the Fed to focus on eliminating “shortfalls from maximum employment,” rather than minimizing “deviations from maximum employment in either direction.” Vice Chair Clarida also, in a recent speech, took care to point out that even after the current labor market dislocation has passed, the Fed will not raise rates simply “because the unemployment rate has fallen below any particular econometric estimate of its long-run natural level.” On the whole, recent Fed communications make clear that the Fed is not interested in raising rates until the labor market broadly returns to pre-pandemic conditions at a minimum.

However, the maximum employment emphasis within the Fed’s framework review and forward guidance will be tested, both by market participants’ anticipations and by dissenting voices within the Federal Open Market Committee (FOMC). In response to the COVID-19 pandemic, Congress has passed two of the largest fiscal packages ever, and looks primed to pass a third. President Biden has promised to issue another round of stimulus checks while also extending enhanced unemployment insurance provisions from prior relief bills.

Despite the widespread business closures and the massive hit to GDP and employment, many market participants and political commentators rely on the simple expectation that the increase in government spending will necessarily lead to inflation.

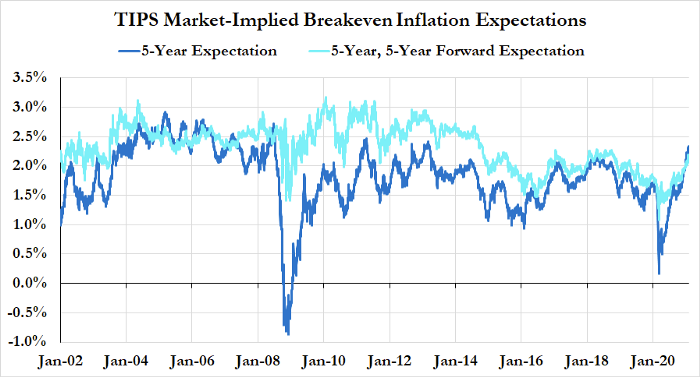

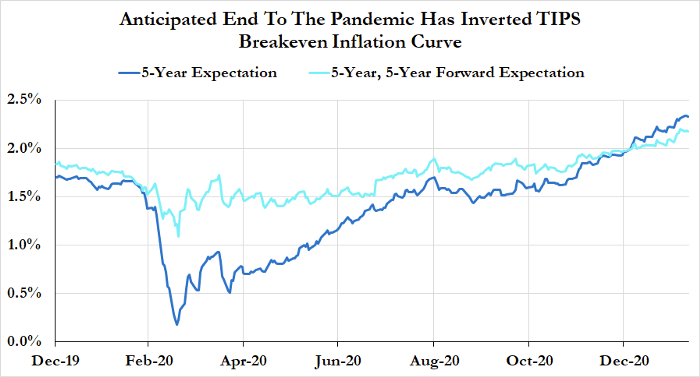

While longer run market-implied inflation expectations are indeed rising, market participants see upward price pressures being more front-loaded.

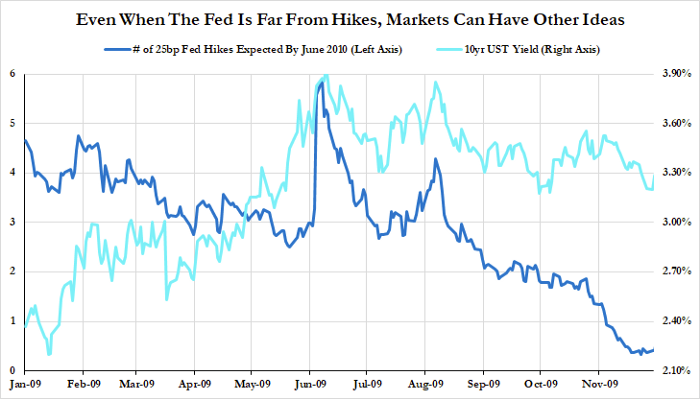

Even when the Fed has tried to communicate a dovish path for interest rate policy, markets often misinterpreted the Fed’s reaction function and reflected tighter financial conditions as a result.

With all of that said, as the pandemic winds down and vaccinations roll out, there are three scenarios which the Fed should consider when thinking about the influence of inflation on interest rate policy. While inflation anxieties have been largely muted by the scale of economic disruption, there remains a nontrivial chance that we see some price acceleration as public health conditions normalize. What will prove critical in the months ahead is the ability to look through transitory inflation to focus on measures of labor market strength.

Scenario 1: Neither Transitory nor Persistent Inflation

The first scenario is the easiest to understand. It is possible that businesses scale up capacity at the same pace as demand rises once the pandemic ends. In this situation, there is no inflation to worry about, and the Fed remains accommodative while workers return to their jobs. Employment steadily rises as vaccines roll out, and the economy moves smoothly into recovery. There is no pressure from commentators or politicians to hike rates, as there is no inflation to point to. The Fed’s goal in this scenario would be straightforward: do everything it can to ensure that the recovery is as fast as possible.

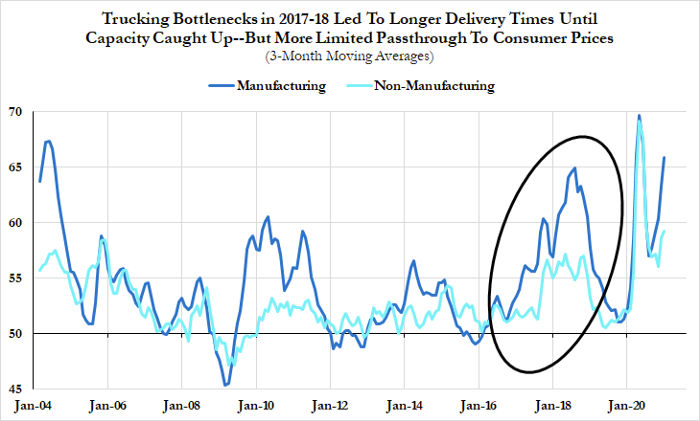

However, this may not be the most likely scenario. Social life returning to normal is likely to entail substantial sectoral shifts with long and variable lags throughout the entire economy, and that might be markedly different by geography. These may even have knock-on effects higher up the supply chain, with temporary bottlenecks expressing themselves in ways other than higher prices. Vendor lead times and delivery times might grow longer, and firms may even engage in outright quantity rationing.

This brings us to our second scenario, one in which the sectoral rotation accompanying the end of the pandemic brings on a bout of transitory inflation.

Scenario 2: Transitory Inflation, No Persistent Inflation

Early on in the pandemic, optimistic commentators frequently made reference to “pent-up demand,” the idea that the pandemic forced a significant increase in aggregate savings rates, and that when it ends, consumers will be looking to spend those unintended savings. Predictions of a “V-shaped recovery” were often predicated on this dynamic. While consumer spending did take some hits after CARES Act facilities expired, it has remained reasonably strong throughout the pandemic, especially among higher-income consumers who have seen relatively less employment disruption.

What seems much more likely is extreme pent-up demand for certain kinds of services. Many are tired of being locked inside and may take the end of the pandemic as an occasion to spend on leisure and hospitality in ways they were not otherwise able or willing to. This may create inflationary pressures in selected sectors, as a huge number of very small and fine-grained capacity bottlenecks are hit by a sudden and substantial increase in demand for travel, hospitality, and related consumption. If demand increases more quickly than capacity can return, prices may rise, and we may soon see significant one-off increases in PCE components related to this consumption.

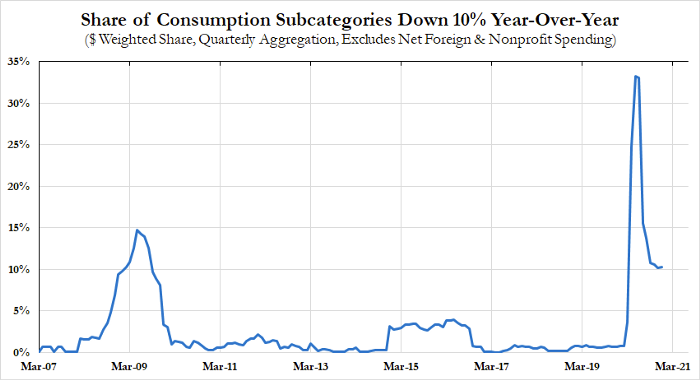

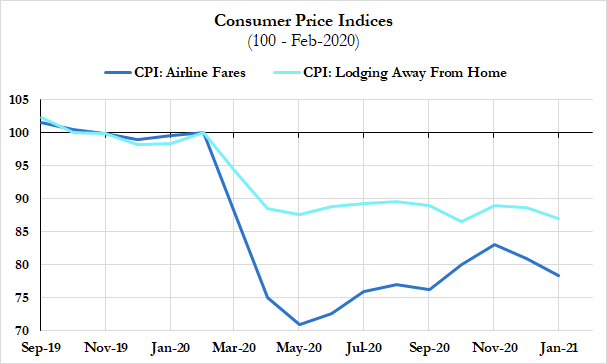

For policymakers, temporary price increases should not be the dominant factor in how they chart out the course for interest rates. As shown above, sectors vulnerable to substantial post-pandemic consumption shifts represent less than a quarter of the total PCE inflation component weights.

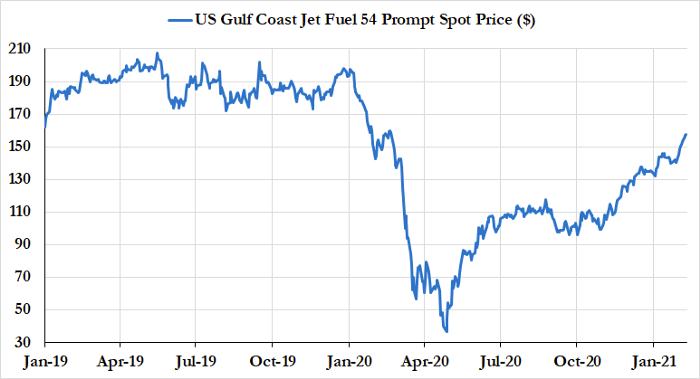

It may be good, for example, for hotels to get some pricing power back to make up for margins effectively lost during pandemic. Rotation within supply chains will also take time, as jet fuel prices are now starting to rise again to meet an expected surge in the demand for air travel.

These sectors required an ad hoc mix of low-interest loans and grants to make it through the pandemic. If they make up for lost margins by using price rationing as they bring capacity back online, it’s hard to see that as an unmanageable inflationary outcome over the longer run.

Depending on how far the impacts of this new spending move up the supply chain, we may see price increases in sectors traditionally associated with more persistent inflation. However, this will likely only be for a short period. Inflation from short term capacity constraints is something of a common occurrence, even in the teeth of recessions. It indicates little about the health of the overall economy, and next to nothing about the state of the labor market.

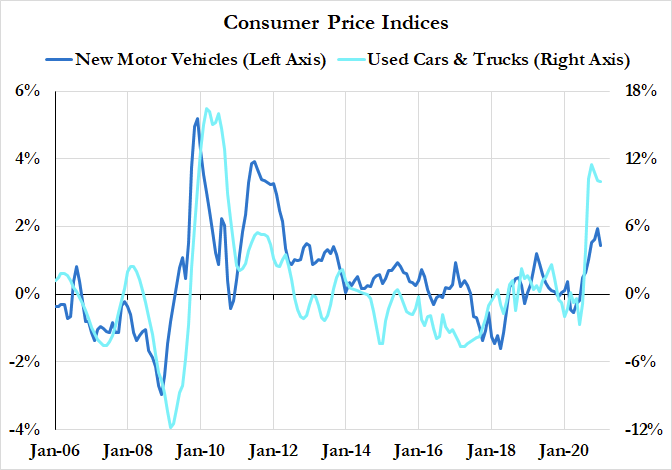

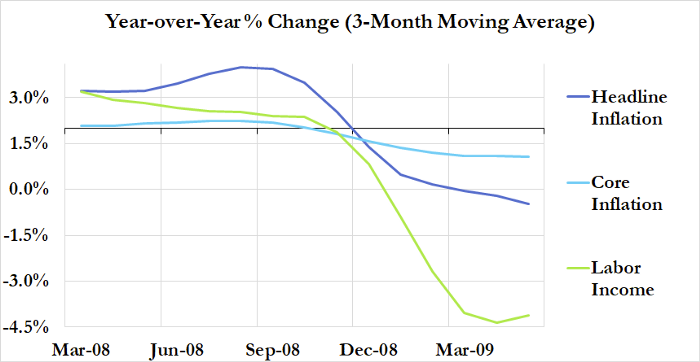

To illustrate, consider the one-off inflation in new and used cars following the Great Financial Crisis. The Cash for Clunkers program incentivized the purchase of new cars, while the precipitous fall in interest rates incentivized the purchase of new and used cars alike. After about a year of inflation, prices leveled off as capacity adjusted to a new level of purchasing. At no point did this dynamic have a useful signal to offer about labor markets or future inflation. This is yet another example of why it’s useful to break out inflation by component to make sure not to act on transitory, unrelated movements.

If, following the end of the pandemic, services come online more slowly than demand increases, there is likely to be some price increase in services and upstream sectors, enough to move the aggregate inflation data.

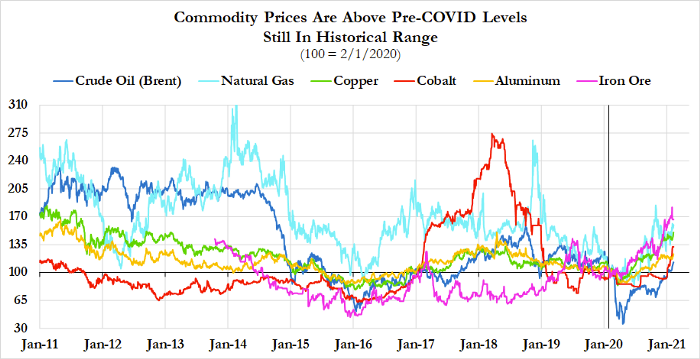

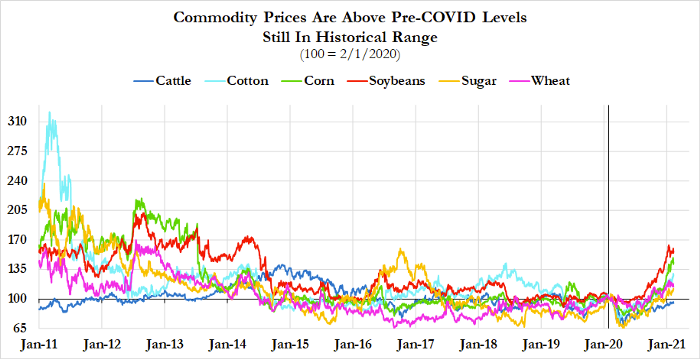

The price of commodities have broadly increased over recent months.

We know that increases in the price of basic commodities may lead to inflation in finished goods. Oil, a commodity at the beginning of many supply chains, exhibited this dynamic quite pointedly in the 1970s. Firms facing a sudden increase in intermediate goods passed this price increase on to consumers, and the result was price increases in seemingly unrelated PCE components.

However, without an attendant increase in wages, all of this inflation represents a transitory form of price rationing as capacity expands to meet current demand, rather than a persistent, reflexive pattern of price acceleration.

Without wages accelerating proportionally, real income actually declines throughout that period of inflation, curtailing purchasing power and slowing real demand for consumer goods and services. It is hard to argue that the economy is in an inflationary feedback loop due to a relative price change that causes real household incomes to fall.

Scenario 3: Persistent Inflation

Which brings us to our last scenario, one in which the effects of a sharp takeup in labor, coupled with historically strong household balance sheets, pave the way for more persistent inflationary pressures. This situation is the proper object of inflation anxiety: that increased financial well-being will lead to excessive household consumption in a manner that creates a positive feedback loop on wages and unit costs. In the past, this anxiety has been used to justify or suggest preemptive rate hikes shortly after the beginning of an economic recovery. Today’s labor markets can’t afford any policy missteps. What is most important about this scenario — and which seems highly unlikely given the degree and composition of labor market damage — is how to distinguish persistent inflation from transitory inflation. The ability to do this will be key to preventing Fed policy missteps.

In order to bring about maximum employment consistent with the Fed’s statutory mandate, it is critical that the Fed be able to discriminate between the second and third scenario above. Prematurely hiking will slow expansion and threaten to create another “jobless recovery,” something the country can ill-afford. Luckily, there exist clear indicators that can help differentiate between persistent and transitory inflation.

Disentangling Transitory From Persistent Inflation

In the benchmark models that the Fed relies on, accelerating inflation comes from labor demand outstripping labor supply such that workers are able to successfully and successively demand wage increases that match or outstrip increases in consumer prices. The central idea behind this model is that tight labor markets are — after some particular threshold for labor market tightness is crossed — inherently inflationary. This dynamic is most succinctly described by the Phillips Curve, which intends to show a tradeoff between inflation and unemployment.

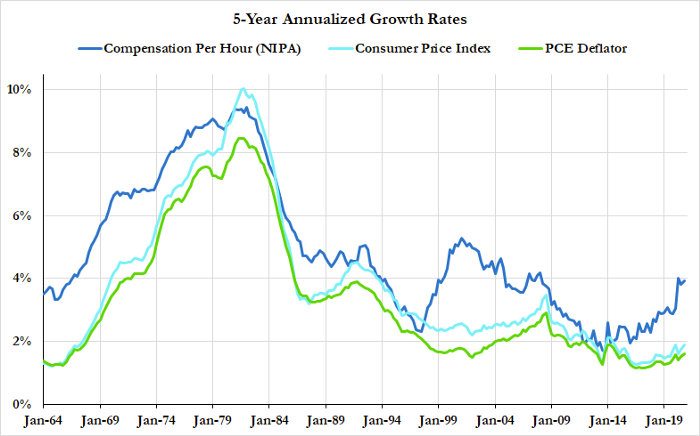

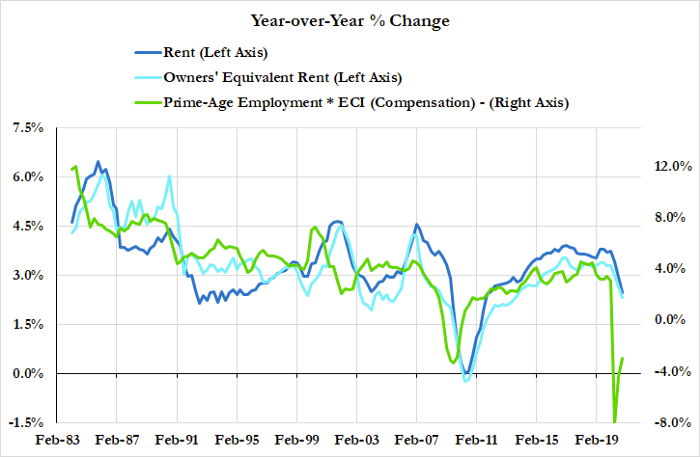

FRB/US, still the main macroeconomic model in use at the Federal Reserve, utilizes a particular specification of a New Keynesian Phillips Curve (NKPC) which relates Core PCE inflation to Employment Cost Index (ECI) hourly compensation. Higher inflation is presumed to be correlated to higher ECI hourly compensation, while compensation is expected to fall with inflation. Though a number of Fed governors — especially Chair Powell — emphasize that the Phillips Curve has become nearly flat of late, and the current specification takes into account expectations and relative price shocks, the mechanism within the model remains fundamentally driven by labor market slack and its effect on wage growth.

In this model, when labor markets are slack, there is minimal pressure to increase wages. Bargaining power remains with employers rather than employees. However, if labor markets tighten, employers will have to compete on wages to attract new workers, pushing up compensation and unit labor costs. If employers are unwilling to sacrifice profit margins, they raise prices to match the increase in unit costs, inaugurating an inflationary cycle. Since labor markets remain tight, and this tightness is the source of the bargaining power that led to wage increases, there’s supposedly nothing to stop labor from demanding at least equivalent wage increases in subsequent periods and continuing the cycle. This inflation in the production and purchasing of consumer goods then goes on to have negative effects on all kinds of unrelated economic processes that inflation hawks abhor.

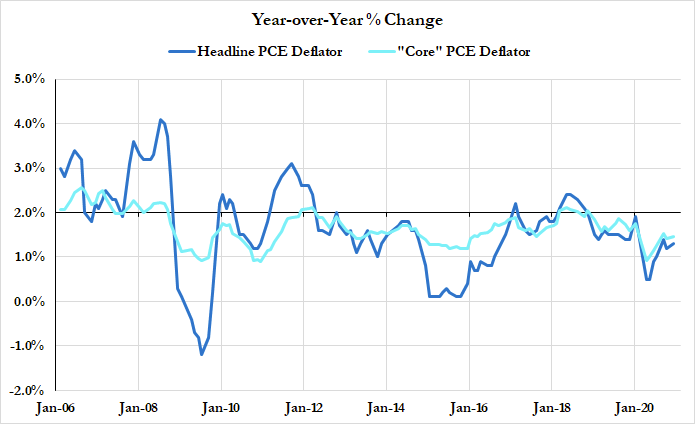

However, for inflation to be persistent and durable within this model, it is critical for both aspects — increases in wages and prices — to show up in the data. If wages are rising but prices are not, this represents a straightforward increase in real income for labor. Vice Chair Clarida is on record in a number of places commending recent increases in the labor share of output. Keep in mind also that the data we observe for prices often embeds quality improvements. While sticker prices consumers observe may be increasing, the quality-adjusted prices that the BLS publishes tend to show more disinflation. An increase in real income for labor straightforwardly indicates that slack capacity in the economy is finding productive work.

If, on the other hand, prices are rising but wages are not, this represents a straightforward decrease in real income for labor. Prices rising without costs rising increases margins somewhere in the economy, and so real wages fall. Inflation accompanied by falling real wages will quickly burn out and resolve to a simple change in relative prices. 2008 provides the prima facie example of how inflation acceleration cannot sustain itself if incomes continue to deteriorate.

With all this in mind, it should be uncontroversial to say that the core indicators to look at when deciding if observed inflation is transitory or persistent are mainly wage measurements. Chair Powell made this point quite succinctly during the most recent FOMC press conference, saying that the Fed will wait until changes show up in the “data, and not just the outlook.”

If one sees increases in the Employment Cost Index (ECI) and other measures of wages alongside an increase in inflation, it’s more likely to be a situation in which growth rates in spending, wages and prices are more durable and therefore justify some proportional interest rate adjustment from the Fed. To be clear, the ECI has not weakened as much as one would have expected over the course of the pandemic. However, if there’s no increase in these measures alongside observed increases in inflation, there is no reason for the Fed to act, especially if labor utilization remains anywhere near as depressed as it has been since the pandemic.

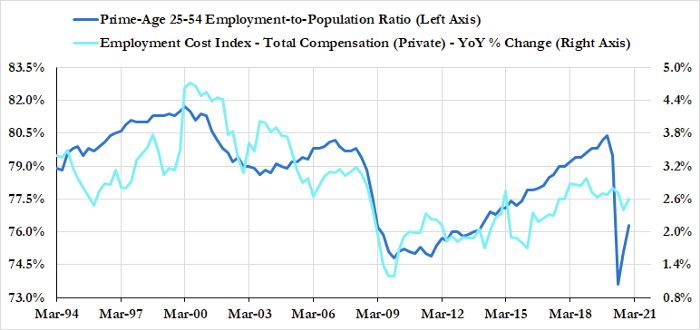

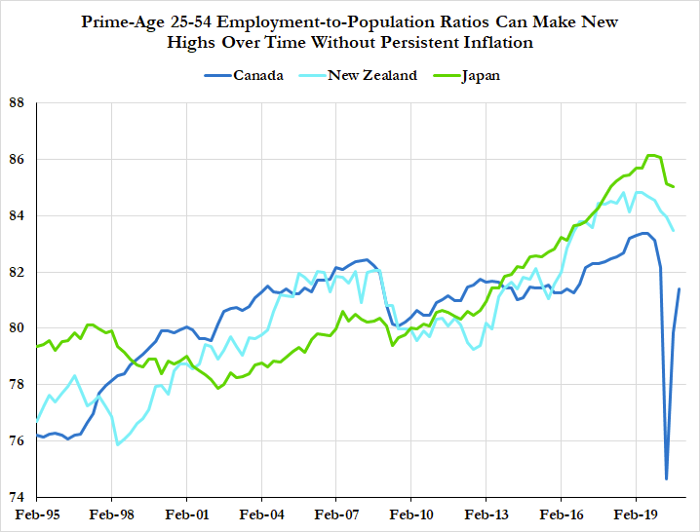

To a lesser extent, and for the purpose of model confirmation, it would also be prudent to look at the prime-age employment to population ratio or Ernie Tedeschi’s “NPOP” as measures of labor market tightness. If your model is that persistent inflation is driven by labor markets that become so tight that workers are able to bargain for wage increases, it helps to make sure that employment levels are high relative to their historical levels.

Even if we do see some persistent signs of inflation, it would be wise for the Fed to disentangle short-term and medium-term estimates of what is achievable in terms of labor utilization. International experience shows us that even as economies might see some coincident price acceleration when labor utilization hits new peaks, such acceleration tends to be temporary and does not preclude the achievement of further, higher peaks.

If we look closely at the relationship between labor utilization and the more cyclical components of inflation, what should be visible is that it is the change in labor utilization that matters, not the outright level of labor utilization.

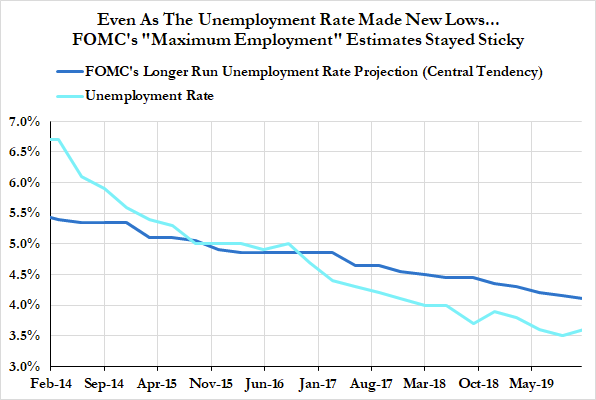

To prudently navigate the constraints posed by its dual mandate, the Fed should provide more clarity in its communications, especially the Summary of Economic Projections. In the post-pandemic environment, it is critical to ensure that estimates of maximum employment are flexible both in terms of timeline and selection of salient indicators for tracking labor market slack and wage growth. ECI and the prime-age employment-to-population ratios deserve to feature at least as prominently than the unemployment rate. Beyond inclusion, the future trajectory of these variables should be subject to more dynamic and generous revision than are usually provided for unemployment rate projections. Traversing these troubled waters will thus require careful, clarifying communication.

Conclusion

The Fed has learned time and again since the Global Financial Crisis that past estimates do not guarantee future levels of full employment. If economic indicators are consistent with transitory rather than persistent inflation, the Fed should shrug off any suggestion that they tighten until labour markets make a full recovery to at least pre-pandemic levels.

While it would be trite to say that the Fed should wait until seeing the whites of inflation’s eyes to hike rates, we would submit instead that they should wait further to make sure that the white they see is in fact an eye, rather than a flare in their lenses. Hiking rates on evidence of transitory inflation would be a clear policy error that helps to stymie labor market expansion and bring on yet another jobless recovery.