"Real Wages" and Aggregation: A Methodological Mess

“Real wages” are often presented as a neutral measure of the ability of households to buy definite quantities of real goods after adjusting for changes in both prices and wages. In reality, "real wages" explain far less about household economic well-being than these stories confidently imply.

“Real wages” are often presented as a neutral measure of the ability of households to buy definite quantities of real goods after adjusting for changes in both prices and wages. As inflation has overshot expectations during the pandemic recovery, some have used this measure to undercut the value of wage gains made by American workers. In reality, "real wages" explain far less about household economic well-being than these stories confidently imply.

The measure compresses distributions of wages and consumption baskets into a measure that reflects purchasing power over a single consumption basket. In practice, an aggregate produced by dividing a stable series by a volatile series will always be dominated by movements in the volatile series. This creates empirical problems for those attempting to use “real wages” as a means to evaluate the financial situation and standard of living across the distribution of household income, wealth and consumption. On the theory side, there are no natural units with which to aggregate “definite quantities of real goods,” and so attempts at developing an aggregate measure of “real wages” which relies on “aggregate quantities of real goods” will be at best partial, and at worst actively misleading.

Higher Consumption, Better Liquidity…Lower Real Wages?

Despite elevated inflation readings, we see higher consumption and better household liquidity in the form of savings and financial surpluses today than we did before the pandemic. From this, you would think that the fiscal response to the pandemic has been an unqualified success. Checks went out across the board, poverty rates fell, and workers have regained some bargaining power lost to decades of decaying unionization. And yet, some are claiming that the standard of living has in fact fallen, because "real" wages are down. If this makes no sense to you, you’re not alone. Unlike consumption and financial balances - for which we have reliable data at the household level - measurements of "real" wages are aggregates derived from other aggregates and so suffer from the aggregation problem, something that even Nobel Prize-winning economists have oftenfailed to grasp. Untangling this economic paradox - that consumption and household liquidity are both up, yet "real wages" are heading down - requires that we investigate how economic aggregates really work.

Macroeconomics, as the study of the economy in aggregate, can’t help but use aggregates in its stories about the world. Working with aggregates is tricky, though, and we have to make sure that the aggregates we use map empirical data onto theoretical concepts in a coherent way. Sometimes a particular aggregate is so intuitively appealing for a given argument that commentators and policymakers ignore how incoherent the methodology that connects data to concept is. Today this errant methodology leads to a very natural question for American workers--how can I be consuming more, and still have money left over to save, if my “real wages” are substantially lower?

As a theoretical concept, “real wages'' are intended to measure how much stuff households can buy with the income they make. Over time, measures of this concept are supposed to signal whether households are getting ahead or falling behind once the whole economic picture is taken into account. However, these measures face some significant challenges, as the goal is to convert a nominal measure - wages in dollars - into a measure of heterogeneous physical goods. Nominal measures have natural units that can be aggregated straightforwardly: dollars. Physical objects - say, used cars, meals at restaurants and cell phone service - each have their own units (a number of cars, the calorie and nutritional content of a meal, some number of packets of information sent at a particular frequency), but don’t have a unit that all three can be aggregated in. Dollars won’t work: what good is saying that $50 buys $50 worth of rice, if $50 worth of rice is fifteen pounds one day and twenty pounds another? We’ll get into the challenges this presents later.

If “real wages” are really falling, households should face a choice between spending more dollars on the same goods as before - sacrificing nominal liquid net worth to maintain real consumption - or consuming fewer goods in order to preserve their net worth. Today, we see strong and growing consumption expenditures alongside improving household balance sheets, and far above-average savings.

Source: Bureau of Economic AnalysisSource: Board of Governors of the Federal Reserve

We can see that - whatever the discourse around rising inequality - all income levels have seen their liquid savings increase. In fact, the increase has been strongest in percentage terms among lower-income Americans, those often considered to be the hardest hit by rising inflation.

Source: JP Morgan Chase Institute

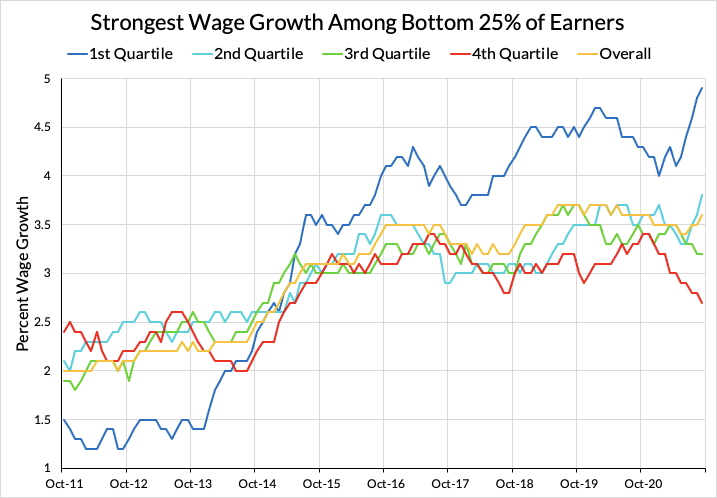

Data from the Atlanta Fed Wage Tracker corroborate this as well: wage growth has been far stronger for the bottom quartile of earners than the top quartile in recent months.

Source: Federal Reserve Bank of Atlanta

If consumers of all income levels are able to save more while simultaneously consuming more, how can it be that, as some have pointed out, measures of “real wages” are indeed falling?

Source: Bureau of Labor Statistics

No matter which aggregate specification you pick - the Employment Cost Index (ECI) deflated by CPI or PCE and Average Hourly Earnings deflated by CPI or PCE - we see aggregate measures of “real wages” are falling.

Source: Bureau of Labor Statistics, Bureau of Economic Analysis

Against stories of rising wages and tightening labor markets and the strongest household balance sheets in years, this doesn’t make sense. The problem is not that households are doing more with less, the problem is the methodology for calculating aggregate “real wages.” All four of the indices of “real wages” above are produced by dividing an index of nominal wages by an index of the price level. Each of those lines - rather than indicating whether households are, in general, able to buy more of what they buy for how much they work - tells us about the movement of two aggregates. These measures show whether the price of one specific basket of goods is moving up or down more quickly than a given measure of aggregate wages. As explained below, this isn’t a theoretically coherent measurement, and that incoherence creates empirical and methodological problems that severely undermine arguments built on measures of aggregate “real wages.”

The Aggregation Problem

The fact that real wages are falling while nominal measures of household well-being are rising is a clear example of the difficulties posed by the “aggregation problem.” As simply as possible, the “aggregation problem” is that well-defined micro-level concepts - where a set of inputs are fed through a function and produce an output - cannot be turned into macro-level concepts by simply aggregating the inputs and feeding them through the same specification of the micro-level function.

Think about this like a factory that receives an order for 1000 cakes. The buyer is expecting 1000 individual cakes, all individually boxed up on a truck. The way to deliver an aggregate of 1000 cakes is to mix each set of ingredients together for each cake, bake them separately, and then box them up together. The wrong way to do it - the way that illustrates the issues of the aggregation problem - is to put the ingredients for all 1000 cakes into one pan, bake one giant cake, cut it into 1000 slices, and put each of those slices into a single box. No individual slice looks like a cake, and all the individual slices look the same as one another, where 1000 cakes would all be slightly different. By aggregating the inputs and feeding them through the same function as the micro-level (in this case, baking) you haven’t made an aggregate of 1000 cakes, just one really big cake sliced into 1000 identical parts.

In the case of real wages, the issue is that the measure is meant to proxy how many real goods a given household can buy with the wages it receives. Since every household buys different collections of real goods, and has a different wage path through time, we have to find real wages at the household level before aggregating. It’s difficult - but not theoretically incoherent - to track the consumption basket of each household over time and develop hedonic adjustments to account for changes in goods quality for that household. At each point in time, you can then get an index of whether every household’s wages are buying more of the “real goods” they buy than in the past, although the accuracy of this measure is still subject to the idiosyncrasies of hedonic adjustment and lifecycle consumption shifts.

With the series of real wages from every individual household, an aggregate could safely be constructed in a variety of specifications. A measure produced this way would tell you whether individual households are generally able to buy more or less of the things they actually buy with their wages over time. There would still be issues where outliers would cancel one another out, and weirdnesses presented by the distribution of income and consumption, but it would preserve a substantial amount of empirical information.

However, aggregate measures of “real wages” are never calculated like this, not least because we don’t have the data. Instead of finding each household’s real wage, and then aggregating that data into an index, economists skip a step and start by aggregating the price and wage data - blending all of the ingredients for all 1000 cakes - before baking them. Aggregate “real wages” are measured by dividing aggregate wages by the movement in price of one specific “average” consumption basket: the one constructed by CPI or PCE. This kind of index neither preserves nor contains empirical information about changes in the relationship between wages and consumption baskets at the level of individual households. It only tells us the relationship between an index of wages and one specific consumption basket over time. If you’re a household that makes average wages and buys exactly that consumption basket (3.427% of the household budget spent on a different used car every year and all), that’s pretty useful! If you’re not, well, it mostly tells you about how measured inflation is moving. That’s because the movement of a ratio between two indices over time will be determined by how the more volatile index moves.

Empirical Problems

Empirically, all of this means that measurements of aggregate “real wages” are dominated by movements in inflation, a fact we can see clearly if we add inflation to our earlier chart of “real wages.”

Source: Bureau of Labor Statistics, Bureau of Economic Analysis

When inflation falls, “real wages” spike; when it rises again in the recovery, “real wages” start to fall.We can see this over longer periods of time as well. Real wages are tightly inversely correlated with headline CPI simply because year-over-year nominal wage growth is remarkably steady while inflation is substantially more volatile.

Source: Bureau of Labor Statistics

Changes in gasoline prices account for so much of the volatility in headline inflation that the inverse correlation between gas prices alone and measures of “real wages” is clearly visible. What this means in practice is that, for a household who drives a lot, “real wages” might track their feeling of economic well-being more closely, but there’s no reason for the “real wages” of households that rely on public transit to be that tightly correlated. To see how households’ financial well-being changes over time, you can’t just take the average of products that people buy: just think about how different wage structures are in the kinds of cities where households are far less reliant on automobiles for transportation.

Source: Bureau of Labor Statistics, US Energy Information Administration

By construction, these measures can’t answer the question we most want to ask them: “are households seeing their real position improving or worsening, once changes in their wages and the prices of things they buy are taken into account?” All it can tell us is whether there have been local shocks to measured inflation. As such, we should view these measures, and the arguments that rely on them, with a heavy dose of skepticism.

Instead, we should look at the well-being of households using less powerful, but more theoretically coherent, nominal measures. Rather than our cake example before, where everything has to be carefully coordinated in different steps to make 1000 different cakes, we should stick to nominal measures. If all our quantities are nominal, we can make something more like a stir-fry, where you can make a thousand servings at once, and any plate taken out looks basically like any other plate.

By looking at measures that are denominated in dollars, rather than “basket of heterogeneous goods per dollar,” it’s much easier to build meaningful and coherent aggregates using data that is actually available. The nominal financial surplus of households - how much they are able to save after meeting their consumption needs, and how much their net wealth improves - tells us far more about financial health than “real wages” does. If consumption is rising while wealth is also improving, we can say for sure that the nominal position of households is improving. This may not be as impressive as saying that the “real position” of households is improving, but it is something that we can say knowing that it is methodologically supported and well-anchored in empirical data.

“Real wages” as commonly presented are not a coherent aggregate measurement. That it is “the best that we can do” to come up with an empirical measurement of a theoretical concept is an argument that commentators should find better concepts, not that they should sacrifice coherence and sound empirical methodology.

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.