By Alex Williams

Executive Summary

- The federal government should provide support to state governments during economic downturns in the form of block stabilization grants that serve to replace lost tax revenue. This would contrast from the current state of play, in which state governments cut spending and raise taxes in recession to preserve balanced budgets. The net effect of such grants would be shorter recessions, more job creation, and more stable funding for vital public services. The federal government has done this before through the Treasury Department’s Office of Revenue Sharing.

- Our proposal utilizes a trigger-based formula for timing and allocation. Sensitivity to economic indicators ensures our proposal is timely, targeted and scalable. Use of state-level data helps protect against state- and regional-level economic shocks within the federal structure of the U.S. government in a geographically equitable manner. Legislators can “set it and forget it” instead of spending time and political capital on state fiscal relief for every crisis. The COVID-19 crisis has only further revealed the urgency and importance of stabilizing state budgets to prevent economic and public health catastrophe.

Why This Proposal

Counter-cyclical stabilization has been an important part of economic management since the Great Depression. Recessions wreak havoc on workers and businesses, leaving the government to stabilize consumption and investment. However, not all governments are equally able to play this stabilizing role. The federal government is a large and financially sophisticated actor. State and local governments are very constrained — in fact, even more constrained than households and businesses in their ability to respond to economic downturns. State governments in particular are largely not allowed to finance current operations using debt and must instead sharply curtail spending and raise taxes in the depths of a recession. This highly pro-cyclical behavior lengthens economic downturns and further delays the point at which the local economy has recovered enough for state tax revenues to return to pre-recessionary levels.

States can and do save money in rainy day funds. However, this propensity to save represents a net drag on the local economy in normal times and the funds are rarely sufficient to weather a macroeconomic crisis. Additionally, states have very different fiscal bases, and reliance on rainy-day funds exacerbates regional disparities. In order to prevent severe cuts to state services that worsen and lengthen economic downturns, the federal government must provide automatic stabilization mechanisms through intergovernmental grants.

The stabilization grants put forward in this proposal are inspired by existing federal matching grants, but the objective of our proposal is macroeconomic stabilization. Existing matching grant schemes have perverse effects in an economic crisis: as state governments cut spending on programs that are federally funded by matching grants, they receive even less fiscal aid from the federal government. Matching grants increase state spending when the going is good but decrease spending precisely when recession hits and the funds are more urgently needed. The grants proposed here work in the opposite direction of existing matching grants. As the economy worsens and unemployment increases, the size of federal grants increases. When the economy improves, states need less help and the stabilization grants decrease. The timing and allocation formula in this proposal ensures that stabilization grants are timely and scalable to states’ actual funding needs.

Tying grants to the level of observed unemployment allows grants to be timely. Stabilization grants are timely because they go out the month that a recession is detected. They continue as long as unemployment is elevated, and end as soon as the baseline is regained. The size of grant allocations remains timely, as grants are recalculated quarterly as economic facts change. This timeliness is important for ensuring policy flexibility.

The goal of this proposal is to create a system by which state finances can be stabilized automatically without requiring ongoing policy reevaluation from Congress. To achieve this, the flexibility provided by quarterly grant recalculation is critical. This flexibility ensures that our proposal is stable to any recession timeline — all recessions are different. This flexibility also ensures that the policy response changes as the economic facts change, without requiring a lengthy legislative intercession. Most importantly however, quarterly grant recalculation ensures geographic flexibility in policy response. State and regional economic cycles do not move in lockstep — some states and sectors recover more slowly and need more help. This flexibility also ensures that our proposal works for unemployment events that only affect selected states or regions, like natural disasters or sweeping changes in commodity prices.

Allocating grants based on the level of previous-year own-source tax revenue allows grants to be targeted. Different sectors of the economy respond differently to macroeconomic changes. Additionally, different states have different sectoral compositions. Recessions typically tend to hit capital and consumer durable goods production hard, but the current COVID-19 crisis has hit the service sector — normally resilient to recessions — very hard instead. Yet for states’ government finances, the needs are the same: to mitigate the tax revenue outcome of the downturn. Importantly, this proposal does not prescribe a one-size-fits-all approach. Different states have different tax bases, often owing to their different economic structures.

The allocation formula put forward in this proposal respects state-level decision-making about the relative size of government. High-tax and high-service jurisdictions will see larger grants for the same increase of unemployment rates than will low-tax and low-service jurisdictions. This ensures that state governments cannot game the allocation formula, as grant allocations are made on the basis of budgetary decisions made by state governments prior to the crisis.

At the same time, our proposal also aims for geographic equity. Some states have more fiscal capacity than others. This makes their economies more resilient to negative shocks than states with less fiscal capacity. One of the most important variables that distinguishes the states that are most in need of countercyclical federal aid is the unemployment rate. Employment is also more likely to recover when state governments have the capacity to avoid austerity policies during recessions and recoveries (Carlino and Inman, 2013). By targeting unemployment our proposal ensures that all states will receive the aid necessary to weather an economic downturn, regardless of local fiscal capacity.

Most importantly, these stabilization grants ensure orderly operation of existing institutions on both the state and federal level. On the federal level, state fiscal relief has historically been a part of crisis-specific bills, ensuring that it is only addressed when the problem is sufficiently severe to require a massive response. Because state aid is rolled into these laws, it becomes subject to both the specific crisis at hand, and federal level political brinkmanship. However, we know that every time unemployment increases, states face budgetary shortfalls. If we automate the process of providing fiscal support to state governments, states effectively have an insurance policy that federal lawmakers do not have to reconsider every time there is a crisis. This allows federal policymakers to focus on the more idiosyncratic challenges posed by each economic downturn.

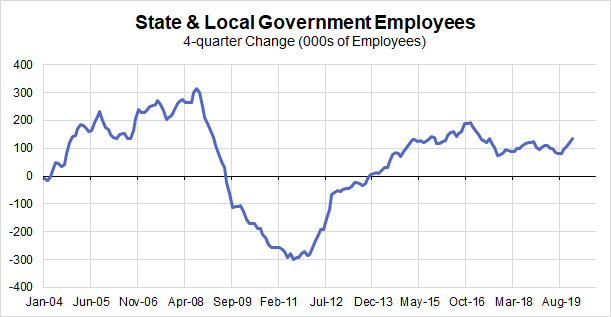

At the state level, this institutional continuity is even more important. When tax revenues fall in a crisis, states respond by cutting spending and raising taxes. However, states historically cut three dollars of spending for every one dollar of tax increases (McNichol 2012). These cuts often come in the form of reduced public sector employment. Additionally, lower staffing makes it harder to access many state services, whose utilization rates increase in a downturn (McNichol 2012). Fiscal stabilization from the federal government will allow states to ensure that they do not cut jobs during a recession.

It is particularly perverse that much of the federal support of state governments in crisis is attached to infrastructure investment or new projects. This creates a situation where losses of tax revenue lead to the destruction of existing jobs, while federal support attempts to create new, unrelated jobs. Ensuring that state jobs are not cut in the first place saves time and administrative difficulty and can be easily accomplished using this proposal. It is easier to prevent job loss than to create new jobs.

Our proposal takes cues from a variety of other recent proposals and synthesizes them into a robust whole. Our trigger mechanism for stabilization payments was originally put forward by Claudia Sahm in “Direct Stimulus Payments for Individuals” for the volume “Recession Ready”. Furman, Fiedler, and Powell III (2019) also propose adding recession-sensitive formulas to allocations for the Federal Medical Assistance Percentages (FMAP) in the same volume. These proposals are very good, and we draw much from them, but they are ultimately limited by total Medicaid spending, which comprises roughly 16% of state-funded expenditures. This would necessarily cap the total federal stabilization grants in the neighborhood of $250 billion.

Bartik (2020) and Gordon (2018) put forward broader programs for stabilization grants using triggers similar to the ones used in this proposal. Bartik (2020) offers many of the same solutions as ours but envisions the policy as limited to the pandemic period. Gordon (2018) adds a trigger-based stabilization mechanism to a variety of existing categorical grants. While this simplifies the initial administrative implementation, it will require substantially more maintenance in the long term, especially given long-running political fights over the structure and status of health care provision more broadly.

The Proposal

We propose that a separate office for supporting state government finances be created within the Department of the Treasury. This office — the Office of Fiscal Harmonization — will oversee the allocation of stabilization grants to state governments on the basis of historical state tax receipts and observed unemployment. Both timing and duration of grants are set by changes in the unemployment rate. The dollar value of the grant allocated to each state is determined by the state in question’s prior-year own-source tax revenues, and the amount in percentage points by which the unemployment rate in that state exceeds the pre-trigger three-month moving average unemployment rate. This proposal is meant to provide fiscal security for budget-constrained state governments during economic downturns beyond their control. A similar facility to the one proposed here existed between 1972 and 1986 as the Office of Revenue Sharing under the Department of the Treasury.

Timing

Timing is critical in recession prevention. Economic time often moves much faster than political time, and our proposal aims to create automatic stabilizers for state governments. These automatic stabilizers preserve the spirit of the federal structure and ensure that state governments have the funds necessary for preserving public sector employment, investment and services.

In a crisis, utilization of state services increases at the same time as tax revenues fall (Greenstone and Looney 2012). States have rainy day funds that can provide for them for a short time, but it is nearly impossible to predict how long recessions will last once they’ve begun. By 2012, total state rainy-day funds had depleted by nearly 83%, from $69 billion to $12 billion, even in the face of substantial fiscal tightening at the state level (McNichol 2012). In order to preserve continuity of state services and employment, it is critical to ensure grants to states begin as soon as a recession is detected. Using trigger-based policy ensures that policy responses are tailored to economic needs.

This proposal offers two different versions of a triggering event for stabilization grants, one using national data, and the other using state data.

- In the version using national-level data, stabilization payments begin when the monthly national unemployment rate rises half a percent above its three-month moving average.

- In the version using state-level data, stabilization payments to a given state begin when the monthly unemployment level in that state rises 0.75 percentage points above its three-month moving average. We use a higher trigger for state-level unemployment rates because state-level unemployment rates are more volatile.

In both versions, the first payment goes out the month that the stabilization program is triggered. Following that, payments continue every quarter using quarterly unemployment rates. The size of the grant varies each quarter with the unemployment rate, in a way explained in the following section. These payments continue until the unemployment rate falls to the level of the three-month moving average when payments were first triggered.

With this timing structure clearly communicated, states can be confident that there will be sufficient fiscal support for the duration of the crisis. Knowing this, states won’t feel pressured to cut essential services in the expectation of revenue shortfalls and will ensure continuity of services.

Administrative Structure

From an administrative perspective, this proposal will be structured along the same lines as the Office of Revenue Sharing from 1972. In the original form, the Office of Revenue Sharing was meant to share some percentage of federal tax revenues with state governments. Our proposal does the same but is agnostic about the source of the funding — whether earmarked from federal tax receipts, debt-financed, or financed by direct monetary creation. That said, the structure is the same.

The Department of the Treasury creates an Office of Fiscal Harmonization and endows it with a trust fund. This trust fund receives a large initial allocation from the federal budget, as well as an earmarked allocation each year going forward. In order to ensure that this trust fund does not run out in a crisis, its initial allocation must be sufficiently large to cover 100% of total state own-source revenues for one year. The initial allocation must be this large in order to ensure that the facility is sufficiently capitalized to provide for all state governments at the necessary level for the duration of the immediate COVID-19 crisis. Were this proposal to be enacted in normal times, the initial allocation would not need to be so high, but some estimates had the United States as a whole approaching 30% unemployment. Even if such gloomy estimates do not come to fruition in this crisis, the next crisis might be far less kind.

Allocations from this trust fund are made to states using the timing and allocation mechanisms described above. They are paid directly from the Office of Fiscal Harmonization trust fund to the general fund of each state that is receiving a grant allocation. These grants follow the formal rules of grants made by the Office of Revenue Sharing. They are made on the condition that states not use grant money to increase spending on federal funds matching programs above a specified level. They are also made on the condition that states spend 100% of the grants within the year granted or be subject to clawbacks. Importantly, these grants are made on the condition that total staffing in all associated state agencies and services are not reduced in the fiscal year these grants are received. Preserving employment and investment through the downturn is the critical macroeconomic purpose of this proposal. Finally, in order to best accomplish the goals of these grants, states that receive them are barred from increasing — or decreasing — tax rates or pension payouts in any quarter in which they receive a stabilization grant.

While the size of this program would be substantial, its purpose is fundamentally to empower states, not to coerce them. The federal government is in an ideal position to insure state governments against the macroeconomic risks that their operating budgets are currently exposed to. The purpose of these conditions are to ensure that this stabilization scheme has the desired macroeconomic outcome of preserving employment and investment. It should hopefully serve the interests of both federal and state government interests, but should state governments find the conditions of the proposal excessively burdensome, there is no penalty for opting out.

This administrative structure ensures that the federal government does not decide ahead of time which aspects of state tax revenue will be hardest hit by the recession. It allows states wide latitude in allocating funds, so long as they satisfy the basic conditions for how the money is spent and that state employment is not reduced during an economic downturn. The grants are intentionally larger than what is strictly necessary to return tax receipts to their expected values in order to ensure that compliance with the proposed conditions is not an excessive burden on states. State fiscal assistance of this form has a well-understood playbook and strong legislative precedent.

Allocation

Allocation of grants is a sensitive manner, and this proposal ensures that it is not possible to game the stabilization grants. The stabilization grants proposed here are meant to prevent cuts to services due to unexpected revenue shortfalls. Therefore, each state’s expected revenue is the most important data point for calculating grant allocation. Empirical research has indicated that tax revenues are highly sensitive to changes in the unemployment rate, Fiedler, Powell III (2020). When unemployment increases, income tax falls as income falls, sales tax falls as consumers spend less, and public fees fall as citizens utilize fee-based services less often. Knowing this, this proposal uses the unemployment rate and expected own-source revenue for each state to allocate stabilization grants. This insulates the proposed Office of Fiscal Harmonization from federal-level political jockeying.

Our proposal allocates grants using a two-step process. First, when a stabilization grant is triggered using the timing mechanism above, a baseline unemployment rate for the purpose of allocation is calculated. To do this, we take the average unemployment rate over the preceding three months for each state receiving stabilization payments. Under a state-level trigger system, all states that have elevated unemployment sufficient to trigger payments will receive payments. However, under a national-level trigger system, it is possible that some states will not have a current unemployment rate above their calculated baseline unemployment rate, and so will not receive stabilization payments. These states will receive stabilization grants in the first quarter that their current unemployment rate exceeds their calculated baseline unemployment rate. This data gives us the number of percentage points by which current unemployment exceeds baseline unemployment.

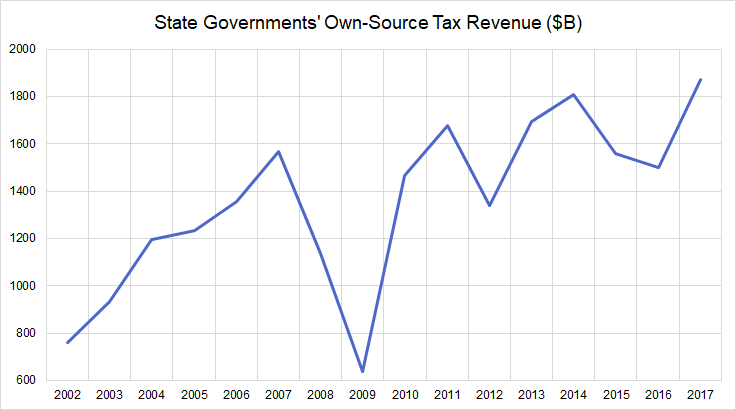

To determine the size of a given state’s stabilization grant, we then look at the state’s own-source tax revenue using data provided by the National Association of State Budget Officers (NASBO). For each percentage point that the current unemployment rate exceeds the baseline unemployment rate, we allocate a percentage of the state in question’s previous year own-source tax revenues. The elasticity of state revenues to a given change to the unemployment rate is likely to evolve over time as the structure of the economy changes. As a result, the precise calculation of the optimal revenue replacement rate should be delegated to the Office of Fiscal Harmonization and updated to reflect new information.

The main objective of the revenue replacement rate should be to ensure that the trend revenue growth is restored in the vast majority of states. During the Great Recession and its aftermath, the revenue replacement required to restore trend revenue growth, and not simply missing tax revenue, was close to 8% across all fifty states Williams (2020). For comparison, a 5% match restores trend growth only in a little more than half of all states. Regardless of the final match percentage, this formula ensures that state-level allocations are proportional to expected growth in tax revenue, adjusted for macroeconomic conditions.

The allocation formula is thus: the number of percentage points of excess unemployment, multiplied by the state’s previous year own source revenue, multiplied by the Office of Fiscal Harmonization’s updated estimates of the revenue replacement rate. This grant allocation formula captures each state’s expected tax revenue for a given quarter as well as the expected shortfall for a given increase in the unemployment rate.

Allocations from the proposed Office of Fiscal Harmonization take the form of block grants. State finances are highly complex, and federal grants are traditionally conditional grants attached to specific state-level programs. In a recession however, it is impossible to predict ahead of time what economic sectors will be hit the hardest and which state government revenue streams will be most severely impacted. As such, stabilization payments take the form of block grants to the state’s general revenue fund so that they reflect the most pressing needs within the states’ operating budgets. This minimizes administration at the federal level while allowing states to choose how to allocate these block grants to support the finances of local governments. While this may seem unprecedented, the grants provided by the original Office of Revenue Sharing took exactly this form.

There is much worry about federal “bailouts” of state governments. However, these worries misunderstand the relationship between the federal government and state governments. Discussions about federal-state financing relationships are often in terms of “moral hazard,” where an agent can make a choice that benefits themselves at the expense of the principal. Traditionally, states are considered to be agents, while the federal government is considered a principal. In these conversations, it is assumed that states can behave irresponsibly and rely on the federal government to bail them out, but this is exactly backwards. Despite the capacity to run deficits in recessions, the federal government does not take full responsibility for services provided at the state level. The federal government is incentivized to under-spend on state support, since it retains the benefits of spending less in non-crisis periods while avoiding the blame for insufficient public service provisions during crisis periods.

Some Precedents

State fiscal support has been an important part of crisis response for the past 15 years. The two main examples are the CARES Act and American Recovery and Reinvestment Act. Both of these responses fell short in critical ways. After outlining the benefits and drawbacks of the crisis-driven response to state fiscal support, we look at two programs that provide examples of how state fiscal support should be structured.

The American Reinvestment and Recovery Act of 2009 (ARRA) included substantial state fiscal support. This support was meant to defray costs to states arising from the financial crisis and ensuing recession. However, this fiscal aid only arrived well after the crisis had begun and ended long before the crisis finished. In 2012, many state unemployment rates had not recovered, and states’ rainy-day funds were completely exhausted. There was insufficient federal political will to secure further aid to hard-pressed states. The end of this fiscal support meant a second round of budget cuts and job losses in state agencies, thereby diminishing an already weak recovery. In addition, much of the funding provided from the federal level to states was on a per-project grant basis and targeted to “shovel-ready projects.” These projects take substantial time to permit and break ground on, delaying the point at which federal assistance money reaches workers. Additionally, these “shovel-ready projects” were being funded at the same time that police, firefighters, teachers, and state administrators were being laid off. Rather than backstop state tax revenue, the ARRA used states as a conduit to administer a variety of new projects. The ARRA implicitly predicted the length of the recession at its outset by setting a timetable for funding that was not responsive to changes in key economic indicators. The prediction it made was wrong, and so despite the fact that state tax revenues were far from recovering their pre-crisis growth trajectories, the federal government failed to provide stabilization payments beyond the original timeline.

The Coronavirus Aid, Relief, and Economic Security Act (CARES) provided fiscal support to state governments in order to defray costs associated with the COVID-19 pandemic. These fiscal supports come in the form of targeted grants to specific programs expected to see increased uptake during the COVID-19 crisis. These include supports for housing, childcare, community development, education and public health. These grants come through existing grants to agencies, one of the most administratively simple responses. Also included in the CARES Act is $150 billion for unbudgeted costs incurred before December 2020 in responding to the COVID-19 pandemic. These grants are distributed to states on the basis of population, a reasonable metric when facing a public health crisis.

The CARES Act addresses expected new costs faced by state governments in response to the COVID-19 crisis, however, it completely ignores the fact that many states have lost ten to thirty percent of their revenue base, for the duration of the crisis. It provides specific grants for services closely related to the crisis response but ignores that normal state services are facing a historic budget crunch due to the loss of tax revenues. The CARES Act would be an exemplary response to the crisis were our proposal already enacted. Unfortunately, states are already cutting programs that are required to be funded out of general revenue. For example, New York, a hotspot of the epidemic, is already budgeting for draconian cuts to Medicaid on the expectation that tax revenues will come in grossly under previous expectation. The CARES Act addresses the need for new expenditures, but ignores the loss of tax revenue, and as such will be ineffective in combating the crisis in state budgets.

In contrast to these ad hoc approaches to state fiscal support undertaken in crisis, we look at two examples of systematic aid to states in a federal system.

The Canadian system of provincial equalization payments was established in recognition by the federal government that different provinces have different economic bases, and therefore, different fiscal bases for provincial services. To mitigate this, the federal government maintains a system of transfer payments to ensure that all provinces meet a minimum per capita tax revenue. This is done by averaging the per capita tax revenue of a representative selection of provinces. Equalization payments account for up to 20% of the budget in some provinces. While these equalization payments are not sensitive to recessions — if the tax base in all provinces decreases simultaneously, equalization payments decrease as well — they demonstrate that general fund-based stabilization can work within a federal system.

This general fund stabilization is an important difference from the US system. State funding in the US is 90% categorical grants delivered through federal agencies to support related programs at the state level. These grants are targeted by a state’s ability to meet the federal government’s mandate, rather than by equalizing the per capita tax base of each state. Were the US to run a state stabilization system similar to Canada, disparities in service provision between states would narrow, as the tax base in Alabama or Louisiana is strikingly different in size and structure from that of California or Illinois. Our proposal offers a version of that equalization, but one which is also sensitive to macroeconomic conditions.

The second precedent comes from the United States of the past: the Office of Revenue Sharing created by the State and Local Fiscal Assistance Act of 1972 (SLFA Act). The act allocated federal revenues directly to state — and through state passthrough grants, local — governments. The grants were made using an allocation formula that took into account population, a “tax effort” factor, and a relative income factor. Grants were made 2:1 to local governments over state governments. However, states were given wide latitude in making use of granted funds. Local governments were encouraged to allocate funds to capital expenditure projects, however, maintenance and operations were considered acceptable expenditures, as well as a variety of “priority expenditures” that encompassed the majority of state and local government functions.

The SLFA Act was explicitly an anti-recessionary measure, but nevertheless contained few provisions to ensure that funding was timely and targeted to recessions. Rather than waiting for a recession to hit, it simply increased funding to states at all times. Our proposal forces states to tax when the economy is in good shape, but provides them insurance for this tax revenue when the economy is in bad shape. Our proposal builds on this previous law by adding more flexibility, better timeliness, closer attention to economic facts, and better targeting.

Conclusion

State fiscal aid is an important part of the federal response to an economic crisis. It is so important in fact, that it should not be re-litigated and re-legislated in every economic downturn. Our proposal makes use of past legislative precedent to assemble an Office of Fiscal Harmonization that ensures states have security in their tax revenue streams. It is more timely than past responses, by ensuring the appropriations and allocation mechanisms are transparently laid out prior to an economic crisis. Spending happens exactly when it needs to, which allows states to plan without worrying about revising budgets downwards and cutting jobs in a recession. It is more targeted than past proposals, as the allocation formula is sensitive to the severity of the recession, the differences in sectoral composition between states, and differences in taxation between states. It is more democratic than prior proposals, as states allocate their stabilization grants to ensure that democratically agreed upon services continue, without a second layer of budgetary wrangling from the federal level. This proposal is one that you can “set and forget.” It works for any crisis that results in substantial unemployment and serves as a first line of defense for state-level services. Most importantly, enacting this proposal allows political energy to be focused on resolving specific crises as they arise, without having to also add state fiscal support to any emergency legislation.