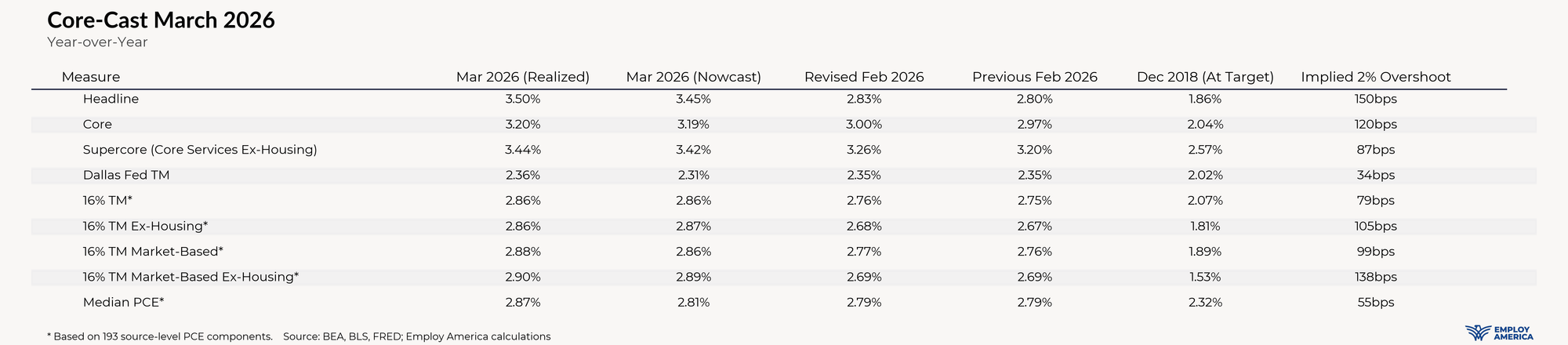

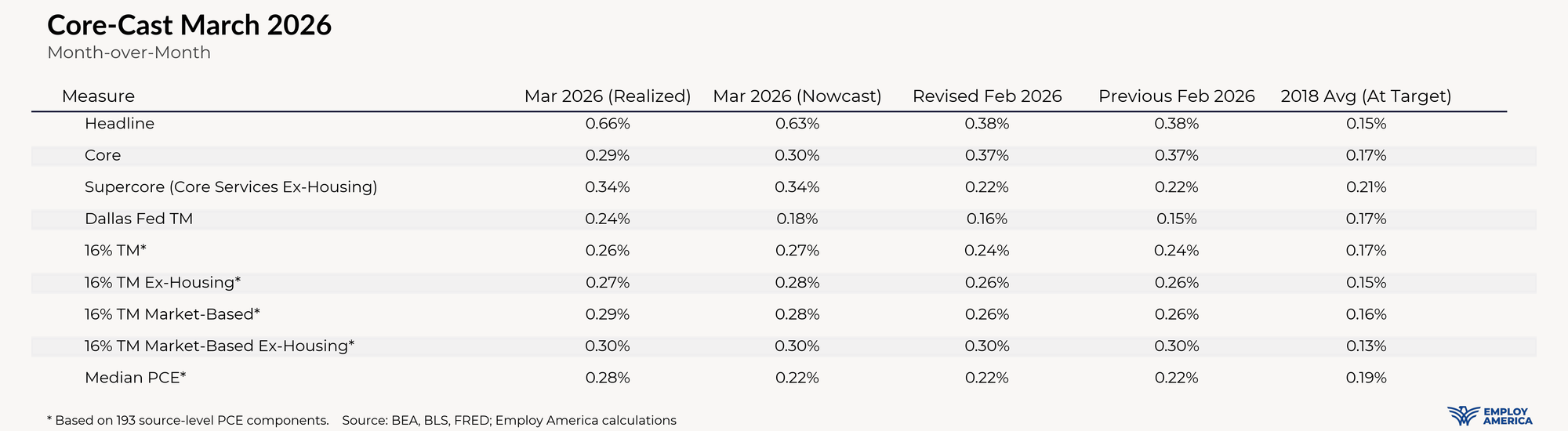

After Kevin Warsh's professed interest in Trimmed Mean PCE at his confirmation hearing, we published updated nowcasts for all PCE inflation gauges, including Trimmed Mean and Median inflation, as well as updated estimates for Headline, Core, and Supercore PCE. Compared to those nowcasts, we didn't learn much in the PCE release. The major gauges were within 1-2 basis points, both on month-over-month and year-over-year readings.

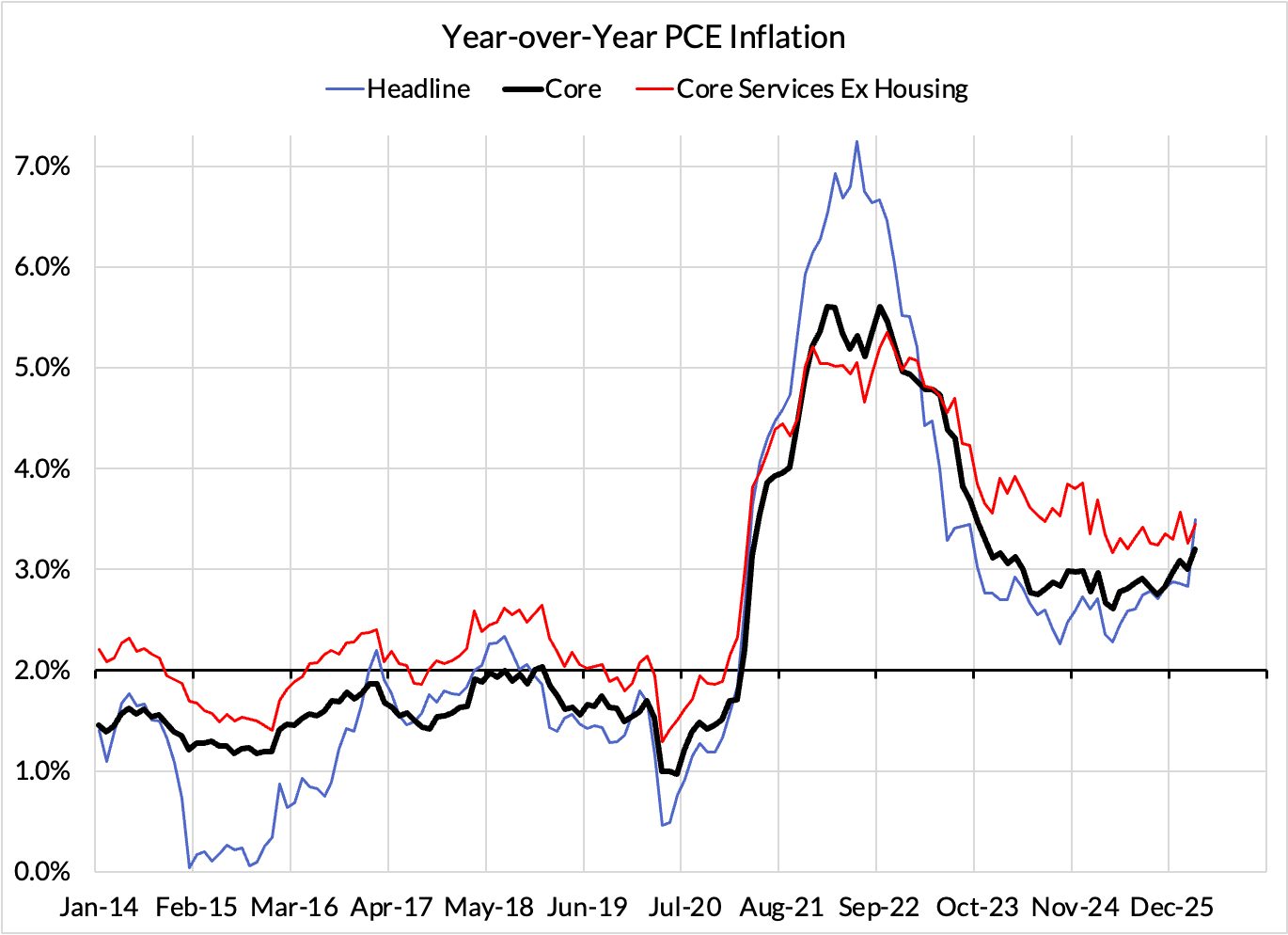

The Fed is in a pickle. Inflation on almost every relevant summary gauge is picking up steam and the trends were beginning before the outbreak of war. We now have four consecutive months in which inflation readings have been running strong, and given what we anticipate from airfares and housing in April, we could very likely see a fifth straight month of inflationary strength. It is fully understandable why FOMC members are getting uncomfortable with the current easing bias and shifting in a hawkish direction. The inflation data is accelerating even as the downside risks to growth, labor markets, and financial markets appear to dissipating over the near term. Even cyclical sectors like housing and manufacturing have shown some local improvement. While some might be quick to write off Presidents Kahskari, Logan, and Hammack's dissents as irrelevant to the FOMC's final decisionmaking, we see them as leading indicators amidst this inflation backdrop. Other Fed Governors are also moving hawkishly and will likely grow more open to dropping the easing bias and considering a tightening bias if current data trends persist for another couple of months.

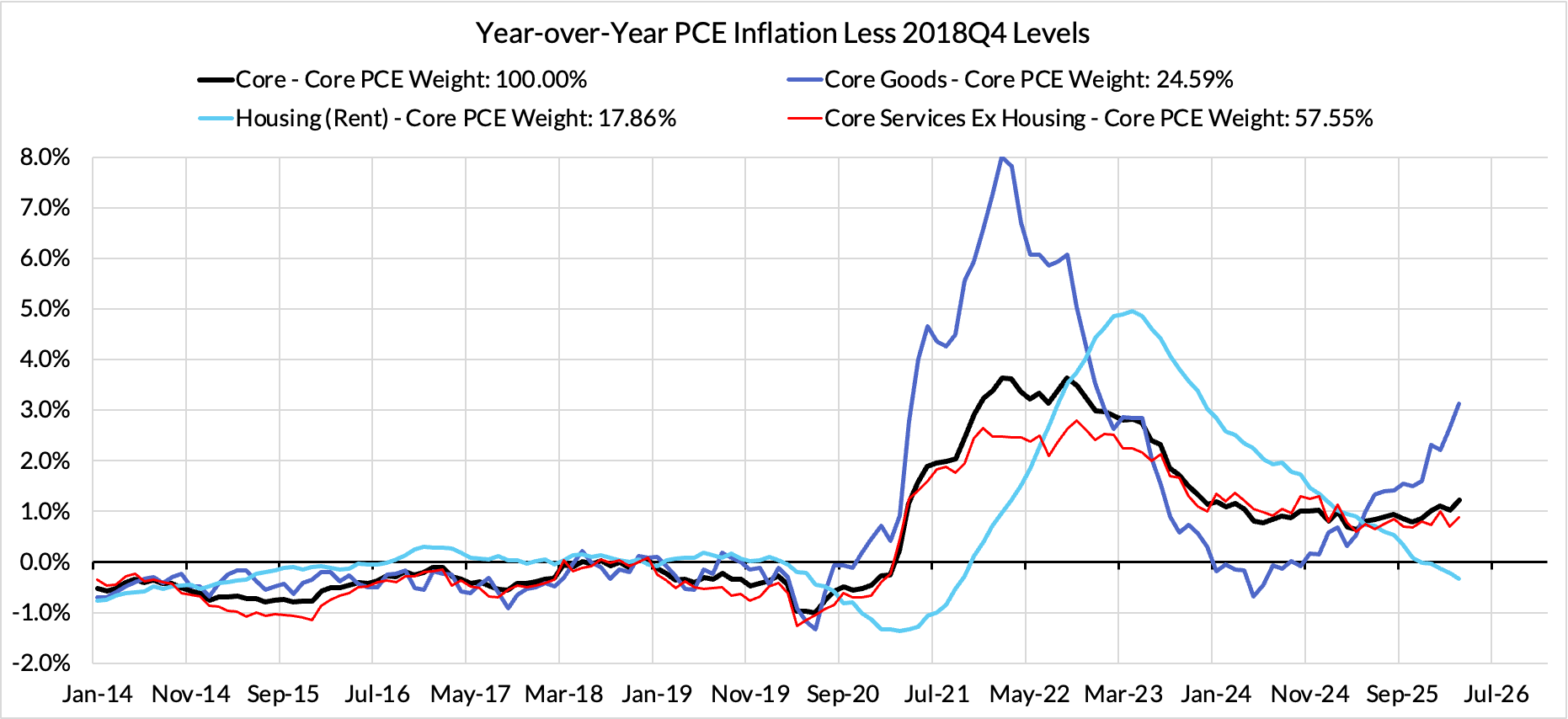

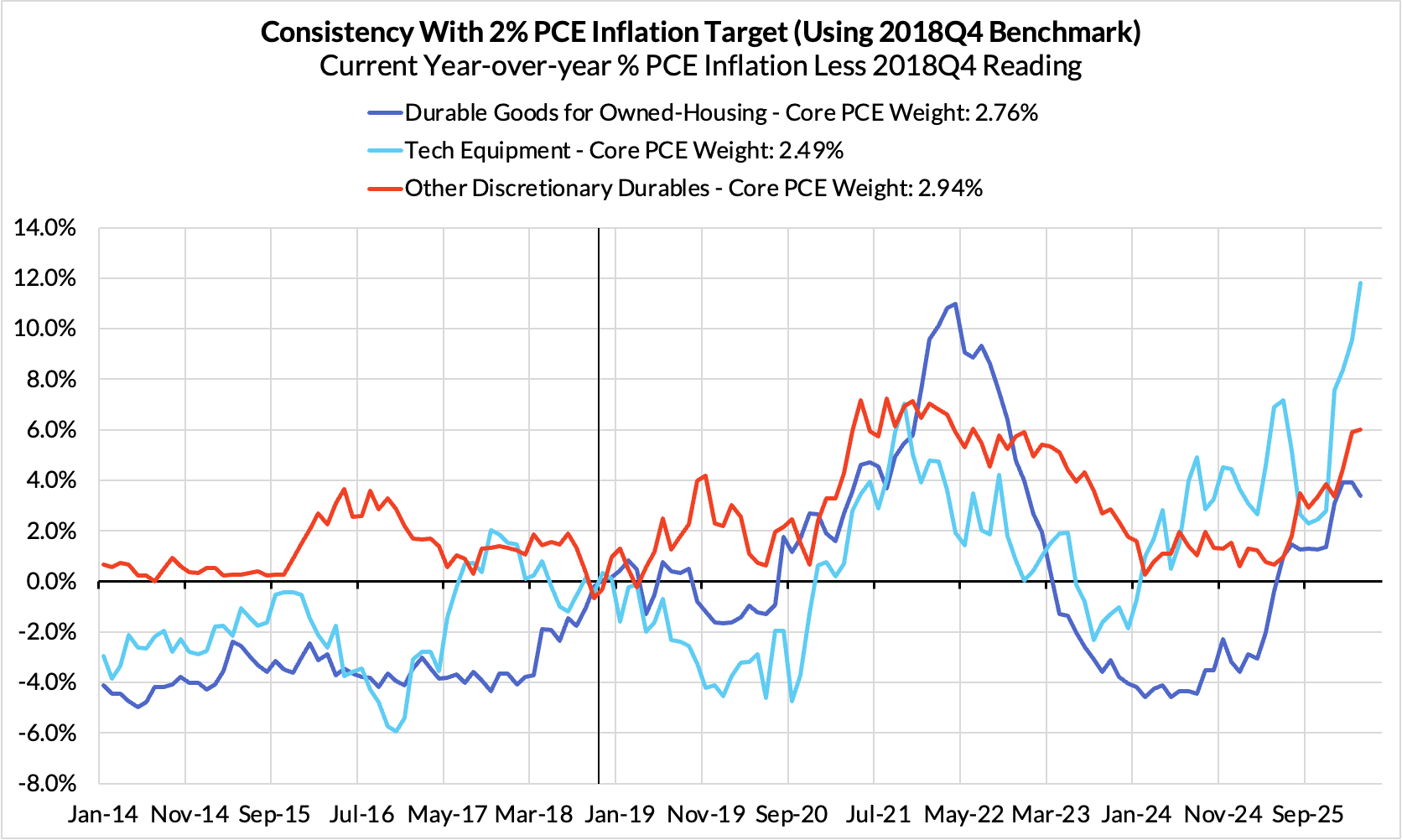

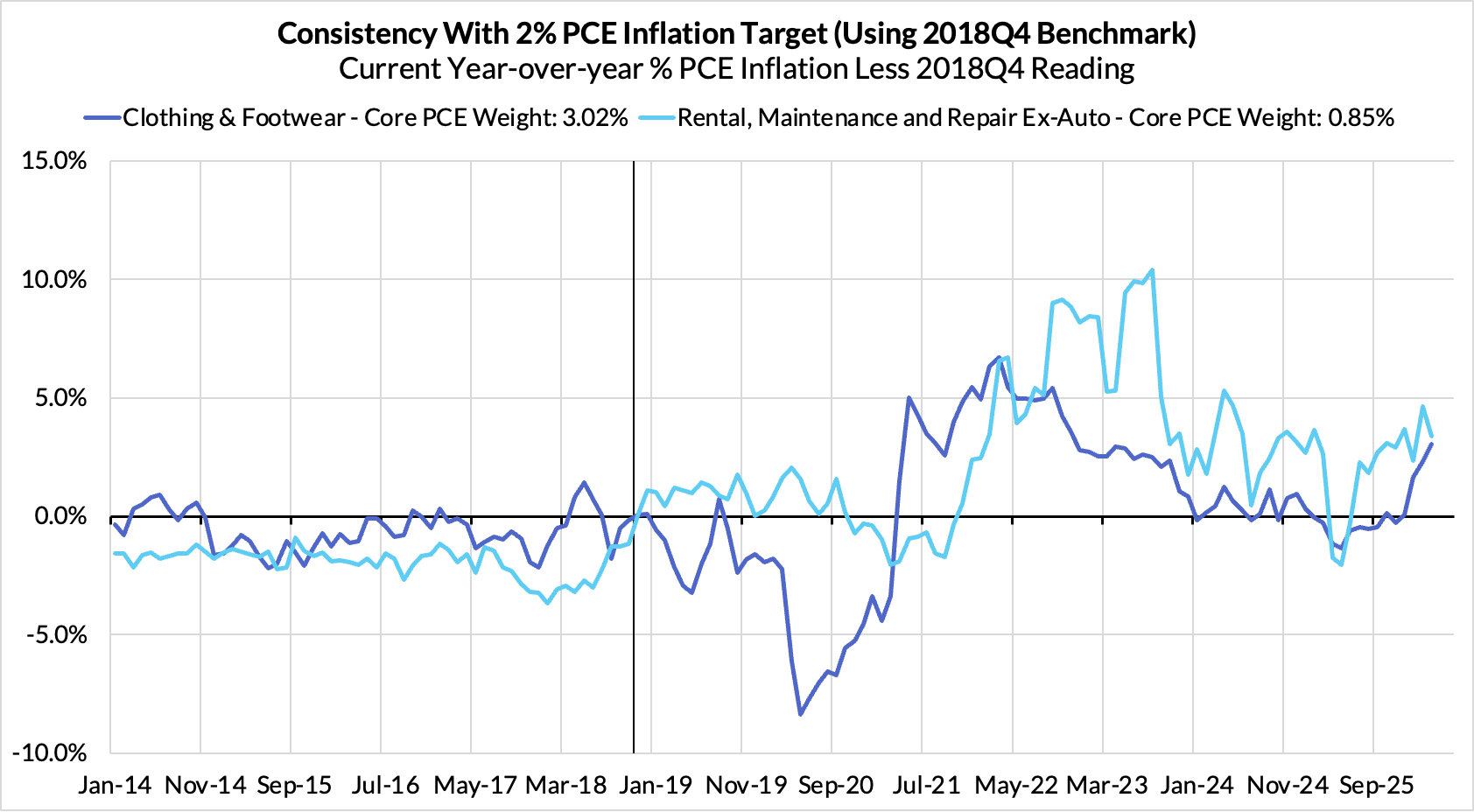

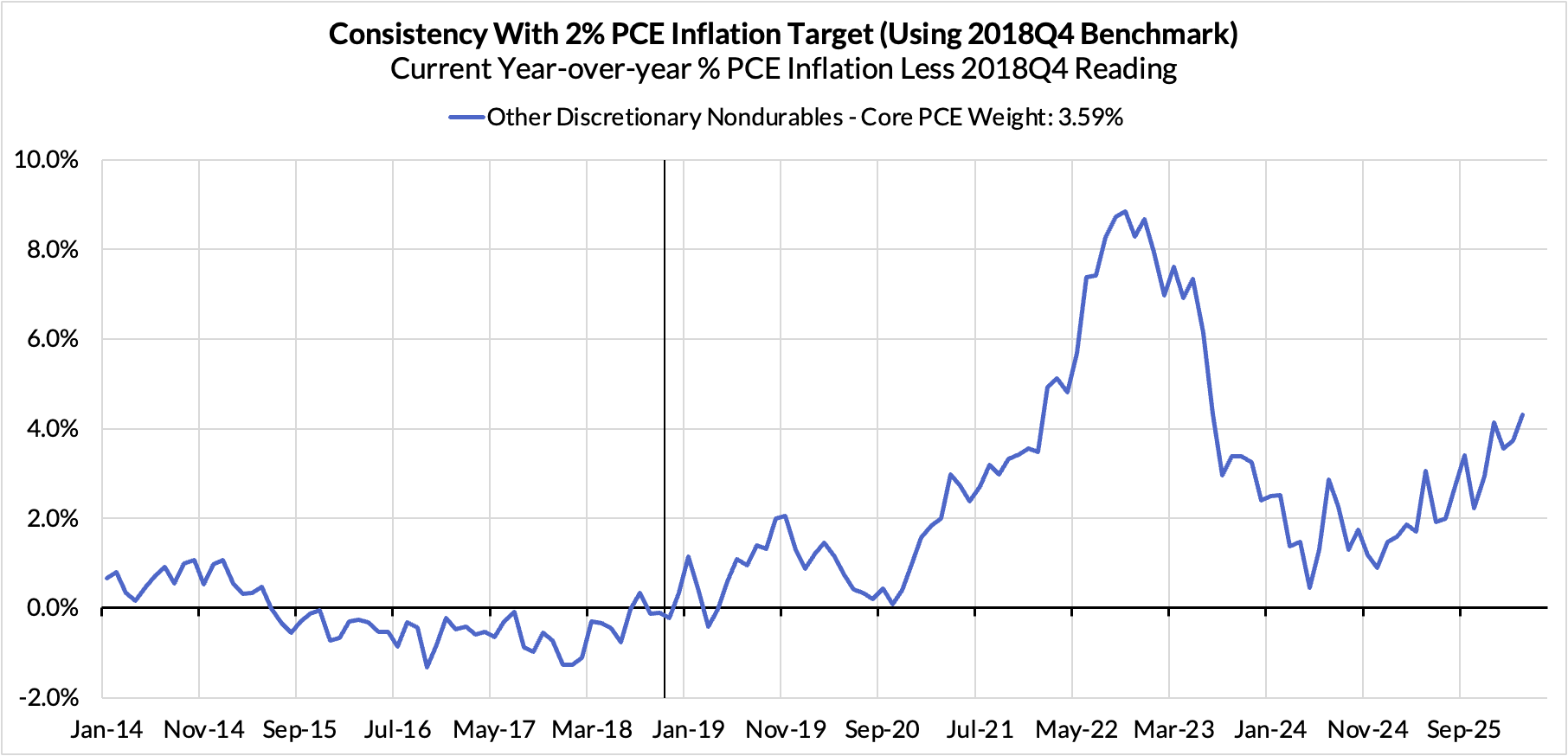

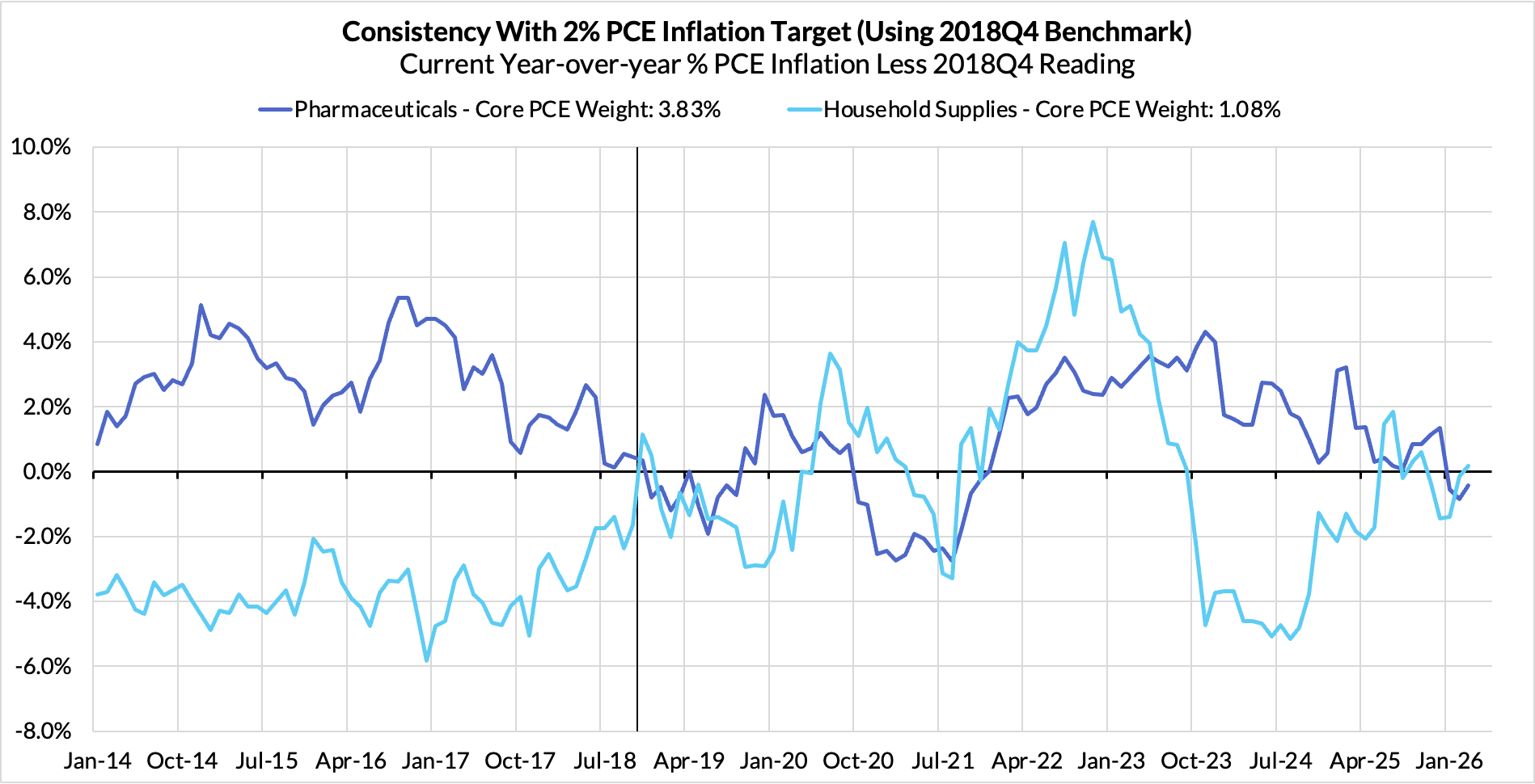

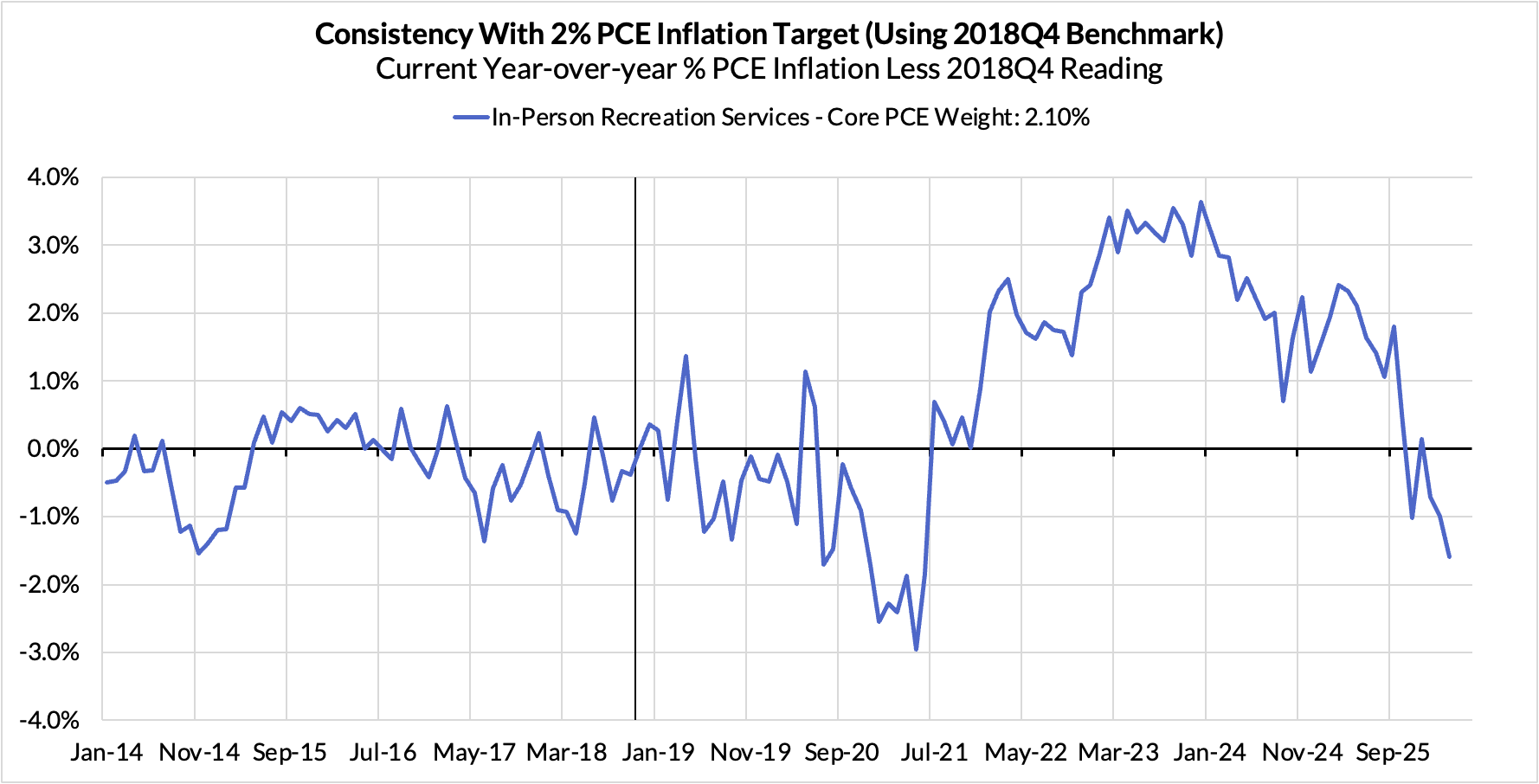

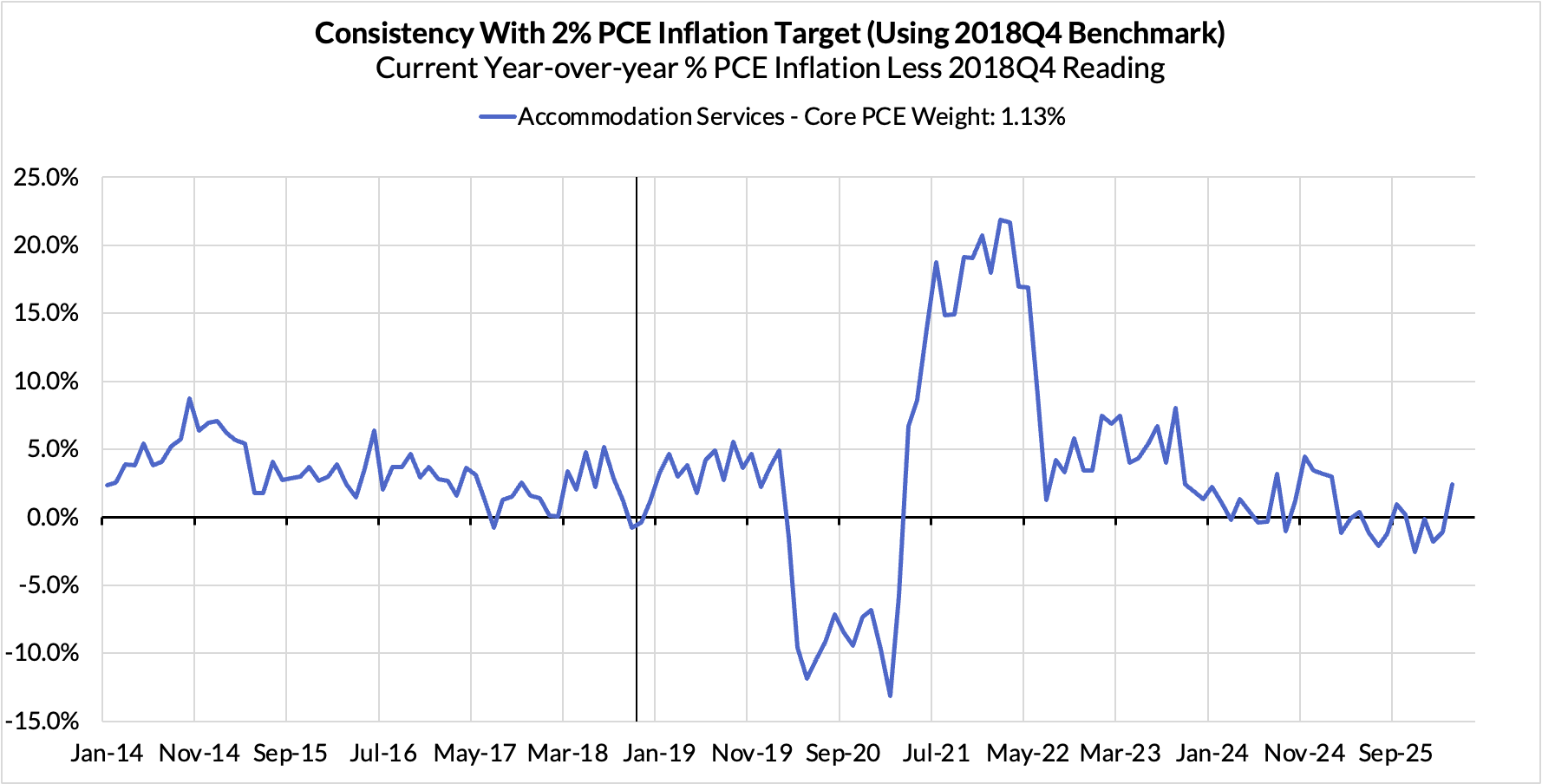

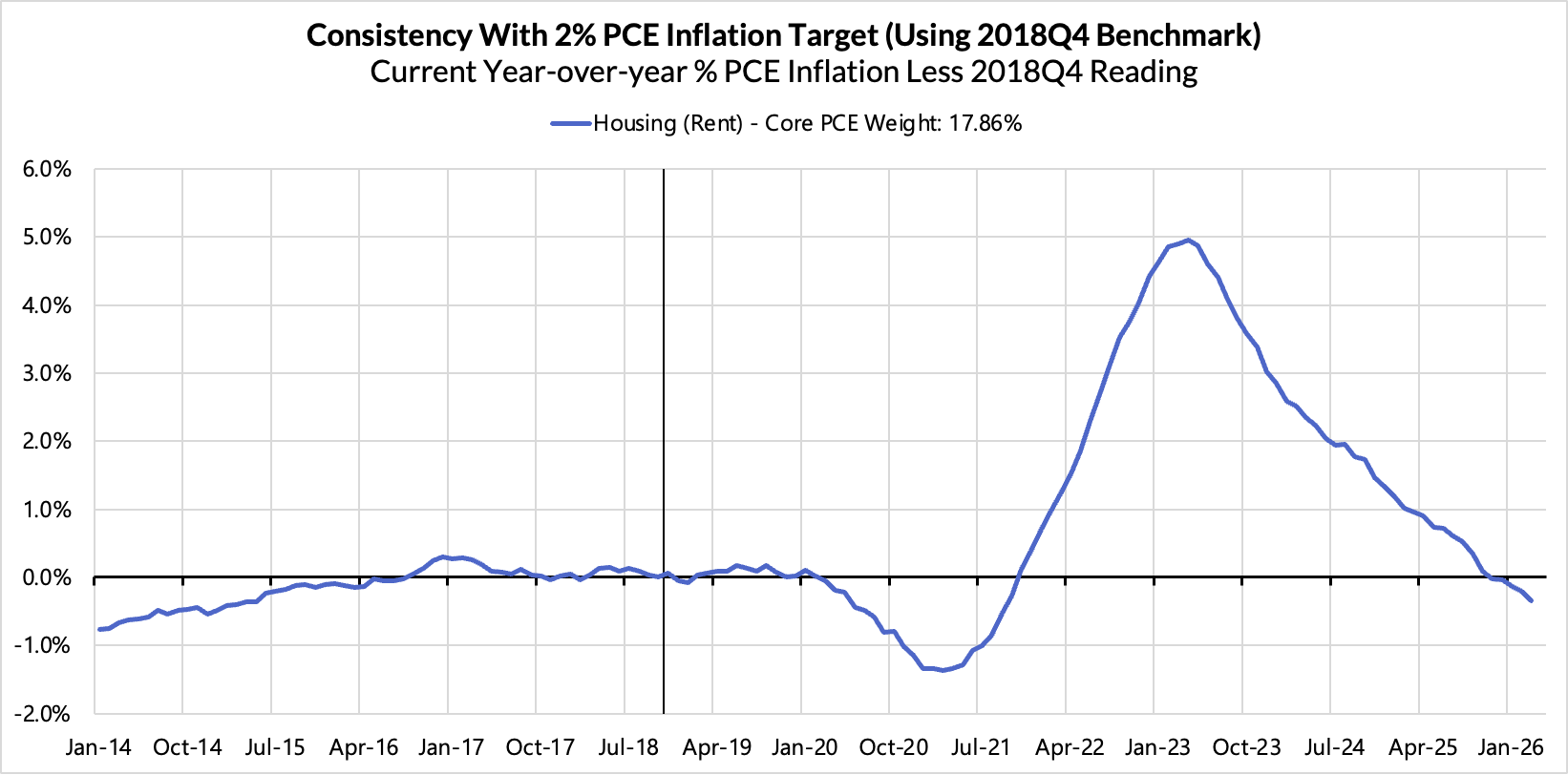

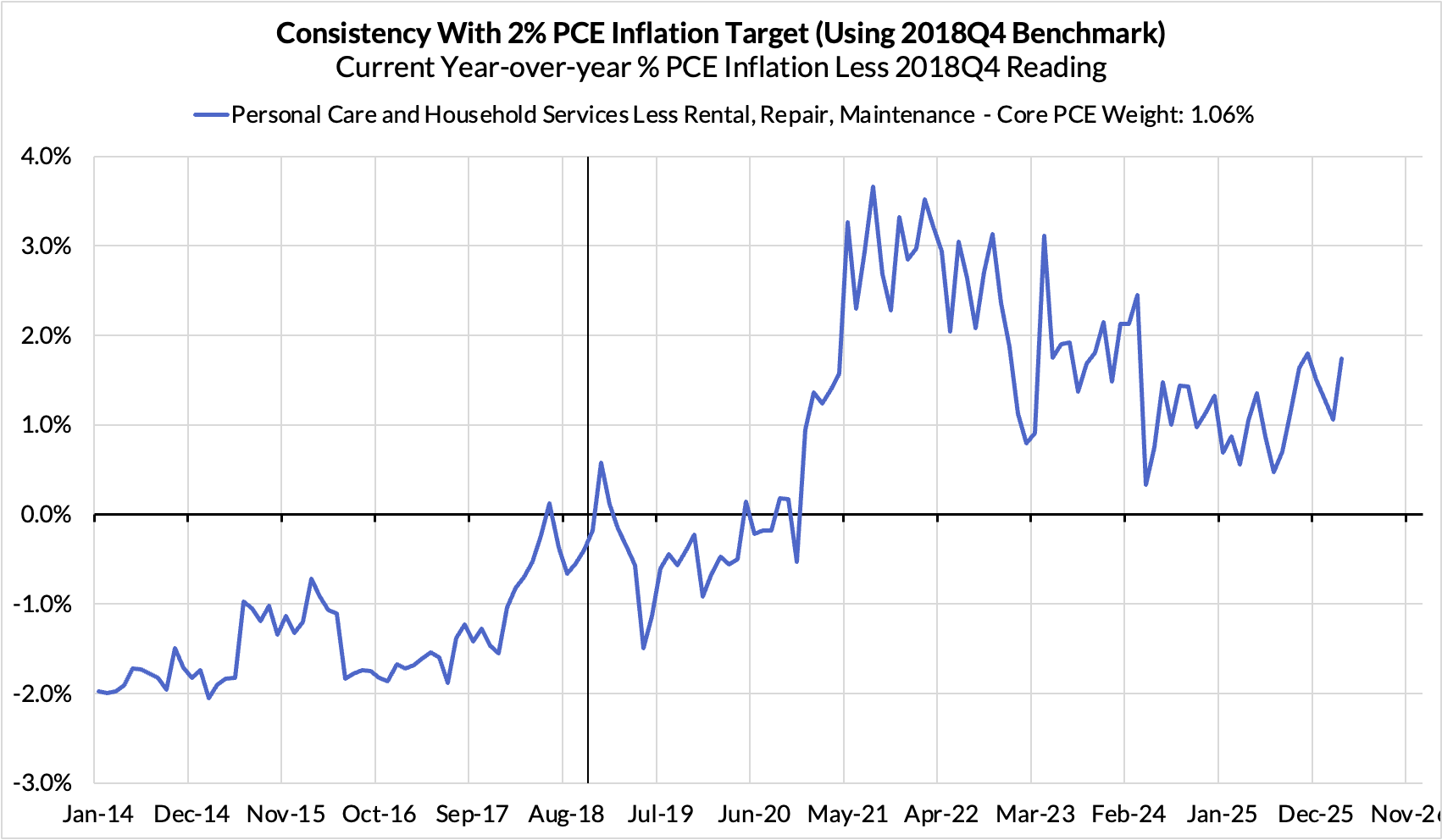

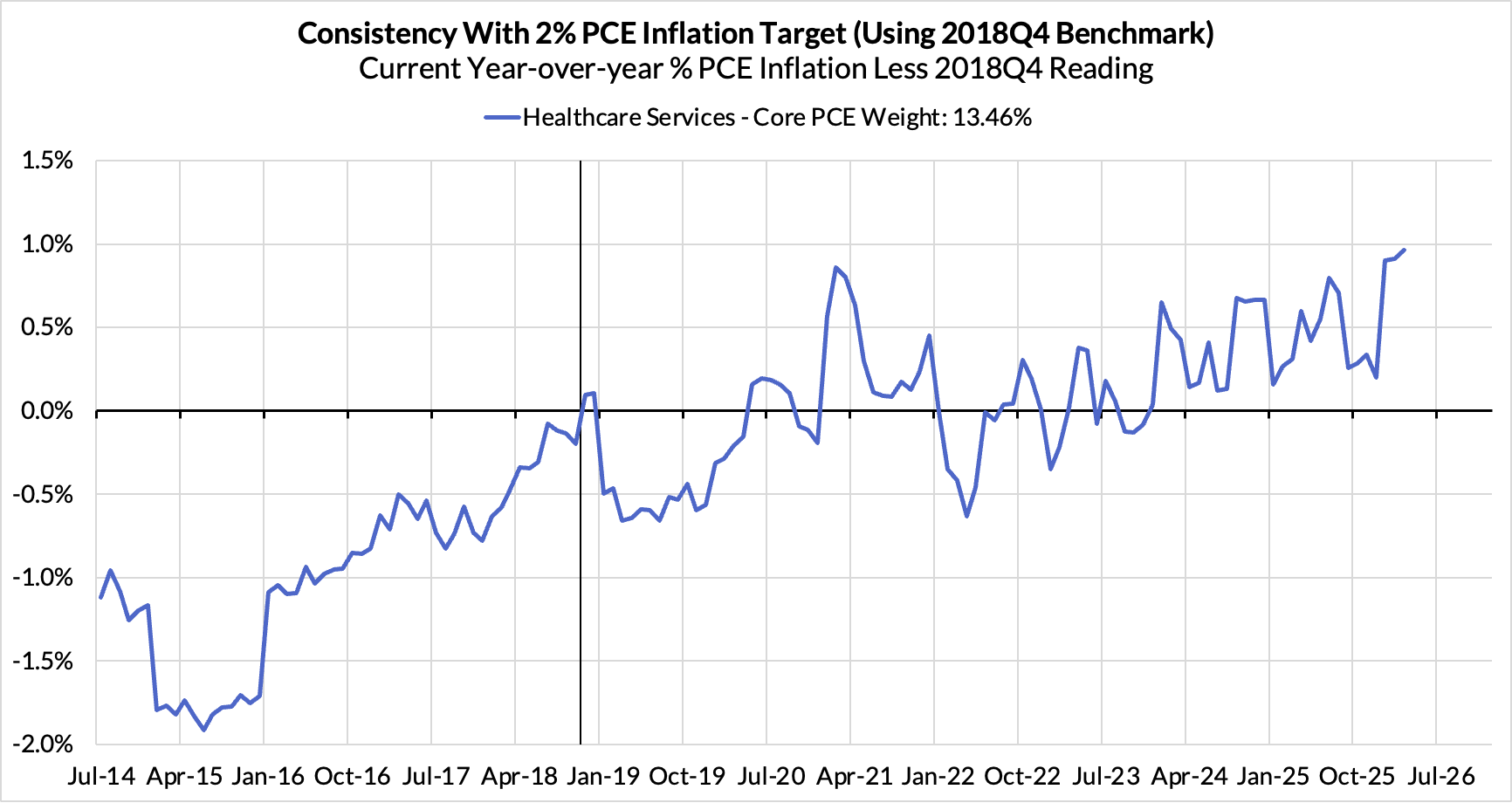

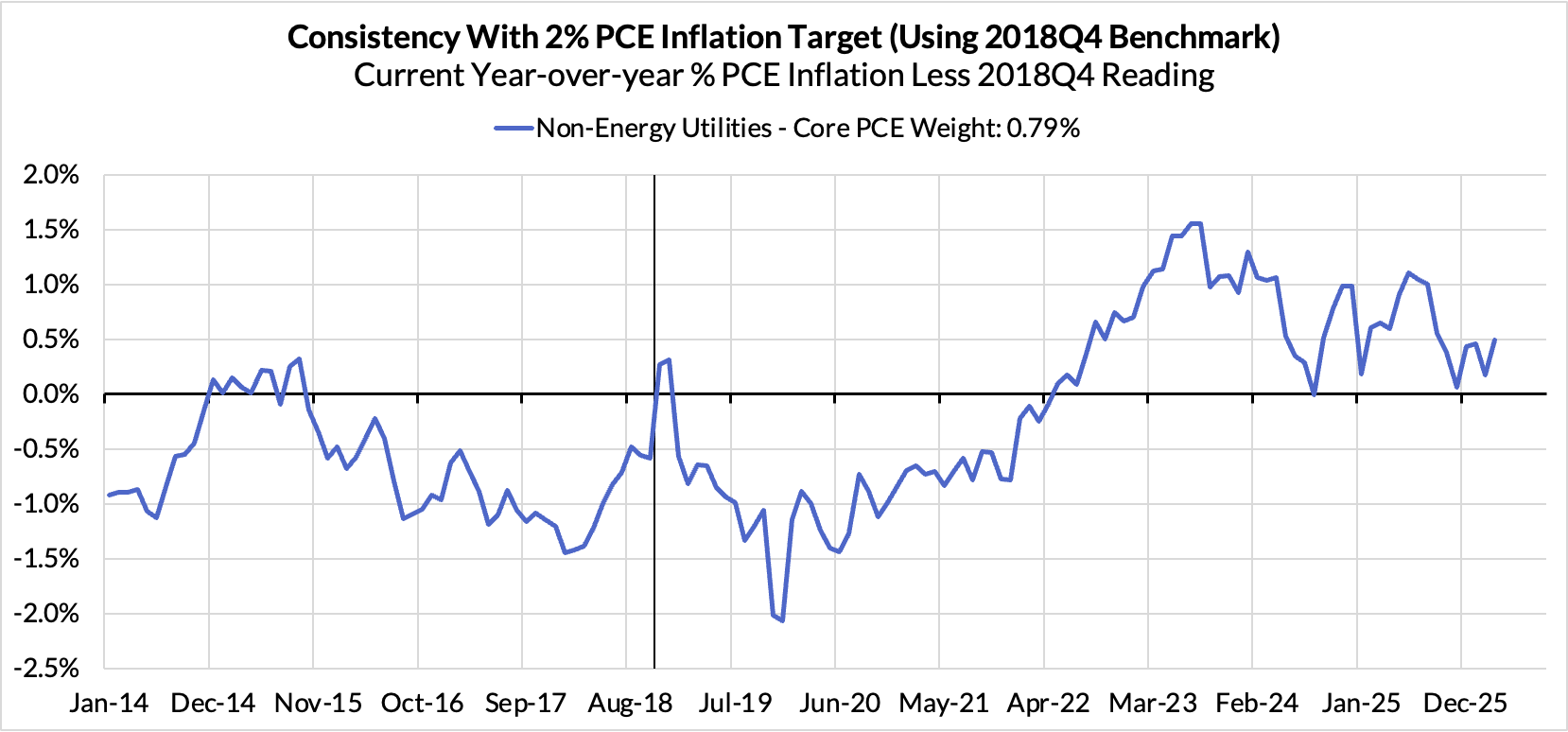

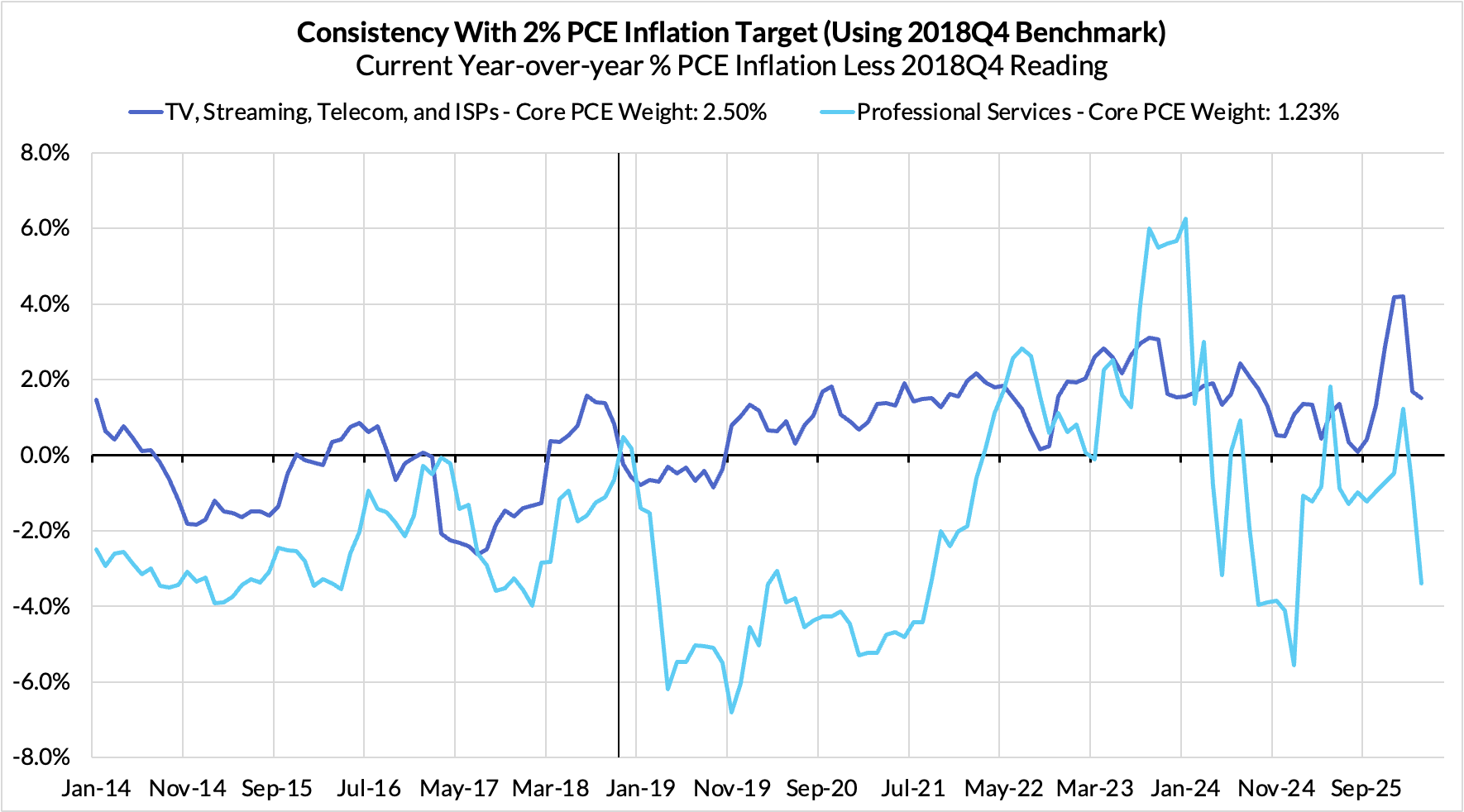

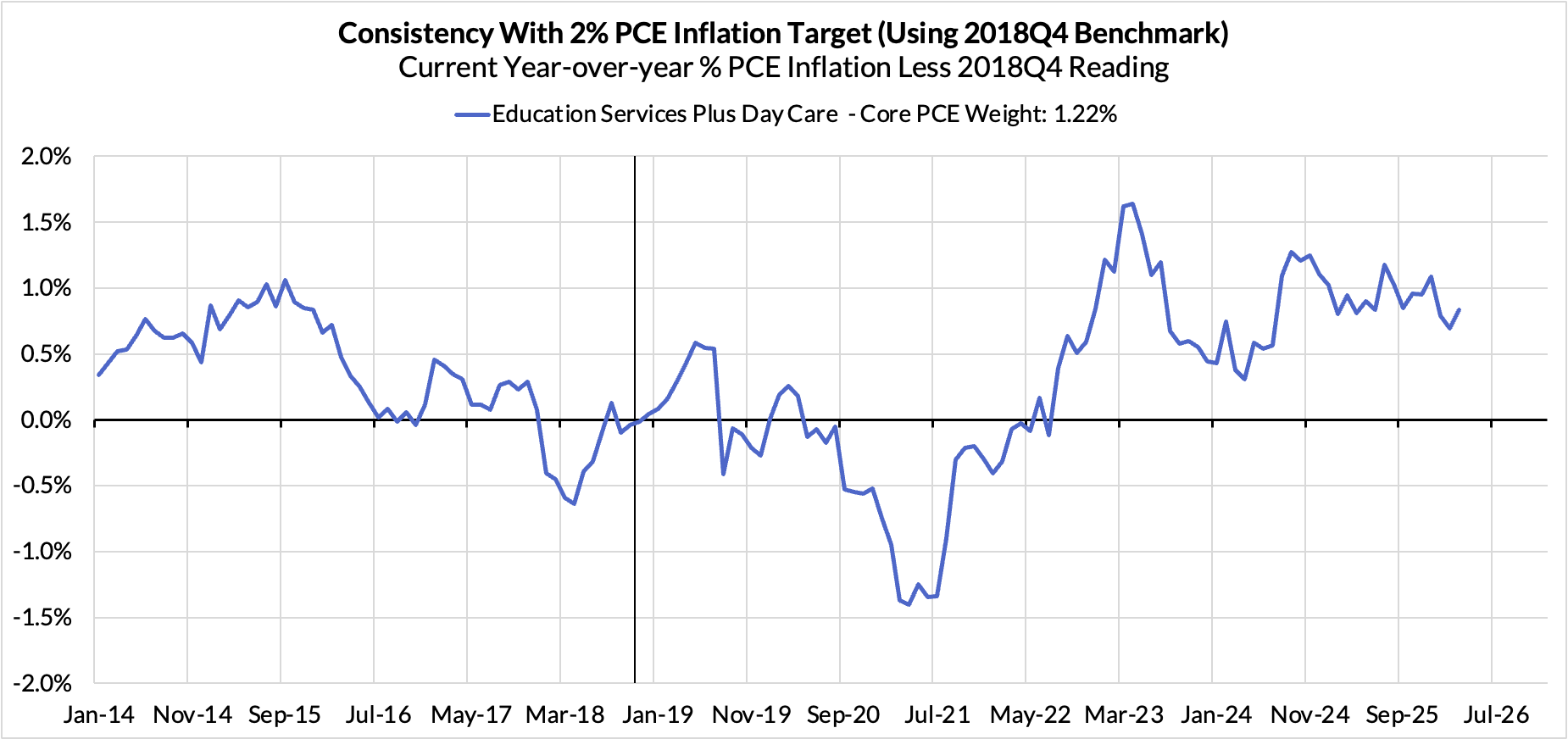

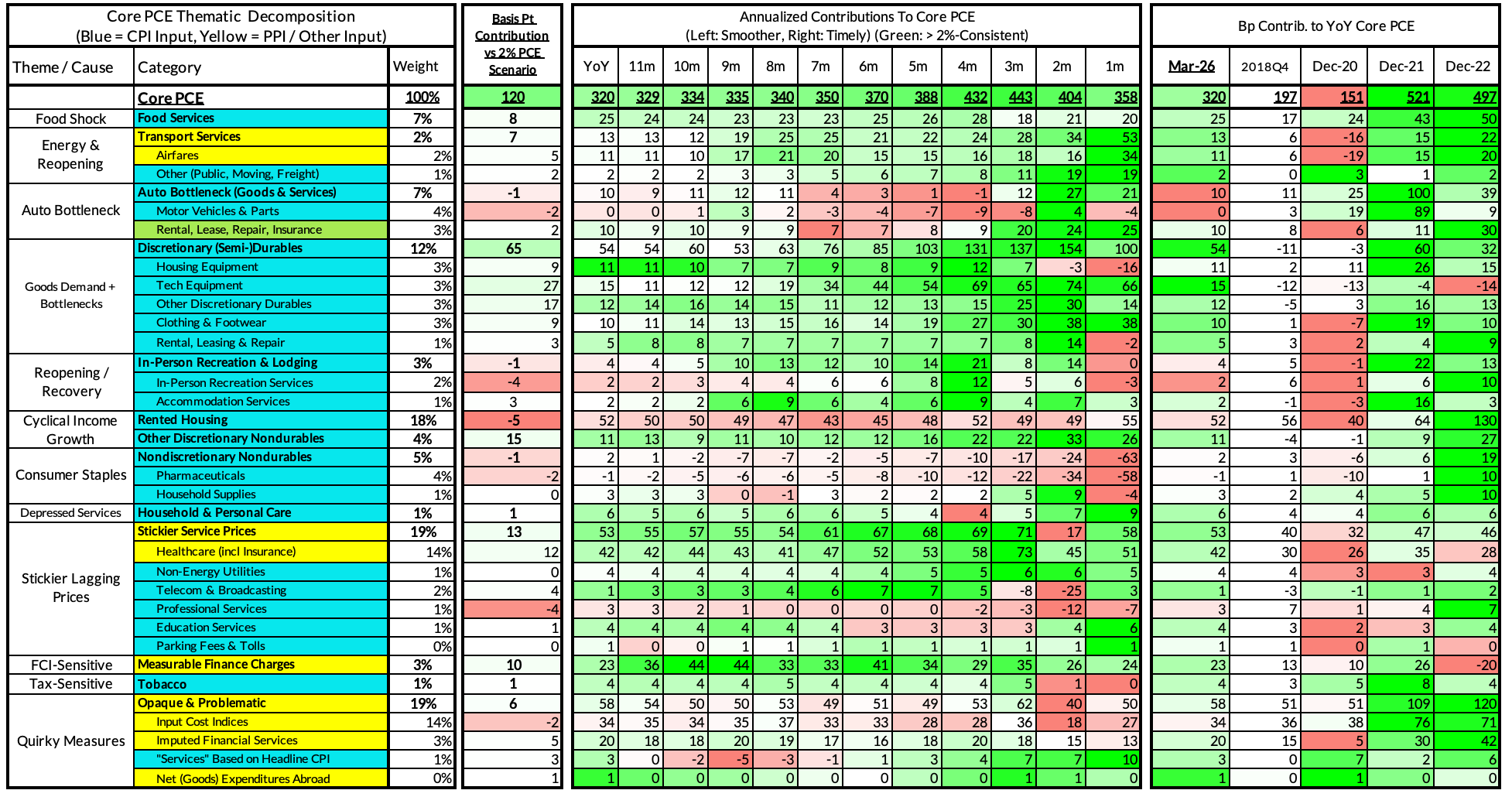

Inflation Overshoots At The Component Level

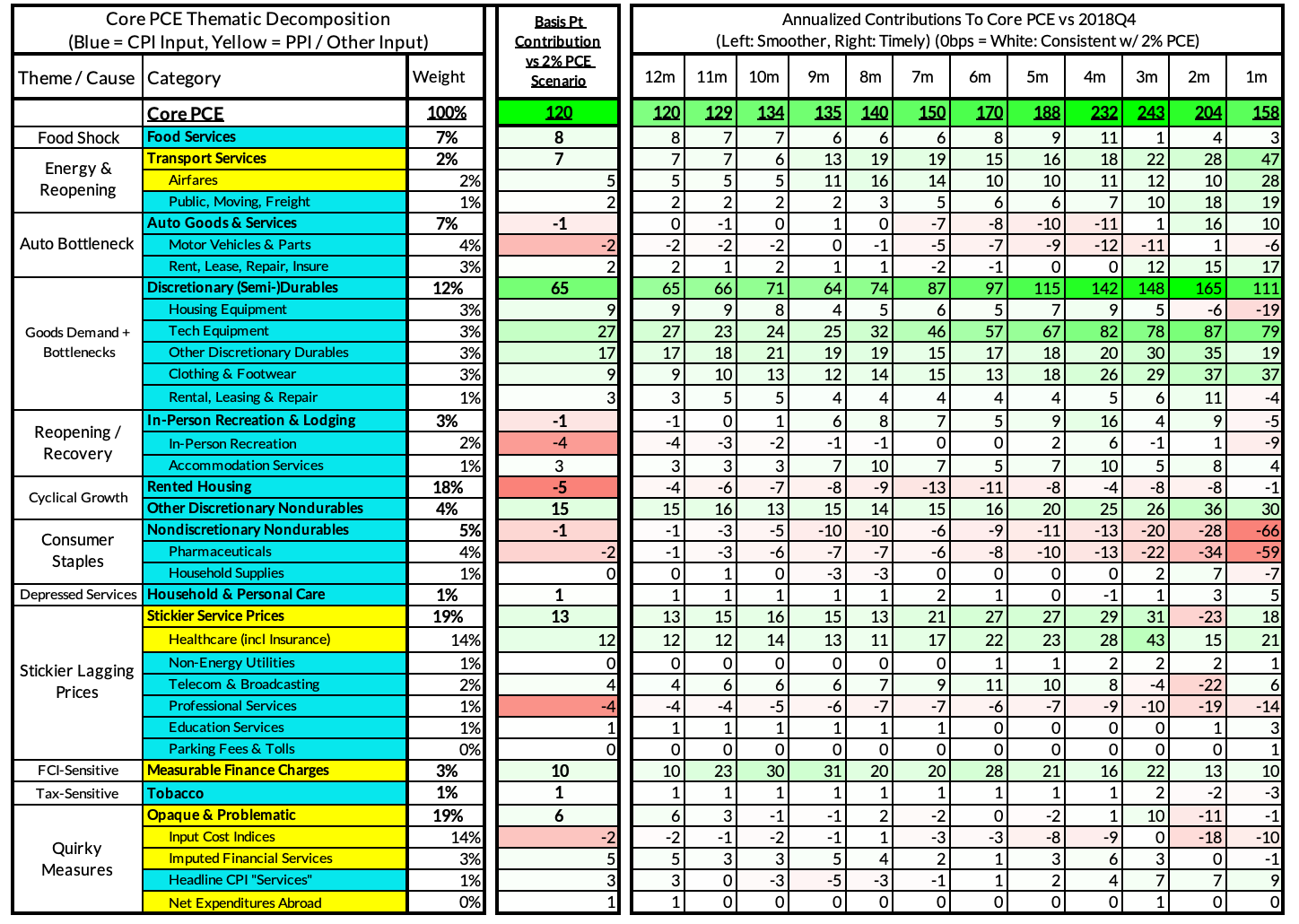

For the Detail-Oriented: Core PCE Heatmaps

Right now Core PCE (PCE less food products and energy) is running at a 3.20% year-over-year pace as of March, 120 basis points above the Fed's 2% inflation target for PCE.

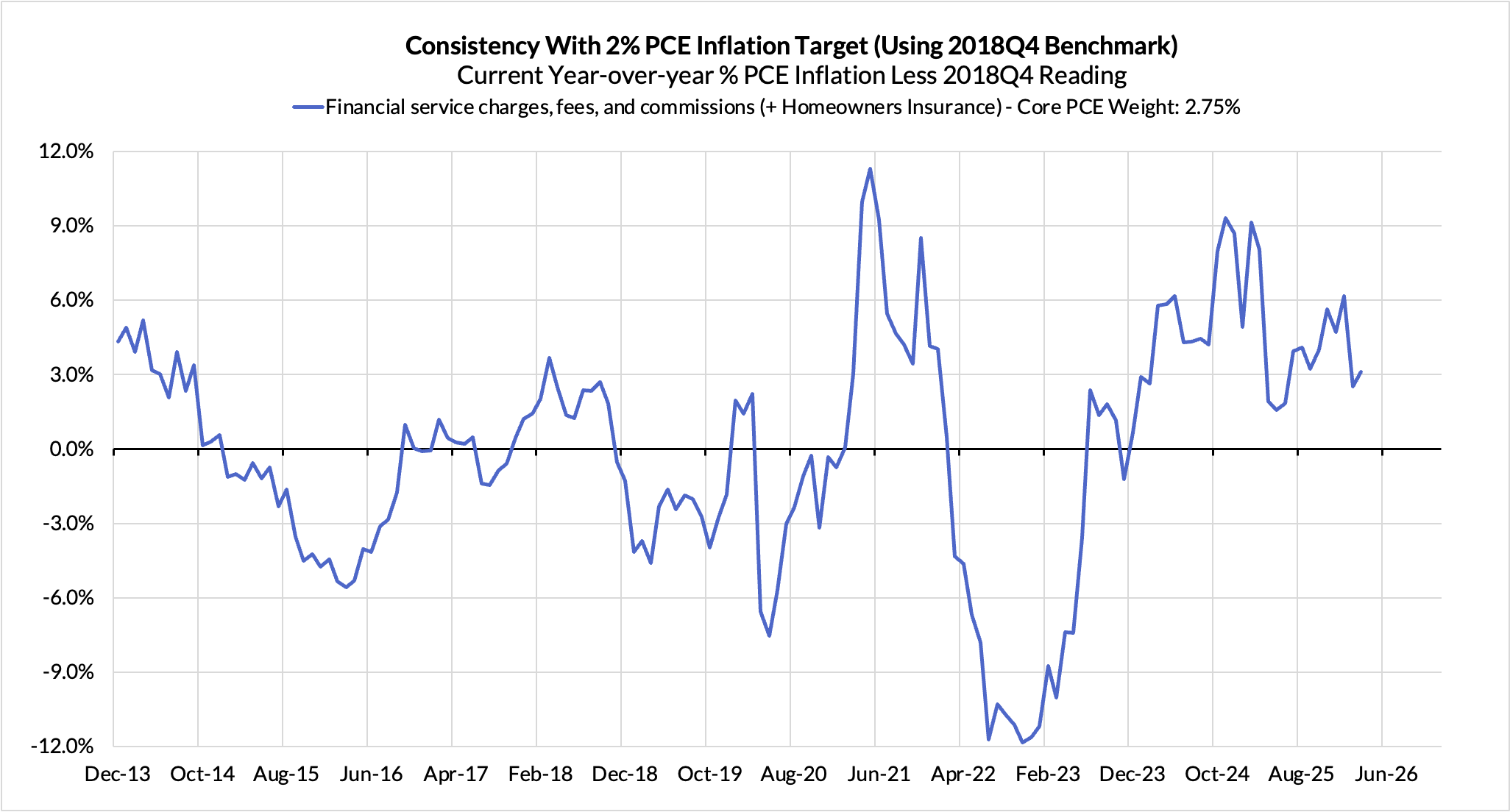

Equity market effects are adding 10 basis points to the overshoot.

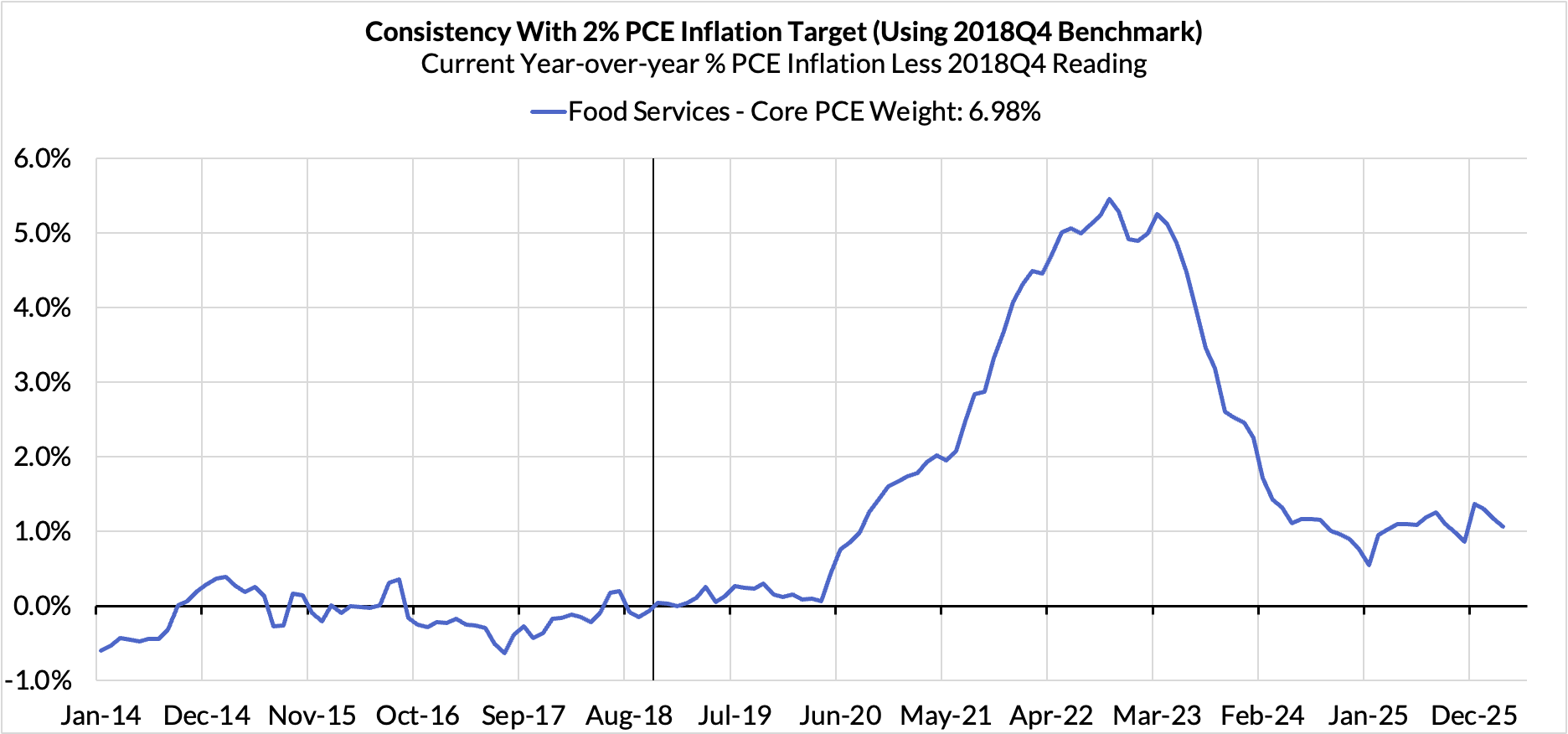

Food inputs likely adding 8 basis points to the overshoot.

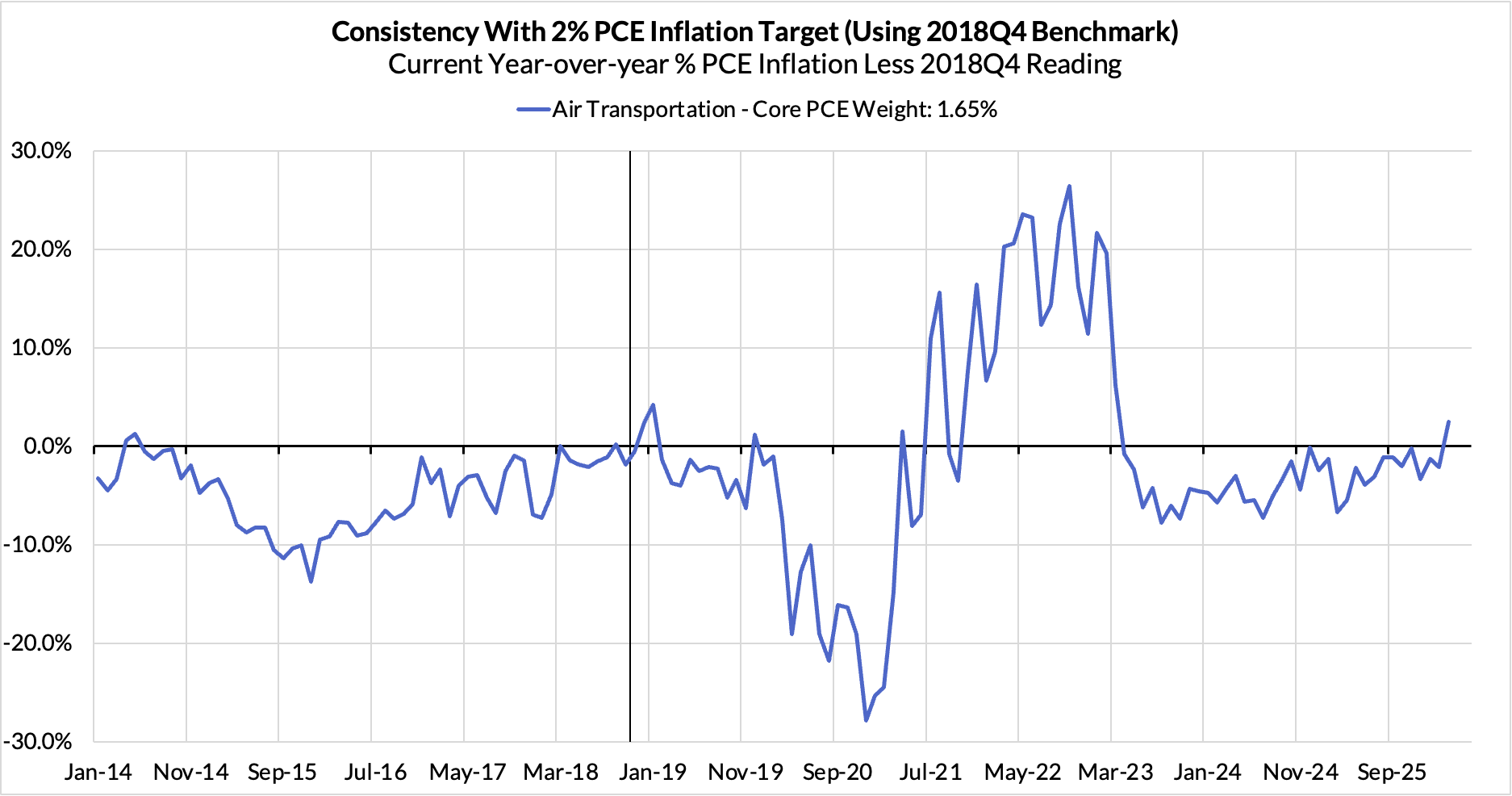

Airfares and moving services are adding 7 basis points to the overshoot

Telecommunications and broadcasting are adding 4 basis points.

The final heatmap below gives you a sense of the overshoot on shorter annualized run-rates. March monthly annualized Core PCE ran at a 358 basis point pace, a 158 basis point overshoot vs 2% target inflation.

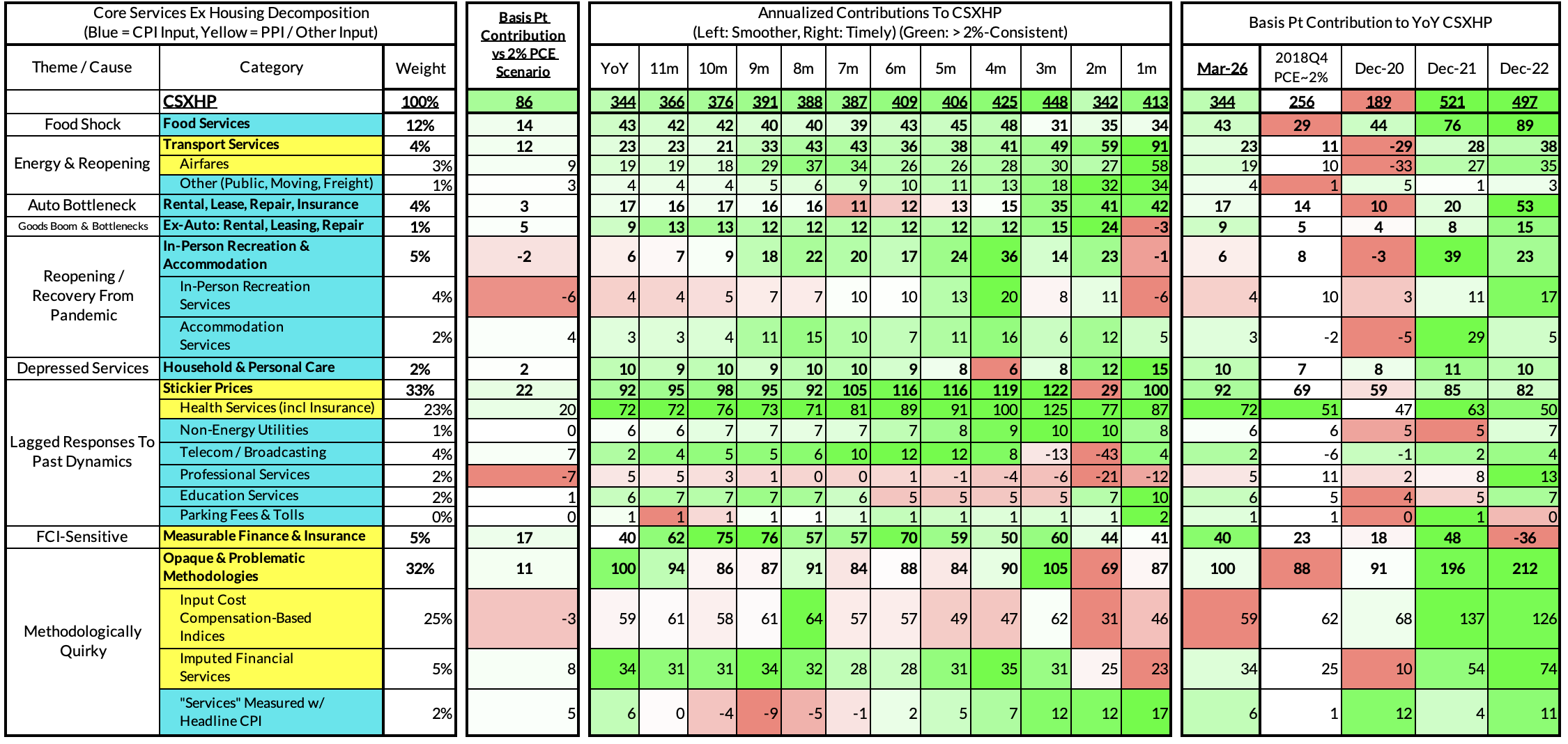

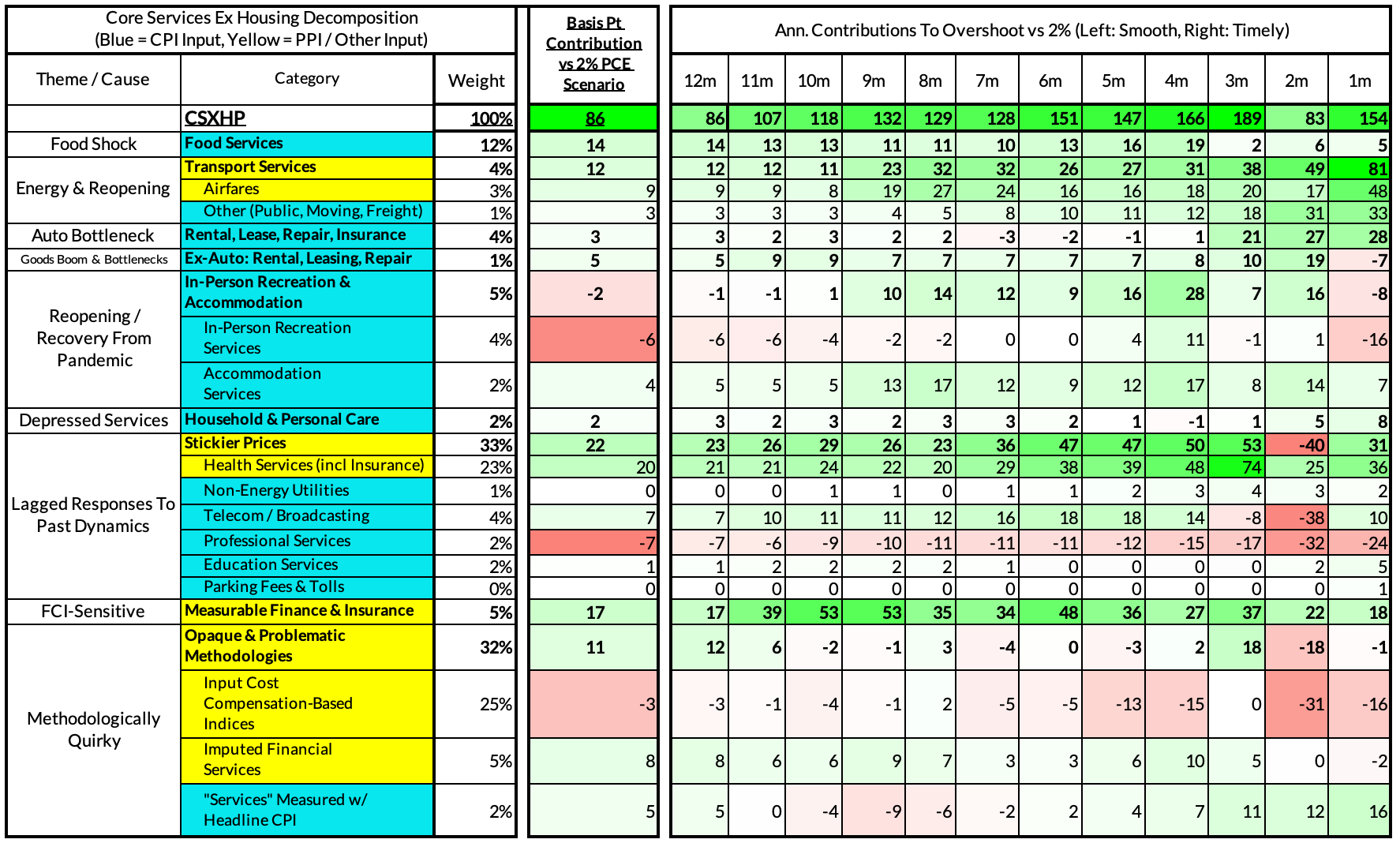

For the Detail-Oriented: Core Services Ex Housing PCE Heatmaps

The March growth rate in "Core Services Ex Housing" ('Supercore') PCE ran at a 3.44% year-over-year pace, a 86 basis point overshoot versus the ~2.59% run rate that coincided with ~2% Headline and Core PCE inflation.

The March monthly supercore ran at a 4.13% annualized rate, a 154 basis point annualized overshoot of what would be consistent with 2% Headline and Core PCE.

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.