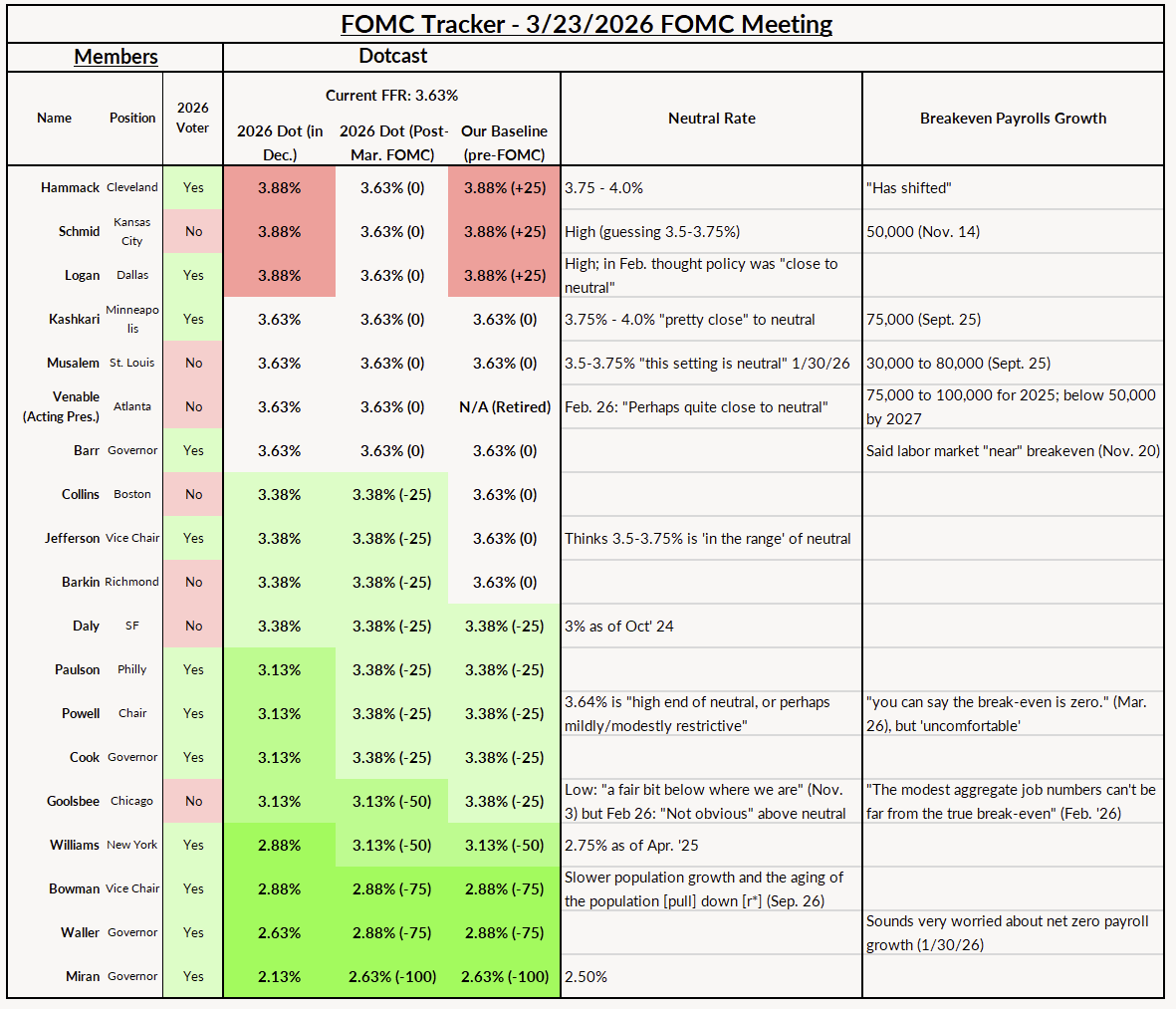

After last week's FOMC meeting, the hawks explain their dissents. Warsh is going to have a tough time reaching anything approaching consensus for rate cuts this year.

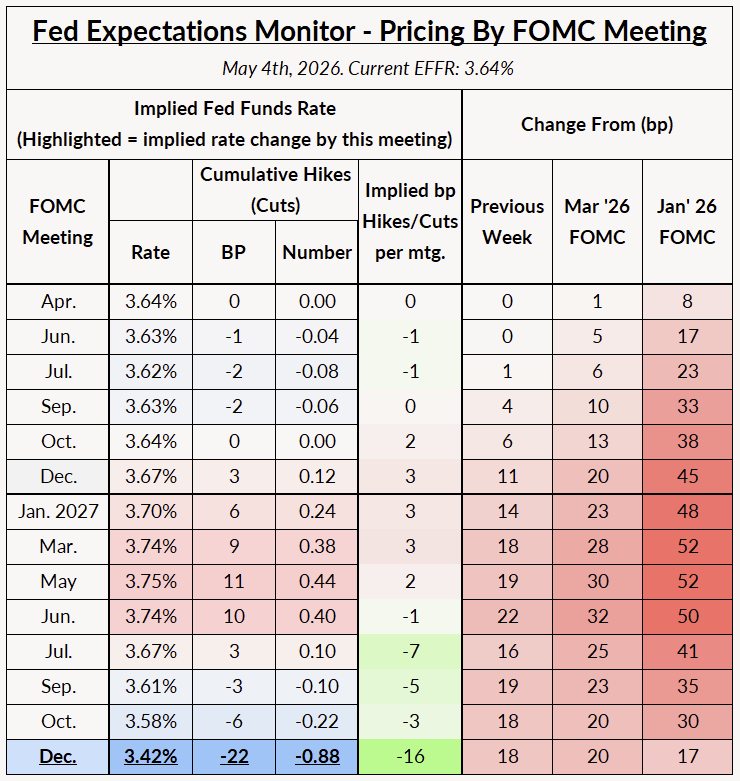

Market views: Market expectations for the federal funds rate path rose sharply after last week's FOMC meeting and PCE inflation report.

Markets expect little action on rates in 2026, but are pricing in a near-even chance of a hike by May of 2027.

Our views:

Our base case remains the same as previously: no cuts this year. Even before the Hormuz shock, the inflation picture was not looking favorable.

As we warned before the meeting, the Committee is likely more hawkish than they are letting on in public. This is still the case; the three hawkish dissents against the easing bias in the FOMC statement by Hammack, Kashkari and Logan are prescient of where the rest of the Committee is headed.

These dissents were only the voters—at the very least, Schmid, Musalem and Goolsbee would have joined them, but they are not voting members this year. Warsh is going to have a tough time reaching anything approaching consensus for rate cuts this year with that much opposition on the Committee.

After last week's FOMC meeting, the hawks explain their dissents.

Hammack and Logan both cited broader inflationary pressure prior to the Iran conflict (Hammack: "Inflation pressures continue to be broad based"; Logan: "Even before recent increases in the prices of energy and other commodities, those measures had been running meaningfully above 2 percent") to justify their opposition to an easing bias in the statement. Logan notably cited trimmed mean inflation (note that Dallas is the Regional Bank that puts out the trimmed mean inflation measure that Warsh likes to cite) as "running meaningfully above 2%"—it's hard to read this as anything other than a shot across the bow of Kevin Warsh.

Kashkari was slightly different—he had an optimistic view of the inflation picture prior to the war.

Joining the dissenters was Goolsbee, who sounds more like Hammack and Logan, citing broader inflation pressures.

Note: We use a LLM (Claude) to assist in extracting quotes from FOMC appearances. When given the appropriate context, we have found that Claude performs well in this context. We check and edit Claude's work. All of the analysis above this note was written by a human, without LLM assistance.

"Uncertainty around the economic outlook has increased in 2026 and makes the future path for monetary policy more uncertain, as well"

On her dissent: "I did not believe it was appropriate to include an easing bias around the future path for monetary policy"

On the "additional adjustments" language: "This forward guidance was put into the statement to signal a pause rather than an end to the easing cycle. I see this clear easing bias as no longer appropriate given the outlook"

On the labor market: "Activity in the US economy has been resilient thus far in 2026, and the unemployment rate has been little changed near my estimate of full employment since last summer"

On inflation: "Inflation pressures continue to be broad based, and rising oil prices present an additional source of inflationary pressure. Uncertainty around the economic outlook is elevated, with upside risks to inflation and downside risks to growth and employment"

"I supported the decision not to change the target range for the federal funds rate. However, I dissented from language in the post-meeting statement that suggests the next adjustment to the target range will most likely be a cut"

"I am increasingly concerned about how long it will take inflation to return all the way to the FOMC's 2 percent target"

On trimmed-mean / volatility-adjusted inflation measures: "Even before recent increases in the prices of energy and other commodities, those measures had been running meaningfully above 2 percent, leaving doubts about how long it will take inflation to return to target"

"The conflict in the Middle East raises the prospect of prolonged or repeated supply disruptions that could create further inflationary pressures. At the same time, the labor market has been stable, with low unemployment and payroll job gains keeping pace with labor force growth"

"Depending on which of these scenarios materialize, it could plausibly be appropriate for the FOMC's next rate change to be either an increase or a cut"

"In light of the two-sided risks to monetary policy, I believed the FOMC should not give forward guidance implying a bias toward rate cuts at this time"

"I supported the Federal Open Market Committee's (FOMC) decision to hold the federal funds rate at this week's meeting, but I dissented against the FOMC's action because I did not think it was appropriate to continue to include the following phrase in the policy statement: 'In considering the extent and timing of additional adjustments…'"

"Given recent economic and geopolitical developments and the high level of uncertainty about the outlook, I do not believe such forward guidance is appropriate at this time. Instead, the FOMC should offer a policy outlook that signals that the next rate change could be either a cut or a hike, depending on how the economy evolves"

On his pre-Iran-war views: prior to the conflict he was confident core inflation was headed back to 2%, and his March SEP showed one more 25bp cut in 2026

On the benign scenario (Strait reopens quickly, oil falls to ~$88 by year-end): Blue Chip forecasters expect core PCE at 3% in 2026, which would mark "roughly 3 percent for three years in a row"

In the benign scenario: "I could imagine the optimal monetary policy response to be holding rates where they are for an extended period and then easing only gradually, once the inflation shock has begun fading, having proven to be transitory"

On the adverse scenario (extended Strait closure): "Federal funds rate increases, potentially a series of them, could be warranted, even at the risk of further weakness to the labor market"

"I firmly believe that anchored long-run inflation expectations are necessary for achieving maximum employment and a vibrant economy"

On whether markets/White House should expect rate cuts: "I think we all need to be open-minded about where interest rates are going, because there's so much uncertainty coming out of the Middle East"

"There's so much uncertainty about the outlook in the Middle East right now, I don't feel comfortable signaling that a rate cut is in the cards. You know, we might in worse scenarios, we might have to go the other direction"

On the labor market: unemployment rate "has been at around 4.3%. It's bounced around a little bit for the last six months, so it seems like mostly the labor market is moving sideways"

"If this conflict is prolonged, or if it gets much worse from here, then I think that could be a real downward shift to the growth trajectory to the U.S. economy"

On supply-chain duration (citing a Minnesota CEO): even if the Strait reopened today, "it would probably take six months for their supply chains to return to something like normal"

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.