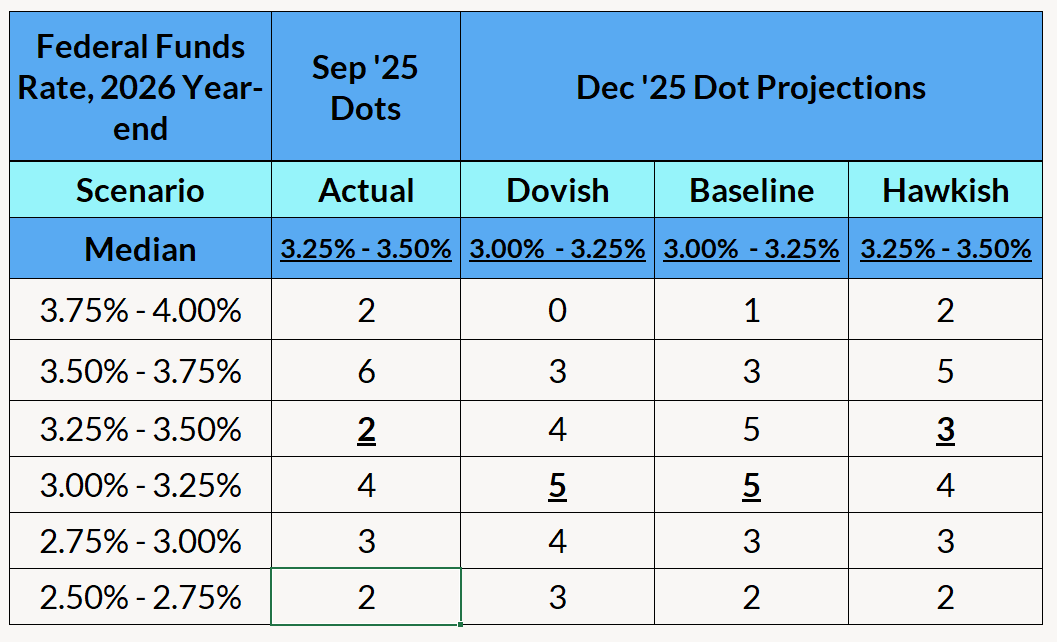

We expect the rate cut to be accompanied with a strong preference for optionality to pause at the next meeting, with no clear commitments to further cuts anytime soon. Our baseline case has the median projection at 2 more cuts in 2026, but with nine members projecting no more than one cut.

Note: Subscribers to MacroSuite received our FOMC preview at the beginning of the blackout period before each FOMC meeting. If you're interested in becoming a MacroSuite subscriber, please reach out to macrosuite@employamerica.org

Takeaway:

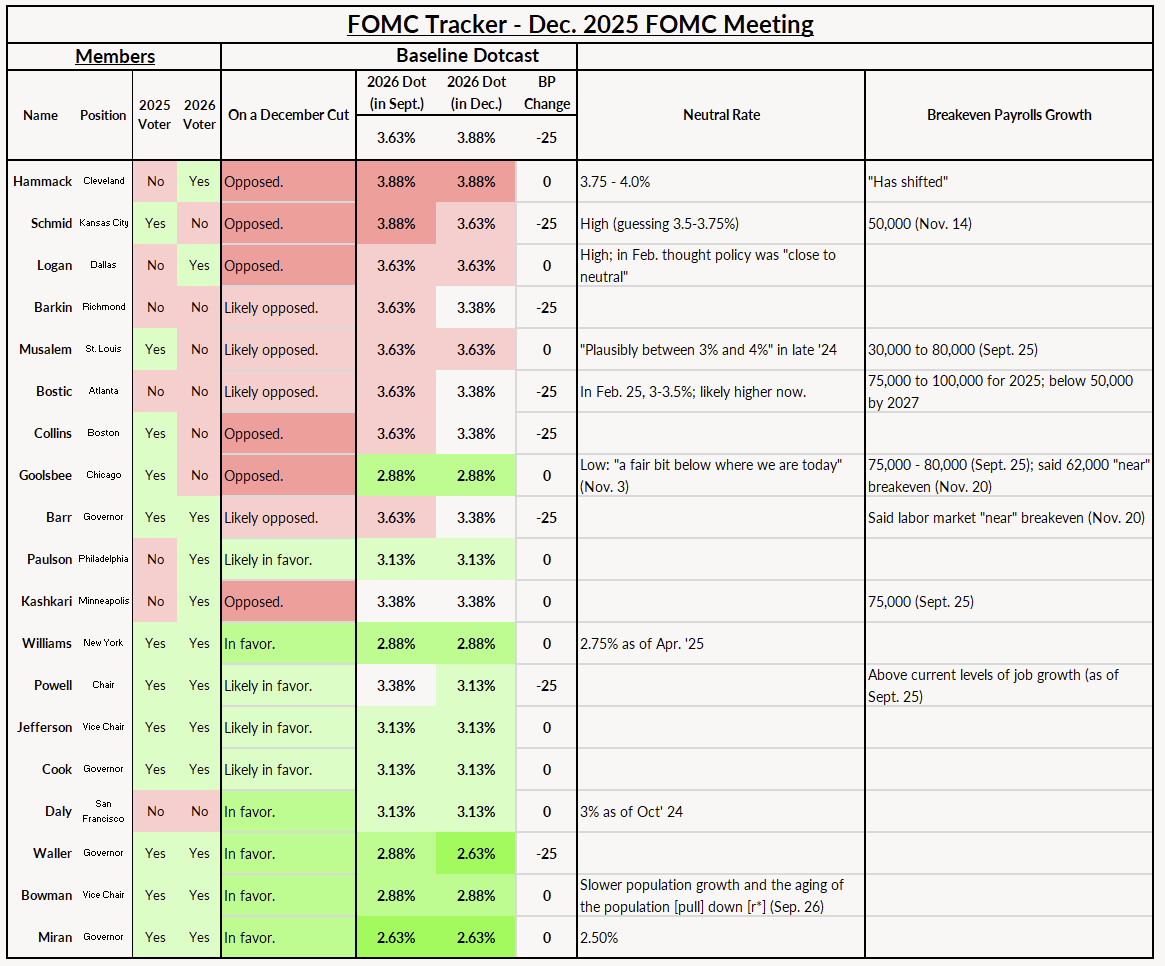

A December cut has been the base case ever since New York Federal Reserve Bank President John Williams hinted at one on November 21st, and looks to be a lock tomorrow. Despite the protestations of the regional bank presidents, enough key members of the Board of Governors, which carries disproportionate voting power, are in favor of moving.

We expect the rate cut to come with a significant amount of dissent, both in the votes and in the Fedspeak following the meeting. Schmid will surely dissent again, and some combination of Musalem, Collins and Goolsbee may join them. Hammack, Logan, and Bostic are also likely to be against a cut, although they don’t have voting power this year.

There isn’t a way of avoiding the deep disagreement amongst the Committee, but Powell may get some more marginal hawks on his side through the statement and press conference. We expect the rate cut to be accompanied with a strong preference for optionality to pause at the next meeting, with no clear commitments to further cuts anytime soon. Waller already has declined to signal further cuts in 2026 in his remarks.

Even after this week’s meeting, the disagreement amongst the Committee should continue into 2026. The disagreement amongst FOMC members is as much about the destination of the neutral rate as it is how restrictive policy should be. Because of this, we expect the dots for 2026 to range from 3.75% to 4.00% (one hike) to 2.50% to 2.75% (4 cuts), with clustering around 3.00% to 3.50%. Our baseline case has the median projection at 2 more cuts in 2026, but with nine members projecting no more than one cut.

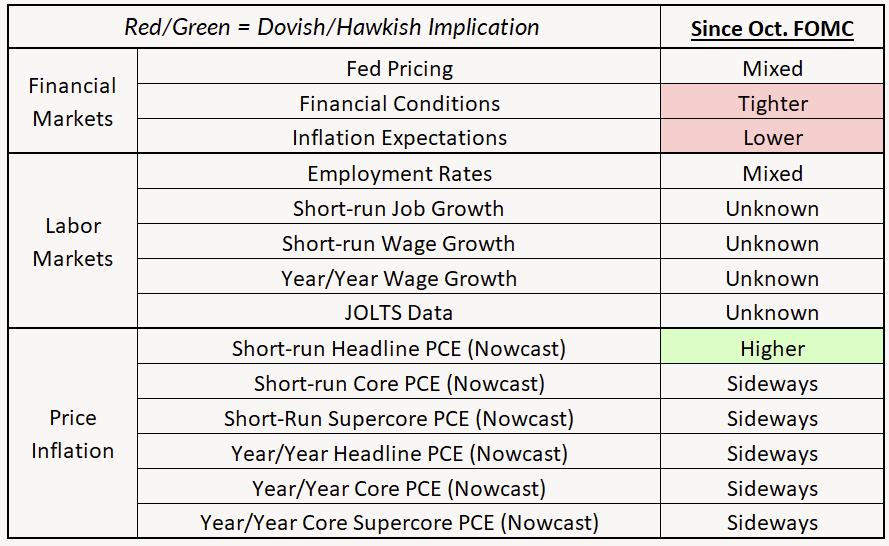

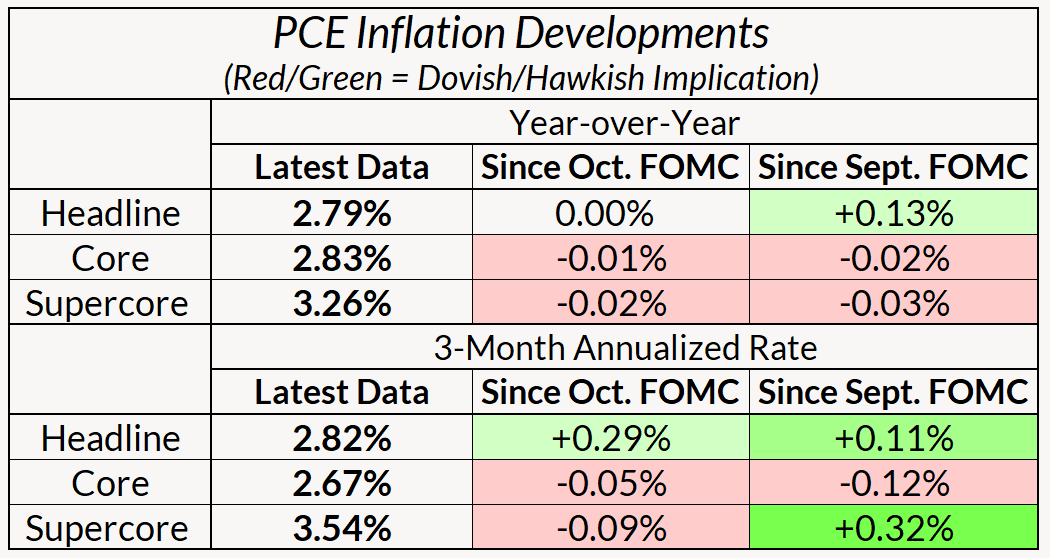

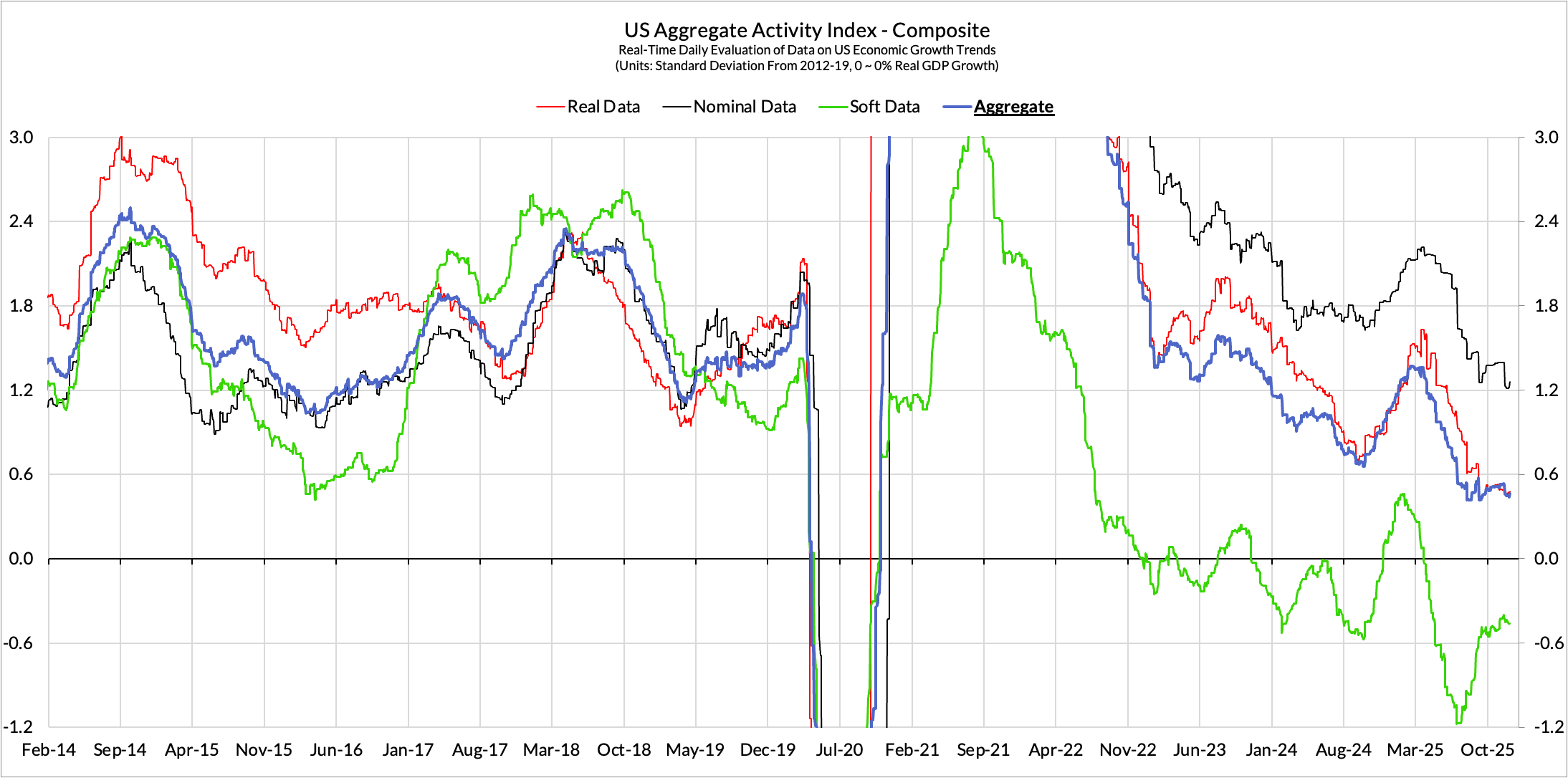

The intermeeting period has been notable due to the lack of data developments as surveys were either not collected or significantly delayed during the government shutdown. We will only have stale and significantly-delayed inflation and jobs reports for September. The September jobs data—already out-of-date—showed strong payroll gains but also an increase in the unemployment rate to 4.44%, not far from the 4.5% median FOMC projection from the September FOMC meeting.

In lieu of timely payroll and household survey data, the next-best source of data is unemployment insurance claims. There, initial claims remain low and show no signs of a spike in layoffs, while continuing claims have climbed slightly over the past couple of months. Retail sales increased by just 0.2% in September, and consumer confidence hit a seven-month low in November, with buying intentions for large purchases falling.

In the absence of the usual flow of data, the Fedspeak has seen hawks and doves alike retrench their positions. Regional bank presidents, who generally see higher neutral rates and are more concerned about inflation, have thrown cold water on supporting further rate cuts, while Board members (plus Williams and Daly) have been confident about tariff effects on inflation being transitory and the labor market being more shaky.

Key Fedspeak since the Last Meeting

Jefferson: “While still solid, I continue to view the risk to my employment forecast as skewed to the downside.” (11/17)

Barr: “I am concerned that we’re seeing inflation still at around 3% and our target is 2%, and we’re committed to getting to that 2% target, so we need to be careful and cautious now about monetary policy” (11/20)

Cook: “I view the latest reduction in the fed funds rate as another gradual step toward normalization. I see the current policy rate as remaining modestly restrictive" (11/3)

Waller: "January's a little trickier... you might see more of a meeting-to-meeting approach." (11/24)

Bostic: "I view the Committee's monetary policy today as marginally restrictive and favor keeping the funds rate steady until we see clear evidence that inflation is again moving meaningfully toward its 2 percent target."

Collins: “There are risks on the employment side.. if I saw evidence of more softening and weakness, I would take that seriously” (11/22)

Goolsbee: “In the near term I'm a little uneasy front loading too many rate cuts, and counting on (that) this will be transitory and inflation will go back down” (11/28)

Logan: "With two rate cuts now in place, I’d find it difficult to cut rates again in December unless there is clear evidence that inflation will fall faster than expected or that the labor market will cool more rapidly." (11/21)

Williams: “I still see room for a further adjustment in the near term to the target range for the federal funds rate to move the stance of policy closer to the range of neutral” (11/21)

Paulson: “Each rate cut raises the bar for the next cut.” (11/20)

Daly: "On the labor market, I don’t feel as confident we can get ahead of it... it’s vulnerable enough now that the risk is it’ll have a nonlinear change" (11/24)

Musalem: “I think there’s limited room for further easing without monetary policy becoming overly accommodative” (11/13)

What we’re thinking

With the unemployment rate already reaching 4.44% in September and retail sales and consumer confidence sending a downside signal, a cut at next week’s meeting is appropriate. Consumer spending faces headwinds in Q4 and Q1 as EV credits expire, government shutdown effects show up in the data, and job growth and immigration growth both slow. Between the “stag” and “flation”, we see “stag” as the bigger threat.

The division amongst the Committee headed into this week’s meeting highlights the need for the Fed Chair to command respect and credibility among the rest of the members of the FOMC. So far Powell has done that job admirably, and has wielded that respect to great effect (for example, at last year’s 50 bp cut in September). Hassett, who is at the time of writing supposedly tapped to be the next Fed chair, as of a few weeks ago levied accusations of partisanship at the Committee for thinking of not cutting in December. He’s not the most craven option out there, but he’s unlikely to be able to convince the rest of the Committee to pursue dovish policy (as opposed to Waller).

How Has The Data Evolved Since Last FOMC?

Labor Market Dashboard

For September 2025

Change from

Household Survey

Current

1M Ago

3M Ago

12M Ago

2019 Avg

Employment Rate (Prime-age)

80.7%

0.0%

0.0%

-0.2%

+0.7%

Unemployment Rate

4.44%

+0.12%

+0.32%

+0.35%

+0.77%

Sahm Indicator

0.23%

+0.10%

+0.07%

-0.27%

+0.22%

Black-white Gap

3.7%

-0.1%

+0.5%

+1.7%

+0.9%

Participation Rate (Prime-age)

83.7%

0.0%

+0.2%

-0.1%

+1.2%

Payroll Growth (3-month avg., thous.)

Current

1M Ago

3M Ago

12M Ago

2019 Avg

Total Nonfarm

62

+44

+8

-71

-104

Total Private

57

+41

-1

-37

-91

Government

5

+3

+9

-34

-12

Cyclical

-32

+15

-6

-25

-77

Acyclical

95

+29

+14

-45

-26

Wage Growth

Current

1M Ago

3M Ago

12M Ago

2019 Avg

Average Hourly Earnings (3m/3m)

4.0%

+0.3%

+0.7%

+0.1%

+0.8%

ECI Total Comp. (3-month)

3.8%

N/A

+0.2%

+0.4%

+1.1%

Atl. Fed. Median Wage Growth (yoy)

4.1%

0.0%

-0.1%

-0.6%

+0.4%

Indeed Postings Wage Growth (yoy)

2.4%

-0.2%

-0.1%

-1.1%

-0.9%

JOLTS

Current

1M Ago

3M Ago

12M Ago

2019 Avg

Hiring Rate

3.2%

-0.1%

-0.2%

-0.1%

-0.7%

Quit Rate

1.9%

-0.1%

-0.1%

-0.1%

-0.4%

Layoff Rate

1.1%

0.0%

+0.1%

0.0%

-0.1%

Job Openings Rate

4.3%

0.0%

-0.3%

-0.3%

-0.2%

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.