We expect the dots to move upwards, with most members that projected cuts in December taking a cut out of their projections. We see the median on the knife-edge, with half of the Committee projecting no cuts.

Note: Subscribers to MacroSuite receive our FOMC preview during the blackout period before each FOMC meeting. A public version of the preview will be released closer to the meeting. If you're interested in becoming a MacroSuite subscriber, please reach out to macrosuite@employamerica.org

As expected, the Fed will hold and signal an extended pause amidst uncertainty from the War in the Middle East.

We expect the dots to move upwards, with most members that projected cuts in December taking a cut out of their projections.

We see the median on the knife-edge, with half of the Committee projecting no cuts (and some projecting hikes). Most members projecting cuts will only have one cut.

A hawkish scenario may see some additional members projecting a hike this year (possibly Kashkari and/or Musalem moving from no cuts/hikes to a hike).

Even a more dovish scenario still sees some upwards movement in the doves' dots.

We still think the Fed will maintain an easing bias, but that timeline is getting pushed out. There may be talk about switching to a tightening bias, but it would take a few more upside inflation surprises to get there.

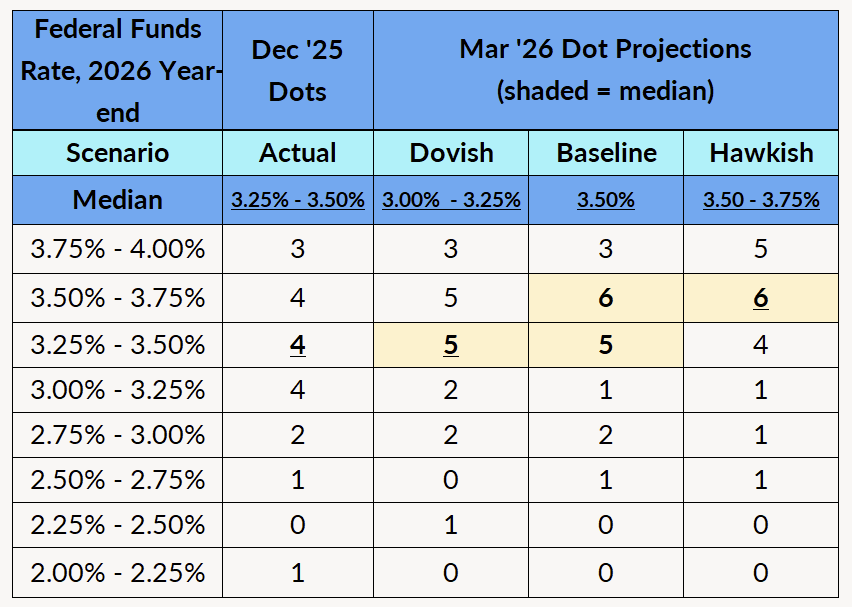

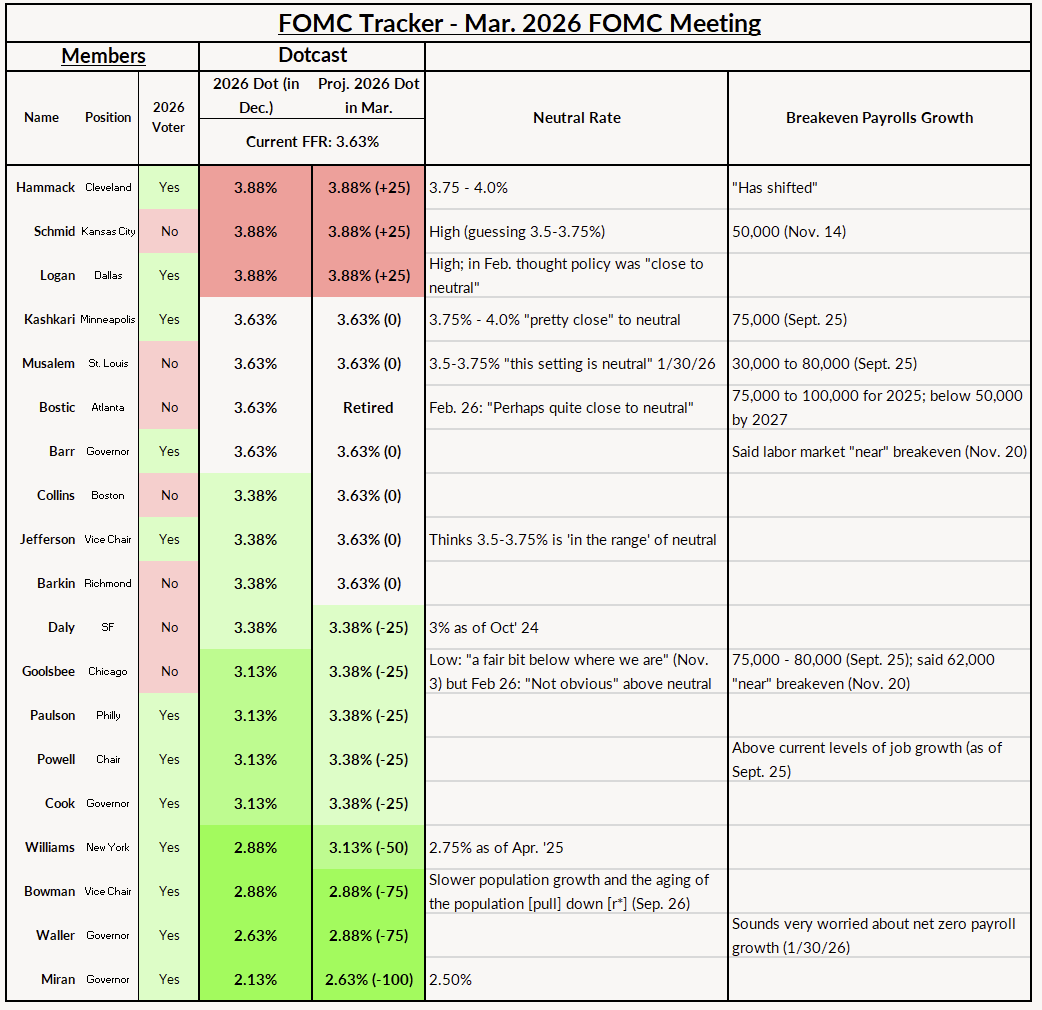

Note: 18 dots; Bostic has retired.

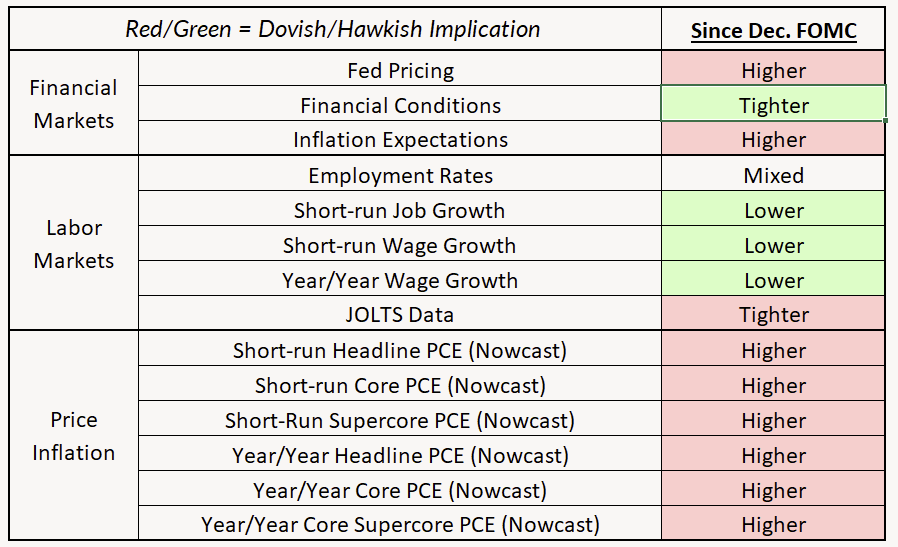

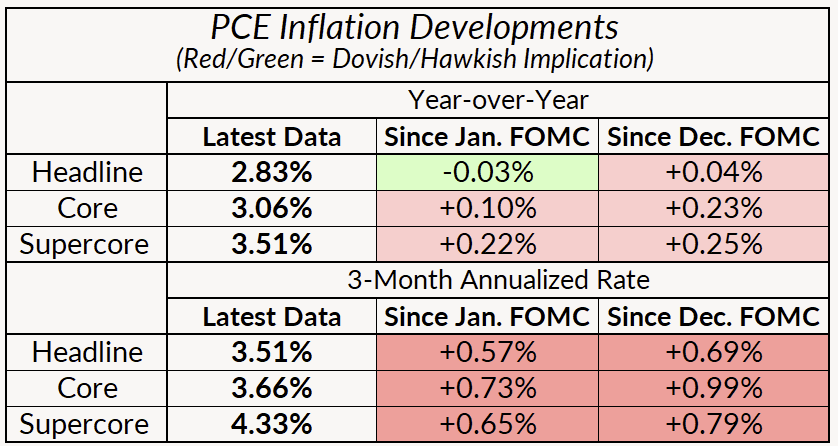

The inflation data that came in since the previous meeting was pretty ugly, and all of that precedes the conflict. Core PCE price inflation is at 3.06% on a 12-month basis, and 3.66% on a 3-month annualized basis.

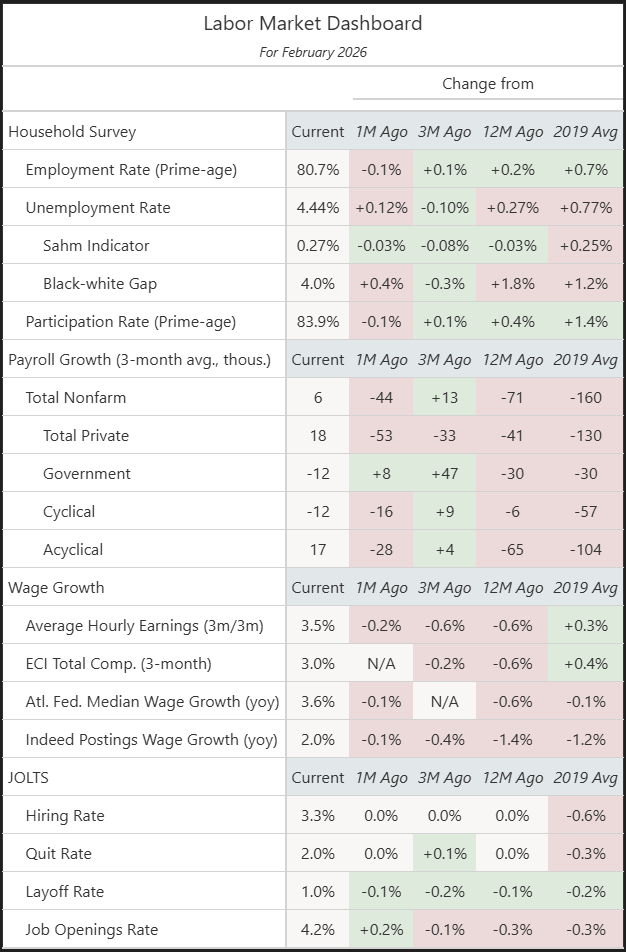

Although February's NFP print was ugly, by the time of the meeting next week, the Committee will have fully digested the quirks of the odd birth-death model changes and other factors contributing to the -92,000 payroll drop. The NFP print may give Waller and Miran more resolve to call for easing, but the hawks will be unconvinced.

We will be looking for signs that the Committee is taking the idea of hiking as the next move seriously. Will it be seriously discussed at the meeting and how many members pencil in a hike for this year? There will be some members that want it mentioned as a possibility if upside inflation risks materialize this year.

Fed Pricing and Dot Estimates

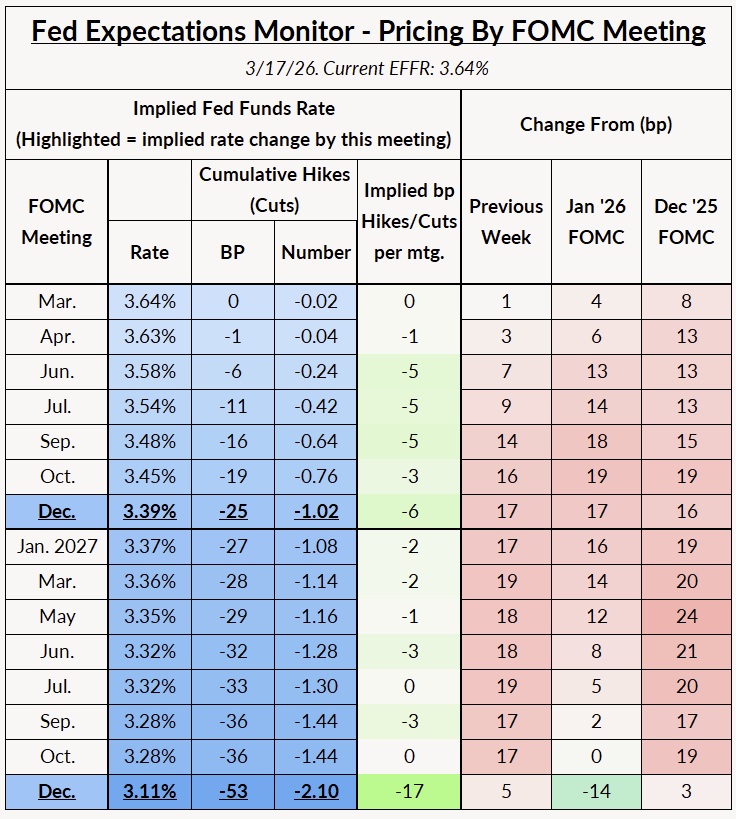

Over the past week, the market has removed a full cut from Fed pricing this year. Market pricing sees just 1 cuts this year and 1 cut next year, with those cuts most likely coming in the back half.

March comes with another round of the dot plot. Our baseline splits the Committee at nine for no cuts (or even a hike) this year, and nine seeing at least one cut (for a total of 18; Bostic is retired and has not been replaced).

We think the moderates (Collins, Jefferson and Barkin) are likely to move to no cuts this year, and most of the doves will move to one cut this year, with the thinking that a cut can come late this year "after the dust settles," as Austan Goolsbee would say. The Trump appointee doves (Bowman, Waller and Miran) continue to sound dovish and concentrated on labor market risk, writing off the inflation data.

We think the most hawkish (Hammack, Schmid and Logan) will stay put at projecting a hike this year. They will see the recent inflation data as confirmation of their beliefs. It's not out of the question for another one or two members who previously saw no change in the Federal Funds Rate this year to join them—Kashkari and Musalem are the most likely here.

Hawkish scenario: Kashkari and Musalem pencil in a hike for this year, and two of Goolsbee, Paulson, Powell and Cook move to no cuts this year.

Dovish scenario: One of Jefferson/Barkin/Collins maintains a cut this year, and a couple of Goolsbee/Paulson/Powell/Cook maintain two cuts—but there's still some hawkish movement among the doves.

Key Fedspeak since the Last Meeting

Bowman: "I was fine with holding at our January meeting, but now that we’ve seen that the labor market, maybe that was an anomaly" (3/6/26)

Waller, on a weak jobs report: "The question is why are you just sitting on your hands?... My job is trying to help the economy and achieve our dual mandate. And if the labor market's not looking good, then I have to make this trade off." (3/6/26)

Collins: "I do not see an urgency for additional policy adjustments, and I will be looking for clear evidence that inflation is moving durably toward the 2 percent target — something that might occur only over the second half of the year."

Goolsbee: "I remain hopeful, expecting that conditions will improve, that we'll start to see some progress on inflation, head us back to two percent, and by the end of this year that we would be in a situation that we could commence our march back down to something like the settling point, which is below where we are today." (3/6/26)

Kashkari: "Now, with the geopolitical events, we need to get a lot more data in... I had a lot of confidence up until a couple of days ago."

Williams: expects "overall inflation to come in at around 2-1/2 percent in 2026, then fall to 2 percent in 2027, as the effects of tariffs on inflation wane." (3/3/26)

Barkin: "If you can replace poultry workers, I think you've got a reasonably open job market." (3/5/26)

Daly: "The hopes that the labor market was steadying, maybe that was too much, and we really have to keep our eye on the labor market." (3/6/26)

What we’re thinking

The Fed's in a hard place. With the bad inflation data and the backdrop of geopolitical conflict, the case for cuts anytime soon has rapidly diminished. The labor market looks stable-ish, and the inflation data is pretty bad. We think there are inflationary risks to the upside, given the DRAM shortage, used car pricing, tariff effects, and now oil.

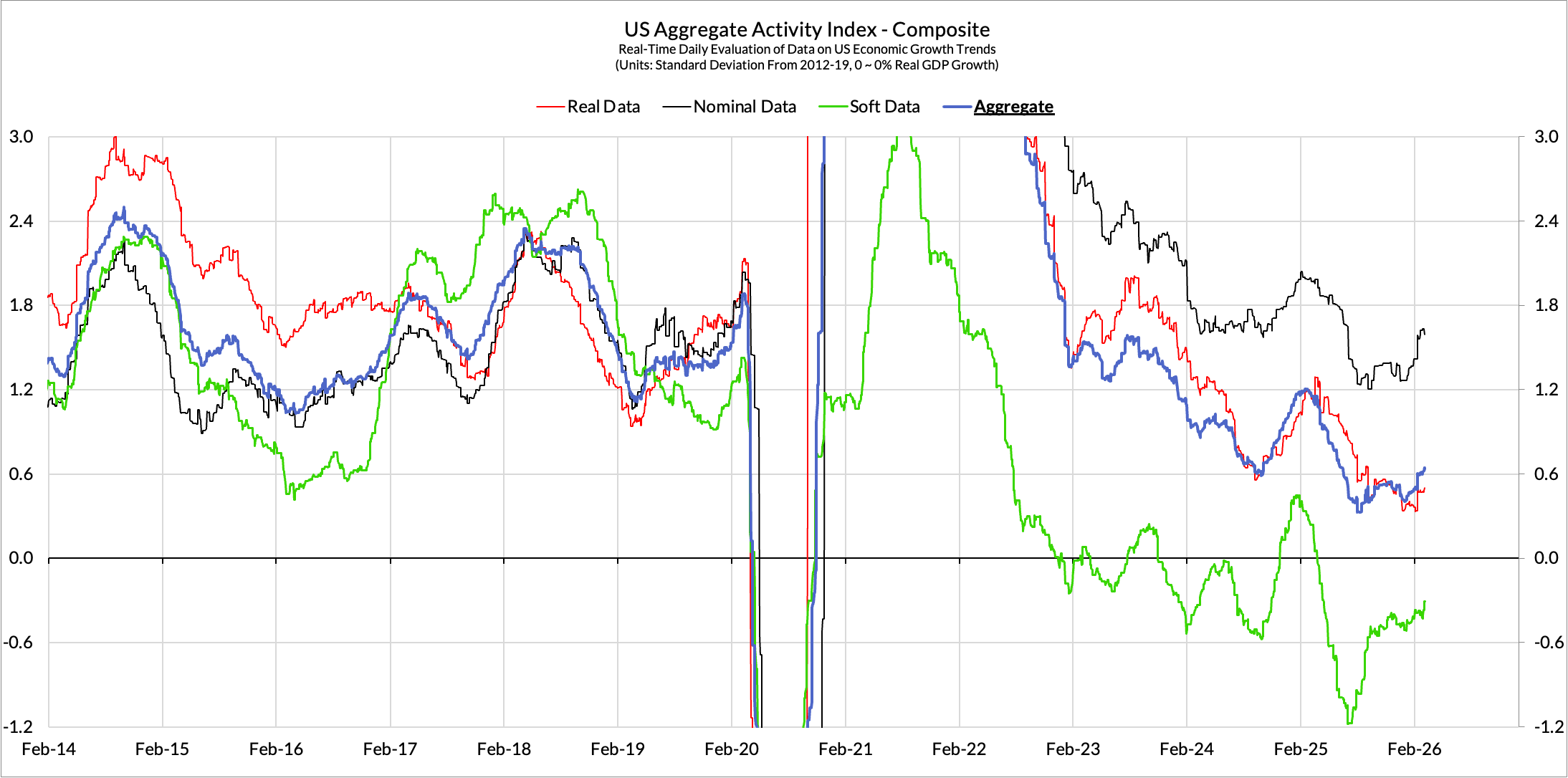

How Has The Data Evolved Since Last FOMC?

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.