September Supply Chain Monitor

Each month, we publish a public version of the donor-exclusive Supply Chain Monitor to better inform macroeconomic discussion about developments on the “supply side.”

Each month, we publish a public version of the donor-exclusive Supply Chain Monitor to better inform macroeconomic discussion about developments on the “supply side.”

Each month, we publish a public version of the donor-exclusive Supply Chain Monitor to better inform macroeconomic discussion about developments on the “supply side.” As this monitor is visually dense, we provide a guide to the structure, intuitions and methods of the Supply Chain Monitor here.

From a supply chain side, we are largely out of the pandemic. Most of the long, pandemic-era shortages have ended, outside of a few straggler sectors; logistics and lead times have recovered. Topline measures are all stabilizing – input costs, domestic production, and nominal imports – but slowly, as the pandemic recovery winds down. Under the hood though, there is substantial variation between different subsectors. Some sub-sectors are producing substantially above their pre-pandemic levels, while others are producing substantially below them. We also may be seeing the first stages of the push-pull between higher interest rates and industrial policy on the fiscal side. The Fed should remain attentive to the impact of high interest rates on the supply side as it considers the path of interest rates in 2024.

Auto production has been a central focus throughout the pandemic because of its outsized impact on measured inflation – especially measured core inflation. With the continuing resolution of the semiconductor shortage, production of finished assemblies (the series reported in the monitor below) has steadily grown.

Many expected this to lead to a broader loosening in the market for new and used autos, but disinflation has not come in as strongly as expected given the deflation in the wholesale market. This is due in part – according to the BLS – to auto dealers taking higher profit margins over the pandemic as they rationed a limited quantity of vehicles on price. However, part of the reason they are able to take those profit margins is due to the sheer volume of missing vehicles.

If the UAW strike does have an impact on the price of automobiles, it’s important that we be clear where it comes from. Near-term price increases in this market will more likely be a consequence of the actions of dealers, rather than OEMs. In fact, the price increases will most likely be traceable – as they have been all pandemic – to the actions of car dealerships rationing an unexpectedly-limited quantity of vehicles. If a strike means a cut to the quantity of vehicles rolling off the lines, opportunistic dealers may see this as an opportunity to further firm up their own profit margins.

Indexes of domestic production of oil and gas are increasing, and rig counts have recently begun to rise. Input prices have fallen back after reaching brief, sharp peaks when supply chains were taxed at the height of the 2021-2022 energy crisis. In fact, at that time, supply chain difficulties were frequently cited (alongside “capital discipline”) as a core reason why oil production was not rising to meet rising oil prices. As the prices for key inputs to further investment like steel pipe continue to ease, we can expect input prices in these industries to continue falling.

We can also see some evidence of the problem that we have been referring to as “grade skew” showing up in the rise in imports of refined petroleum products. Essentially, the grade of oil produced by the marginal US producer isn’t well-suited for making the products that the market is currently missing: heavy distillates like diesel. As markets for these refined products have tightened, we have seen a jump in the importation of refined petroleum products. As we argue in the article linked above, there are ways to use the Strategic Petroleum Reserve to mitigate some aspects of this problem.

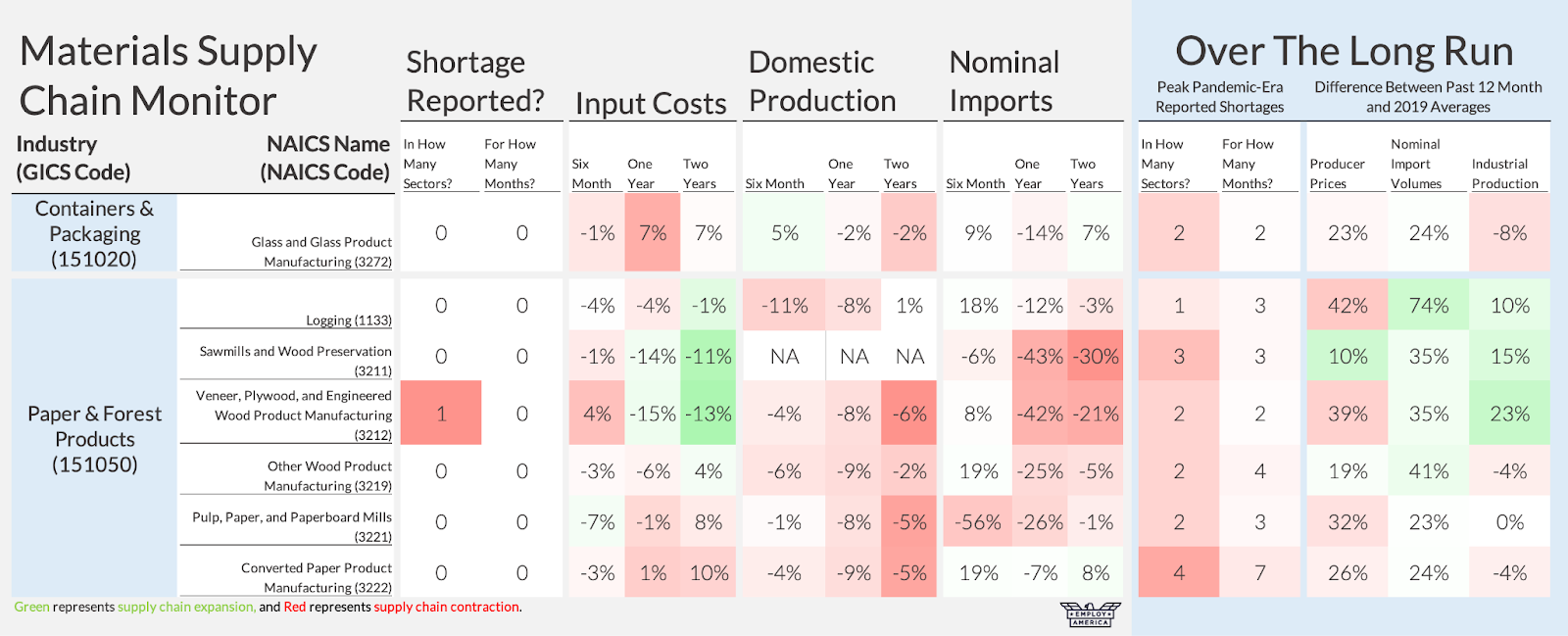

Early on in the pandemic saw extreme gyrations in construction materials, most especially lumber. Following the shortage and subsequent market volatility, much of the market for lumber has remained depressed. We continue to see evidence of that, in fading input prices, domestic production and imports for most paper and forest products. Interestingly, and unlike a number of other sectors, production in logging, sawmills and engineered wood product production is substantially above pre-pandemic levels.

For non-lumber construction materials, we see a situation where the US may be capitalizing on fading Chinese demand for concrete and cement amidst a rolling real estate slowdown. Domestic input prices have risen notably for non-lumber construction materials, but imports are picking up as global demand for construction supplies softens.

HVAC equipment is critical to construction and building repairs – especially as building upgrades like heat pumps play a critical role in the decarbonization transition – but is struggling to recover to even pre-pandemic levels of production. For much of 2022, this was reflected in news reports of HVAC parts shortages, but in 2023 imports rose substantially as US producers tapped foreign capacity. In terms of the supply chain for the broader economy, this is good news, but it is worrisome to see that despite being a “straggler sector” overall, domestic HVAC production is beginning to turn down again in recent months.

Earlier this year I argued that continued strength in investment in – and production of – heavy duty trucks would be a tailwind to the growth picture. So far, this seems to be panning out, with steady to accelerating growth in domestic production against steady input prices. This is exciting, given that production is increasingly shifting towards decarbonization-friendly vehicles. It’s not enough to make electric trucks available: firms have to have the investment dollars and the will to use them to replace an ICE truck with an EV truck. The fact that input prices for this industry have not risen nearly as appreciably as production suggests room to run before supply chains pose a binding constraint.

In the monitors below, we see continued acceleration in domestic production of a range of tech sectors – computers, communications and navigational equipment, semiconductors – while input prices have largely remained similar to pre-pandemic. Interestingly, the cost of manufacturing semiconductors does not seem to have been significantly impacted by the ramp up in production in response to the long semiconductor shortage. All of these sectors still have significant distances to close in order to catch up with pre-pandemic levels of domestic production, but so far the recovery in this sector appears to be resolving bottlenecks without overtaxing upstream supply chains.