We will most likely see continued strength in pricing for new and used vehicles through the next six months, owing to the sheer volume of “missing” automobile assemblies accumulated over the pandemic. If completions continue at a rate in line with the last 6 months of production, we will likely see new and used auto dealers retain the pricing power they have built up over the pandemic, without gaining more. This will mean little further inflation from new and used autos categories in inflation indices, but it will also mean little disinflation in those categories as well. The semiconductor shortage still poses a significant problem for foreign and domestic auto producers alike.

The Case of the Missing Automobiles

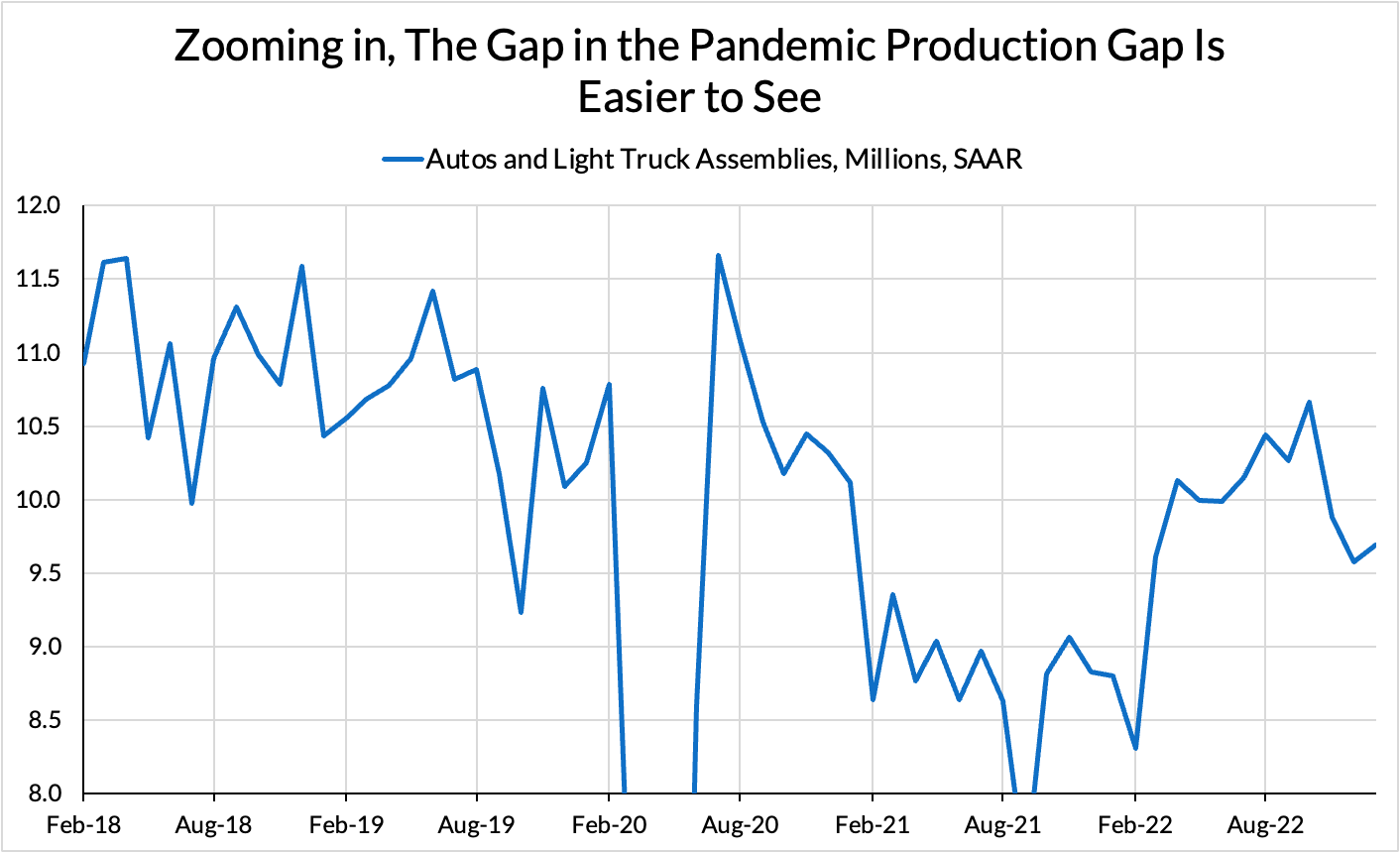

Lately, commentators have argued that it is no longer valid to attribute continuing inflation to “long over” stories like supply chain disruptions and the semiconductor shortage. Just looking at the rate of production of auto assemblies would seem to confirm this intuition; the SAAR flow rate is closer to its pre-pandemic levels:

So why aren’t prices for new autos swiftly falling, now that production has “recovered” and can presumably match present demand?

For the simple reason that an economy is made up of both stocks and flows. To dig in on this question, I ran the numbers on how many vehicle assemblies are actually reported as having been made monthly, to see just how bad a hole the pandemic has left the auto market in.

The first burst of missing production is the pandemic onset, when shop floors closed as businesses and politicians figured out what to do about the pandemic. From there, production roughly held steady with pre-pandemic rates until the semiconductor shortage began to bite in early 2021.

We have covered this particular shortage dynamic – where automakers canceled orders for necessary chips early in the pandemic, and found themselves unable to source new ones later on – extensively in other reports. There is also some evidence that the proximate physical capacity shortage in this case is, in fact, overseas. Recent ISM reports have confirmed this dynamic as well, with electrical and electronic components having been reported as "in shortage" for over two years at this point.

The bottom line is that, for 2021 and the first half of 2022, domestic auto assemblies remained substantially depressed relative to their pre-pandemic run rate. From the second half of 2022 on, production was able to recover sufficiently to approach that pre-pandemic run rate, but automakers remain hamstrung to go much further.

The problem is, there’s now a 5 million automobile air pocket.

So What’s Gonna Happen?

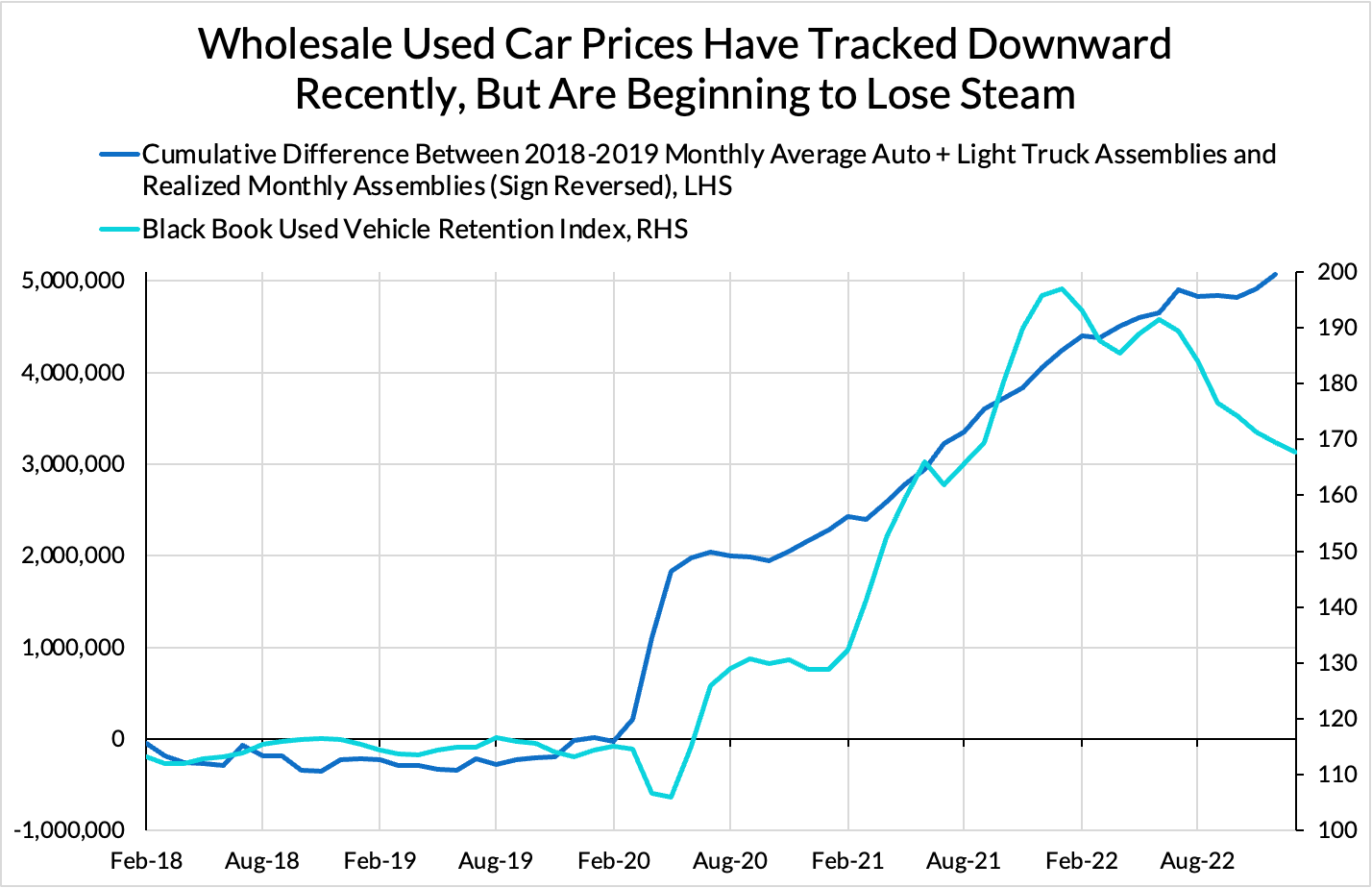

Many analysts hoped throughout 2022 (myself included) that 2023 would bring an outsized deflation in the prices of used and new automobiles. However, against anecdotal evidence of an increase in lease buyouts (which keeps new inventory from arriving in used auto markets) and this air pocket in new autos, we’ve begun seeing firmer-than-expected pricing in used auto markets.

An interesting aspect of this chart is that the Black Book Value Retention Index looks to proxy the percent of MSRP that used cars retain. Against rising MSRP for new vehicles in an environment of consistent shortage, for outright deflation in used car prices, we would need to see a sharper slope on the downside than the upside, which we do not see above.

So when can we hope to see significant deflation in used (and new) autos? Sadly, it might be a while. The two situations that seem most likely from here are either:

- The Bad Scenario: Lower assemblies become normal, and the price of new autos remains durably high, pushing the marginal cost-sensitive buyer into the used car market, and the prices of related services continue accelerating

- The Good Scenario: Assemblies ramp substantially above 2018-19 levels, eventually leading to price corrections in first the new, then used, car markets.

This second path will take some time, as well as incentives. How this all evolves over the next few years with changing preferences and various production challenges and incentives around electric vehicles is hard to predict. In the meantime, it seems reasonable to expect firm prices in these categories for the next few quarters. This is frustrating from the perspective of inflation management.

Can The Fed Help Here?

This also may be a market in which the Fed’s choice to pursue higher interest rates can contribute to disinflation at the level of a specific market. But how they do so in the near-term is hard to see. We don’t yet have Fed data for moves in consumer credit since overnight rates have moved north of 4%, but the existing data is suggestive. As of last September, rising interest rates had yet to move used auto finance rates out of their previous-decade range.

Interest rates for new autos are still considerably below pre-pandemic levels, which has helped support increasing loan sizes, which in turn provide the support for higher prices.

Those waiting on the Fed to resolve this issue may end up waiting just as long as those holding out for increased production to resolve it. In the meantime, we may not get the motor vehicle disinflation many of us have been hoping for.