Introduction

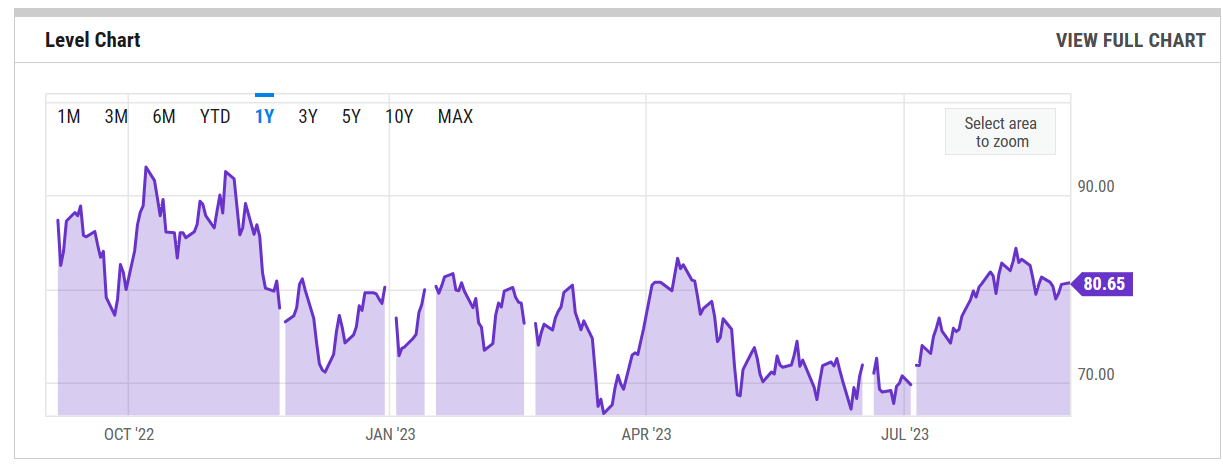

Oil markets have always been a geopolitical concern. Widening crack spreads (reflecting a tighter market) suggest that the emphasis today may be on the “geo,” rather than the “political”, as specific grades of oil—heavy or light, sweet or sour—are associated with specific geographies complicating the overall petroleum market picture in policy-relevant ways. Since hitting highs above $120 in the wake of the Russian invasion of Ukraine last year, the spot price has mostly settled into an acceptable range between $70 and $90 dollars for the past twelve months.

As summer driving season comes to a close, we have not retraced last summer’s gas price peaks. This stability is worth celebrating, but upside price risks loom over the coming twelve to twenty-four months. As we recently wrote, “Commodity price effects tend to have particularly asymmetric passthrough implications, rockets on the way up and feathers on the way down…” The recent price trend upwards in crude coupled with tight crack spreads in the refined products market (diesel and fuel oil particularly) are worrisome trends deep within an economy that has proven remarkably resilient over the rocky post-pandemic era. If the capacity to refine crude into diesel and other fuels is further inhibited, then “the nascent disinflationary impulse could be jeopardized and could even reverse into a new inflationary impulse.”

To manage this looming price risk, the Biden Administration should consider two policy options. First, it might be prudent to relax the price cap on Russian oil to unlock some production of heavier grades of crude. Second, the Department of Energy (DOE) should expand its ability to make long-term fixed-price acquisition contracts and the ability of the Strategic Petroleum Reserve (SPR) to take in “sweet” grades of oil.

The Refined Products Crunch

Oil is a complicated market because the prices of inputs and the prices of outputs all matter to different constituencies. The complexities are visible as differences in price for different grades of refined petroleum products and the spread in value between different refined products—the “crack spread.” The crack spread can tell us important things about trends in refinery capacity and product demand. Pinpointing the exact causes of wide crack spreads can be a difficult mix of guesswork and logic, but Rory Johnston recently laid out a highly plausible theory:

Middle distillates continue to drive the bulk of refiner profitability (as they have for most of the past 18 months) and high-sulphur fuel oil is abnormally strong at -$5–10/bbl (it’s almost always negative) given last year’s collapse. While demand is likely playing some role in HSFO’s recent strength, these latest shifts almost surely reflect the knock-on effects of the OPEC+ and, particularly, Saudi production cuts.

The difference between the relative value of oil middle distillates (diesel, gasoil, jet fuel, etc) and residual fuels, like HSFO last fall vs. today, tells an especially interesting story about the refining sector and what’s currently driving crack spreads. Last fall, diesel cracks were sitting around $50/bbl, while HSFO cracks plummeted to nearly -$40/bbl—residual cracks are virtually always negative, but not typically *that* negative. As discussed at the time in Refiners Unbalanced Barrel, global refineries were running so hot as a proportion of pandemic-weakened capacity that huge volumes of HSFO were being spat out as unwanted byproduct, crushing the relative value of that market. Eventually, pandemic-delayed new capacity came online and diesel demand weakened through the 2022/23 winter, which allowed that balance—diesel cracks fell and HSFO cracks recovered.

Now, diesel cracks are back to that $50/bbl level and HSFO cracks are super tight, around $5–10/bbl. Unlike last fall, this doesn’t appear to be a refining capacity issue—or, at least, not in isolation. Rather, it looks like the driving factor is those production cuts from OPEC+ and Saudi Arabia, which were indeed tilted toward heavier crudes. These crudes do have a naturally higher cut of residues like HSFO, which helps explain the HSFO tightness—but diesel? HSFO is a key fuel of the global maritime shipping industry and also a feedstock for cokers, specialized refinery equipment that converts those low-value fuels into higher value fuels—like diesel.

In short, tight crack spreads are a downstream consequence of recent cuts to the production of medium to heavy sour crude by Saudi Arabia and Russia. There is little the SPR can do in this situation because of the kinds of oil it stores. Releasing anything but heavy or medium sour is unlikely to resolve this specific situation, and could even prove counterproductive depending on the reaction of refineries and refined product markets to further grade-skew in domestic oil markets.

One policy mechanism that is capable of shifting grade-skew in oil markets, currently available to the Administration, and capable of working on the relevant timelines is to relax the Russian price cap. It’s encouraging that the Treasury Department has communicated a willingness to adjust the price cap in light of market conditions.

Acting Assistant Secretary of Economic Policy, Eric Van Nostrand, just reiterated that flexibility stating, “We come to this policy with humility and recognize these markets can change rapidly. We also know, like with all of our measures, Russia will attempt to evade the price cap. We remain vigilant in monitoring oil markets and the whole Coalition remains focused on enforcing our sanctions.”

Whatever the exact mechanism, given the tightness in the market and the announcement of further cuts by Russia and Saudi Arabia—it might be the right time to consider relaxing implementation or enforcement to unlock increased heavy crude production, at least in this interim period while we wait for additional refining capacity to come online.

It’s of course, impossible to know for certain whether the Russian cuts are undertaken in concert with Saudi Arabia, or in response to economic incentives related to the price cap and the prices available in ex-G7 oil markets, or what can be shipped without G-7 participation. Perhaps they were undertaken in an attempt to narrow the differential between Urals crude and Brent. In any event, Treasury has a wealth of proprietary data to examine both the impacts (and success) of the price cap as well as how economic actors are responding to it.

Whatever the motivation, if relaxation of the enforcement or implementation of the price cap can unlock production of some heavy or medium sour crude from the Urals, it may be warranted. Whether or not a tough sanctions regime can withstand another energy inflation shock remains to be seen. But some short-term relief to mitigate the likelihood of a substantial shock could help the regime endure.

The exact mechanism may be a relatively minor policy shift like relaxing enforcement or major shifts like increasing the price of the cap. These may seem like capitulations, but it’s important to understand that the price cap functionally operates in a manner to increase the bargaining power of external actors purchasing and contracting with Russia. In a higher price environment, that bargaining power decreases, potentially pushing countries to ignore the cap entirely. Accordingly, it’s helpful for the long-term legitimacy of the cap to nimbly and flexibly respond to market conditions rather than incentivize nations to work around it and undermine its legitimacy.

The exact choice is up to Treasury and other G7 nations implementing the cap to decide, but overall, the goal should be to unlock barrels of heavy to medium sour from the Urals in order to stabilize grade-skew for domestic refineries. And beyond that, the Administration can take actions to build its ability to stabilize the domestic crude picture long-term through the SPR.

Improving Long-term Acquisition Capacity at the SPR

Though the current oil market issues demonstrate that there are limits to the kinds of oil market problems that the SPR can resolve, that shouldn’t take any energy away (no pun intended) from the Biden Administration’s historic efforts to mitigate oil price volatility and boost domestic production using the SPR. At the end of last year, President Biden reiterated a commitment to use the certainty of SPR contracts to boost domestic production:

“fixed price contracts... will protect taxpayers and help create certainty around future demand for crude oil. That will encourage firms to invest in production right now, helping to improve U.S. energy security and bring down energy prices that have been driven up by Putin’s war in Ukraine.”

The SPR’s acquisition authority remains well-suited to carry out that policy goal. The successful execution of fixed price contracts was a massive positive step forward for the DOE. With this demonstration of improvement in bureaucratic capacity, the next step is to use that bureaucratic capacity to create a permanent ability to boost domestic production through strategic use of acquisition authority. Right now, there are two specific actions DOE should strongly consider: (1) execute a long-term fixed price contract; and (2) explore a “swap” of sour crude for sweet to orient the caverns more towards domestic short-cycle production.

1. Executing a Long-Term Fixed Price Contract

Now that the DOE has successfully executed two forward fixed price contract acquisitions, it should leverage this know-how to establish better energy policy for America. It’s time now to show that the DOE can conduct a long-term contract, the kind that could ultimately be utilized to incentivize producers towards additional production and provide much-needed structure to American oil markets.

The DOE may balk at committing itself so far out—uncertainties ranging from unforeseen releases, the return of exchange barrels, or maintenance could arise that complicate intake into the caverns. Fortunately, this is all the more reason to build the institutional capacities to execute on long-term contracts—the further out the contract is, the larger a delivery window DOE can provide without incurring any considerable cost. Furthermore, DOE can and should communicate ahead of time an intention to release the producer from the obligation to deliver if tight market conditions necessitate it. This provides valuable optionality for both the SPR and the broader market. DOE has the incidental contractual flexibility to manage the complexity of a longer-term contract.

Another option would be to attempt a more novel method of acquisition through a futures contract and a swap. DOE could purchase a WTI futures contract or issue a solicitation for equivalent contractual terms. This would have the benefit of targeting one of the most liquid crude benchmarks and a relatively thick part of the curve. This would mean acquiring sweet light crude, rather than the sour that DOE has most recently acquired. If DOE must acquire sour crude to maintain cavern homogeneity, it could issue a follow-up differential solicitation to swap the sweet delivered at Cushing for sour delivered to Big Hill.

Admittedly, this would be a complicated undertaking. The date of the contract should roughly be the length of the production cycle for short-cycle shale production. That means somewhere in the realm of eight to fifteen months would be appropriate—a physical settlement date between May and December 2024 seems ideal. At minimum, DOE can and should conduct a forward fixed price contract dated between May and December of next year. Though DOE is unlikely to acquire at a volume to move the production frontier in a meaningful way, building the institutional capacity is a critical next step. Should DOE receive an appropriation or money from future releases, it can deploy that institutional capacity swiftly to boost short-cycle US shale production.

2. Orient the SPR Caverns to Sweet Light Production

Another approach for the SPR is to intentionally target purchases of grades of oil commonly produced by short-cycle shale or “tight” oil. As it stands, recent acquisitions have all been for sour crude—typically produced offshore in the US Gulf Coast (USGC)—but that is a consequence of the history of the US oil market, not a plan for its future. Over the past ten years, the bulk of US domestic production has shifted to shale, formations of which usually produce light sweet crude. These short-cycle wells are relatively easier and cheaper to ramp up and ramp down than the large-scale deepwater wells that preceded them, which should make them more amenable to policy influence. Ensuring that our institutions for stabilizing the oil market are able to make the best use of our most abundant domestic resources is key for long-term policy success.

If “preservation of cavern homogeneity” is the binding constraint from procuring more sweet light crude, DOE should explore whether certain caverns can be drained of sour crude with sweet to replace it. After identifying such caverns, DOE would have several technical and policy options to conduct a swap. An exchange could work—as recently as last year, DOE conducted an exchange where the grade released was different than the grade received. Alternatively, DOE could simply prioritize those caverns in the event of a future release. Again, the exact mechanism should be determined based on the operational constraints of the SPR and the multiple policies it must balance. The end goal should be to reorient the caverns so that the SPR has the flexibility to directly target the short-cycle shale patch.

Conclusion

Today, oil prices face upside risks, while domestic refinery capacity is squeezed by a relative paucity of heavy and high-sulphur crude. This presents unique risks to the inflation outlook—especially if we see significant increases in the price of logistically-critical diesel and bunker fuels.

In the immediate term, it is worth exploring relaxation of the Russian price cap in order to unlock some heavy or medium sour crude from the Urals. Furthermore, action can be taken now by DOE to ensure the SPR can target domestic crude production more effectively.

Since its historic step for the power and flexibility of the DOE as an oil market participant, DOE has dealt in contracts less to the US production landscape and has yet to really flex its muscles as a strategic purchaser. The natural next step is to use this newfound power and flexibility to secure a more stable and reasonable US energy policy.