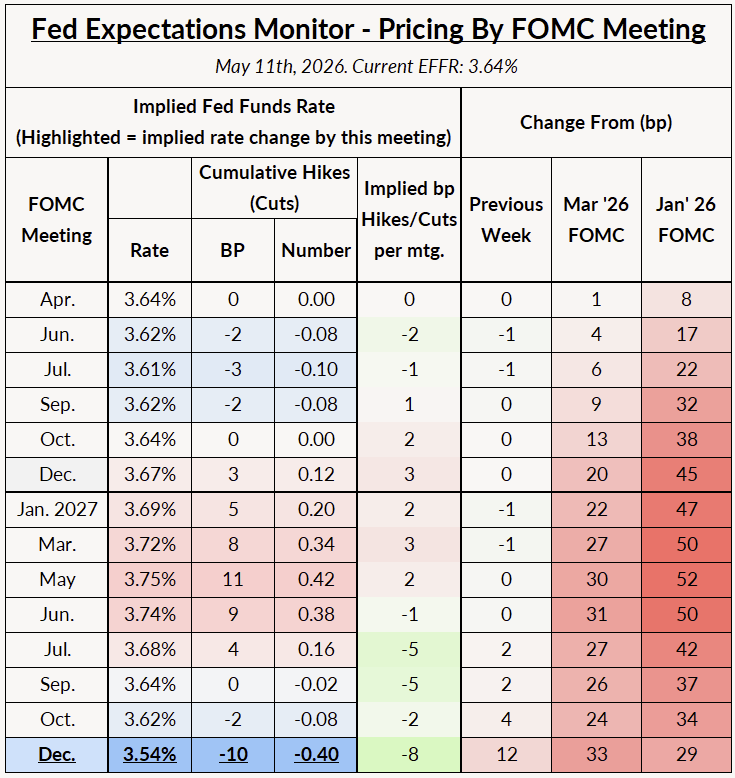

Market views: Market expectations for the federal funds rate path were largely similar to last week.

Markets expect little action on rates in 2026, but are pricing in a near-even chance of a hike in 2027 H1.

Our views: Our new base case: no cuts in 2026, a hike in 2027H1.

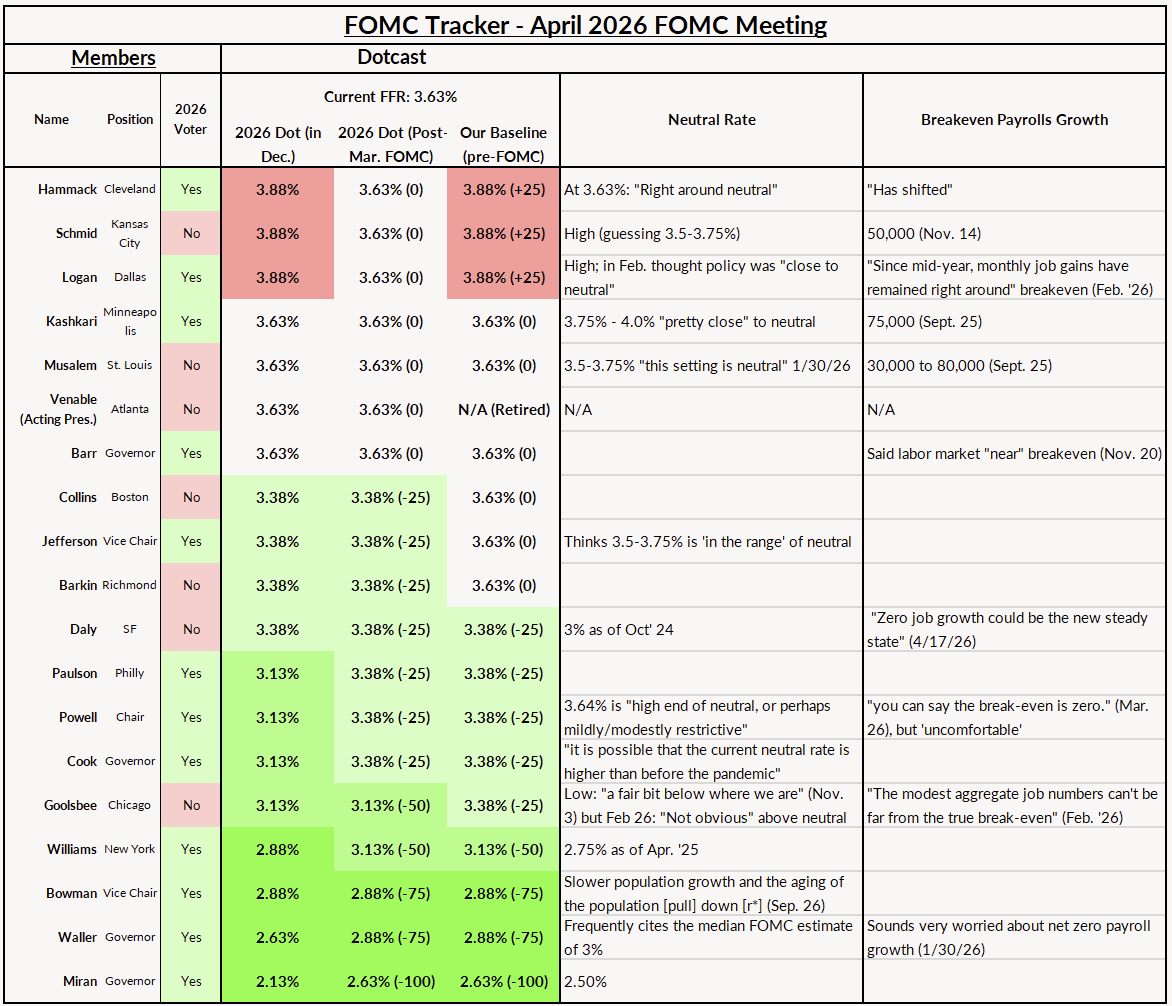

Opposition to an easing bias is now widespread on the Committee: we count seven regional Fed Presidents who likely oppose the easing bias in the most recent statement.

The most recent data from the labor market shows a stabilizing labor market, and even some tentative, nascent signs of a pickup in hiring, posted wages, and job switcher wage growth.

The combination of a steady labor market, elevated inflation, and rates close to the Committee's estimate of neutral all point towards a hike as the next move, if anything. We think that the data will most likely push the Committee towards a hike by 2027H1, but late 2026 is also possible, especially if the labor market picks up.

Voting power in the Committee is heavily skewed towards the doves, with almost all of the opposition to an easing bias coming from regional Fed Presidents.

Watch for Fedspeak from Jefferson, Barr, and Cook, the most likely Board members to push back against easing from Warsh.

Also watch for Daly and Barkin. We have yet to hear from Barkin; Daly is still maintaining an easing bias but would be the next President to go. Both have voting power next year.

Also voting next year is the Atlanta Fed President, who has yet to be selected.

We will have a more complete explanation of our Fed Views out this week.

Opposition to an easing bias continues to spread among the Committee, with Collins, Musalem and Goolsbee explicitly siding with the dissenters. None are too surprising, and there are likely at least seven regional Fed Presidents now opposed to an easing bias. You can see Hammack actively laying the groundwork for pro-hike arguments, saying that she hears that "an inflationary mindset is starting to become entrenched" in people's minds.

Still maintaining an easing bias are Daly and Williams. Among the regional Presidents, Daly would be one of the next to go. Daly downplayed the dissents, arguing that the most important thing is that the Committee agreed to hold, and still expected an underlying path of the economy that may eventually lead to cuts.

On the political side, Miran expressed opposition to Powell's continued presence on the Board. Kashkari gave an interview in which he vocally called out the investigation into Powell as a political "pretext"—this is pretty outspoken for a regional Fed President.

For those keeping score, the current count on an easing bias is probably:

Against an easing bias: Hammack, Schmid, Logan, Kashkari, Musalem, Goolsbee, Collins

For an easing bias: Miran, Waller, Bowman, Williams, Daly, Powell

Currently Unknown: Venable (Atlanta interim), Jefferson, Barkin (probably against easing), Paulson (probably for easing), Cook, Barr (normally hawkish, but did not dissent).

Note: We use a LLM (Claude) to assist in extracting quotes from FOMC appearances. When given the appropriate context, we have found that Claude performs well in this context. We check and edit Claude's work. All of the analysis above this note was written by a human, without LLM assistance.

Said the current stance of monetary policy is "well positioned" to balance dual mandate risks given elevated inflation, mixed labor signals, and Middle East uncertainty

On the labor market: unemployment at 4.3% has changed little over nine months and payroll growth is consistent with underlying labor force growth; soft data point to increasing slack, and the hard/soft dissonance may reflect a "low-hire, low-fire" labor market

On the inflation outlook: base case is inflation around 3% this year before dropping to the 2% target in 2027 as tariff and energy effects fade

On tariffs: pass-through is being borne overwhelmingly by domestic producers and consumers, mostly complete in the next few months, but Williams anticipates a fresh round in coming months adding upward pressure

Said underlying inflation outside imported goods and energy has remained stable, with no significant second-round spillover yet

Press Q&A after speech

"We will at some point need to be lowering interest rates" to reflect lower inflation

Higher-than-expected 2026 inflation pushes off the date of cuts but doesn't change the basic story

Said energy costs were already rising before the Iran war, driven by AI data-center demand and aging infrastructure, with the war's added impact depending on Strait of Hormuz duration

On US insulation from gas-price shocks: US natural gas products "are not part of a global market", noting export constraints leave the US "a little bit insulated"

On pass-through: the most immediate effect is the increase in gasoline prices, and that "could bleed over into other prices", with effects already in fertilizer

On duration risk: "the longer that goes on, the greater the risk that the inflation we're seeing in these prices becomes embedded in the economy"

On the Fed's reaction function: it "depends heavily on whether the productivity growth happens unexpectedly or is anticipated to be coming in the future"

Unexpected gains → inflation contained, rates can fall; anticipated gains → extra investment and spending drive inflation up, requiring higher rates

On the AI-hype channel: "The bigger the hype, the more rates would need to rise to prevent overheating"

Central case: an unanticipated productivity surge mechanically pulls rates down; an anticipated one does the opposite. With anticipation, inflation still falls and output heats up, but the nominal rate rises rather than falls

Calibrated magnitudes: an unexpected 1pp productivity surge → ~75bp of cuts; a fully anticipated 1pp/year surge for 10 years → ~50bp of hikes for the duration

Signals to watch: wealth effects on consumer spending, data-center investment driving up land/electrician/chip costs for non-AI firms — all hints that productivity growth is pushing the natural rate up

On expectations data: a Chicago Fed survey by Ezra Karger found the median economist, tech worker, and member of the general public expects a significant productivity boost over the next ten years; OECD and McKinsey project similar

On the cost of a "wait-for-it" strategy: higher inflation, a more overheated economy, and a larger eventual rate increase than if the central bank had tracked the natural rate from the start

On the FOMC statement: said the signal that the next move is more likely to be a cut was "a little bit misleading", given her view of the economy

Outlook: rates "on hold for quite some time", with the duration not yet clear

Said the statement should have had a "pretty neutral stance" on whether the next move is down, up, or on hold for a long period

Labor market: "relatively stable... in a low-hire, low-fire equilibrium"

On inflation: missing the 2% target for five years, with Iran-conflict pressures potentially making it more persistent; inflation expectations described as largely anchored

Said she hears business concern that "an inflationary mindset is starting to become entrenched" in people's minds

Cited a stylized cost-of-living example: US consumers and businesses have seen "10 years' worth of 2% inflation" in just the last five years, with a $400 emergency fund no longer covering car repairs that now run $600–700

Per local press coverage, Kashkari said he heard "cautiousness" from regional business leaders — that there's "a lot of uncertainty" from tariffs and the Iran war, and businesses are "nervous" until they get more clarity

Framed the visit as part of incorporating regional perspectives into national rate-setting

The Frontline documentary, premiering 5/12/26, was previewed 5/8/26 with on-the-record quotes from Kashkari about the DOJ investigation of Powell:

On the historical context: in the 113-year history of the Fed, "nothing like this has ever happened before"

On the investigation's motivation: Kashkari said it was "clear that this was a pretext" — that the administration disliked the FOMC's monetary policy decisions and wanted to "change the people making the decisions"

"Strongly supportive" of the decision to leave rates unchanged, but also preferred to adjust the statement so it would not align as closely with the presumption that the next move will be a cut

Favors a more "agnostic" stance on the future path of rates; rates likely on hold "for a longer time period, with further easing further down the road"

Modal scenario: inflation accelerates to just above 3.5% in the next few months, then eases back toward about 3% by year-end

On the dissents: said the phrasing of the statement is "less important than the actions" of the Committee, and the real signal is that everyone agreed to the decision

Characterized policy as "slightly restrictive", with downward pressure on inflation if the Iran war resolves

Said it is too early to tell whether the rate-cutting cycle is over; reaffirmed commitment to 2%; no indication yet that the energy-price surge is driving medium- or longer-term inflation expectations higher

Conditional outlook: if the conflict ends, oil falls, and pass-through is limited, she expects "the underlying dynamics that we were facing prior to the conflict to return"

Labor market is stable and isn't generating inflationary pressure

Said inflation is running meaningfully above target and that the balance of risks has shifted toward inflation rather than employment

Argued the policy rate may need to stay on hold until inflation is clearly returning to 2%; allowed there are "plausible scenarios" in which the Fed could either cut or hike

On underlying inflation: cited business-contact reports of higher prices for aluminum, helium, diesel fuel, and other inputs — "disruptive" effects with confidence-channel implications for hiring

Labor market: said it "seems like it has stabilized"

Characterized current policy as "either neutral or slightly accommodative"; near-term inflation expectations rising, longer-run expectations starting to "drift up slightly"

Quoted a business leader on hiring caution: "The best worker to fire is the one that I haven't hired" because of uncertainty

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.