Labor Market Recap April 2026: An Easing Bias is Coming to an End. The Age of a Tightening Bias is Nigh.

The question is no longer going to be “when will the Fed cut?” but rather “will the Fed hike?”

The question is no longer going to be “when will the Fed cut?” but rather “will the Fed hike?”

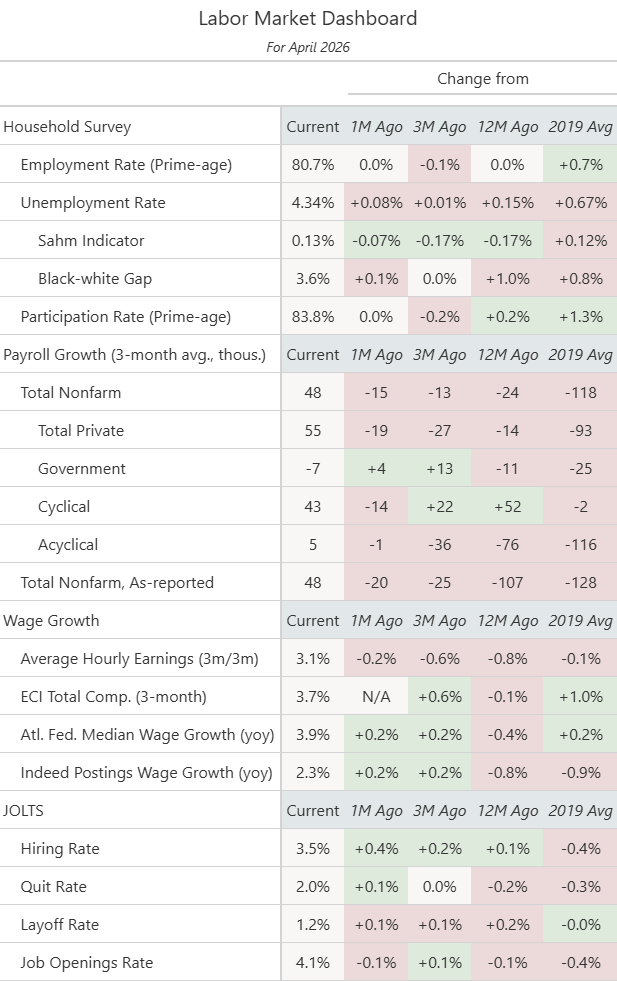

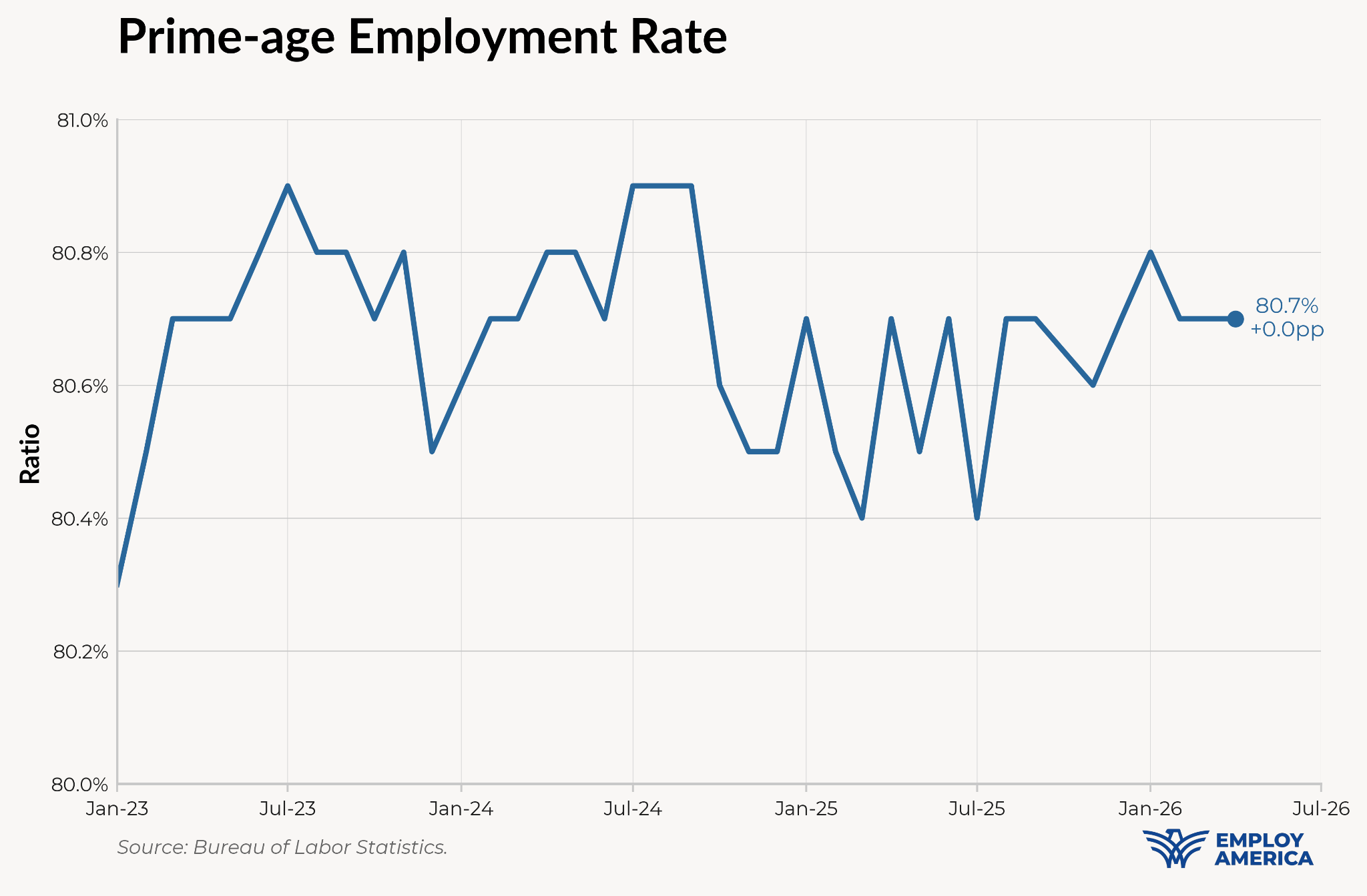

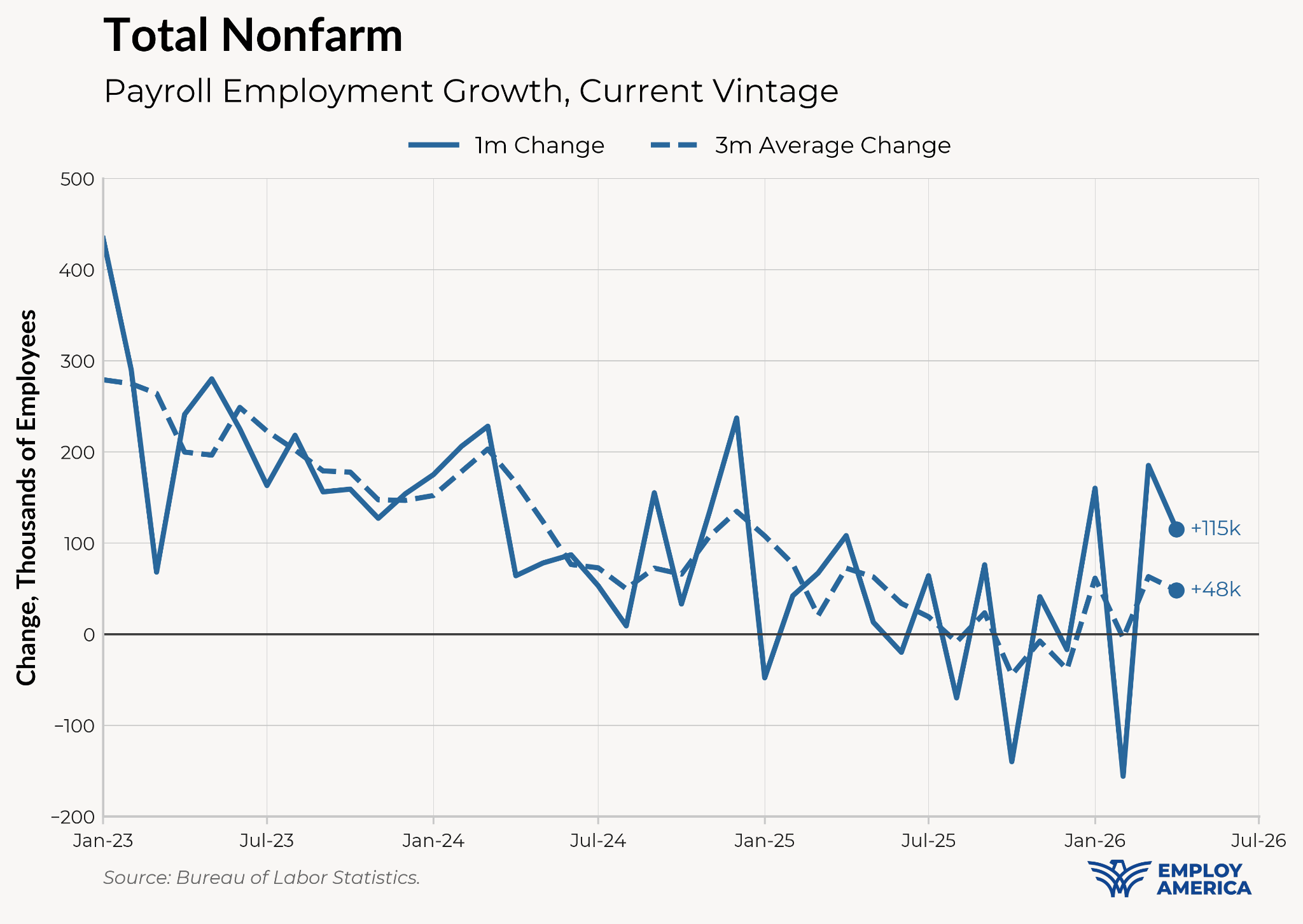

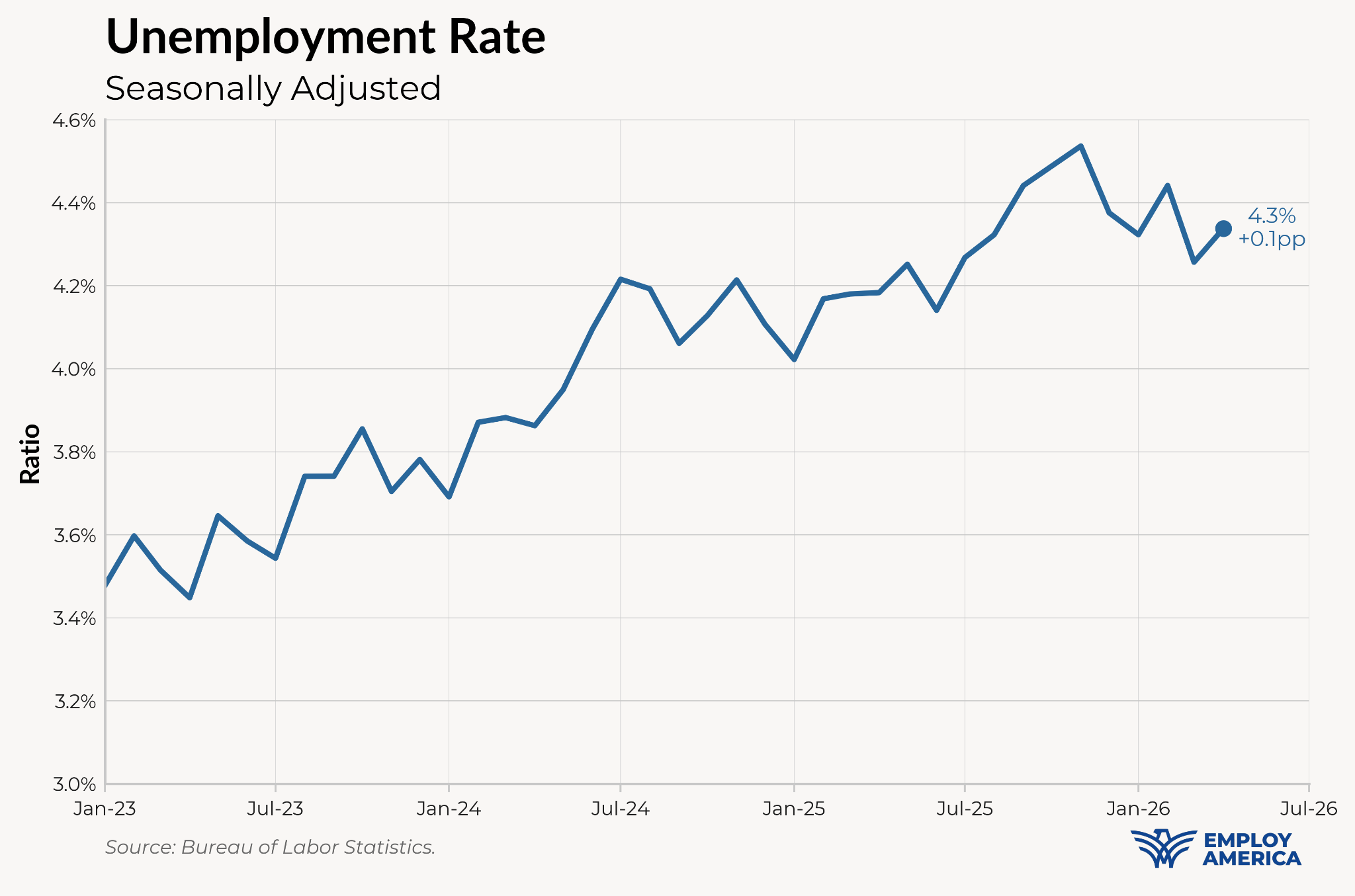

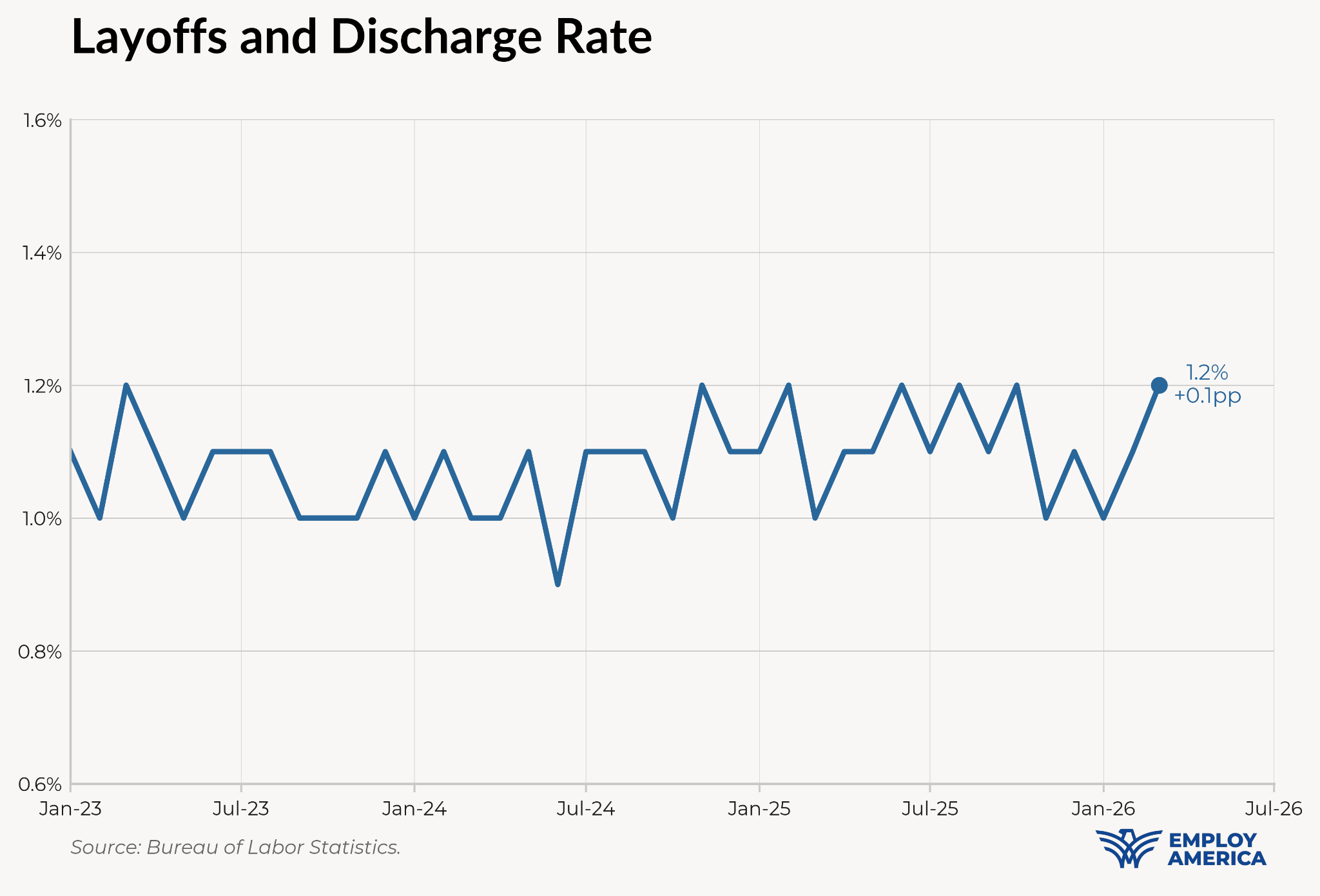

The labor market added 115,000 jobs in April, with small revisions to previous months. Payroll growth was particularly strong in the trade and transportation sector, especially couriers and warehouses. The unemployment rate rose by 0.08pp to 4.34%, and prime-age employment and participation rates were unchanged from last month. Short-term unemployment was up sharply, but well within normal variation; similarly, the layoff rate is up to 1.2%, from 1.0% in January. Wage growth was very soft in April, and we may be seeing wage growth suppressed by increasing costs in healthcare benefits. However, posted wages show signs of troughing.

The overall takeaway from the data is that the labor market is holding steady—and the Fed will take this as its sign to move away from its easing bias. This is probably the cleanest read of the labor market we’ve got in a while (there was little significant strike activity this month, for example). As we’ve been flagging for months now, the data is likely to push the Fed away from easing and even potentially towards hikes this year, even though the Fedspeak has been more dovish. With this data in hand, we expect the Fed to remove its easing bias at the next meeting and begin to lay the groundwork for a pivot to a hiking bias later this year.

A steady labor market

The top-line data from this month is frankly not too interesting. The labor market appears to have achieved some semblance of stability over the past half-year. Prime-age employment has been the same over the past three months, and payroll growth has recovered to somewhere comfortably within most estimates of breakeven.

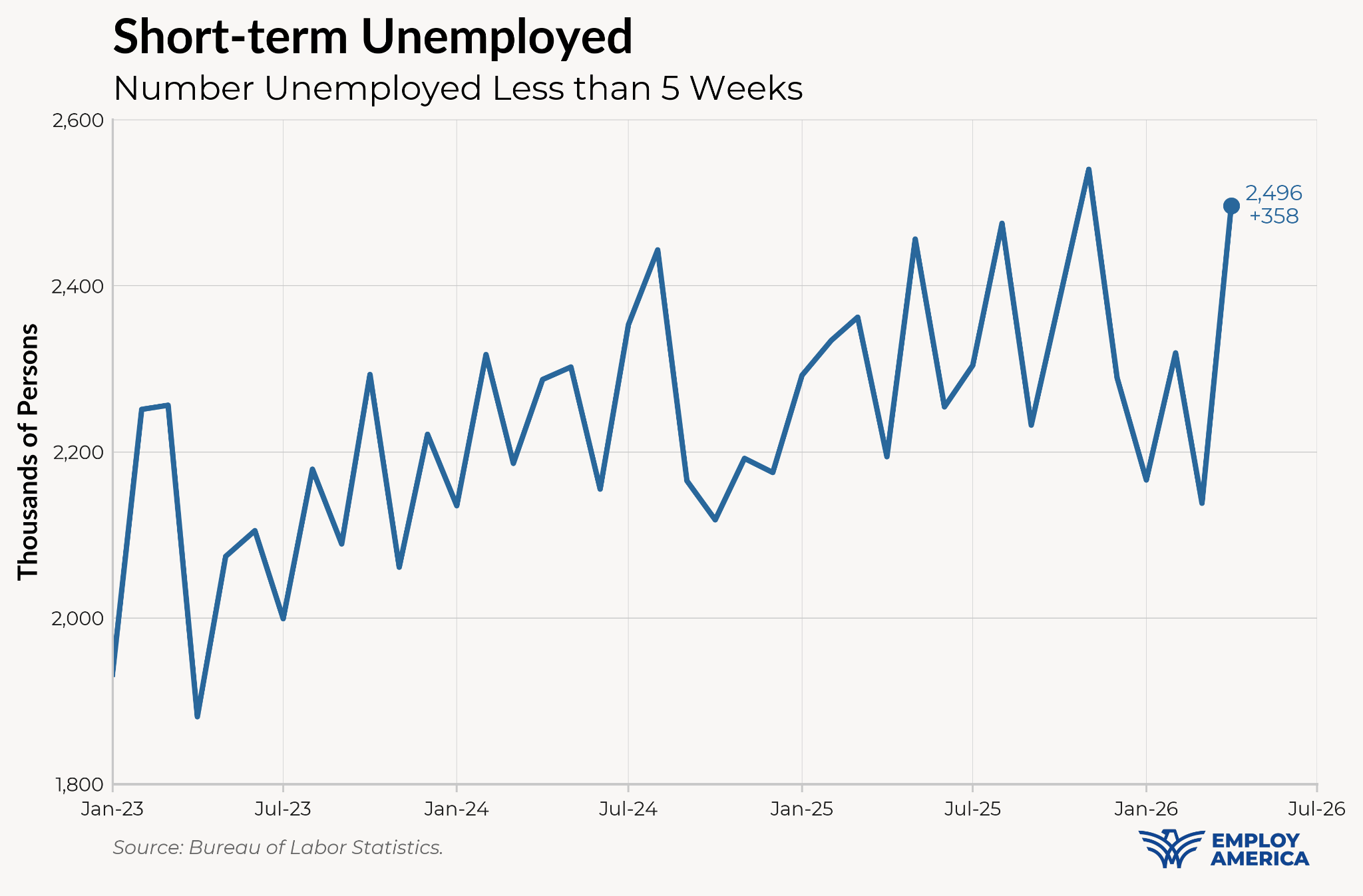

The only red flag: the number of short-term unemployed in the household survey spiked in April. This is a rather large increase, but the overall level is still historically low and within its range over the past year.

It’s possible that we are seeing the effects of a slight pickup in the layoff rate—again, these are still at a historically low level—in the JOLTS data over the past few months.

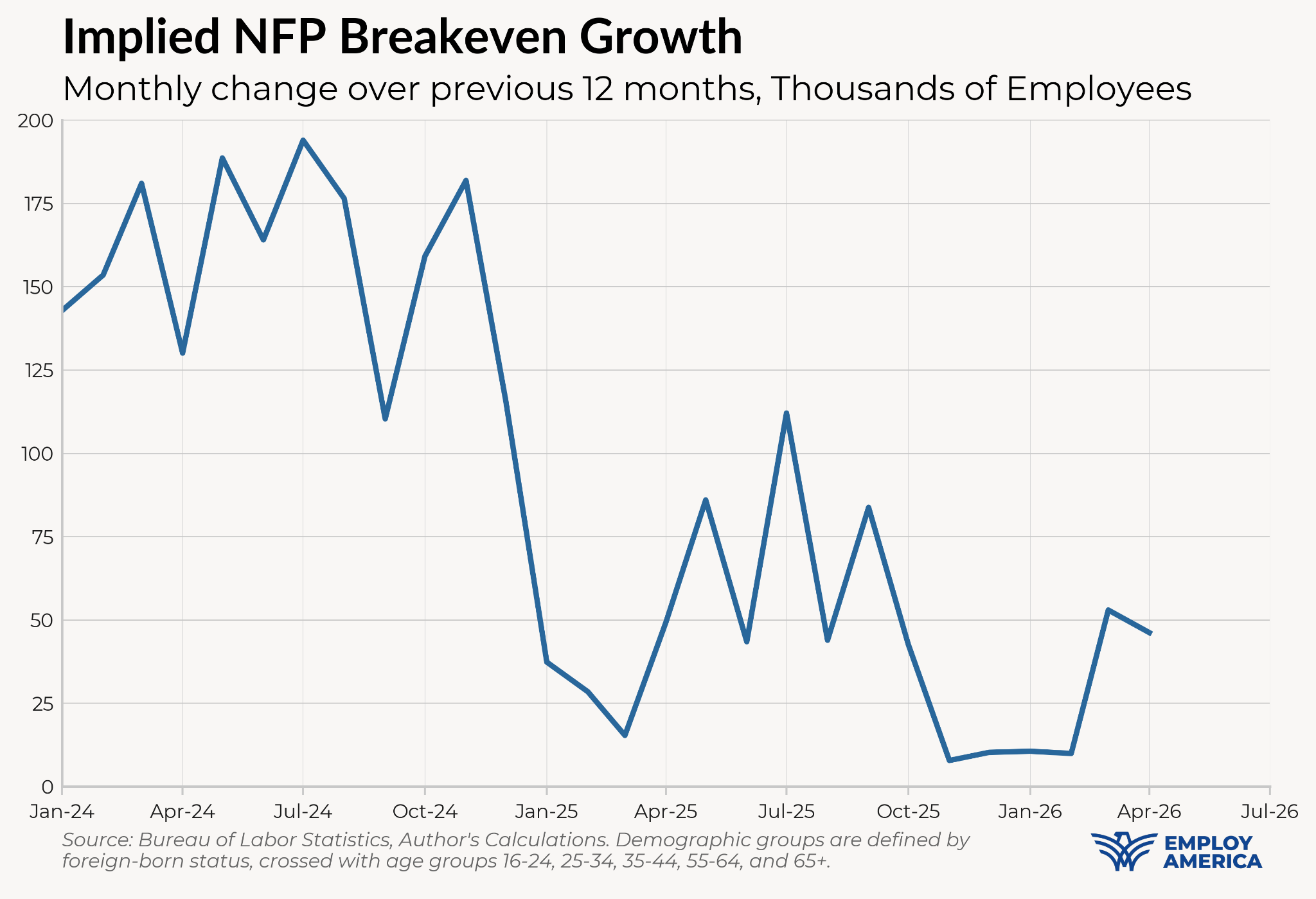

The pickup in payrolls growth alongside the slight increase in unemployment rate brings up our estimate of the implied breakeven rate of NFP growth over the past 12 months to +46k jobs per month, just below the current three-month monthly growth rate of payrolls, +48k per month.

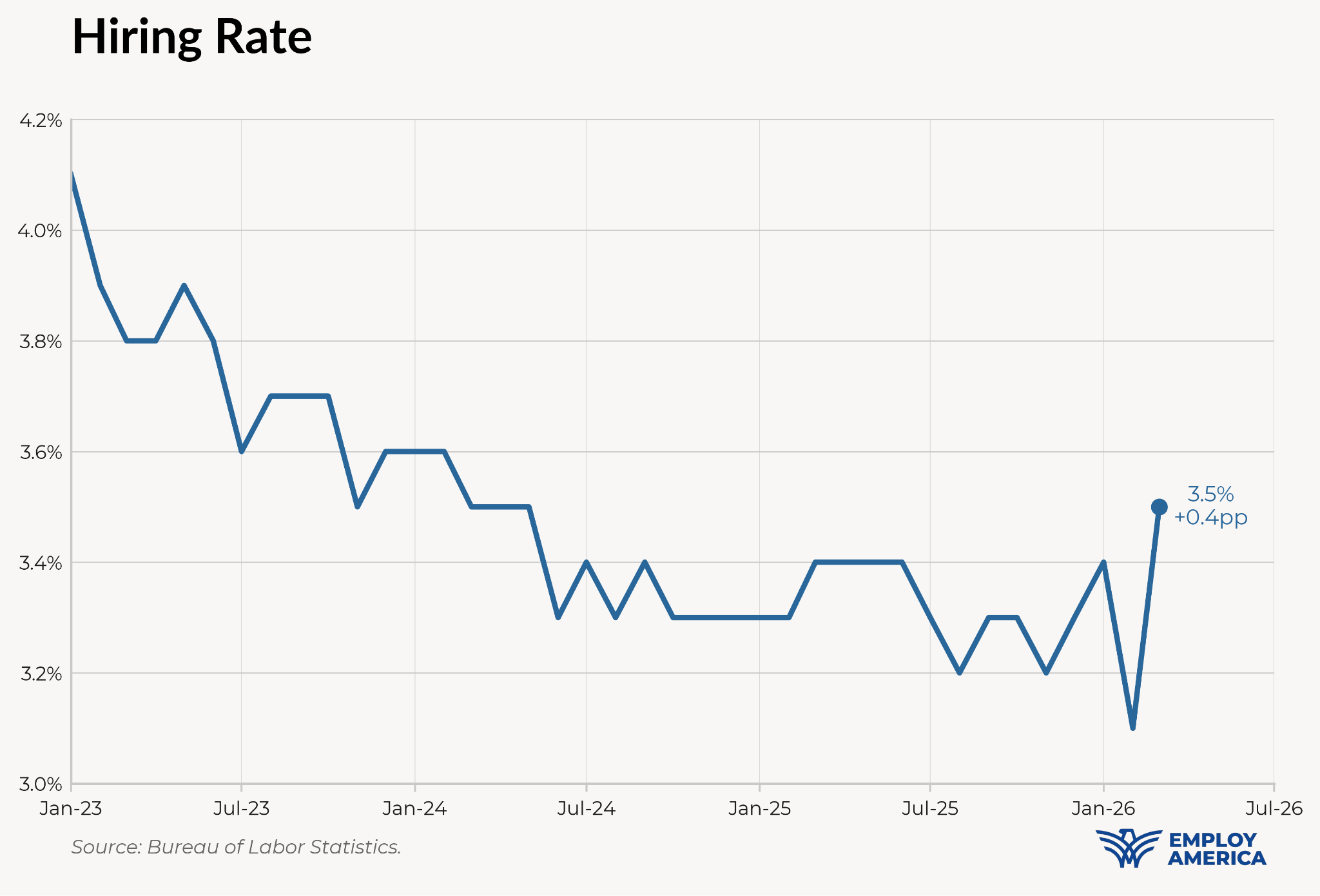

It’s too early to make this call for sure, but we are starting to see nascent signs of a pickup in the labor market. The hiring rate increased sharply in March, rising from 3.1% to 3.5%.

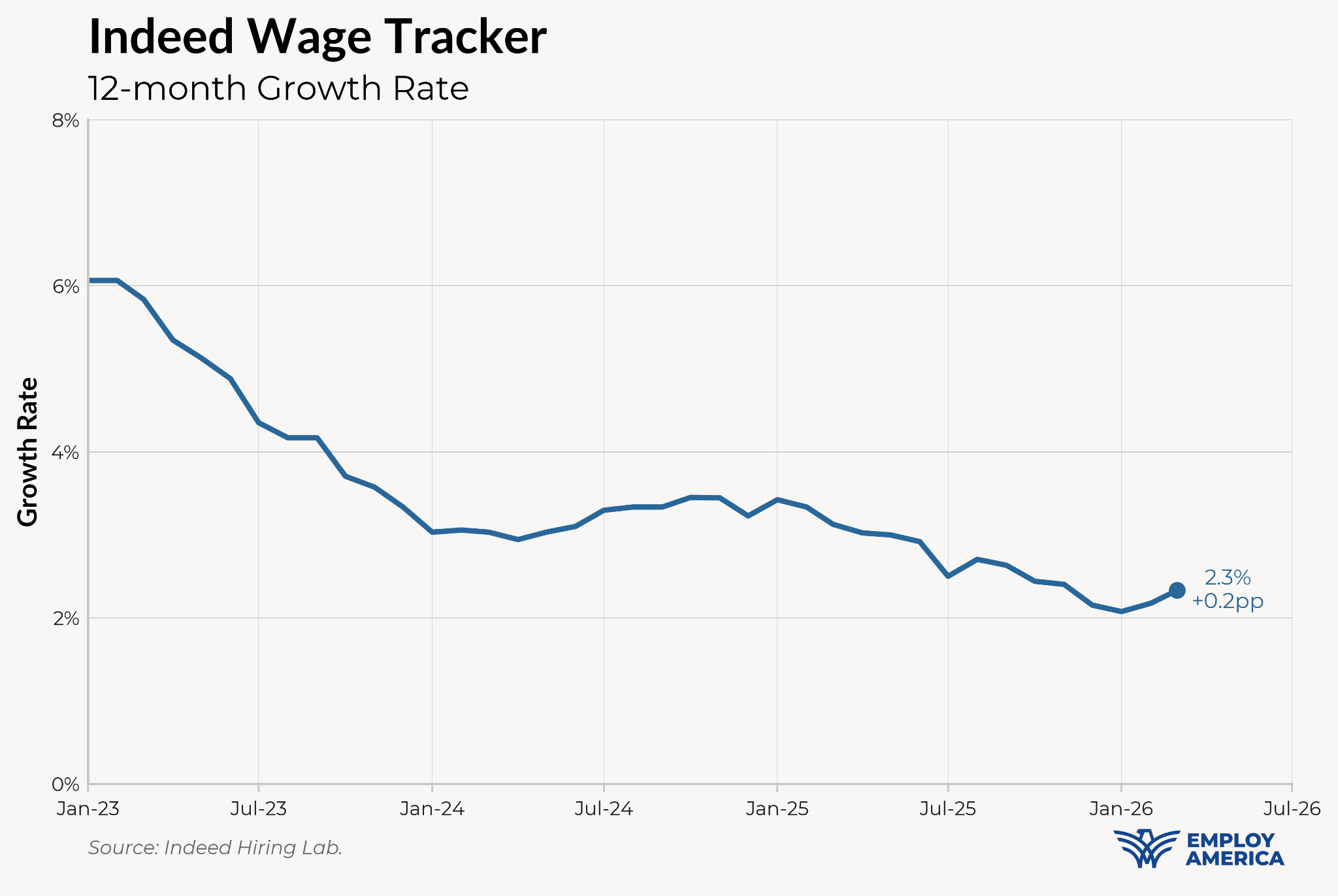

While wage growth was soft this month at 1.94% annualized (likely a one-off reading), posted wages at Indeed appear to have troughed, and have been increasing over the past couple of months:

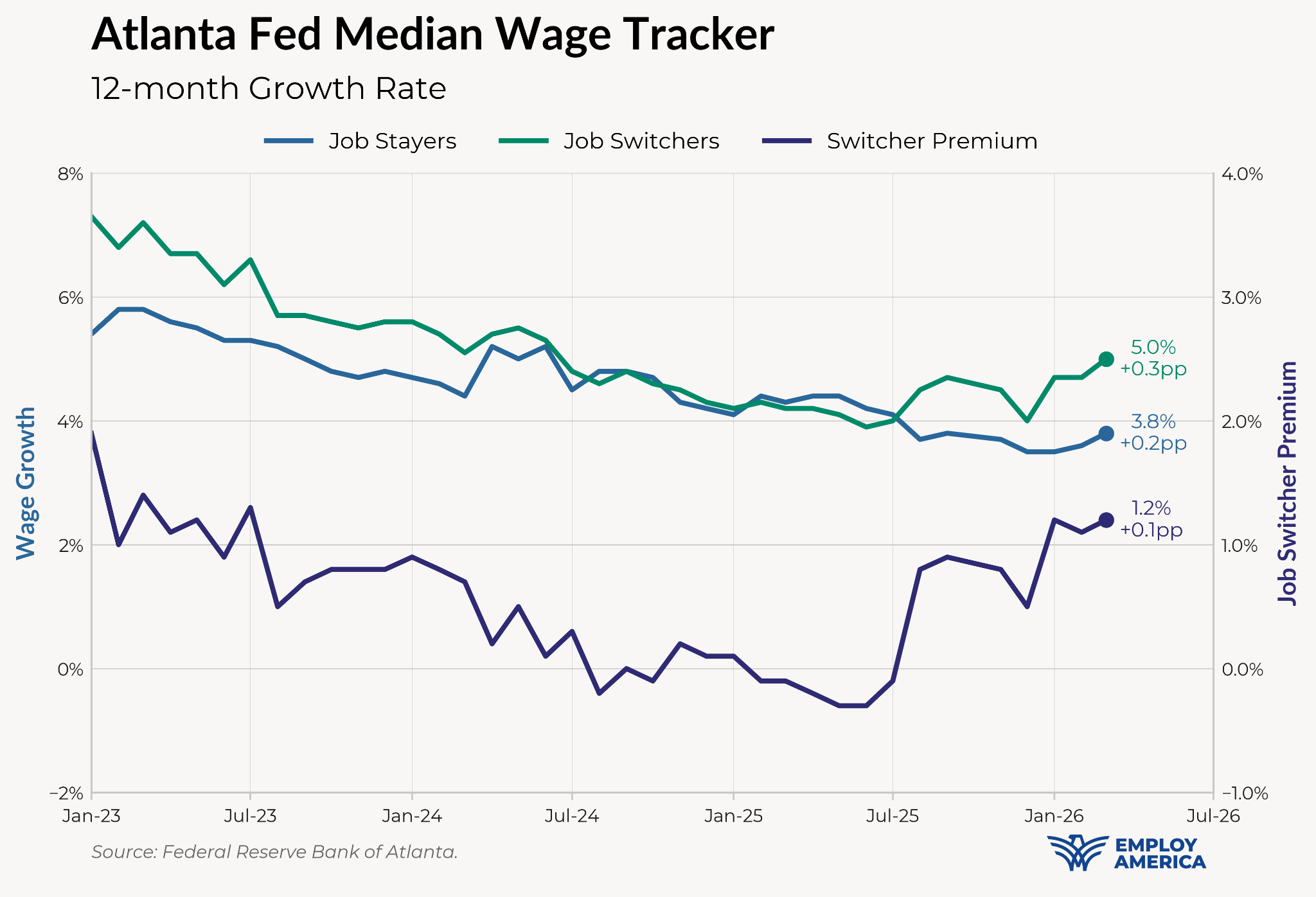

Wages in the Atlanta Fed’s Median Wage Tracker are also troughing, and job switcher wages are picking up. The job switcher premium is 1.2pp, its highest level since January 2023.

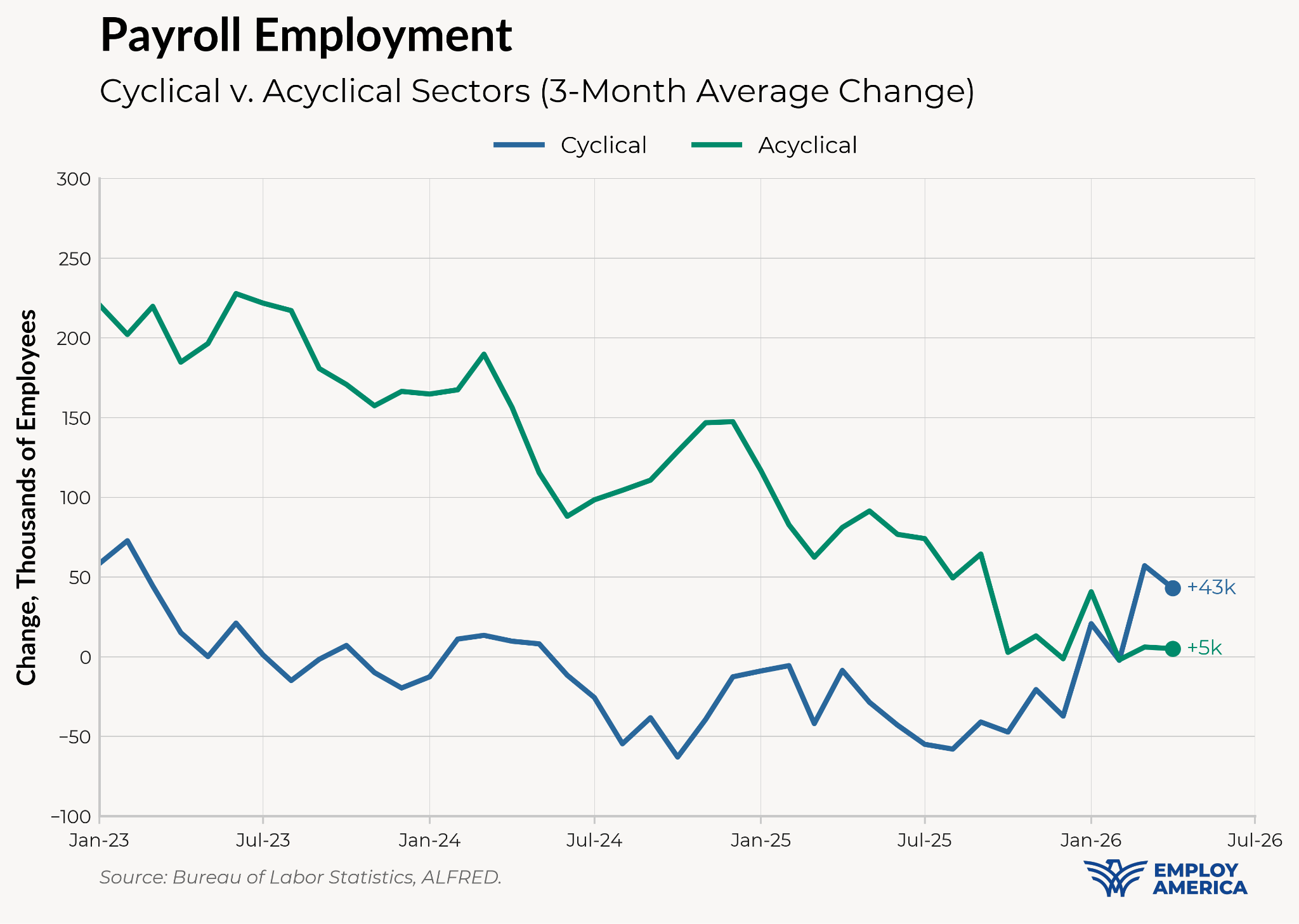

Meanwhile, the composition of job growth has pivoted back towards more cyclical sectors. Payrolls in manufacturing, which had been declining all throughout 2024 and 2025, have stabilized. There’s been a significant pickup in trade, transportation and utilities, especially among couriers and messengers (which is almost entirely trucking jobs), which added 38,000 jobs alone this month.

Again these are just nascent signs. Hiring is still historically low, and posted wage growth is still not impressive. But if the direction of change holds, this could be the trigger for rate hikes later this year.

With inflation uncomfortably high (yes, including trimmed mean estimates) and a clean read of the labor market looking steady, the Fed has all the reason it needs to remove its easing bias. The Fedspeak from most regional Fed Presidents has already shifted away from an easing bias, and we expect more of that to come, including some Board members. The question is no longer going to be “when will the Fed cut?” but rather “will the Fed hike?”

Will the Fed pivot to a tightening bias? Not immediately, and we’d expect the Fedspeak to lag even if the data shifts to that perspective. If the signs of labor market acceleration become sustained and inflation continues to come in hot, expect the Fedspeak to shift towards talking about hiking as the next move. Despite the elevation of Kevin Warsh to Fed Chair, the bulk of the Committee is not only more hawkish but willing to publicly dissent against easing. It will be an uphill battle for him to get rate cuts anytime soon.

In case you missed it: