Post-ECI note: The Supply-side May Spoil Warsh's Productivity Story

Healthcare and energy costs are crowding out labor income and consumer expenditures.

Healthcare and energy costs are crowding out labor income and consumer expenditures.

One of next-Fed Chair Kevin Warsh’s key arguments for justifying rate cuts this year is that an AI-driven “productivity wave” will lead to higher non-inflationary growth. While AI investment is supporting growth and adoption of the technology may eventually lead to an upturn in long-term labor productivity growth, high cost growth in key sectors are not conducive to strong productivity growth this year.

In our series on the drivers of macroeconomic success during the late-1990s, we argued that ample supply and affordability of basic consumption needs like healthcare and energy were a critical part of the story behind the 1990s’ strong labor market gains and productivity growth. Because the late-1990 were a time of relatively benign supply-side conditions, the U.S. economy was able to avoid the inflationary price shocks that plagued other episodes and households were free to spend more of their paychecks on discretionary consumer goods and services.

In 2026, we are starting to see the opposite story. Prices of the essentials, in particular healthcare and energy, are starting to weigh on labor income and consumer spending. These cost shocks won't just affect inflation (yes, including trimmed-mean inflation). While our base case is that the Hormuz shock will tilt the economy more towards inflation than against growth and the labor market, we believe that these supply-side constraints will lead to softer real GDP growth and productivity growth in 2026, even if the AI investment engine continues to buoy the economy.

In our work on healthcare costs, we’ve emphasized the importance of healthcare to the labor market because of the prevalence of employer-sponsored insurance (ESI) as an employee benefit. Nearly 75% of workers aged 18 to 64 receive ESI from their employer, and another nearly 15% are covered as a dependent under someone else’s ESI policy. This results in an effective “head tax” on employment that depresses wages and employment.

Healthcare costs are increasing for a number of reasons. According to preliminary rate filings from insurers for small businesses, insurers cited higher prices for hospital and physician care, tariffs, and increased use of specialty drugs like GLP-1s. These increases lead directly into higher household insurance costs for businesses and households.

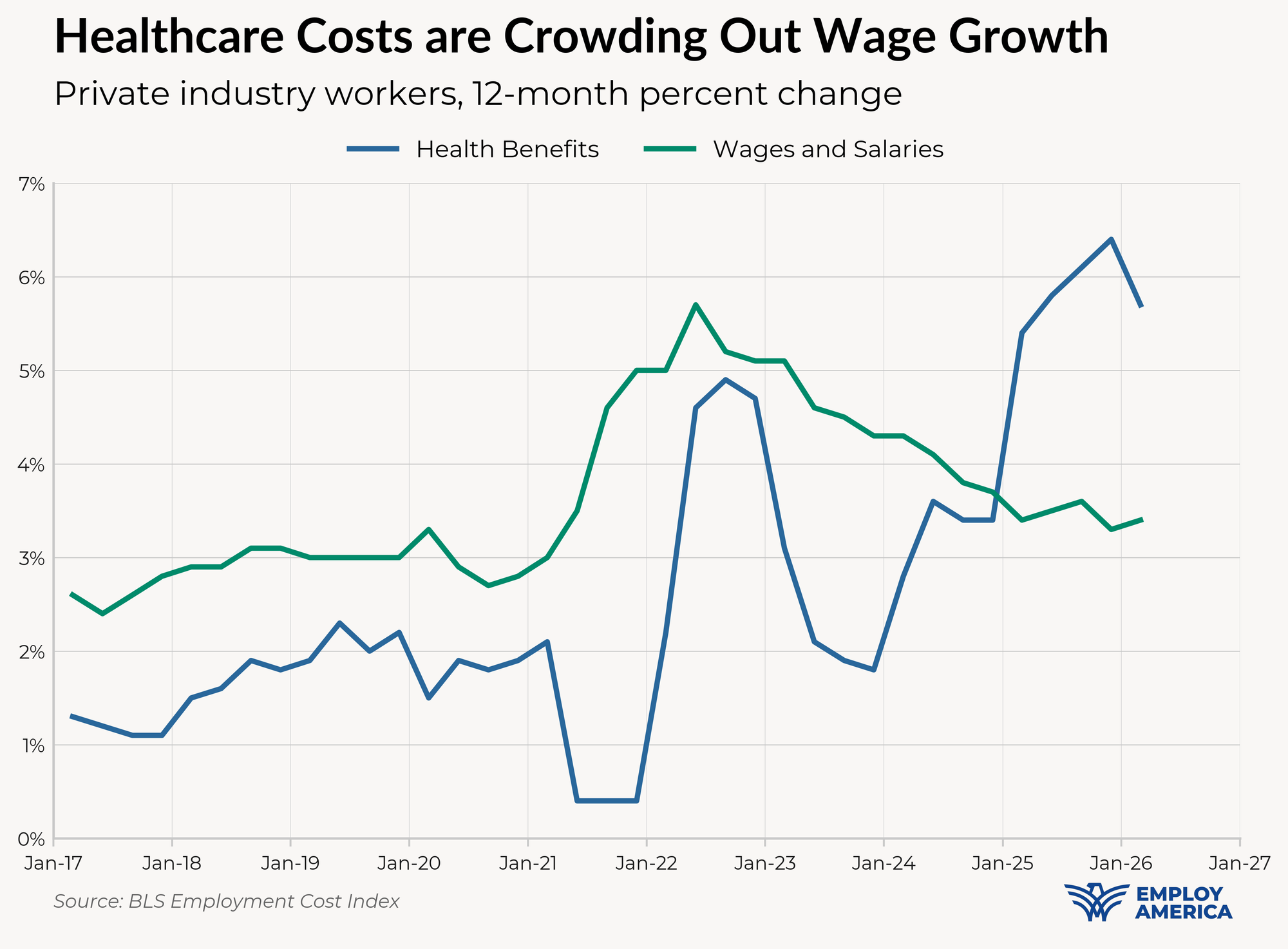

Health insurance benefits account for 7.1% of the total cost of compensation for civilian employees, but is now responsible for an outsized share of the growth in employee compensation costs. In yesterday’s Employment Cost Index report, wages and salaries increased by 0.7% from the previous quarter, but benefit costs increased by 1.3%. The cost of healthcare benefits, which are 5.7% from a year ago, have been growing at a clip not seen since the early 2000s. In surveys conducted late last year, businesses projected that healthcare costs in 2026 would increase by 6.5% to 7.6%, a faster increase than in 2025.

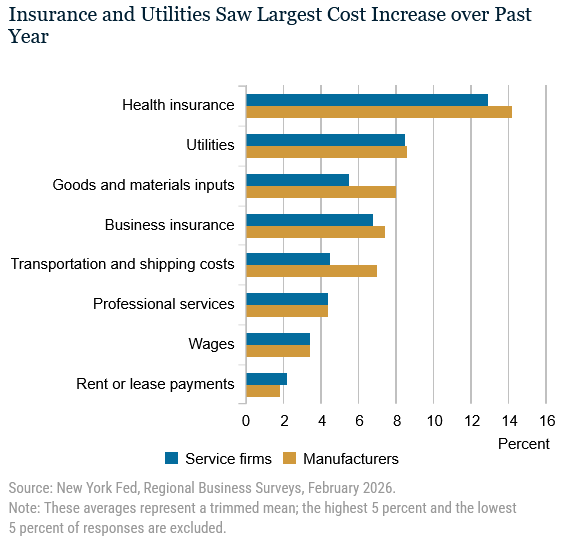

The result is that employee compensation costs are growing quickly, but not in a way that redounds to labor income. The rapidly Increasing costs for ESI plans are likely to dampen labor income. In the New York Fed’s most recent Regional Business Survey, businesses cited double-digit percentage increases in the cost of health insurance over the past year, a faster increase than that of any other production input.

The New York Fed’s survey suggests that the rapid increase in health benefit costs is squeezing wage growth. “Many” firms reported reducing wage increases, and reported that wage increases would have been 0.9 percentage points higher if health costs had remained constant from last year. Still others reported passing on costs to workers by increasing employee contributions. In both cases, the income available to employees to spend on other consumption goods and services is squeezed by the increase in healthcare costs.

For individual market enrollees, the picture is even worse. Premiums for benchmark silver plans increased by 21.7% in 2026, even before changes to enhanced premium tax credits. While the premium increases for these individuals doesn’t affect their wages, it still results in a stark decrease in the leftover income they’ll have to put towards consumption elsewhere.

Gas prices have increased from $2.94 (regular, all formulations) from the week before the start of the conflict with Iran to $4.12 as of April 27th. The extent to which gas prices weigh on consumer spending elsewhere may depend on how persistent consumers perceive the gas price shock to be. If the price increase is seen as temporary, households may be more inclined to smooth consumption and the impact on ex-gas consumer spending may be minimal. However, if the price change is seen as more permanent, the impacts on consumer spending may be larger.

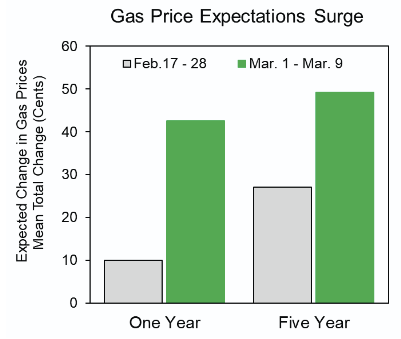

Consumer expectations around gas prices did jump after the War with Iran, with consumers expecting gas prices to be higher by between 40 and 50% over the next five years. Interpreting survey expectations around inflation expectations is always tricky, but taking the survey results on face value suggests that consumers expect a large increase in prices this year that will stick around for an extended period. If that’s the case, they will likely begin cutting back on spending elsewhere; Gelman, et. al (2023) find that changes in gasoline expenditures from permanent price changes are offset one-for-one by changes in other consumer expenditures.

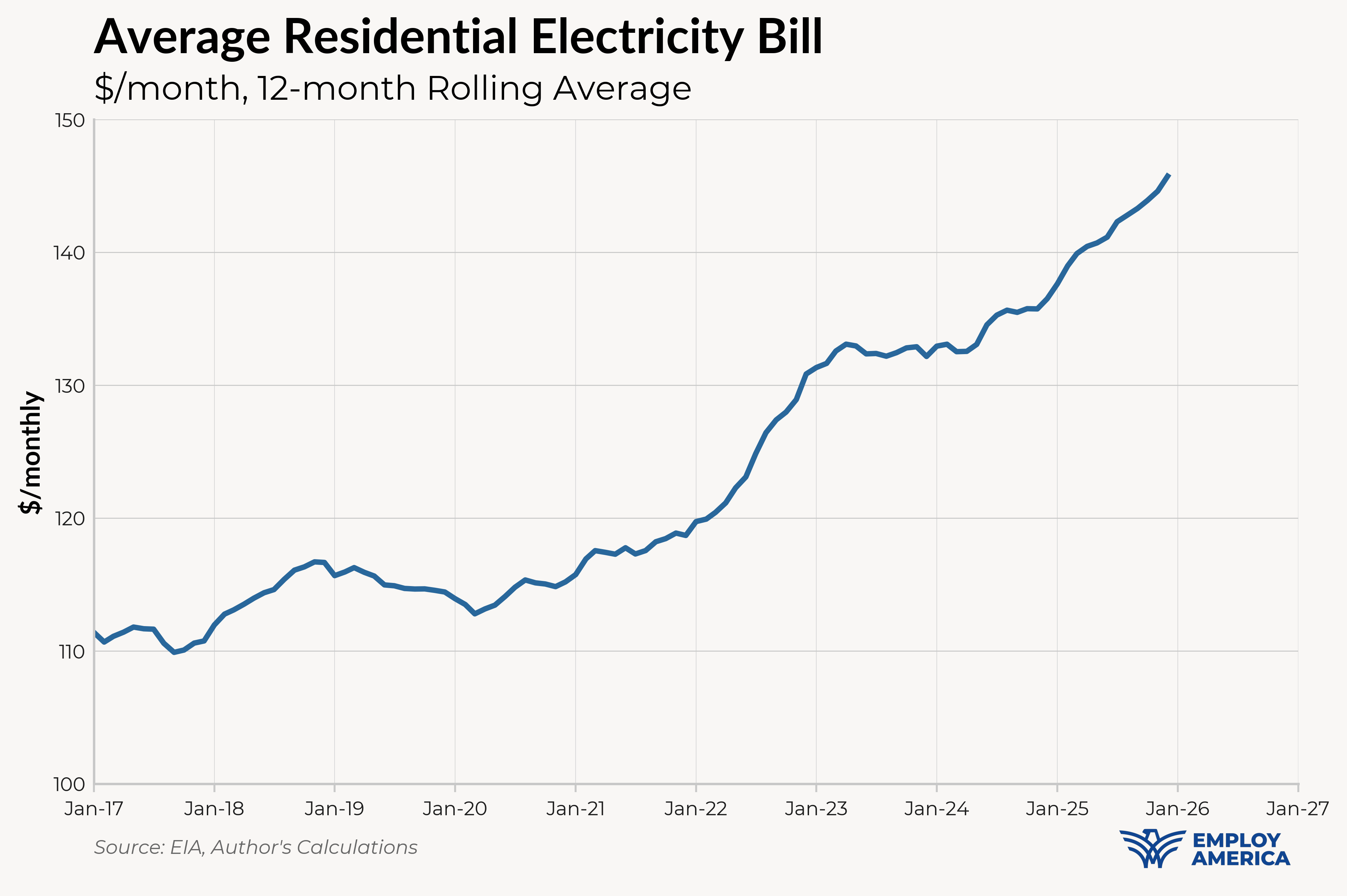

Even before the Hormuz shock, consumers were facing increasing cost pressures from their electricity bills. Most of this is due to an increase in prices, not utilization. Prices are increasing for a myriad of reasons, including the expansion of AI data centers (more recently and in some areas) but larger factors over the past few years include wildfire and storm mitigation efforts and the need to upgrade aging transmission infrastructure. The EIA forecasts that average residential electricity prices will increase by 5.1% in 2026, further straining household budgets.

In addition to pushing up inflation, Increasing healthcare and energy costs will weigh on consumer income and spending going forward. We’re already seeing soft real retail sales in Q1, and we anticipate a further hit in Q2. It probably doesn’t point towards an outright recession, but it’s worth paying attention to.

Higher inflation and lower productivity growth is likely to come just as the new Fed Chair, Kevin Warsh, assumes his position. Unfortunately for him, both of those developments are exactly the opposite of his case for the Fed to resume rate cuts this year. We see a difficult path for Warsh to make this case for the Fed to embrace a more dovish posture, especially after the three hawkish dissents at yesterday’s meeting. Our base case is for the Fed to soon adopt a neutral statement and potentially adopt a tightening bias later in the year, especially if the Hormuz shock persists.

We will have more to say on productivity in the coming weeks, including a deeper dive into the sectoral breakdown of productivity growth in recent quarters and where it might be headed in the near future.

Macrosuite subscribers will receive more timely analysis of this topic in the future. If you're interested in becoming a MacroSuite subscriber, please reach out to macrosuite@employamerica.org