April 2026 FOMC Preview

We’re betting the Committee is probably internally more hawkish more than they are currently projecting. There is a real possibility of a hawkish pivot later this year.

We’re betting the Committee is probably internally more hawkish more than they are currently projecting. There is a real possibility of a hawkish pivot later this year.

Note: Subscribers to MacroSuite receive our FOMC preview during the blackout period before each FOMC meeting. A public version of the preview is released closer to the meeting. If you're interested in becoming a MacroSuite subscriber, please reach out to macrosuite@employamerica.org

Since the last meeting, not much about the Fed outlook has changed. Data from March continues to point towards a steady (and possibly improving) labor market, and persistently elevated inflation. The conflict in Iran and lack of progress in negotiations over the Strait of Hormuz continues to cloud the outlook.

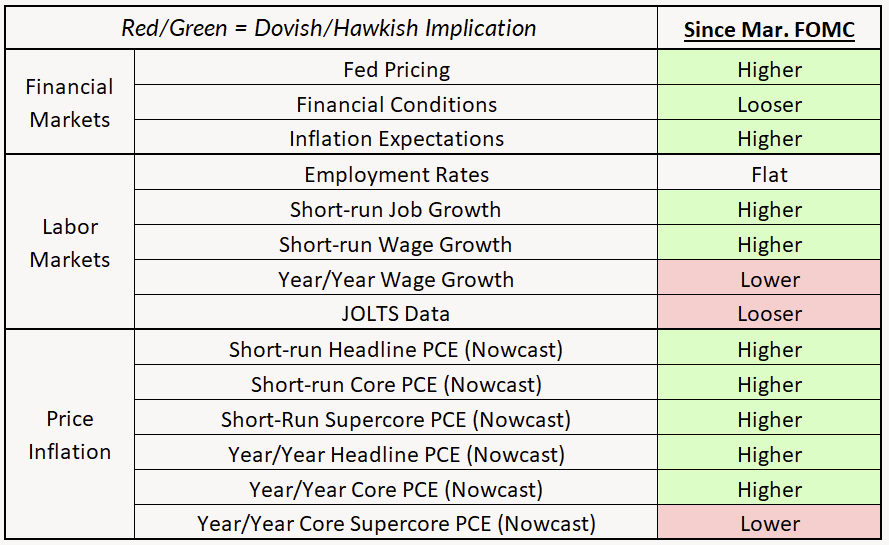

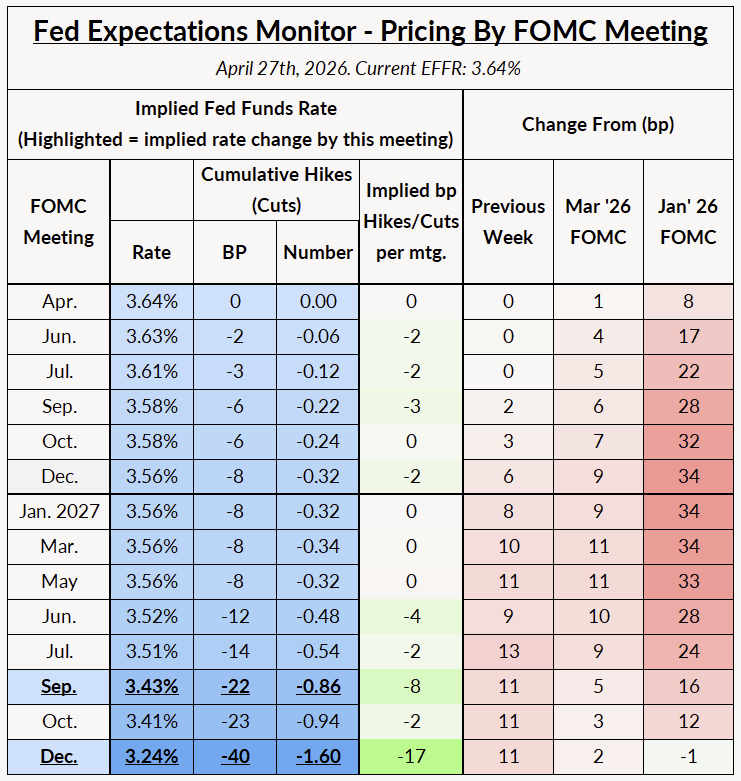

With the data and Fedspeak pointing towards an extended hold in rates (including a hold at this meeting), we expect some more movement towards talk of two-sided risks to be present in both the statement and the press conference. The question is how much the meeting will set the Committee up to make a hawkish pivot. Some things we will be watching for are:

So far, the movement of the Committee towards a tightening bias has been fairly limited, with a minority of members putting much weight on the probability of a hike as the next move. But if you put together the whole picture—inflation at least 100bp over target and rates only 50bp above their neutral estimate, elevated supercore inflation, a labor market that looks pretty steady, stable financial conditions—we’re betting the Committee is probably internally more hawkish more than they are currently projecting. Perhaps they are waiting for more data, or perhaps they are waiting for the Fed Chair nomination story to play out, but there is a real possibility of a hawkish pivot later this year.

Overshadowing monetary policy will be the fact that this is the last press conference of Jay Powell’s term as Chair of the Federal Reserve, and hearings for his would-be replacement Kevin Warsh were held on Tuesday. Now that Thom Tillis has dropped his blockade of Warsh's confirmation, Warsh looks set to become Fed chair by the June meeting. The big question at this week's press conference: will Powell vacate his position on the Board after his term as Chair ends?

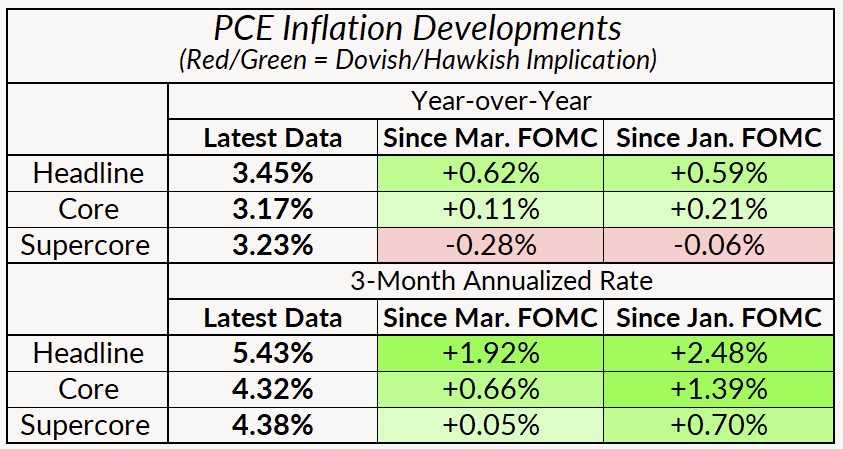

After last week’s PPI data, our corecast is tracking 3.45% year-on-year PCE inflation in March, up from 2.80% in February. Core and supercore inflation are coming in over 4% on a 3-month annualized basis. We’re seeing more inflation coming from categories affected by tariffs (like apparel) and AI-related bottlenecks (like computer equipment and accessories). Healthcare services continue to run strong (and should remain strong on a year-on-year basis).

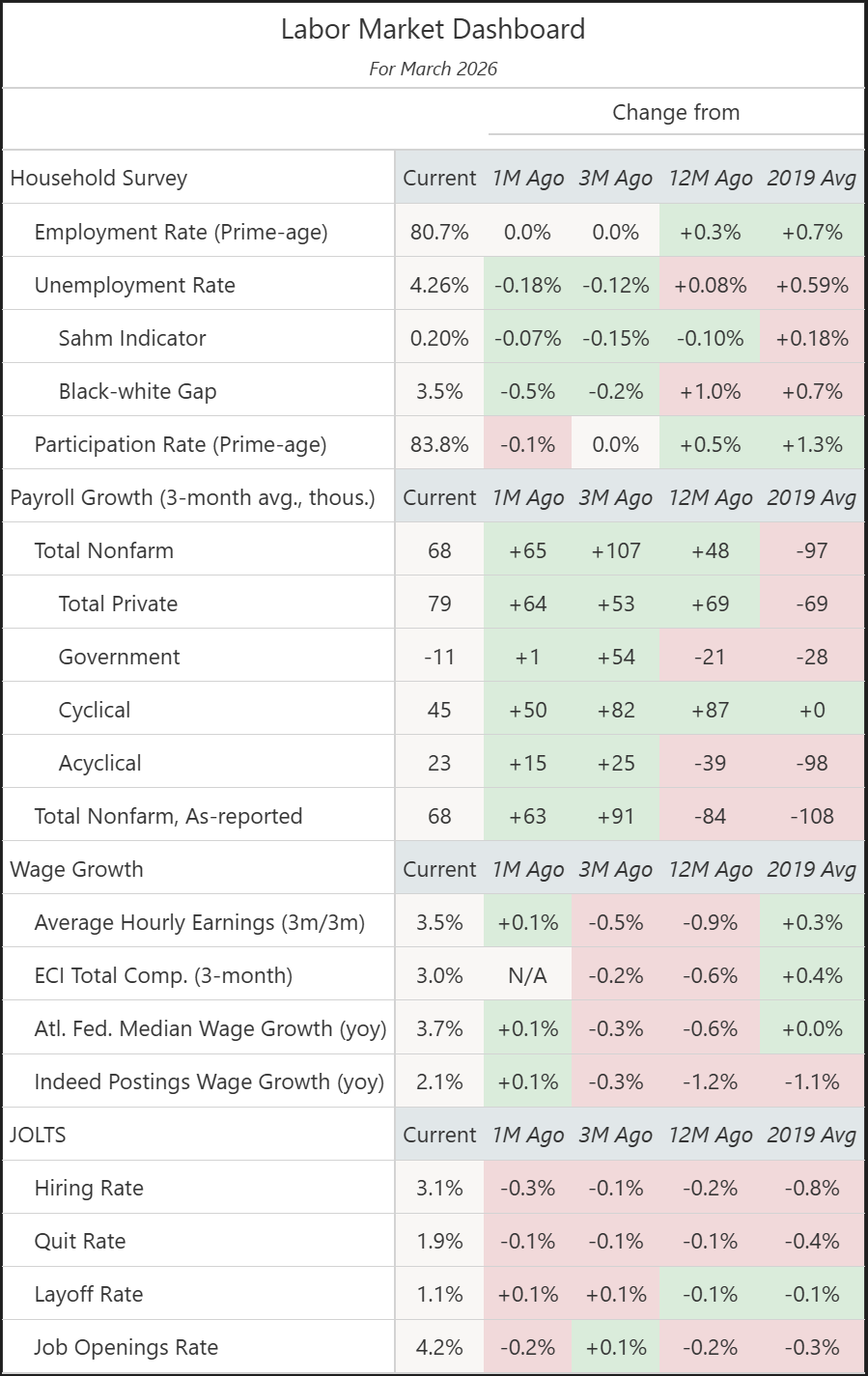

Meanwhile, the labor market looks somewhere between stable and even potentially accelerating. The unemployment rate in March dropped 18 bps to 4.26%, and nonfarm payrolls came in at an eye-popping 178,000 jobs added. The Fed is probably looking through the month-to-month fluctuations around the payrolls numbers that are clouded by seasonality, changes to the birth-death model, and a declining breakeven payrolls number and instead focusing on the household survey’s unemployment and employment rates.

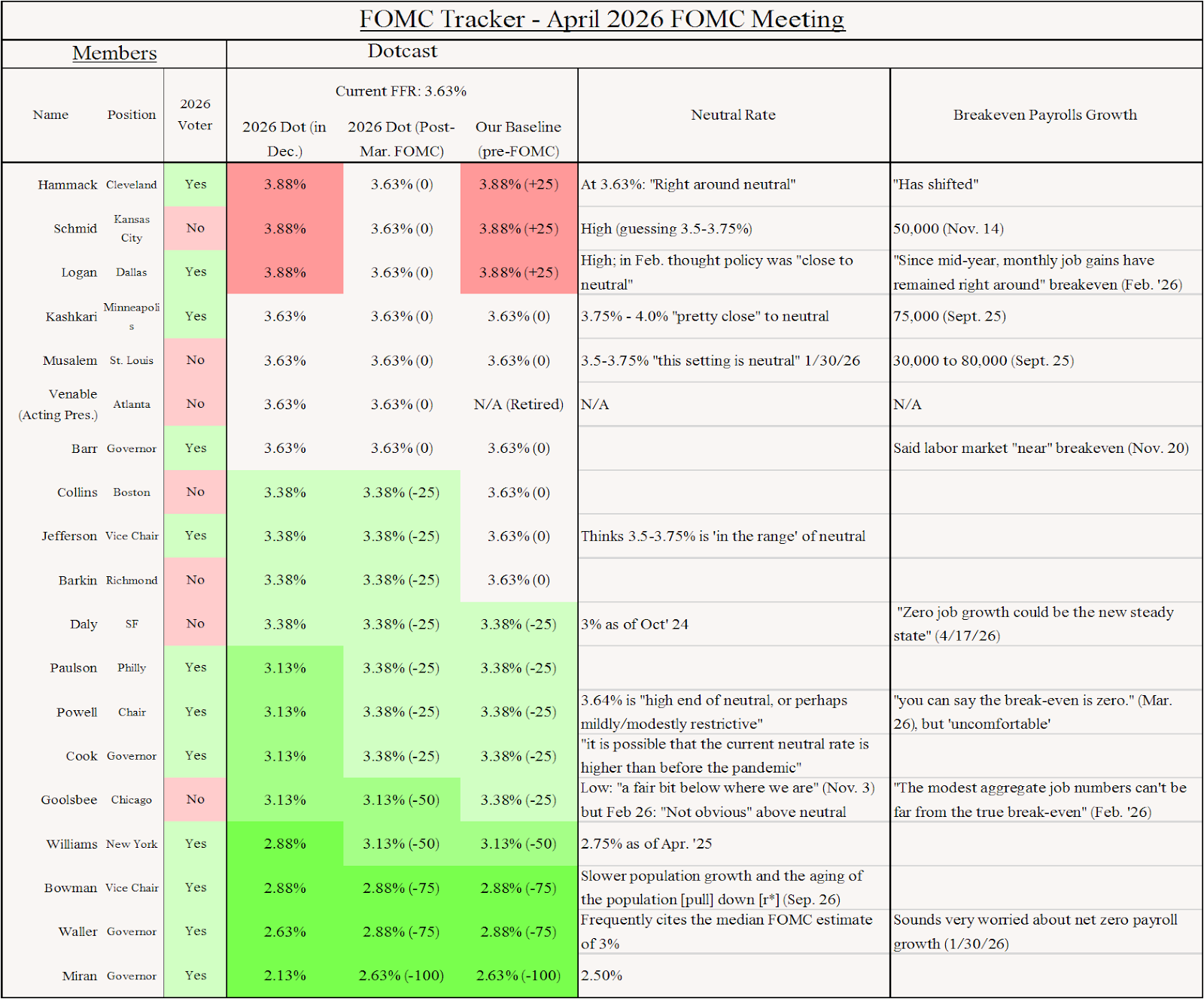

Powell: "Monetary policy works with long and variable lags, famously, and so, by the time the effects of a tightening in monetary policy takes effect, the oil price shock is probably long gone, and you're weighing on the economy at a time when it's not appropriate"

Jefferson: "While the labor market appears to be stabilizing, I remain cautious about that assessment… I continue to see our current policy stance as appropriately positioned to allow us to assess how the economy evolve."

Barr: "There is a risk that this dynamic could lead to inflation persistence, making it more difficult to return inflation to 2 percent. We need to be especially vigilant"

Bowman: "I have three cuts written into my forecast for this year...I still see some fragility in the labor market but we're also seeing a little bit of stalling in the inflation rate, so I'd like to see some more progress on lowering inflation"

Miran: "In March, I wrote down that I thought four cuts was perfect for this year, but if I were writing down a dot today, I might have three"

Waller: "I can look through the effect of recent higher energy prices on inflation because I know it will unwind... leaving me cautious about rate cuts now and more inclined toward cuts to support the labor market later this year"

Goolsbee: "The longer this inflation disruption goes, the more likely it is that the appropriate rate cutting would be put off"; if inflation stays up, "that starts pushing it out of '26"

Schmid: The Fed "must follow through with policy actions to validate stable medium- and long-term inflation expectations"

Williams: "Monetary policy is exactly where it needs to be, and then we can respond if the situation changes"

Daly: Before the oil shock, she anticipated one or two cuts in 2026 would be needed. Currently in "wait and see mode" watching whether higher oil prices spill into other goods and services; could leave rates where they are; "zero job growth could be the new steady state"

Musalem: "We need to see all components of inflation come down in a balanced way. Right now, we have housing doing most of the work. Goods moving the opposite direction, and core non-housing services still sticking"

In case you missed it, our own Skanda Amarnath compared Kevin Warsh’s self-portrait of a principled institutionalist against his actual record of partisan flip-flopping. Read the whole thing here.

Kevin Warsh’s carefully-crafted statements paint a portrait that cannot be reconciled with the record he has established. He was not the dutiful, ahead-of-the-curve crisis-fighting insider he describes; his real-time reading of 2008 was flatly wrong. He has not proven to be the principled institutionalist he describes, instead opting for criticisms that he will only stand by when a Democrat is in the White House, readily abandoning them for whatever might suit his personal and partisan interests, which are currently coupled with President Trump’s preferences.