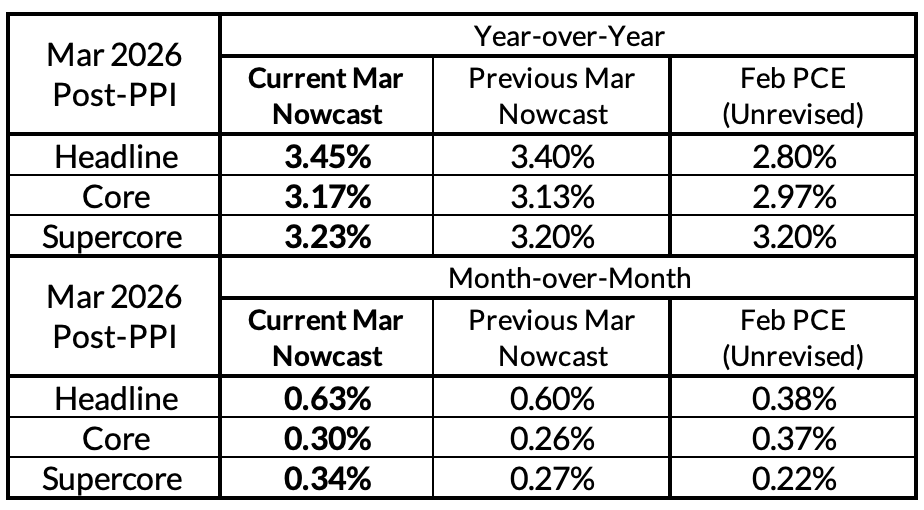

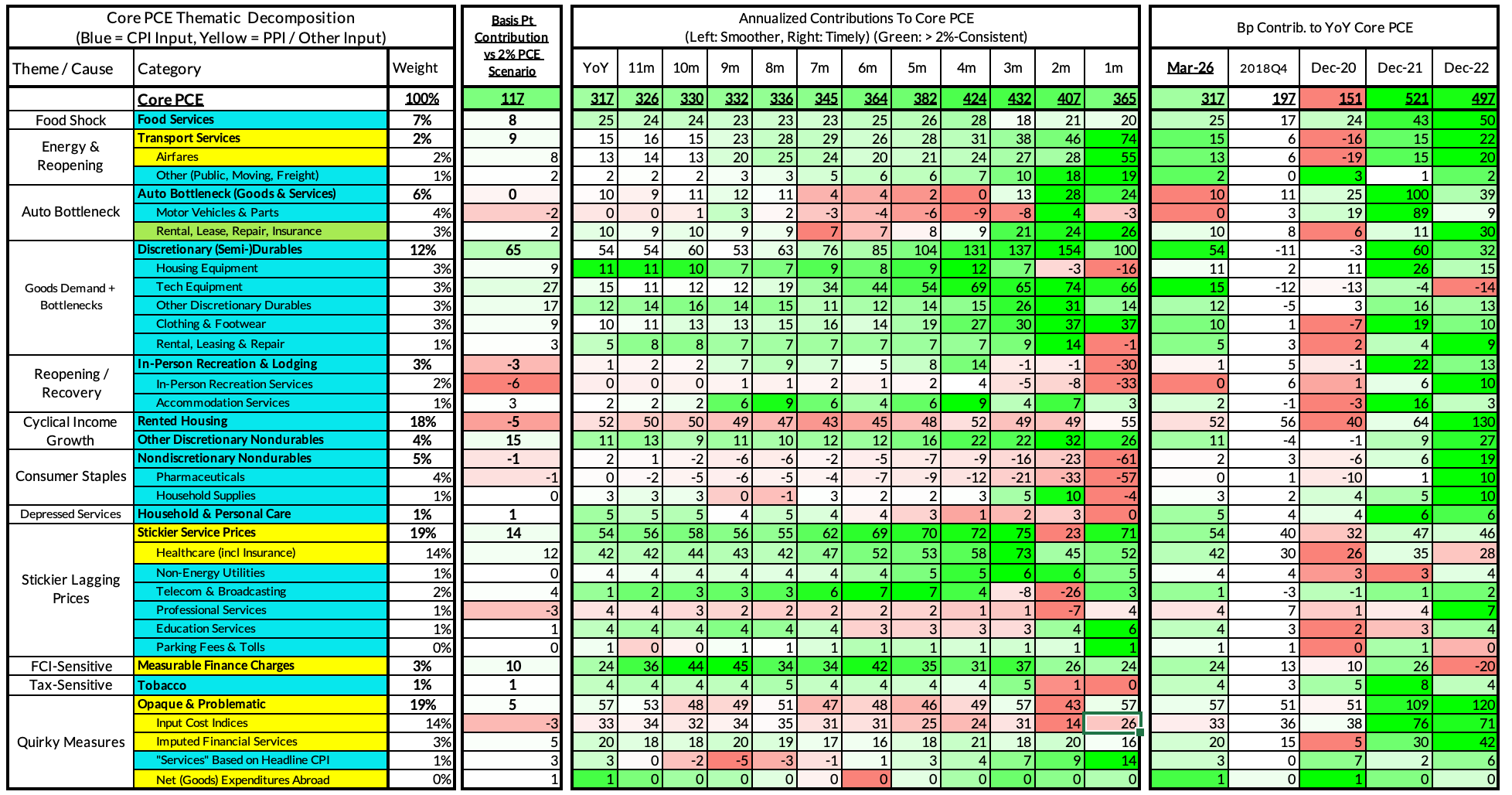

We thought we were penciling in sufficiently strong readings for the PPI inputs in March but apparently not enough. We've marked up our y/y and m/m readings for Core PCE in March by 4bps (26bps->30bps m/m, 3.13%->3.17% y/y. Core PCE is poised to deliver a 4th straight month of growth of at least 0.3% m/m, causing the year over year reading to surge from 2.97% in February up to 3.17% in March.

The sources of the upside surprise were many. Airfares punched even stronger than our firm forecast (closer to the outlier modeled estimates we were originally tracking). The drawdown in the equity market appears to be less relevant than we would have expected for financial services PCE. And healthcare services is continuing to run strong for yet another month in 2026. There is an outstanding issue of whether to map legal services PPI, which came in mildly firmer even as the CPI component fell sharply; if the BEA intends to be intellectually honest, the PPI reading makes sense in light of how they censored the upside CPI surprise in January.

The Fed is in a very rough spot. Core PCE is over 100bps away from the 2% target, trending higher, and vulnerable to new upside risks beyond tariffs: (1) AI-related bottlenecks pushing up goods PCE inflation, and (2) the knock on supply-side effects tied to the closure of the Strait of Hormuz. With the labor market and financial markets maintaining general stability and resilience, a Fed Funds Rate only 50bps above neutral is hard to reconcile with the inflation overshoot and inflation risks of the moment. Today pushes the Fed further to consider adopting a tightening bias in the second half of this year.

Inflation Overshoots At The Component Level

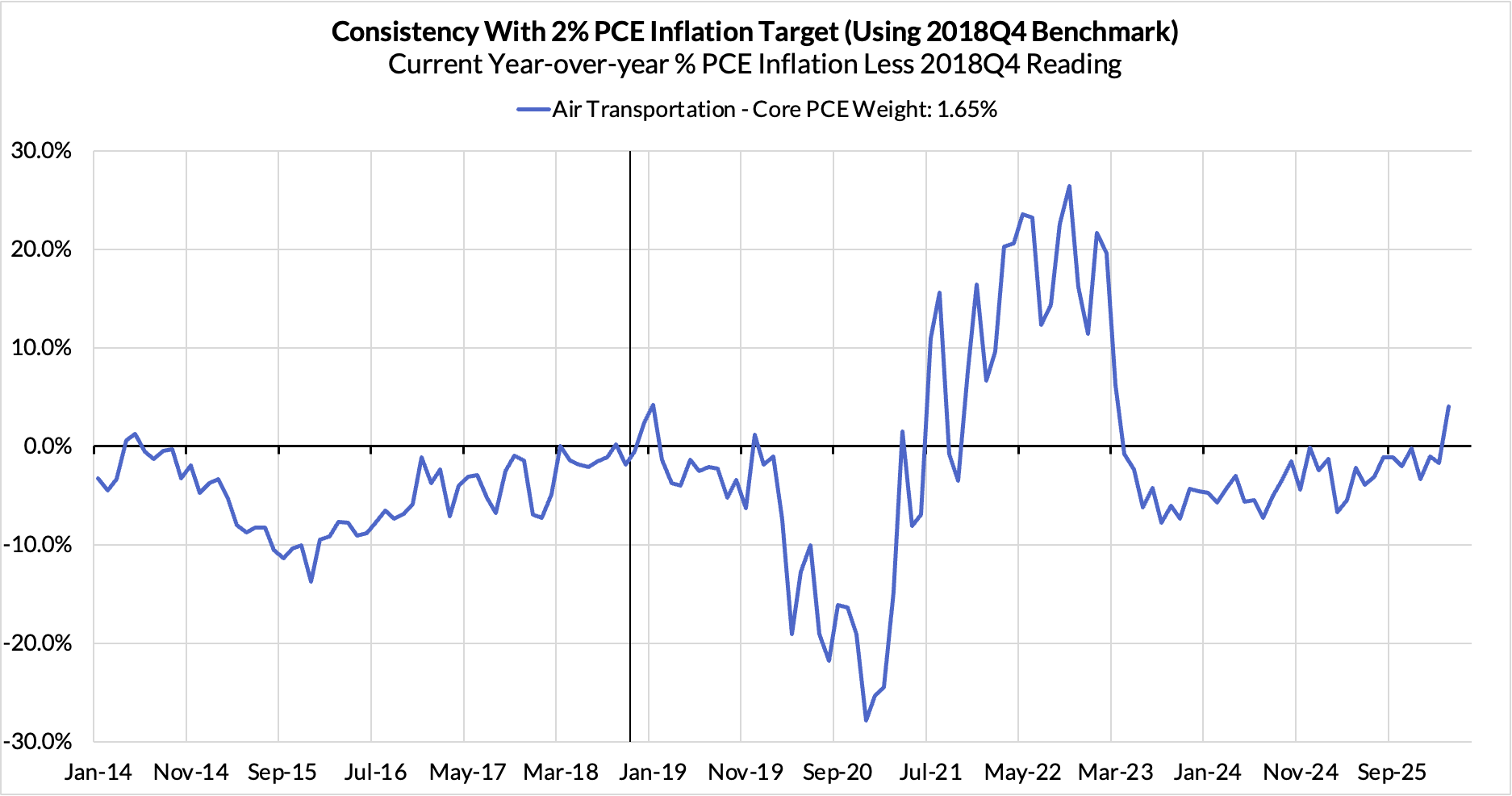

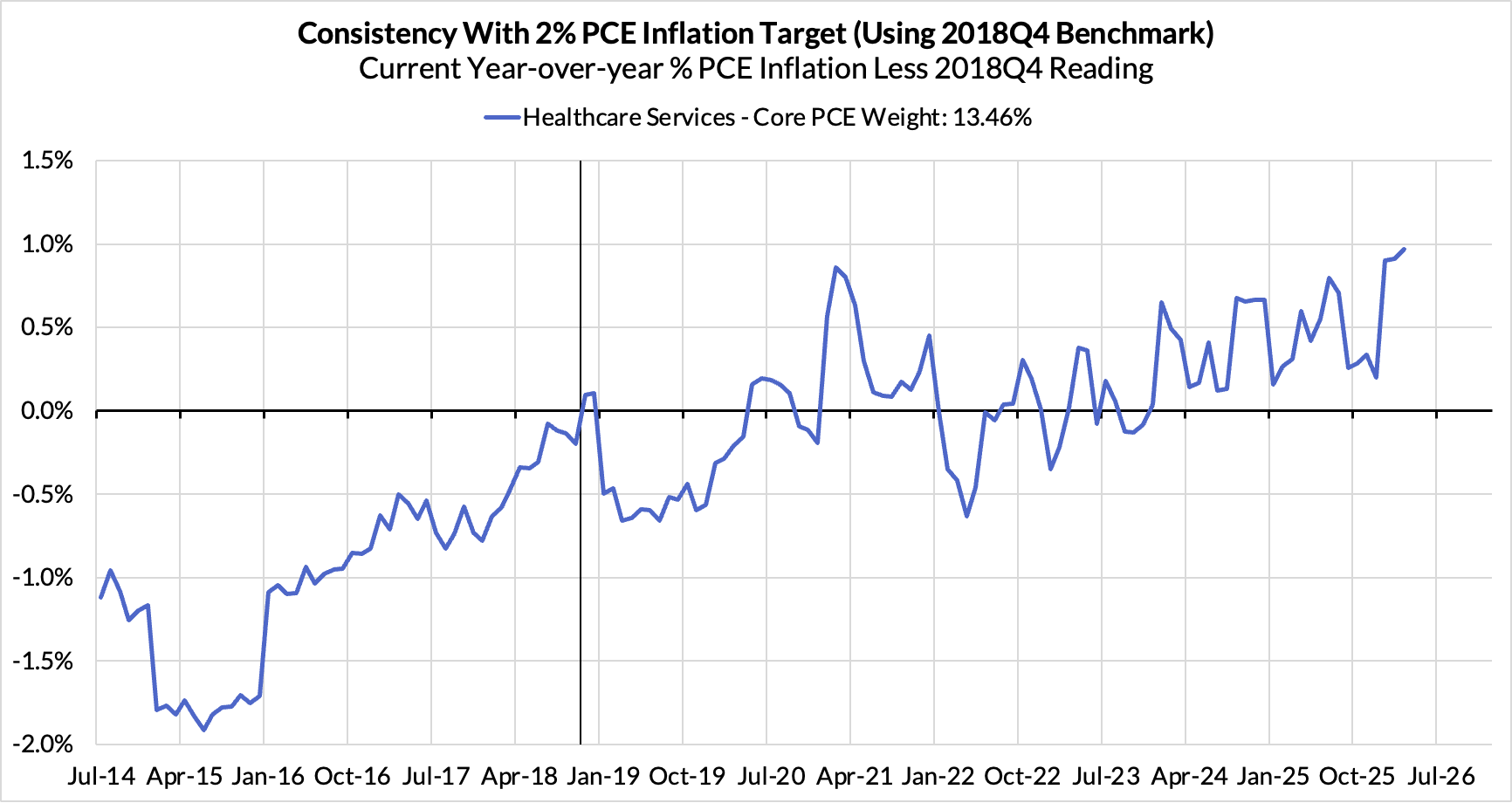

For the Detail-Oriented: Core PCE Heatmaps

Right now Core PCE (PCE less food products and energy) is on track to run at a 3.17% year-over-year pace as of March, 117 basis points above the Fed's 2% inflation target for PCE.

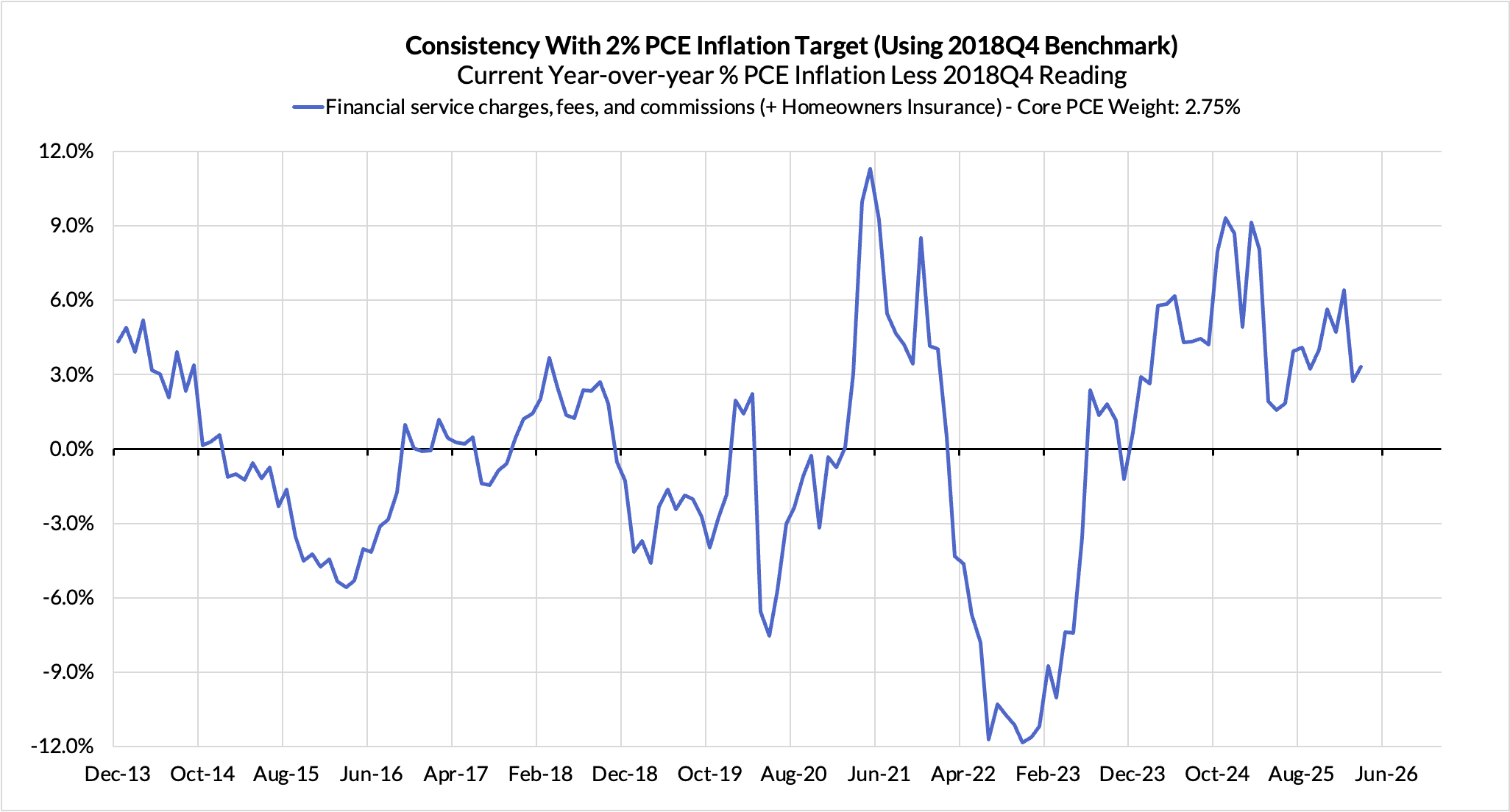

Equity market effects are adding 10 basis points to the overshoot.

Airfares are adding 8 basis points to the overshoot.

Food inputs likely adding 8 basis points to the overshoot.

Telecommunications and broadcasting are adding 4 basis points.

Healthcare services are adding 12 basis points.

The final heatmap below gives you a sense of the overshoot on shorter annualized run-rates. March monthly annualized Core PCE is on track to run at a 3.65% annualized pace, a 165 basis point overshoot vs 2% target inflation. These estimates are subject to some revision as more data gets released (IPI, GDP, PCE).

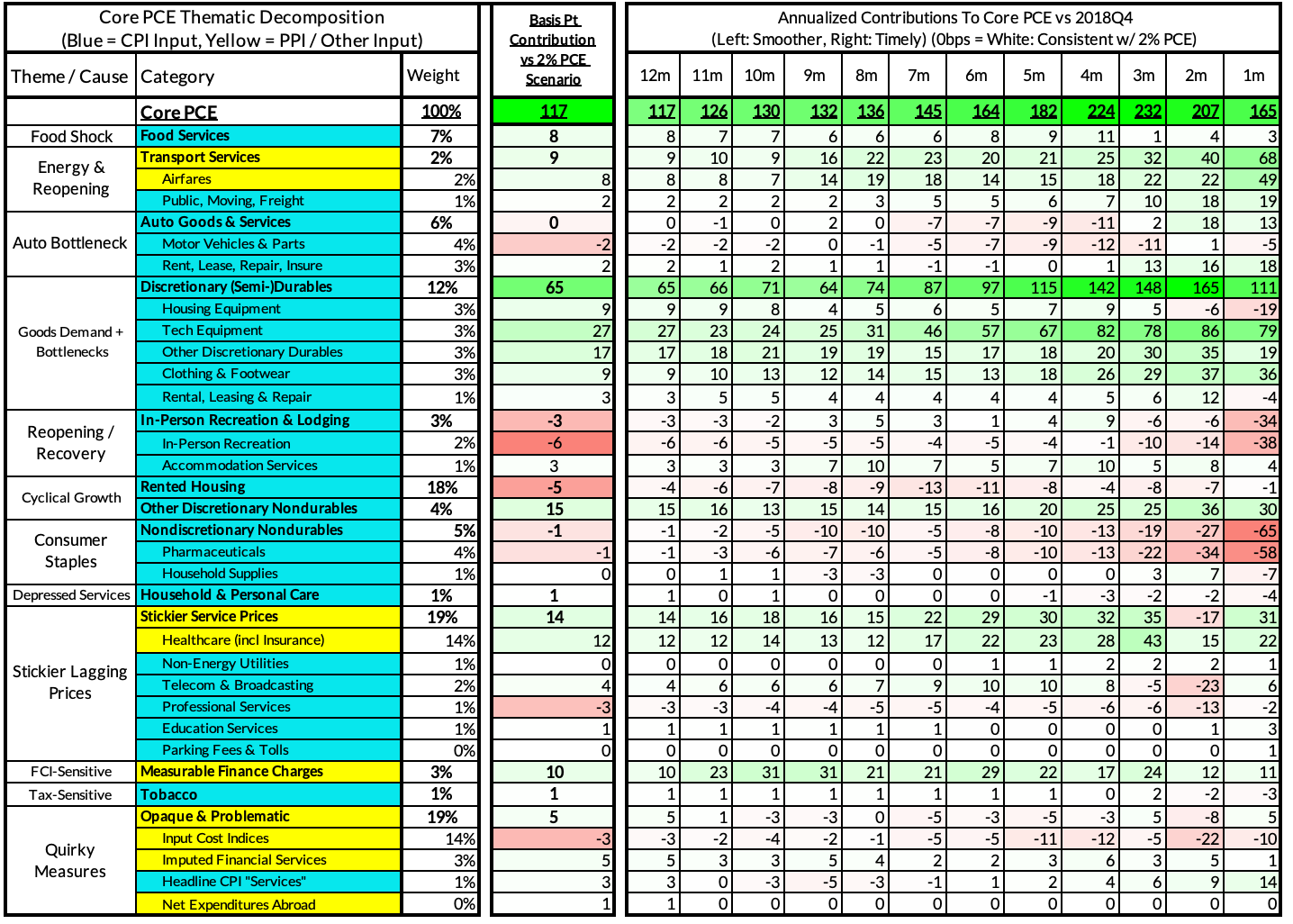

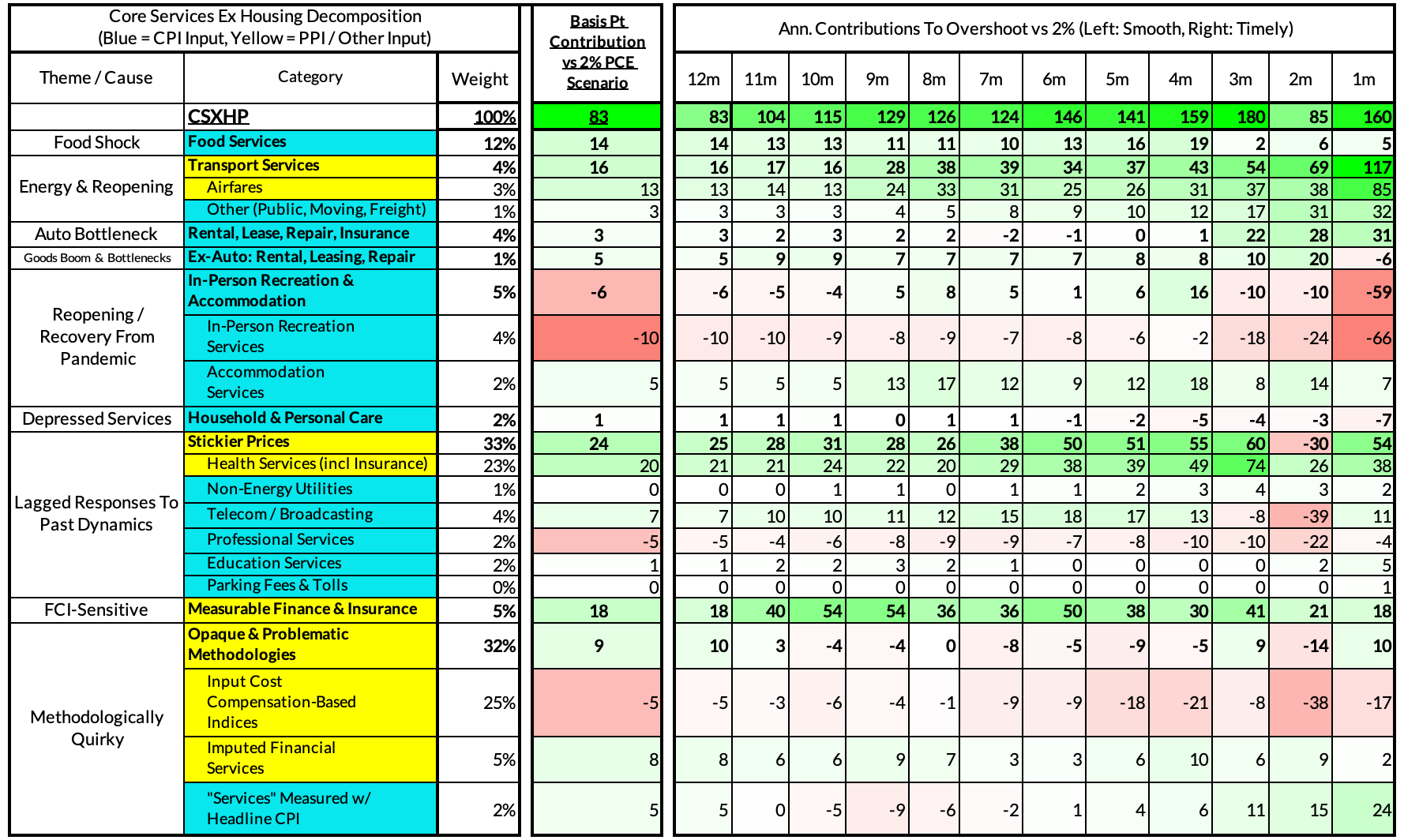

For the Detail-Oriented: Core Services Ex Housing PCE Heatmaps

The March growth rate in "Core Services Ex Housing" ('Supercore') PCE is on track to run at a 3.42% year-over-year pace, an 83 basis point overshoot versus the ~2.59% run rate that coincided with ~2% Headline and Core PCE inflation.

The March monthly supercore is on track to run at a 4.19% annualized rate, a 160 basis point annualized overshoot of what would be consistent with 2% Headline and Core PCE. These estimates are subject to revision as more data gets released (IPI, GDP, PCE).

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.