How The Fed Is Tracking Jobs Day

With jobs day coming up on Friday, it is important to understand how the Fed is tracking the labor market. In particular, it is crucial to not overindex to the monthly nonfarm payroll prints—something we have warned against since 2023. Revisions whiplash, a shifting "breakeven rate" (the number of net-jobs needed to keep up with population growth) from immigration dynamics and an aging population, and added volatility from recent changes to the BLS' birth-death model (which estimates the net creation and closure of businesses not yet captured in the establishment survey) make it difficult to extract a signal from monthly nonfarm payroll prints.

For those who are new here or need a refresher, the BLS releases two reports on jobs day: the Current Employment Statistics (CES, often referred to as the “establishment survey”) and the Current Population Survey (CPS, often referred to as the “household survey”). The establishment survey asks businesses how many employees they have each month while the household survey asks workers about their labor force status, which allows the BLS to calculate measures such as the unemployment rate, labor force participation, and employment-to-population ratios.

As we mentioned above, the establishment survey comes with a host of issues, but the household survey data also has its own set of issues. Since the CPS is a survey, the BLS creates aggregate figures using population weights. However, those population weights may not accurately reflect population changes in real-time, because migration data is difficult to estimate in real-time. Measures like total employment are therefore unreliable.

Instead, the Fed prefers to stick to ratio measures such as the unemployment rate, and the employment-to-population ratio, since migration affects both the numerators and denominators of those measures in a way that should mostly cancel out.

“you can point to the unemployment rate being stable, and in a world where both supply and demand for workers have come down very, very sharply over the course of the past year due to immigration policy largely, you know, a ratio is going to be a better thing to look at than job creation, for example.”

“If you adjust what has been the trend of job creation over the past, let’s say, six months, if you adjust that for what we think our staff thinks, is the overstatement due to overcounting, effectively there’s zero net job creation in the private sector. But actually that looks like that’s about what the economy needs in terms of dealing with very, very low—nonexistent, really— growth in the labor force, which, of course, we’ve never had in our history. So you’ve got a sort of a zero employment growth equilibrium.”

Chicago President Goolsbee 3/21/2026:

“The payroll job creation as an indicator of labor market slack, I think, is a little fraught at a moment when population growth and immigration…and there are a bunch of question marks about labor supply. So I prefer looking at rates…most of those have shown stability and are at levels that are closer to fuller employment than we are on the inflation target side.”

St Louis President Musalem 4/1/2026:

“Analysis by St. Louis Fed staff found that negative supply factors explain much of the private employment growth shortfalls from trend in February, as well as over the three, six and 12 months through February. This suggests to me that the unemployment rate and other ratios, such the vacancy to unemployed ratio, provide more information about current labor market conditions than payroll growth.”

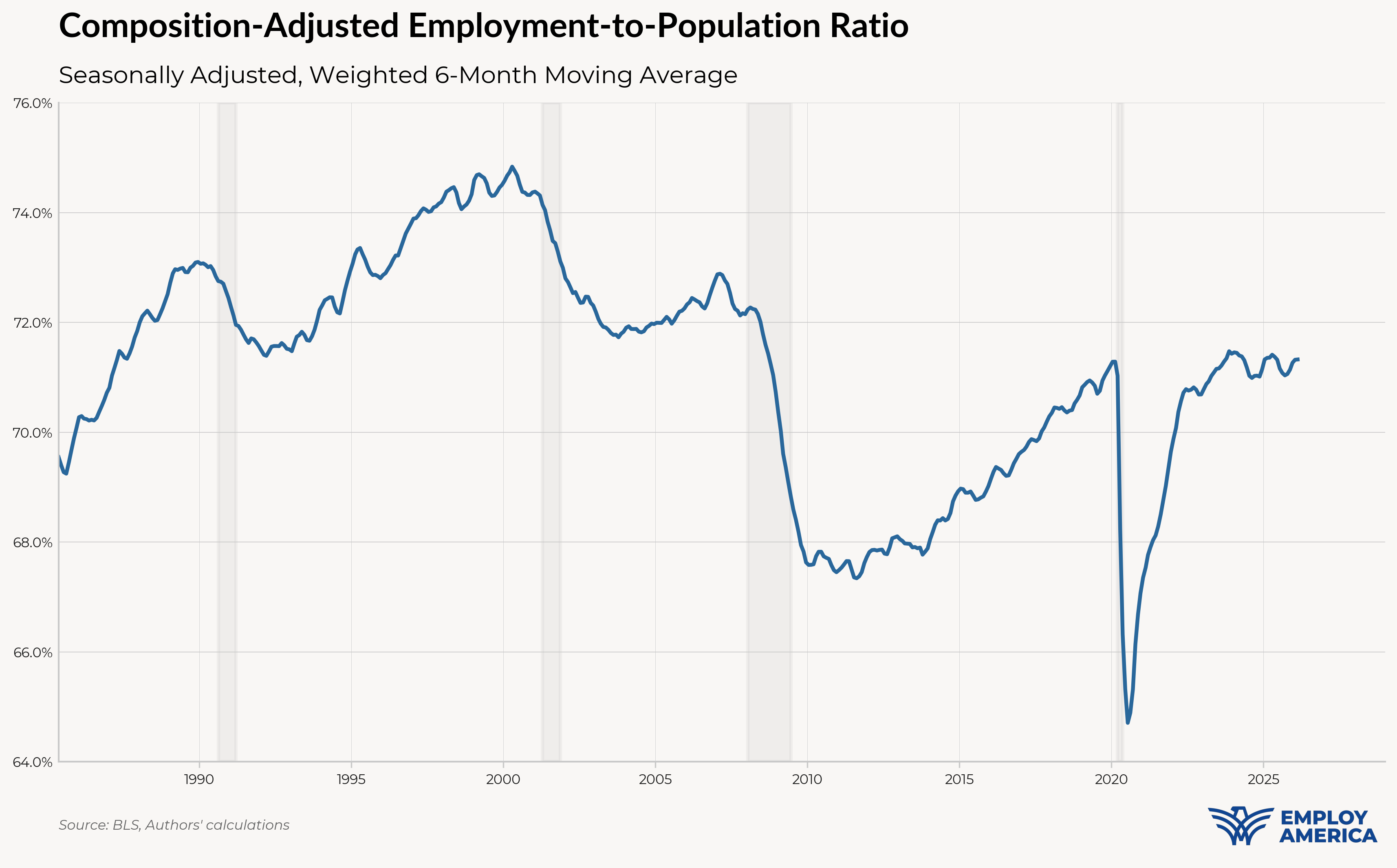

To provide the most robust measure of employment, we weighted the household survey’s employment to population ratio by 5-year age cohorts to match the current working age population. This allows us to match how the Fed is (or should be) tracking the household survey data.

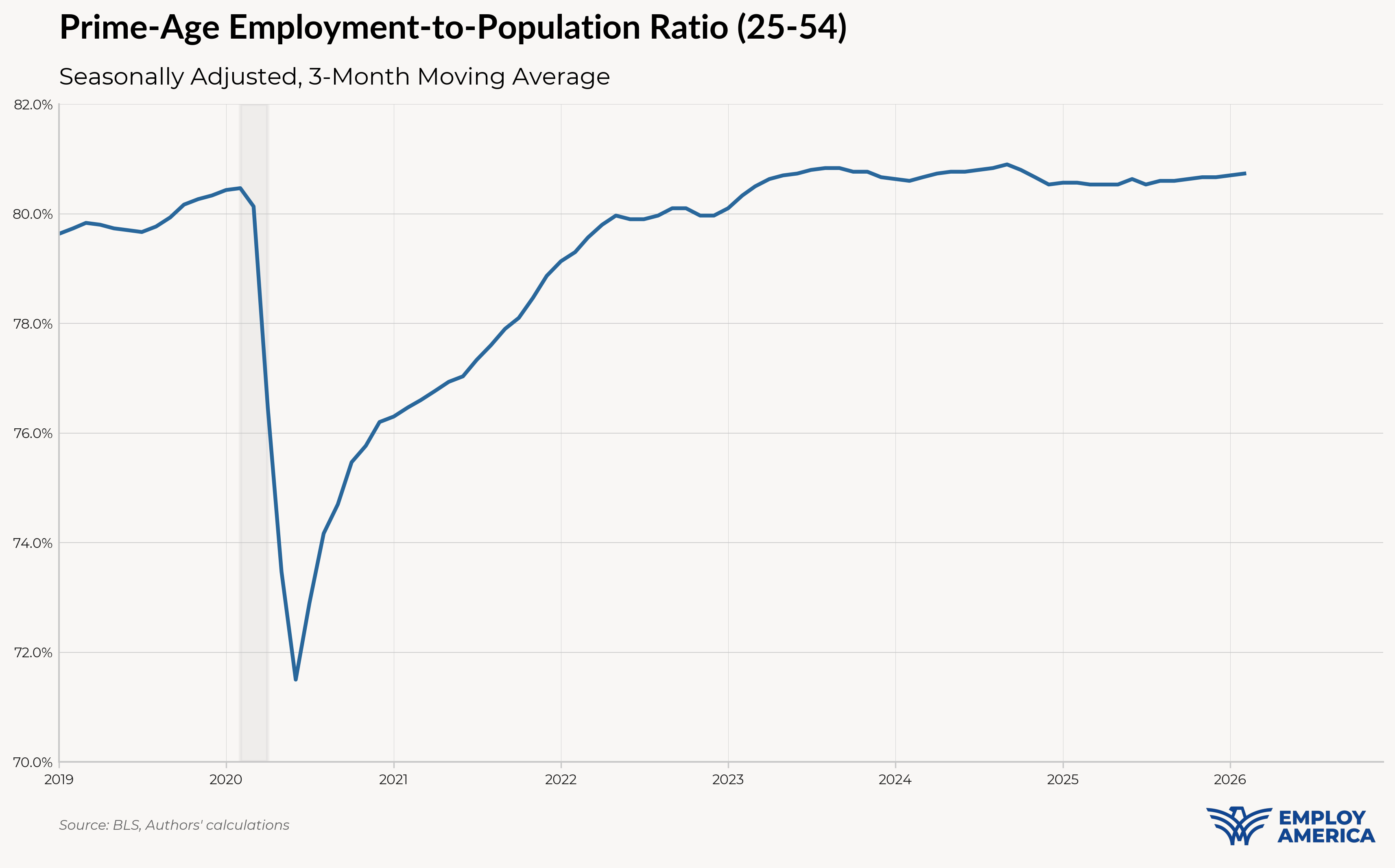

While this is not an easy thing to calculate on the fly, a simple but strong proxy to look upon release of the jobs day data is moving averages of the Prime-Age (25-54) Employment to Population ratio.

KC President Schmid 3/31/2026:

“prime-age individuals between ages 25 and 54 who are less affected by schooling and retirement decisions are participating in the labor market at higher rates than we’ve seen in decades. The employment-to-population ratio for prime-age workers is roughly at 2019 levels and well above average employment rates over the last 20 years. Simply put, with a large share of prime-age workers employed and earning paychecks, the labor market continues to support growth.”

Even though nonfarm payroll growth provides a murkier signal than before, Fed officials are still placing a significant weight on it. The standards for what counts as a “good” or “bad” payrolls number depends on the Fed officials and where they see the breakeven rate (the requisite increase in nonfarm payrolls to maintain the unemployment rate).

Most FOMC members are citing estimates of net population growth to justify their estimates of breakeven rates. For example, Alberto Musalem recently cited this estimate of immigration growth to argue that current nonfarm payrolls growth is on the “lower” end of breakeven growth. However, estimates of immigration growth vary and are difficult to produce. Other FOMC members have shared their views on breakeven payrolls growth:

Dallas President Logan (2/10/2026): “Since mid-year, monthly job gains have remained right around” breakeven

Minneapolis President Kashkari (9/3/2025): 75,000

Governor Barr (11/20/2025): Current labor market “near” breakeven

“You can say the break-even is zero” but that is “uncomfortable” (Mar. 2026)

“This low payroll growth does not necessarily indicate a weakening labor market, as it is likely connected to the fall in the supply of workers due to immigration policies and underlying demographics.”

“If that’s the case, then zero is the breakeven for net new jobs…my brain understands the math but I can’t get through my gut that this is okay.”

KC President Schmid 3/31/2026:

“In fact, job growth has averaged nearly zero over the past 6 months. However, there has also been very little growth in the size of the working-age population. Therefore, the economy doesn’t need to add many jobs to keep the unemployment rate stable.”

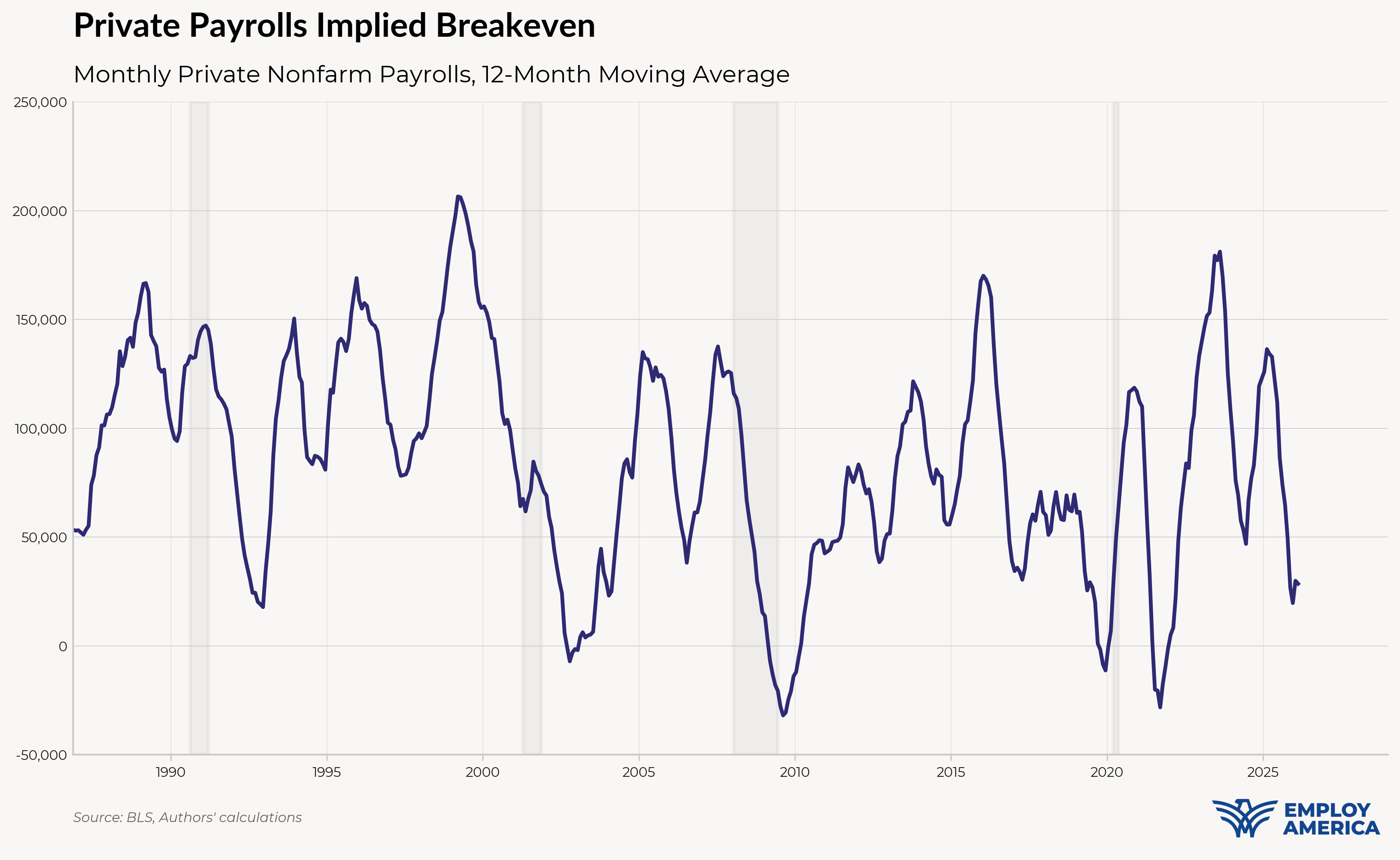

It’s important to note that some of these estimates were given months ago, and FOMC participants’ views of breakeven growth are changing. Given the near-zero payrolls growth (after revisions) over the past six months and the relatively tame behavior of the unemployment rate, it’s likely that participants are revising their estimates of breakeven downwards. For example, Jeffrey Schmid gave a breakeven estimate of 50,000 just six months ago, but seems to believe that it could be near-zero now.

The coincident low performance of payrolls growth and relatively stable employment rates does indeed imply that breakeven payroll growth has fallen. Below, we take the difference between payrolls growth and observed changes in employment rates (after adjusting for differences in establishment and household survey definitions) to back out an implied breakeven rate (for the employment-population ratio). We currently estimate that 40-50k private NFP prints represent an outperformance for monthly payrolls. This is still a work in progress, and we will have more details about our breakeven methodology in a subsequent post.

We shifted our base case to no interest rate cuts for 2026 due to upside inflation risks that preceded the Iran War and have since intensified — the last three months of inflation data has been running close to 4% annualized, double the Fed's 2% target. Fed pricing has evolved considerably and has been volatile over the last couple of weeks – oscillating between hikes and cuts being priced in. Downside risks to the Fed's employment mandate are present alongside the upside inflation risks, but the labor market looks like it is bending rather than breaking, with the household survey presenting a more resilient picture than what the establishment survey may imply.

The Fed has signaled an indefinite hold amidst conflicting risks to its dual mandate. However, FOMC members still maintain that they’re willing to cut if the labor market does look dangerous. With nonfarm payroll prints likely to be volatile going forward, it is important to focus less on the headline payroll numbers and closely track ratios and the evolution of breakeven payroll estimates.