Though they may proclaim otherwise, the Fed is aiming for a recessionary labor market. They might not succeed, they might change their minds, but buried in the Fed’s latest projections is a definite–albeit obscured–statement of intent.

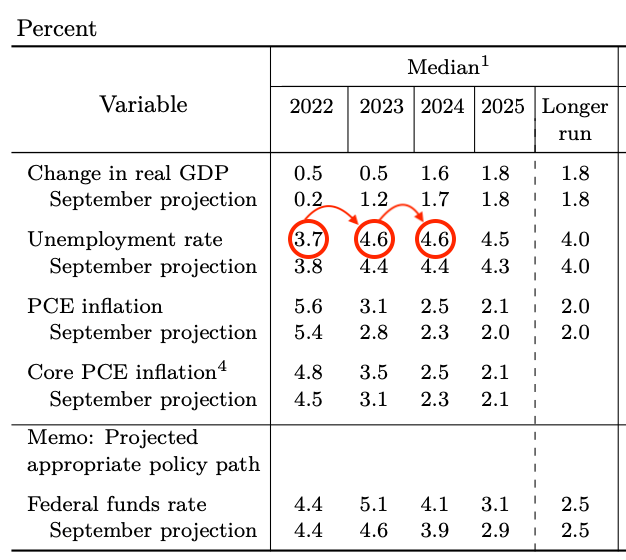

Table 1. Economic projections of Federal Reserve Board members and Federal Reserve Bank presidents, under their individual assumptions of projected appropriate monetary policy, December 2022 [excerpt, emphasis added]

“Well, I’ll tell you what the projection is. I don’t think it would qualify as a recession" Chair Powell at the latest FOMC press conference on December 14, 2022.

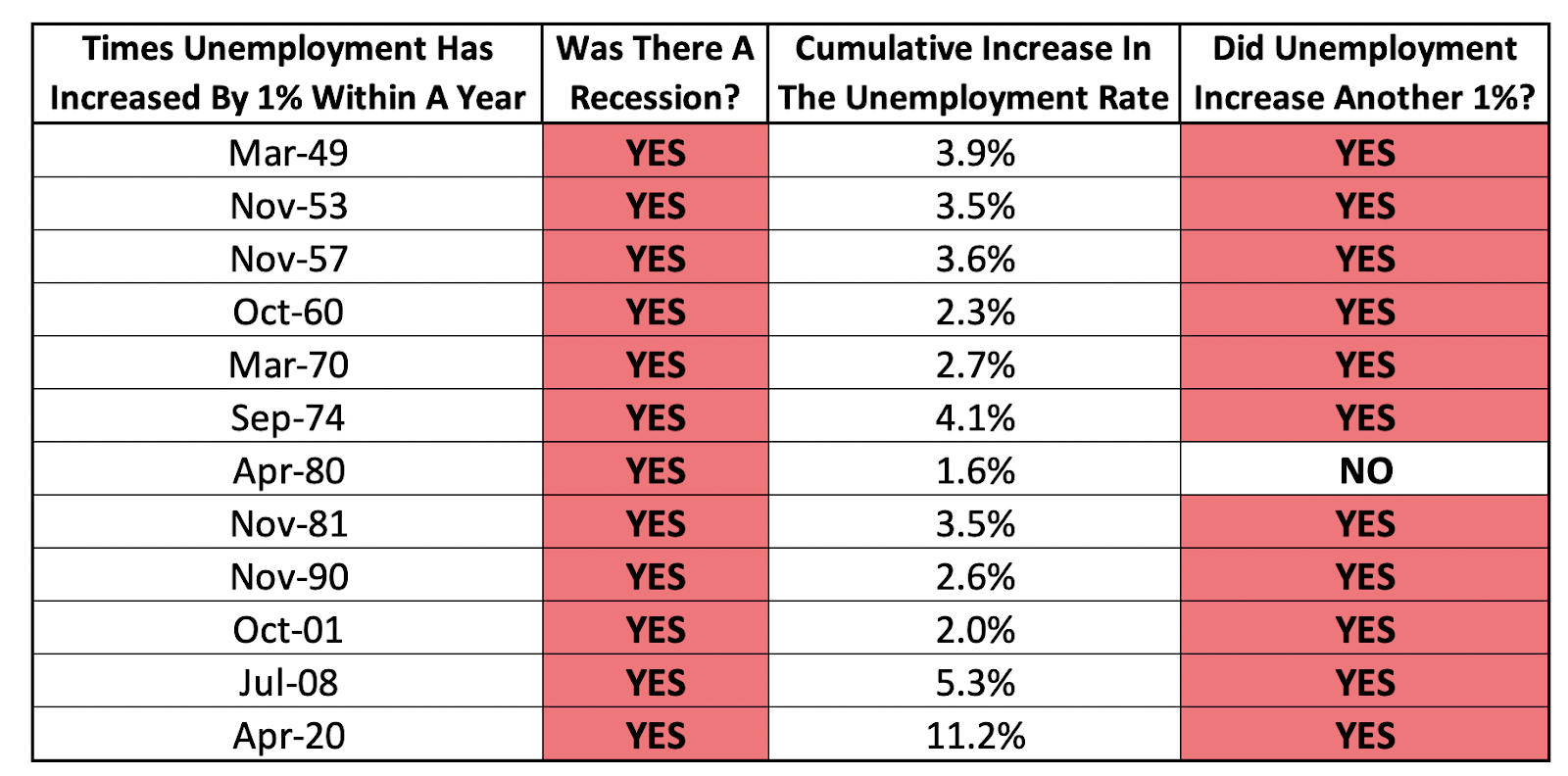

Though they may proclaim otherwise, the Fed is aiming for a recessionary labor market. They might not succeed, they might change their minds, but buried in the Fed’s latest projections is a definite–albeit obscured–statement of intent. The Fed is projecting that the unemployment rate – which reached a low of 3.5% in December – will increase by at least a percentage point (to 4.6%!) by the end of 2023 under “appropriate monetary policy.” The unemployment rate has only increased by 1% within a year twelve times since World War II. Every time, (1) we saw a recession, (2) the unemployment rate continued to increase far beyond the initial 1%.

Simple back-of-the-envelope math says that a 1% increase in the unemployment rate represents a net loss of nearly 1.5 million jobs over one year, assuming the Labor Force Participation Rate (LFPR) holds steady. If LFPR falls with employment, as it traditionally has during recessions, the Fed could plausibly be targeting as many as 2 million jobs lost or foregone.

Yet the Fed is now announcing that it intends to defy both historical trends and common definitions. Instead of defending or justifying the predictions made in the December SEP, Fed officials have argued that the outcomes they are aiming for are (1) not recessionary and (2) that the unemployment rate will immaculately and immediately stabilize. As the pandemic has amply shown, even the most durable regularities can break down. But extraordinary claims warrant extraordinary evidence, and explanation. Instead, the Fed’s projections risk landing on the border of self-delusion and obfuscation.

Recessions are serious. They rightly receive outsized attention because of their employment effects, and not because of what the NBER ultimately says or what the GDP data shows over two quarters. These effects carry tremendous human costs and take a long time to recover from. In the examples in the table above, a full recovery in the unemployment rate – to say nothing of the measured Labor Force Participation Rate – was only achieved with the benefit of substantial time and policy support. To justify engineering a recession, the reasons for doing so must be equally serious and transparently explained.

In previous pieces, we have discussed the primary causal mechanism that we think links labor market deterioration to slower inflation. As simply as possible, the Fed’s rate hikes tighten financial conditions and pressure businesses to slow spending on payroll; lower employment and/or wage growth lead to lower consumer demand growth, which is then meant to translate into lower inflation. But if the Fed intends to increase unemployment by 1% using these tools, they will have to continue hiking aggressively enough to trigger widespread job loss, not just a collapse in openings or a slowdown in hires.

Some might say this recessionary increase in unemployment is merely a side effect of their quest to lower inflation. Yet Fed officials have largely expressed views closer to our own: the labor market is the central vehicle through which the Fed influences inflation.

This was already clear at the November FOMC meeting. When pushing back against Neil Irwin’s suggestion that the Fed’s tools are mostly affecting the housing market and not inflation itself, Chair Powell pushed back, citing the labor market as a main source of disinflationary traction:

Where we firmly depart from the Fed is in the aim. It is one thing to aim for slower growth in employment and wages; it is another to aim for outright job loss, that too at a recessionary scale.

So what exactly do the Fed’s projections under appropriate monetary policy reflect? First, a Fed-induced recessionary surge in the unemployment rate. Second, an “immaculate stabilization” whereby the labor market abruptly normalizes at this elevated unemployment rate with no further recessionary damage inflicted. Their projections suggest that this “immaculate stabilization” will only require 100 basis points of cuts to materialize in 2024, that too only after unemployment begins persistently rising.

In the December SEP, year-end unemployment rises from 3.7% in 2022 to 4.6% in 2023, but then remains at 4.6% in 2024. The first step is consistent with a world where the Fed hikes the economy into recession in an attempt to cool off inflation, but the second step amounts to a convenient delusion.

While the economy is more complicated than simple kinematics, it is well-understood that the trend in the unemployment rate has a substantial amount of inertia. Once it begins to rise, the risk of it rising further is highest. A large enough impulse to slow, stop, and then reverse recent labor market progress is almost certainly a big enough shock for unemployment to rise well past the 1% increase the Fed is predicting. Unemployment increases of this size have never stopped on a dime.

So far, the Fed has avoided acknowledging this recessionary aim. They have good reason to: the Fed using its independence to reverse the hard-won labor market recovery is difficult to defend to Congress or the public.

If the Fed wants to cause a recession, they seem to be in no rush to defend it transparently. Recessions have catastrophic and deeplyunequal consequences for those who lose jobs and wages as a result. The case for the Fed’s intentions is a case that the human costs of a substantial unemployment increase are justified. If “this time really is different,” and the unemployment rate really will stabilize without mass layoffs, the Fed needs a better explanation than the one Chair Powell most recently provided.

The “overhang of vacancies” argument looks especially flimsy in light of the well-documented methodological and empirical shortcomings uniquely associated with job openings data. Job vacancies do a poor job of explaining hiring rates (which have, incidentally, already returned to pre-pandemic pace): most hires take place outside vacancies and recruiting intensity per vacancy varies over time. Many have pointed out that job openings, inflation and wage growth have all remained elevated over the past two years. Yet, before these last two years, the full predictive track record reveals an unimpressive and unreliable relationship. For policy decisions that risk the livelihoods of millions of Americans, one would hope the Fed is not jumping from coincidence to causal inference.

The rest of Chair Powell’s stated reasons come close to anecdotal claims that employers might choose to hang on to more workers amidst a “structural labor shortage.” With employment fully recovering on an age-adjusted basis (outside of part-time septuagenarians), this newfound appeal to “structural labor shortage” looks more like a post-hoc fudge factor–we’ve known for a long time that the US population is aging. Given the Fed’s resources and unique independence and policymaking discretion, one would expect claims to be rooted in systematic data analysis and affirmatively identified causal mechanisms.

We hope the Fed is not trying to be disingenuous here, but the aims implied in the Fed’s projections reflect some troubling outcomes and consequences. The immaculate stabilization the Fed envisions–in the absence of an assumption of strong monetary or fiscal policy support–looks more like “just a flesh wound” denialism to avoid reckoning with the full implications of their intentions. Yet it would not be the Fed losing limbs over the next year, but rather everyday Americans losing jobs. For everyone’s sake, let’s hope these unemployment rate projections don’t come to pass.

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.