Who is Driving the Labor Shortage? Part-time Over-70 Workers

Much ado has been made about the shortfall in the headline employment-to-population ratio and the headline labor force participation rate of late. Many have claimed that recent wage and price pressures trace back to a “labor supply shock”. Some have even tried to make the more nuanced claim that this disappointment holds even after controlling for demographic effects, with specific attention given to workers aged 55 and older. The employment rate of this group in October was 37.9%, compared to its pre pandemic high of 40.5% in July 2019.

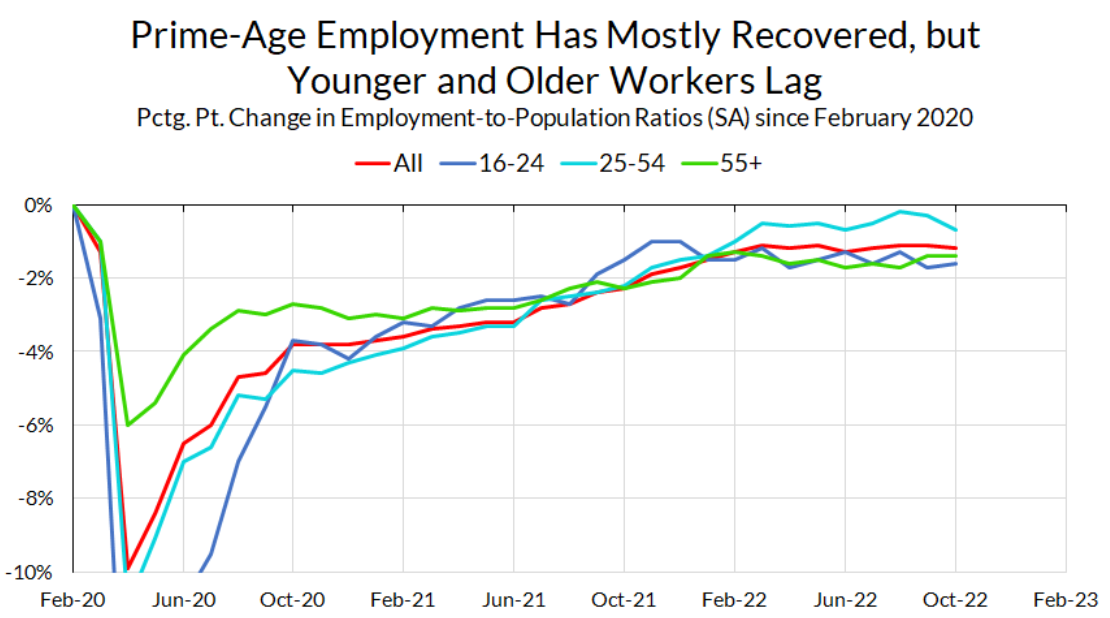

This morning, the Bureau of Labor Statistics released the new Employment Situation Report. As was true in previous months, the data show a strong recovery since the pandemic recession, although there are signs of weakening in the household survey. The prime-age (25-54) employment-to-population ratio fell from 80.2% to 79.8%, slightly lower than its pre-pandemic high of 80.5%. The all-age employment-to-population, however, has not seen the same recovery since the pandemic started. The labor force participation data shows the same pattern.

Some have pointed to stagnant employment rates among older workers as evidence of a labor supply issue. However, in reality, most of this decline is attributable to the aging of the population and a reduction in part-time employment among workers aged 70 and older. In the context of what counts as a strong employment recovery from a pandemic with disparate impacts on the elderly, it is not apparent that there has been critically “missing labor supply” from those older workers that can—or should—be brought back.

“Early retirements” in this older population have been explained in various ways: concerns over COVID, strong balance sheets after a strong fiscal response and stock market returns, or a reevaluation of work-life balance preferences. At the same time, there are concerns that early retirements in this group are presenting a significant drag on labor supply. In a speech last month, Lisa Cook cited early retirements as a cause of stagnant labor supply. Jay Powell has cited “subdued” labor supply as one source of labor market tightness (and implicitly, inflation) in both his May and June FOMC statements.

Labor demand is very strong, and, while labor force participation has increased somewhat, labor supply remains subdued.

– Jay Powell, May 4, 2022 FOMC press conference

In the post, I explain why concerns over these so-called “lost workers” as a source of labor supply issues are overblown. The predominant explanation for the employment shortfall is the aging of the workforce, not lower employment rates within age groups. The shortfall of older workers is primarily concentrated among workers over the age of 70, and specifically those who were working part-time. While there have been economically consequential acute labor shortages in particular sectors—like trucking, construction, and oilfield services—any wage, price, and bottleneck pressures in these sectors cannot be credibly attributed to the shortfall in employment and participation among these elderly cohorts.

What then accounts for the overall shortfall in employment? To answer this question, I decompose the change in the overall employment rate between before the pandemic and now into an “aging effect” and an “employment effect.” The aging effect is the change in the overall employment rate that is attributable to the changing age composition of the population, holding the employment rates of age groups constant. Conversely, the employment effect measures the effect of changes in the employment rates of age groups, holding the age composition constant.

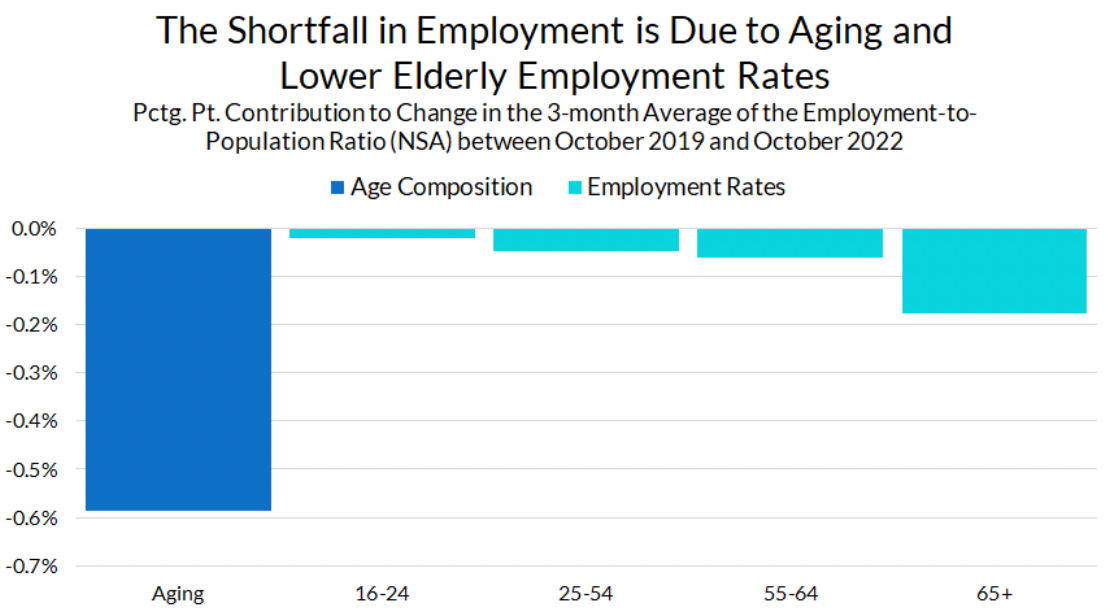

The chart below shows the decomposition of the employment shortfall into these aging and employment effects. Importantly, I use narrow age bands to calculate the aging and employment effects, which allows me to distinguish between older working-age workers (55-64) and the 65+ population. Since the narrower employment rate data is only available on a non-seasonally adjusted basis, I compare the average of the three months ending October, 2019 to the three months ending October, 2022. [1]

The decline in the overall employment rate was 0.89pp. Of this decline, the aging effect accounts for 0.58pp, about two-thirds of the total decline. The “failure” of employment to rebound to pre-pandemic levels is not primarily explained by some decreased “willingness to work”, but rather the steady aging of the population.

The remainder of the decline in employment, 0.30pp, is accounted for by the employment effect. This employment effect is in turn mostly explained by a decline in the employment rate of the 65+ population. The decline in the employment of workers between the ages of 55 and 64 (workers who would potentially be taking “early retirement”) accounts for only a minimal part of the overall decline.

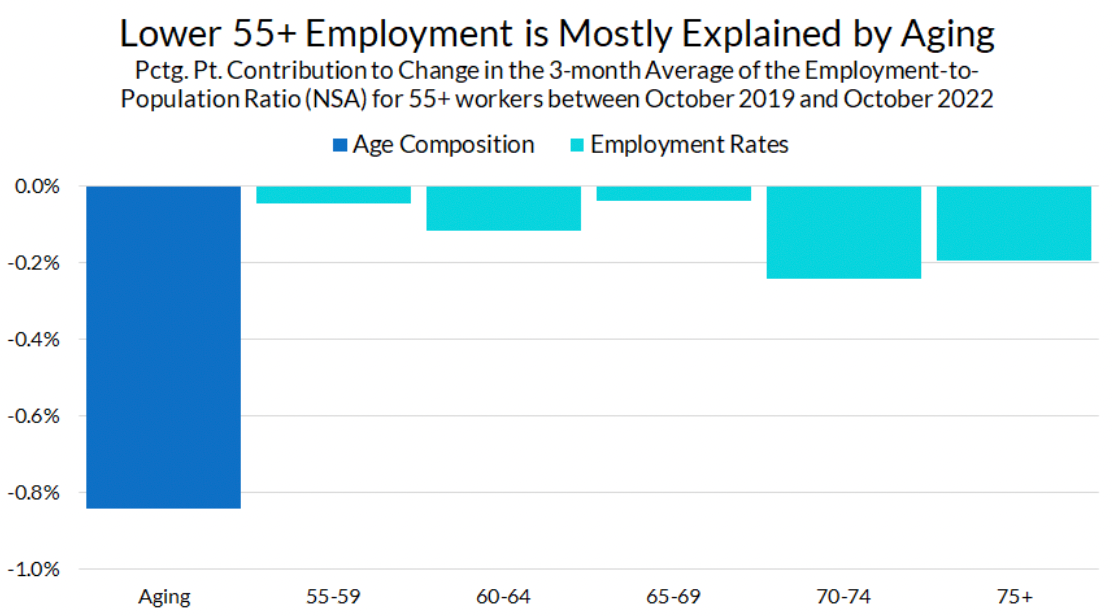

When one takes a closer look at the decline in employment rates in older cohorts, the proposition that the sidelining of these workers is a significant source of “labor shortages” becomes even more strained. In the chart below, I repeat the decomposition exercise for the decline in 55+ employment rates.

As with the overall population, the fall in employment rates among the 55+ population is mostly due to aging within this population. The contribution of the employment effects is concentrated mostly among the oldest among the older workers, those above the age of 70, not the workers between 55 and 69 mostly characterized in the media as affected by “early retirements.” If employment rates of workers aged 55-69 returned to pre-pandemic levels, the overall employment-to-population ratio would only increase by 0.075pp, less than one-tenth of the overall shortfall.

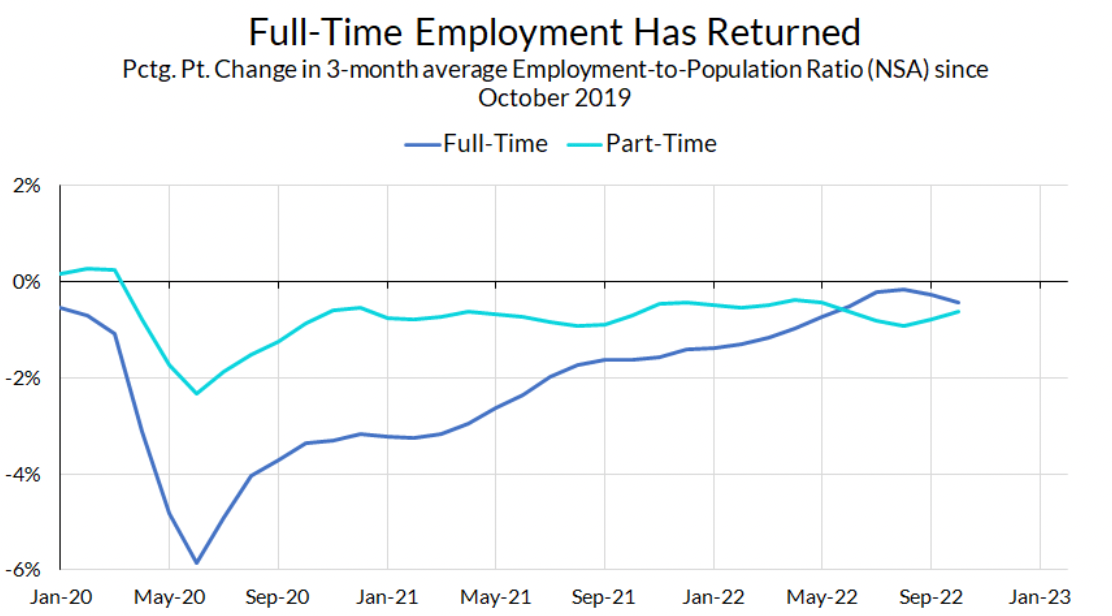

Another reason the labor supply shortage story is overstated is that full-time work (35 or more hours a week) has now nearly fully recovered, and the shortfall in employment is predominantly due to lower rates of part-time work (less than 35 hours). The proportion of the population (3-month moving average) working full-time is only 0.4pp lower than three years ago, while part-time work is 0.6pp lower.

Data on part-time vs. full-time work for older workers is not as disaggregated or frequent as the overall data, but what is available suggests that the decline in employment among older workers is also mostly due to declines in part-time, not full-time, work. The proportion of Americans 65 and older usually working full-time actually increased between 2019 and 2021 (annual averages) by 3.3%, from 6.42 million to 6.63 million. Meanwhile, the number of part-time workers in this age range fell by 11.0% in the same period, from 3.93 million to 3.49 million.

To sum up: the all-age employment-to-population ratio has not caught up to pre-pandemic levels for reasons not primarily due to work disincentives, fiscal support, or nebulous “quiet quitting” phenomena. Rather, the bulk of the fall in employment is attributable simply to the aging of the workforce. The remainder of the shortfall is better characterized by a reduction in septuagenarians working part-time jobs, not early retirement of the working-age.

While there might be acute labor shortages in particular areas, such as pilots or construction workers, these are probably not shortages that are likely to be resolved by “bringing back” part-time elderly workers. In short, it does not appear that there is a substantial labor supply issue in an aggregate sense.

Moreover, this decomposition exercise clearly shows just how successful the labor market recovery has been over the last two years. The sluggish labor market recovery following the Great Recession left many workers on the sidelines for years. Thankfully, the COVID recovery has been much more rapid, due in large part to the strong fiscal and monetary policy response.

However, the October jobs report shows worrying signs of a deteriorating labor market. The prime-age employment-to-population ratio continued to fall from 80.2% to 79.8%. Unemployment ticked up to 3.7%, and full-time employment fell. If trends continue, we risk giving back the gains from the strong labor market recovery. Policymakers need to take this risk seriously.

[1] Jay Powell (and others) have framed the labor shortfall in terms of labor force participation, rather than employment. A similar exercise decomposing the shortfall in labor force participation shows the same story as this decomposition for employment.