Calendar Year Price Revisions Skew Risks To The Upside in January, But The Balance of Risks May Shift Soon After

January is always a high-variance month for inflation readings and especially so for this January. We have been flagging the dynamics that were likely to grease the runway to elevated inflation prints in Q4 (which mostly materialized as described). We expect general strength in the January inflation print, primarily due to stickier prices getting revised at the turn of the calendar year, as a lagged response to supply chain cost pressures and a robust recovery in demand.

Calling an individual month's inflation reading is close to a mug’s game (been there, done that), but there are risks to the upside and downside that we think are worth flagging. For January, we could see the core inflation month-over-month reading running wthin the blazing hot Q4 ballpark (~0.5%-0.7%). As we move through the rest of 2022, the inflationary upside risks are likely to diminish and the downside risks may grow more prominent.

Two Major Upside Risks For January:

Upside Risk #1: Calendar Year Price Revisions (Household Supplies, Furnishings, Packaged Food Products, Food Services). From staple consumer products to durable goods, we’ve seen a number of major industry-leading firms (Procter & Gamble, Kimberly Clark, IKEA, Hershey) announce that they would be raising prices in January, at least partially as a lagged response to elevated logistics costs, input shortages, and strong demand. Even though this is a lagged effect to 2021 dynamics, the outsized December-to-January price increases (relative to the usual seasonal factor) suggests substantial upside risk in categories where demand and pricing is not subject to regular seasonal revision (in contrast with apparel prices). These price increases could be especially sharp, but they also represent limited forward-looking informational content about the forward trends in prices. Some services prices may drive the trend of inflation, but it's usually goods prices that drive the volatility of aggregate inflation readings.

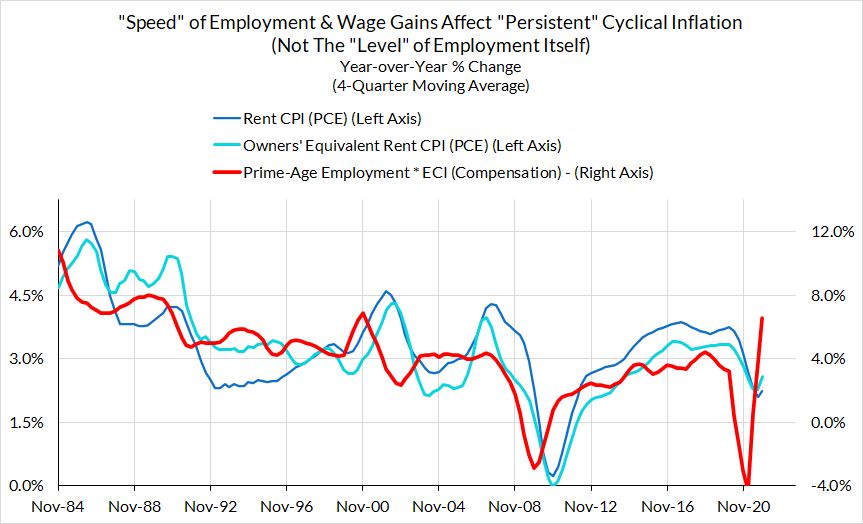

Upside Risk #2: Rent Inflation Catch-Up In Remaining Geographies. Rent inflation is important because it 1) has a high weight within core inflation, 2) is highly cyclical (with a lag), and 3) is highly autocorrelated, such that recent monthly reading is a pretty good guide to the next 12 months. Rent inflation saw substantial acceleration in Q3 and Q4 but has also seen signs of stabilization in terms of the monthly percent change. That said, it should not come as a total shock if we see some further upside risk in January and February among the metropolitan statistical areas with lagging rent markets (New York, Bay Area, Philadelphia, Los Angeles, Boston). The strongest MSAs in terms of rent CPI have seen one outsized increase; if the cyclical recovery simply took more time to hit some of the lagging MSAs, the risk of a monthly pop in some of the lagging markets is elevated.

Downside Risk #1: Auto supply chain (after January). The automobile-related components are showing marginal signs of stabilization and arguably some scope for payback in 2022. Both Blackbook and Mannheim are signaling that we have exited the strong-patch of used car inflation we saw in Q4 of 2021. While the chip shortage hampered new supply of automobiles, the voracious demand from rental car companies was likely the more proximate factor driving the surge. Rental car companies have reportedly recovered most of their fleets now (fleets they previously liquidated in 2020). With demand cooling and signs of improving supply over the course of 2022, the balance of risks to motor vehicle components should begin tilting to the downside soon (after a 55% increase in used car prices in the past six quarters).

Downside Risk #2: Healthcare (January PPI + after January). Congress had a chance to push down healthcare services PCE inflation readings down in January itself but chose to punt the opportunity out to April, the next opportunity for the Medicare sequester to bite. Nevertheless, the January PPI reading (which feeds into PCE) should still show a much milder monthly increase than what we saw in January 2021. The January 2021 was caused by some technical changes in how physician services were classified (a change in E/M codes) and some of this effect was even visible in December 2020 & January 2021 CPI. This was a policy-induced effect that should not be visible in year-over-year readings for physician services (CPI/PPI/PCE) from here. Finally, there are nascent signs of elevated competition in the healthcare space, including cheaper hearing aids and prescription drug prices. Of course, such price changes in the real world do not always get picked up perfectly in the surveys used for calculating inflation. These dynamics are best seen as outlier risks than as something that can reliably feed into the inflation data.

Downside Risk #3: 5G Rollout (after January). For regular observers of inflation data, it should come as no surprise that quality-adjustment can have a substantial influence on telecommunication service prices and aggregate core inflation readings. We saw this play out in 2017, when the release of unlimited data plans drove a 10% decline in wireless telecommunication service prices. It's still not totally clear how the BLS' attempt to adjust for quality will factor in the transition to 5G over the course of the year, but it's worth flagging the potential downside here.

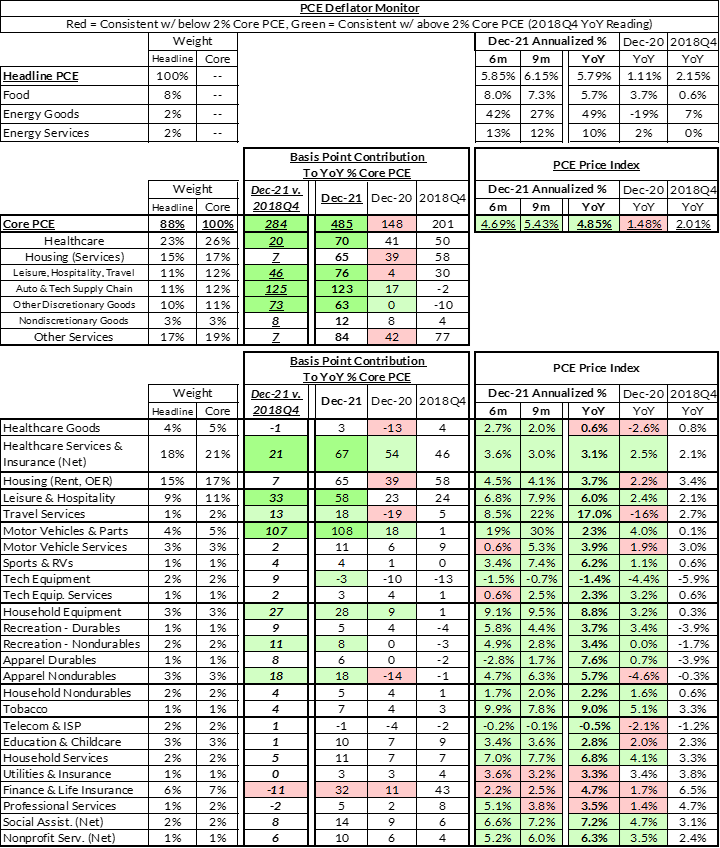

Appendix: December 2021 PCE Decomposition