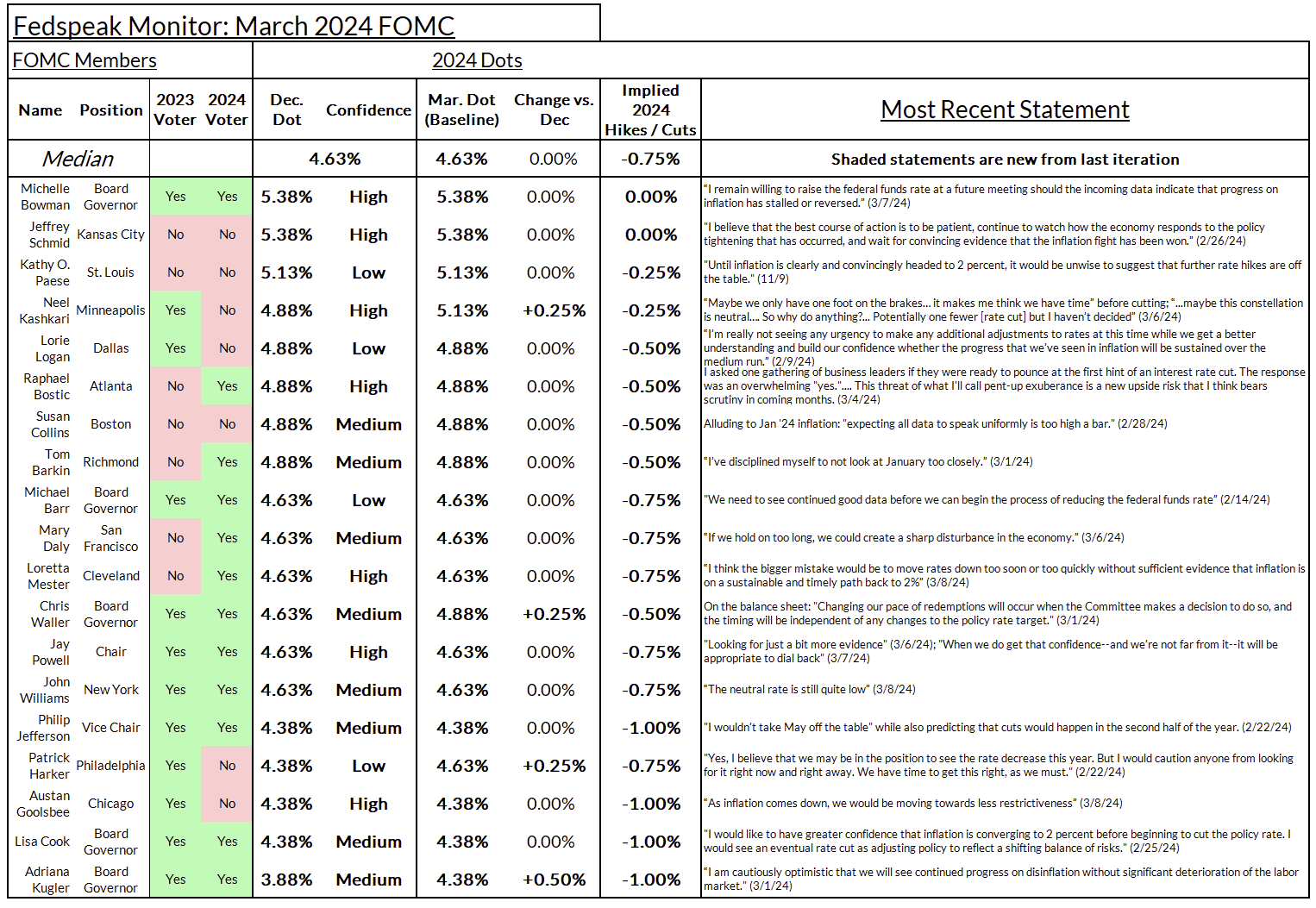

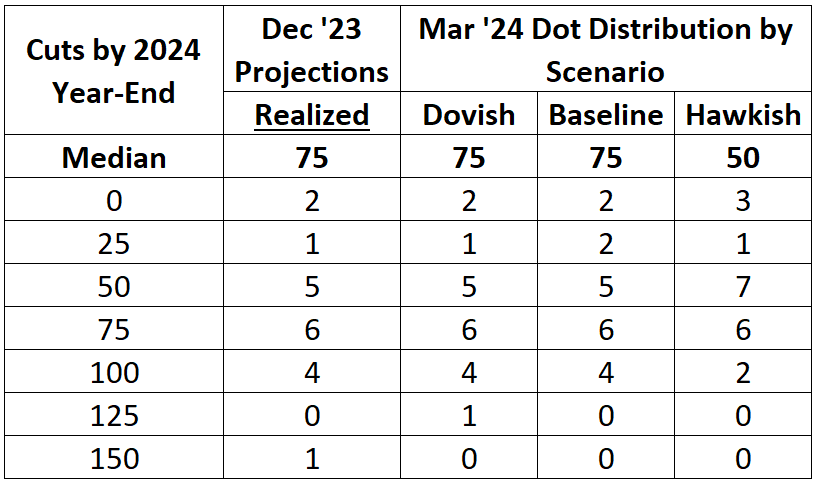

Our baseline forecast of the dots sees most of the dots holding steady, with some dots taking cuts off for this year. . This leaves three cuts as our baseline median dot—but just barely.

If you enjoy our content and would like to support our work, we make additional content available for our donors. If you’re interested in gaining access to our Premium Donor distribution,please feel free to reach out to us here for more information.

Latest Fedspeak and Our Dot Projections

What to look for:

A Hold: A March cut was taken off the table in January and none of the data since then has re-opened the door. A June first cut is the solid base case at the moment. With CPI and PPI portending a warm February core PCE print, a May cut looks to be very improbable. Between the March and May meeting, the Committee will see one more jobs report (covering March, in early April) and one more month of inflation (March, in mid-April). With two hot months of inflation in a row, the Committee will likely want to see two softer months of inflation before cutting. It wouldn’t be out of the question to see Powell actively close the door on May, as he closed the door on March at the previous meeting.

A marginal hawkish movement in the dots: Our baseline forecast of the dots sees most of the dots holding steady, with some dots taking cuts off for this year. The data may move back the timing of cuts, but even a June cut would leave plenty of time for three cuts this year. Based on their recent comments, we see Kashkari, Waller, and Harker removing cuts. The “super-dove” (who was arguing for six cuts) probably goes away. This leaves three cuts as our baseline median dot—but just barely (with ten of nineteen members penciling in three or more dots).

Risk to the hawkish side: That being said, the risk is to the hawkish side at this meeting. There isn’t much scope for more dovishness beyond our baseline. Our dovish scenario keeps dots largely the same as December. We would not be surprised to see more of the Board of Governor doves (Cook, Jefferson) move to three cuts or some of the median members (Mester, Powell, Williams) move from three to two cuts. Any one of the latter would shift the median 2024 dot from three to two cuts.

The Developments That Matter:

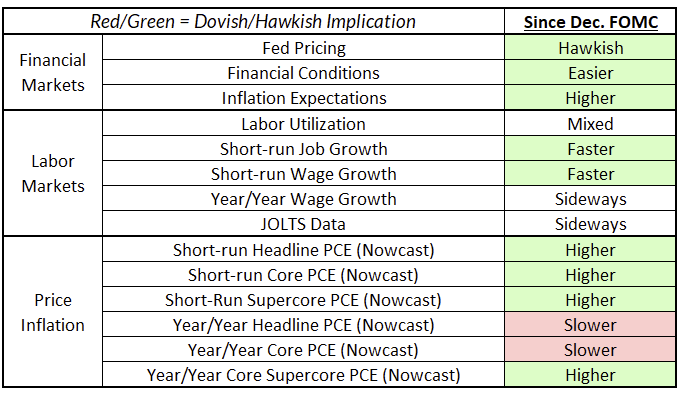

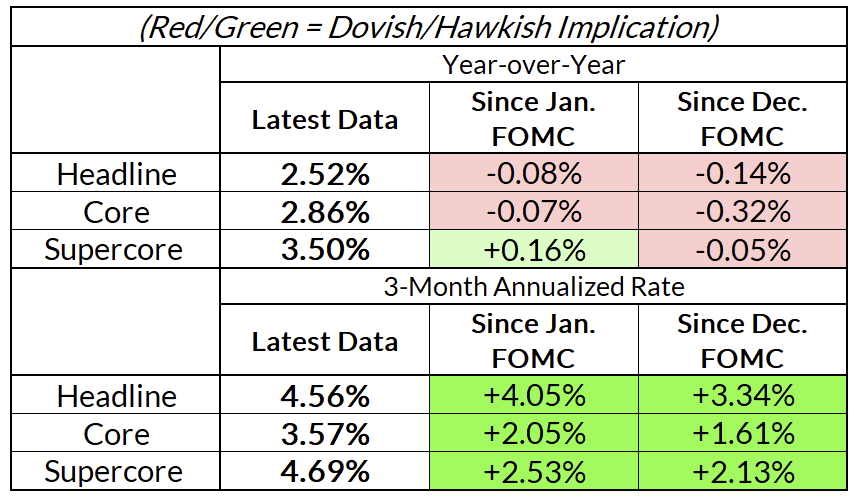

Inflation: January and February were rough months for inflation. Our current corecast is for a 2.86% YoY core PCE print for February. The six-month growth rate of core PCE, which was under 2% in December, should now be over 3% in February. Core services ex-housing inflation will be up on a year-on-year basis versus the previous meeting. Many FOMC members, especially among the moderates in the committee (Daly, Mester, Powell, Waller) have expressed a willingness to look through a hot January potentially plagued by seasonality issues, but two months are probably too much to stomach.

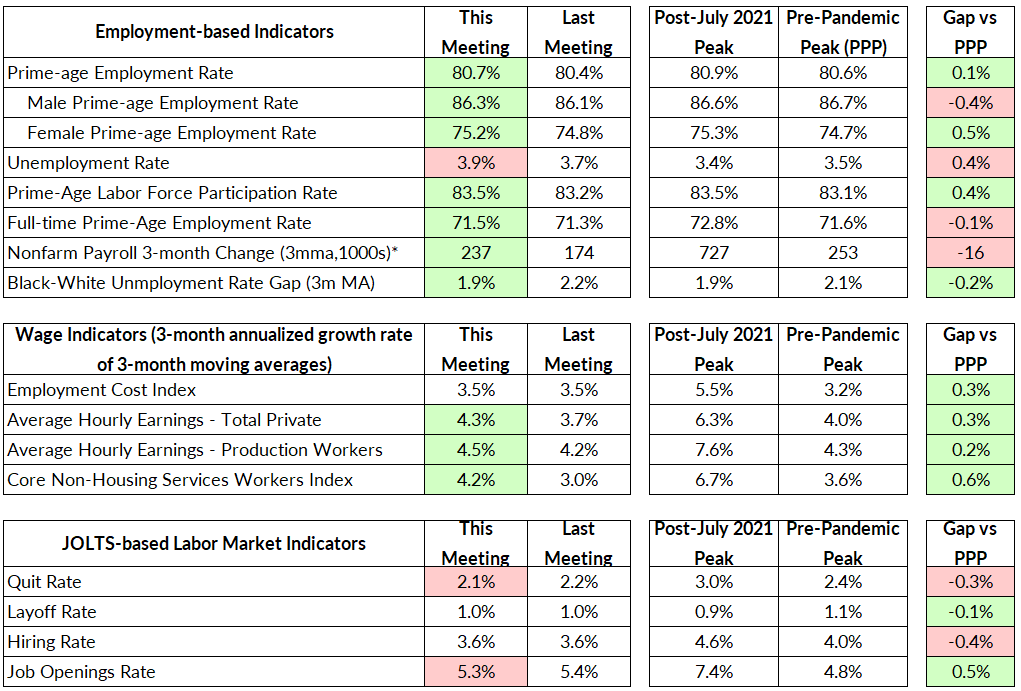

Labor Market Looks OK: Meanwhile, the labor market looks like it is back to the strong/slowing narrative from late-2023 (after a dip in December, which reverted, and an optically hot January, which was partially revised away). This is likely going to give the committee the confidence that they have the luxury of time to wait before beginning normalization.

Fedspeak: Following the January inflation data, the main message from the Committee has been that further patience is going to be needed before rate cuts can begin. The most common refrain is that the Committee is looking for greater confidence that inflation is sustainably on the way back to 2%, and the last few months have certainly not been good for that confidence. This message has been reinforced not just from the centrists and hawks on the committee but the doves at the Board of Governors as well. At the same time, members have been wary of reading too much into January. Most members openly downplayed the notion that hot January inflation was a sign that inflation was reaccelerating, acknowledging the potential for residual seasonality. Whether they will be willing to extend that to February remains to be seen. A few members have started to go beyond the other members in their calls for patience. While the central tendency of the committee seems to favor normalization when they get confidence that inflation is falling, the continued strength in the labor market has Waller and Kashkari opening the door to waiting even beyond that point to start rate cuts.

What We’re Thinking

In our piece on Fed policy in 2024, we endorsed three strategies around rate normalization: front-load cuts (more cuts sooner, then slow the pace), to follow inflation down, and to not pre-prescribe the overall extent of rate cuts. In particular, on the second strategy, we wrote: “Lag if you must, but follow inflation down.” The Fed was always going to lag a Taylor rule prescription, waiting for the disinflationary trend to be clear before beginning to cut. What’s important is that they begin cutting as soon as they have that “bit more” confidence that Powell alluded to in his Humphrey Hawkins testimony.

So far, the core of the committee has communicated that they endorse at least some of our three strategies. Many members have acknowledged that the target federal funds rate should follow inflation down. Daly and Powell have been very explicit in arguing for normalization as a preemptive measure against unemployment risk. Even Bostic, who is considered more of a hawk in 2024, basically endorses this approach (but has a less optimistic inflation outlook than the rest of the committee).

However, we are starting to see some members entertain ideas that would suggest holding rates at their current level even as inflation comes down. Most notable is Kashkari, who recently pondered whether “maybe this constellation is neutral…. So why do anything?” Waller recently gave a speech entitled “What’s the Rush?”, where he cast doubt on the idea that holding rates tighter for longer posed any recessionary risk. These appear to be fringe ideas on the committee, but may pose challenges to Powell if he feels that he needs to get consensus before cutting.

We see Fed restrictiveness in investment, especially residential investment, and gross labor income growth is back to pre-pandemic levels. There may have been an uptick in productivity recently, but this is likely due to supply chain factors rather than a persistent change in technological trends. If Fed officials are worried that the disinflation from supply chains unsnarling is temporary, they should also be worried that the recent strong growth is also temporary. For now, the burden of proof is on those that think the neutral nominal rate is closer to 5% than 2.5%.

How Has The Data Evolved Since Last FOMC?

Latest Corecast:

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.