Rather than careening from disaster to disaster, we might just be having an economy for the time being. The pandemic showed clear deficiencies in capacity and capabilities across a range of sectors, most of which are taking steps to address those deficiencies now.

Each month, we publish a public version of the donor-exclusive Supply Chain Monitor to better inform macroeconomic discussion about developments on the supply side. As this monitor is visually dense, we provide a guide to the structure, intuitions and methods of the Supply Chain Monitor here.

We have redesigned the Supply Chain Monitor in keeping with the end of specifically pandemic-era dynamics. Switching to a view based on 6-month, 2-year and 5-year Cumulative Average Growth Rates makes it easy to see how the sector has evolved over the pandemic era in context of its present state.

We have also added measures of Import Prices to be weighed against the value of nominal imports. In future publications, we will be using the interplay of domestic input prices and production levels with import prices and nominal import levels to tell stories about the evolution of particular sectors during these turbulent times.

Over the pandemic, economic news moved extremely quickly as uncertainty about the future rocketed upwards. Every day, seemingly, something new was breaking down, or suddenly discovered to be insufficient. Yet the modal anecdote across the October ISM Manufacturing and Services surveys alike describes a sense of increasing stability, normalcy and control relative to the previous three years. Rather than careening from disaster to disaster, we might just be having an economy for the time being. The pandemic showed clear deficiencies in capacity and capabilities across a range of sectors, most of which are taking steps to address those deficiencies now. But this is relatively slow and unexciting work.

The Data

Industrial Production Continues To Strengthen: The aggregate index ticked up 0.3% this month to 103.6, with a year-over-year growth rate of just 0.1%. While production did erode over 2022Q4 as the Fed continued to hike interest rates, the aggregate index has now eclipsed its post-pandemic peak. Despite this, there has been considerable sectoral reshuffling under the hood.

PPIs Rebounded Slightly, putting year-over-year growth at -3.3% for “All Commodities” and month-over-month at +0.5% or 6.4% annualized.

Thirty Percent Higher: that’s where Producer Prices have stabilized overall relative to pre-pandemic levels. Earlier in the year, we saw outright deflation month-to-month, but recently input prices have stabilized as recession forecasts have been invalidated and the economy remains strong.

Hard and Soft Data Are Converging On “Steady”: A recurring story this year has been marked weakness in soft data — sentiment indicators, whether for consumers or for firms — vs. strength in hard data. There have been different attempts to explain the divergence, but one thing we are seeing as the year progresses is sentiment converging upwards from pessimistic towards steady while the hard data converges downwards from “hot” to “steady”. New Orders are improving, while Employment and Production are both up. Order books are beginning to recover as more participants have more clarity about peak interest rates over the Fed’s hiking cycle. It feels reasonable to explain this as the dissipation of uncertainty about the near-term path of the economy on the part of both firms and households. The pandemic is decisively over, and supply chains are steadily healing, leading to more confidence in prices, lead time, and thus business performance. As the ISM Manufacturing report notes: “production execution [has] improved”.

The Data In Context

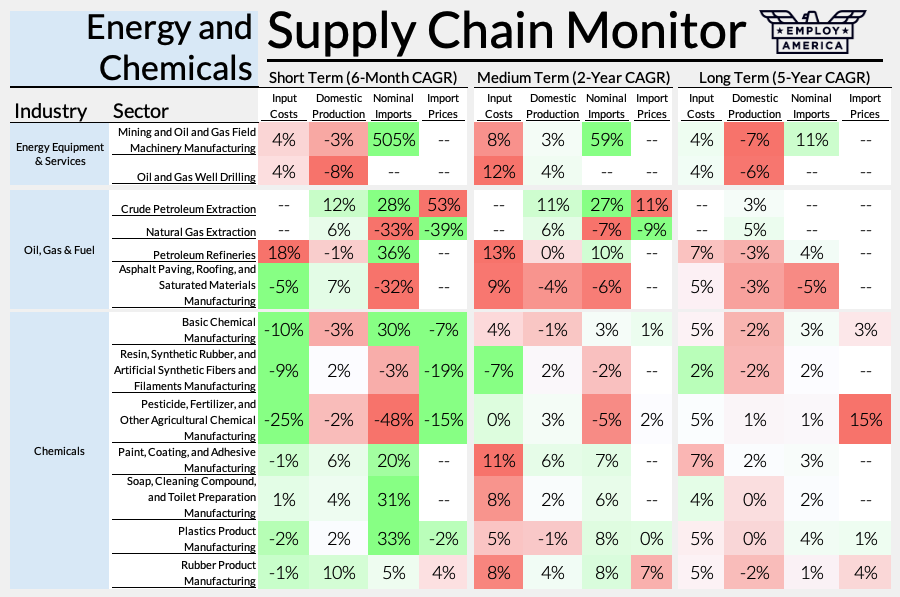

Energy and Chemicals

Chemicals Turning It Around: With this month’s report, we begin to see a turnaround in domestic chemicals production alongside falling domestic and international prices. Chemical manufacturing can be a remarkably circular sector, so falling producer prices may just as easily represent falling firm-side revenues in places.

Refineries Feeling Higher Crude Prices: Although spot oil prices have fallen in the last couple weeks, this dynamic can take time to feed through to lower prices for refineries that negotiate medium-duration contracts for feedstock. It will be interesting to see how the Biden Administration’s interim easing of oil sanctions on Venezuela will impact the cost structures of US refineries geared for the kind of heavy crude they export.

O&G Growing Strong Past Pre-Pandemic Peak: Despite big moves upwards in input costs over the past few years, oil and gas production is still growing strong after passing its pre-pandemic levels and reaching record highs.

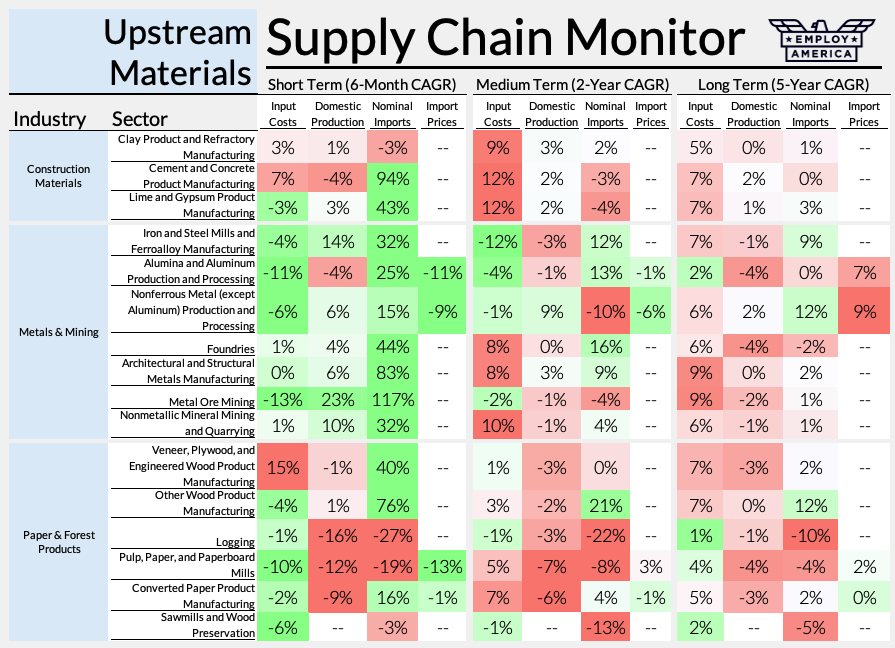

Upstream Materials

Metals Inflation Coming Off The Boil: Energy is a key input to these processes, but domestic capacity limitations following a destructive years-long price competition with Chinese producers are likely playing a significant role.

All Hands On Deck in Metals: Across the board, we are seeing fast-growing imports and slower-growing production of metals and metal products. Despite this, domestic input costs are falling as the price of energy falls.

Wood Products Still Suppressed: Despite some nascent turnarounds in the underlying production data, the wood products industry is facing an uphill climb that will only get steeper as housing construction cools.

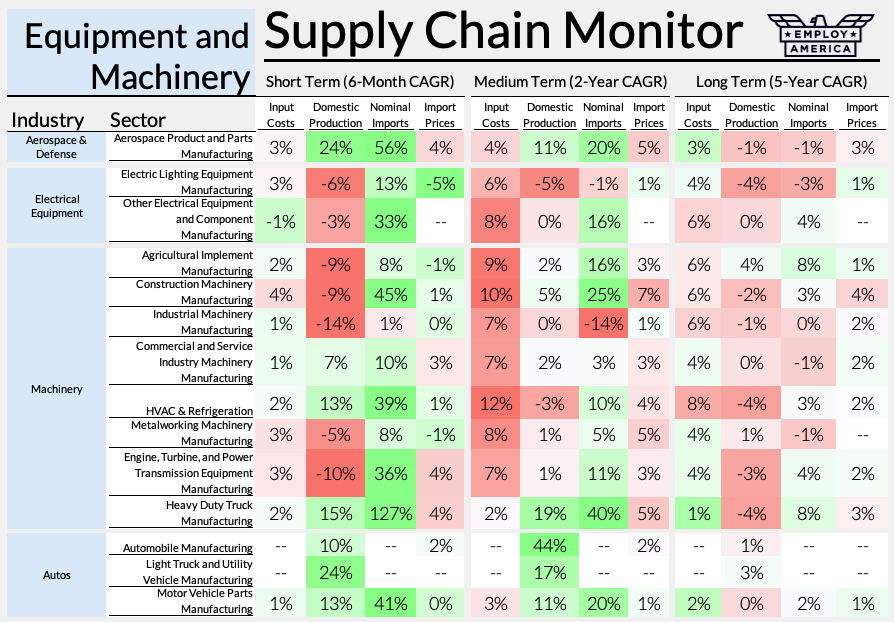

Equipment and Machinery

Domestic Machinery Input Inflation Easing: Despite significant input cost pressures over the past two years, cost inflation in these categories has slowed in recent months.

Import Prices Easing Even Faster: Despite the recent easing in prices, we are still seeing substitution between falling domestic production and rising nominal import volumes across a range of machinery sectors. The differences in long-term CAGR between import prices and input costs are substantial.

Electrical Equipment Shortages Hit Three Year Mark: While the semiconductor shortage has grabbed headlines and disrupted production of a wide range of goods, the shortage of electrical equipment has actually been going on longer. In fact, the shortage of electrical equipment has the potential to become the next major bottleneck for decarbonization — now that the IRA is providing much more generous subsidies for the development of renewable energy projects. The Department of Energy, among others, have noted the makings of a possible transformer shortage as well. Per ISM Services, transformers have been in shortage for over a year at this point. A transformer shortage threatens to limit the ability to expand the electrical grid in ways necessary to achieve the scale of decarbonization and electrification necessary for the climate transition. Lead times for new transformers are so blown out that “it could take 52 to 56 weeks to get new transformers instead of the typical 4-week turnaround from manufacturers” according to one electric cooperative CEO quoted in the article above. This shortage is due in part to limitations on the capacity to produce the grain-oriented electrical steel historically used to build these new transformers’ cores. In response, the Department of Energy is looking to encourage the implementation of transformers with cores made from amorphous steel for efficiency reasons, but the existing market and capacity for the production of that particular alloy is quite small. In fact, steel has been flipping into and out of reported shortage all year, while electrical transmission equipment has only been reported in shortage over the past two months. And yet, despite all this, Electrical Equipment is one of only two manufacturing industries reporting higher inventories in September. Hopefully those inventories start to make it to their customers.

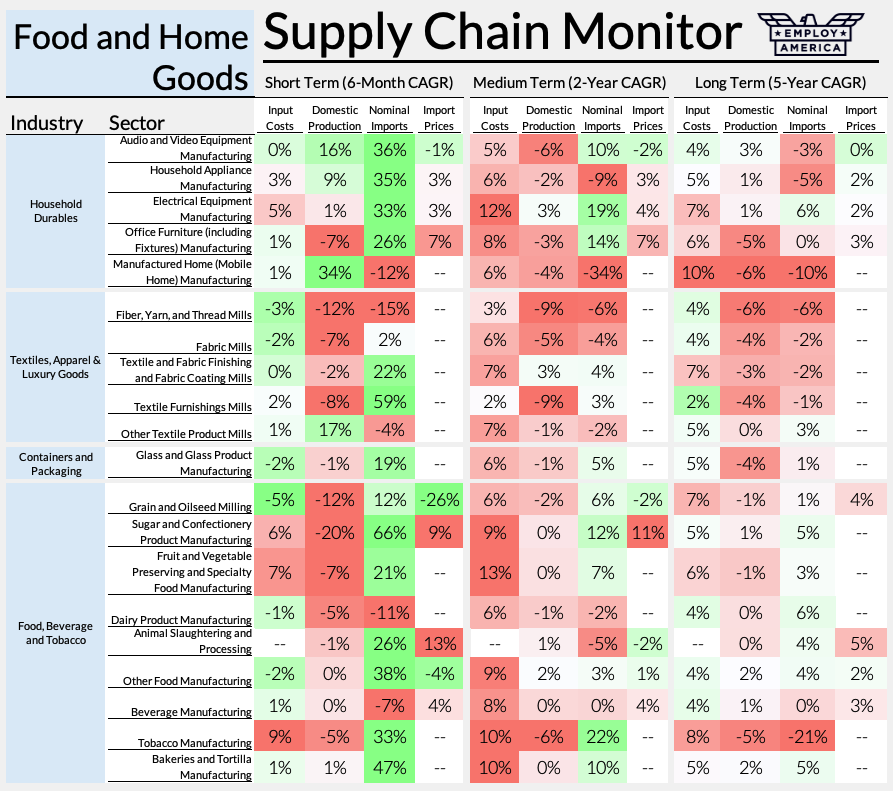

Food and Home Goods

Food Cost Inflation Still Firm: Ongoing world events continue to create significant disruptions in global food markets, leading to rising input costs for food products. US harvests have proven difficult to forecast, as a changing climate led to a nontraditional summer – hotter and drier – and early fall.

Food Trading Imports For Domestics: This Industrial Production report saw dips in the production of a range of foods, while imports in those categories have been rising. One exception though, is Dairy Products, where production and importation are both down.

Mobile Homes Staging A Comeback: One of the stranger consequences of the pandemic has been extreme weakness in the production of mobile homes. Yet, in this most recent release, short-term production is finally growing.

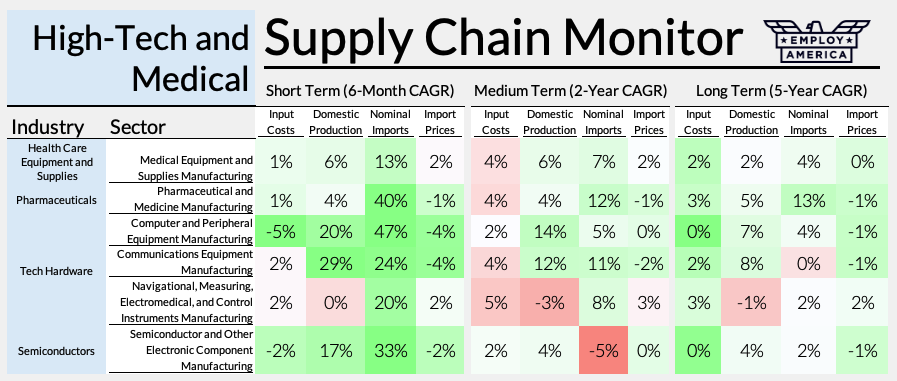

High-Tech and Medical

Supply Chains Easing: As supply chains have sorted themselves out, high tech and medical production has rocketed forward in recent months, even as imports continue to increase and tighter monetary policy binds.

Little Pandemic Cost Pressure: Despite shortages in nearly every category here over the pandemic, few of those shortages have cashed out into higher input costs.

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.