Overall, the Q1 GDP print looks weaker overall than the previous print, with investment growth correspondingly weaker. Nominal GDP grew at 5.5% year over year, and 1.2% quarter over quarter, while inflation-adjusted GDP grew at 3% year over year and 0.4% quarter over quarter. Nominal private fixed investment grew at 5.5% year over year and 1.6% quarter over quarter, while inflation-adjusted private fixed investment grew at 4.2% year over year and 1.3% quarter over quarter.

Despite this weakness, investment is still rising. Rather than flipping into negative, the weakness of this print is the slowing rate of growth across a wide range of sectors. This is a signal of a slowdown, but not yet a recession signal.

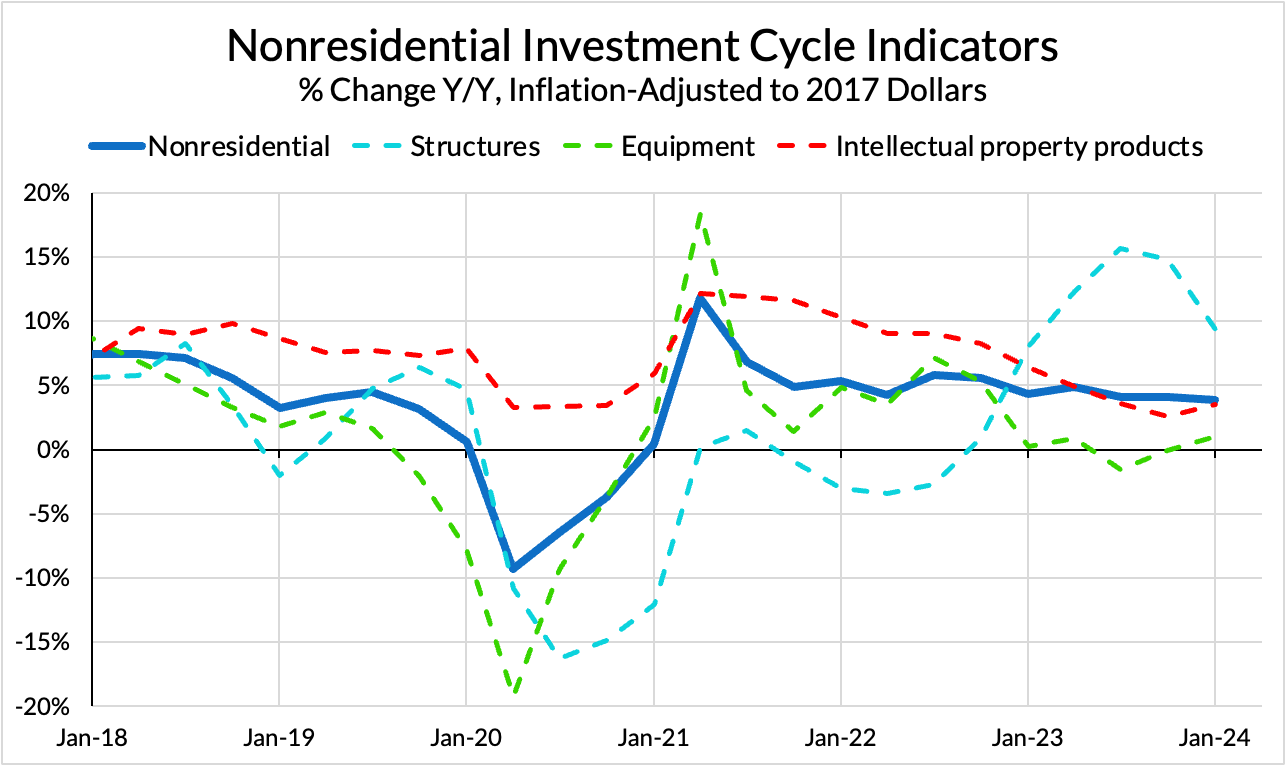

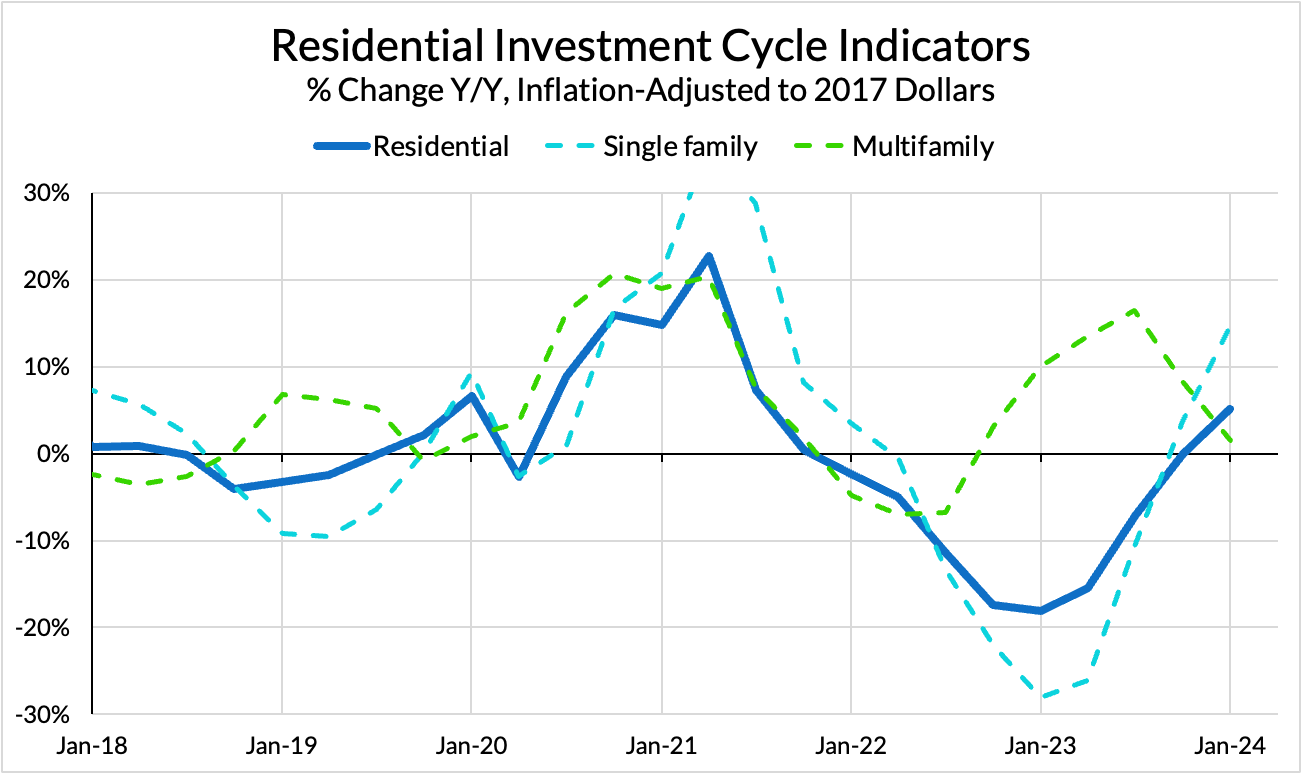

Equipment investment growth is falling more so than residential investment growth. Speaks to firms starting to worry about investment in an environment of sustained elevated interest rates. Residential investment is rising year over year after a substantial falling cycle – however base rate effects mean that even though it is rising now, it is still lower than in recent years.

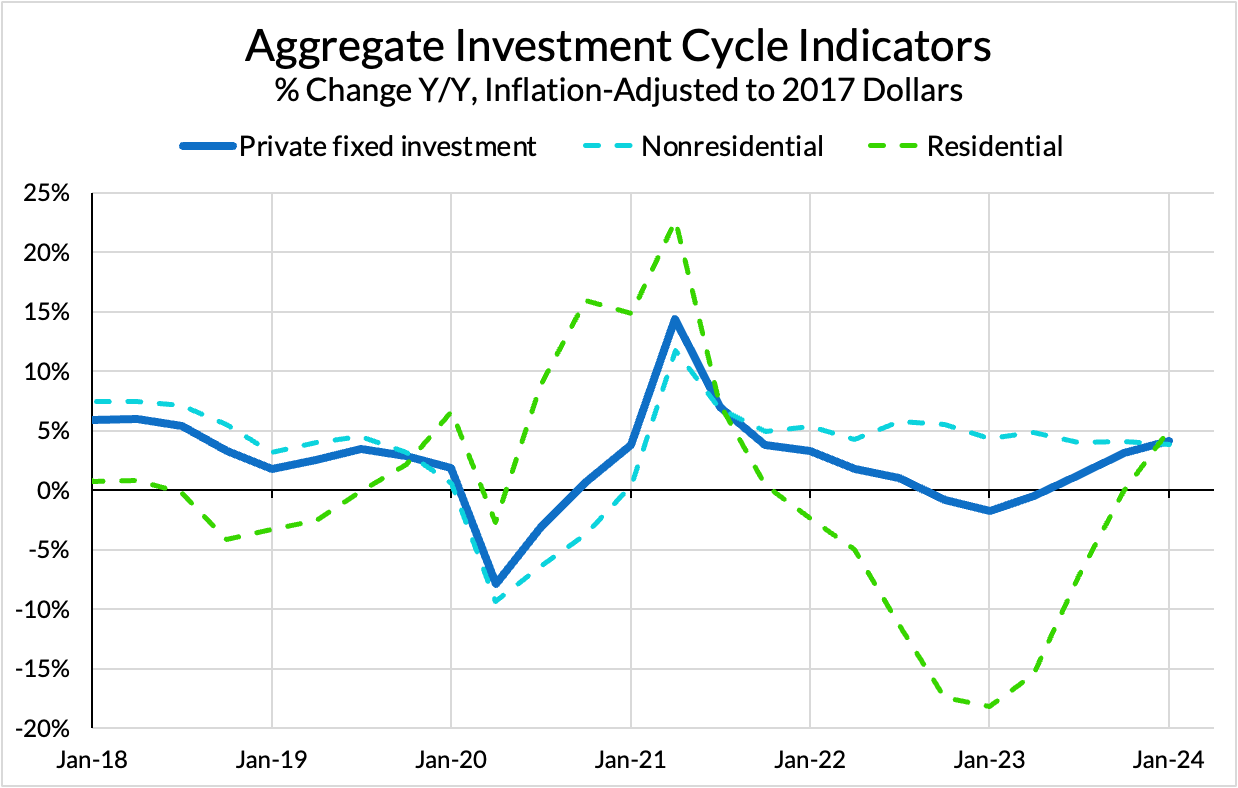

In the aggregate, all these changes more or less balance out. Some sectors rising and some sectors falling is actually what we are told a healthy macroeconomy should be like; tight labor markets and continued spending growth have underwritten continued investment.

This suggests that we are seeing something like a rotation in investment – no single sector is driving a boom or crashing in an outsized way, so some sectors falling and others rising is doing a good job of keeping the aggregate in a good place. This is different from past cycles, where changes in headline investment were often driven by dramatic changes in one of a few underlying sectors. When those sectors hit snags or went bust, aggregate investment went with them – telecoms in the late 90s, the dot-com bust in the early 00s, residential investment in the late 00s. We aren’t seeing a setup for that right now – growth is slowing but still broad-based in investment alongside public funding support for investment in less exciting but necessary infrastructure.

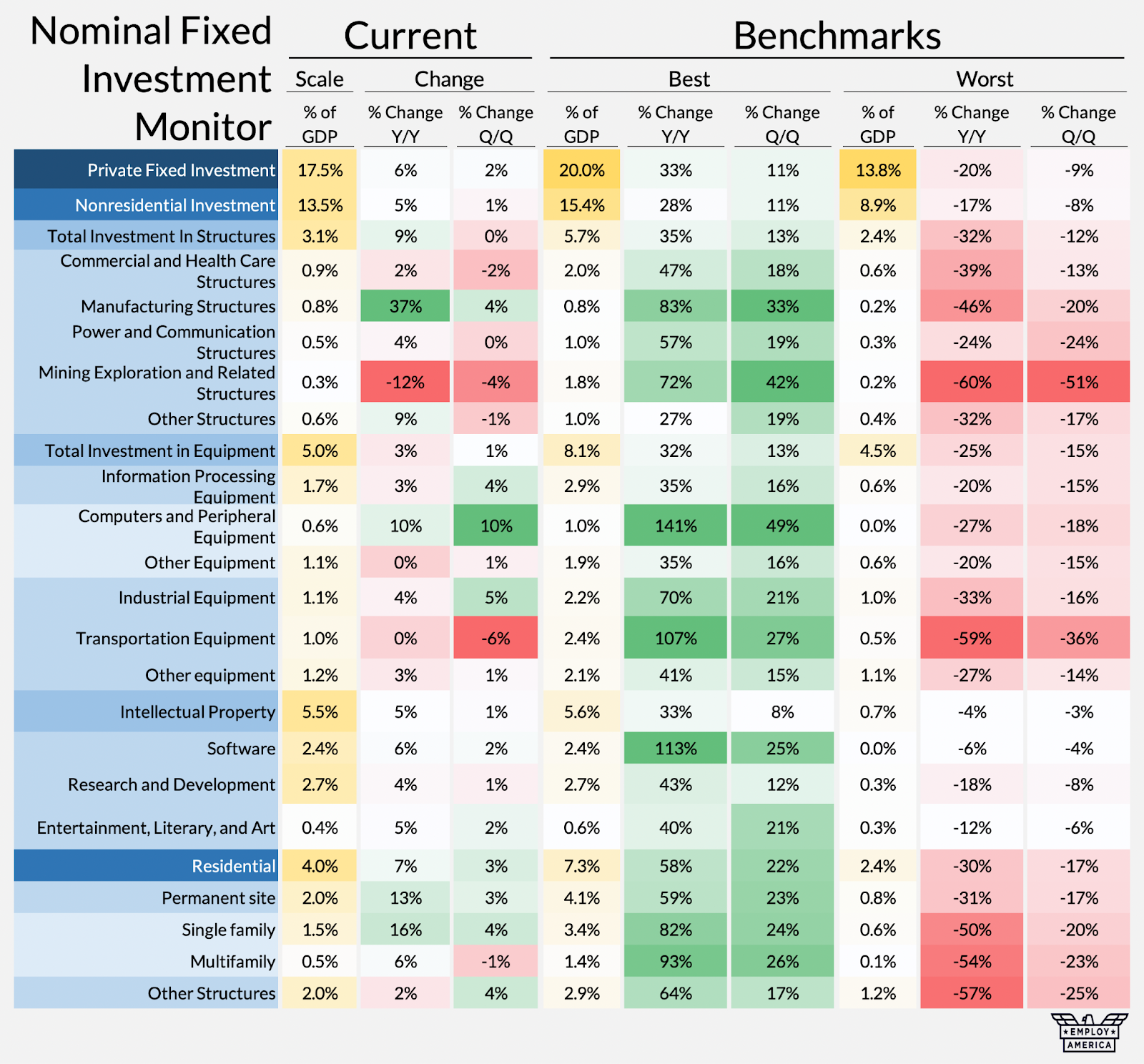

The takeaway? We are seeing strength in some sectors receiving fiscal support, and weakness in some interest-rate sensitive sectors. We are seeing that manufacturing structures investment has hit something of a plateau, albeit at a substantially elevated level. This tracks with recent mentions in ISM surveys of Fed interest rate policy as a potential catalyst for a weakening supply side.

Nominal Cycle Indicators

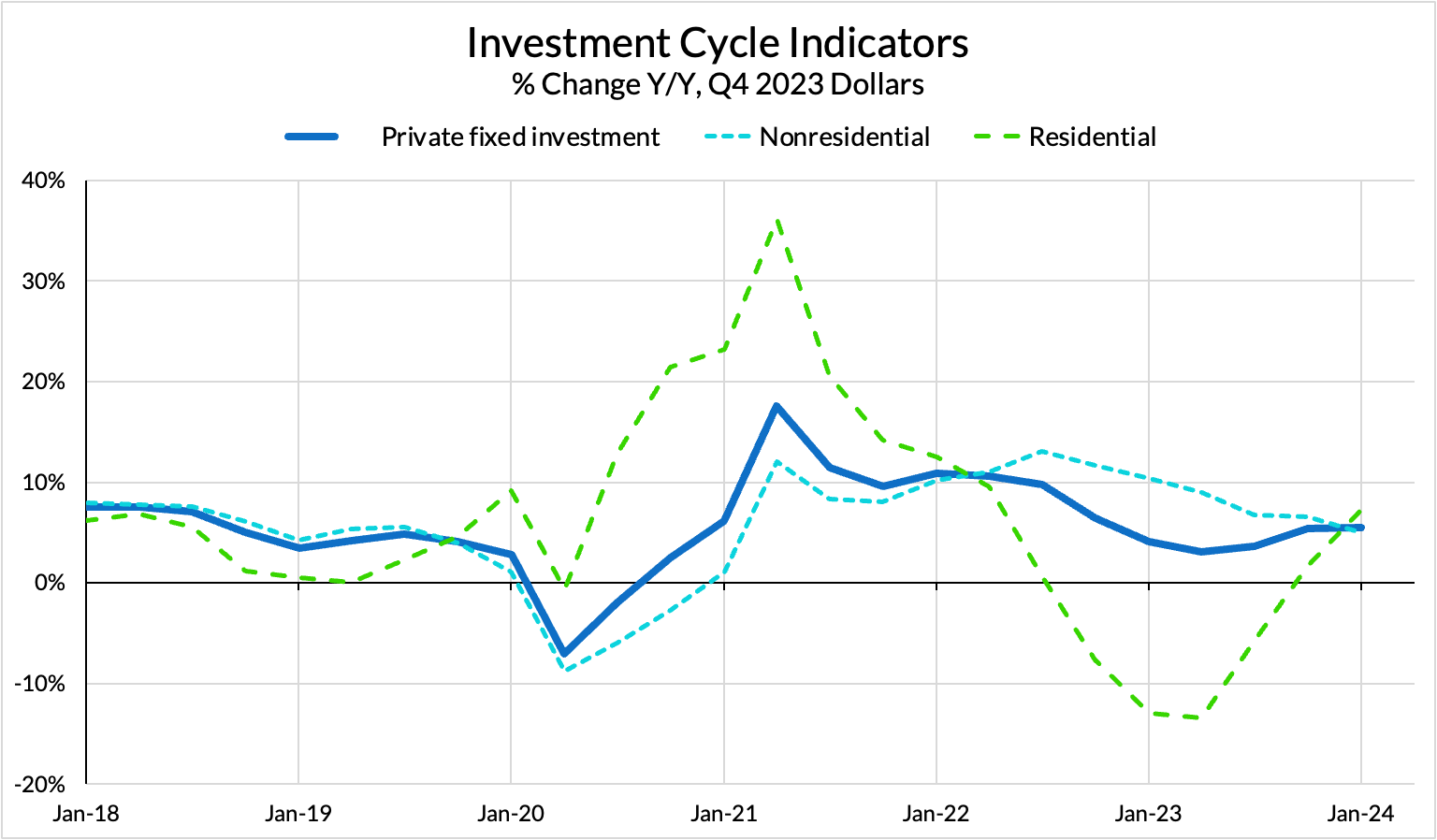

Overall, nominal investment is continuing to grow, which is a tailwind for the economy as a whole. Despite a slowdown in Nonresidential investment, year-over-year growth in Residential investment is keeping aggregate investment growth steady near pre-pandemic levels despite the radically different interest rate environment.

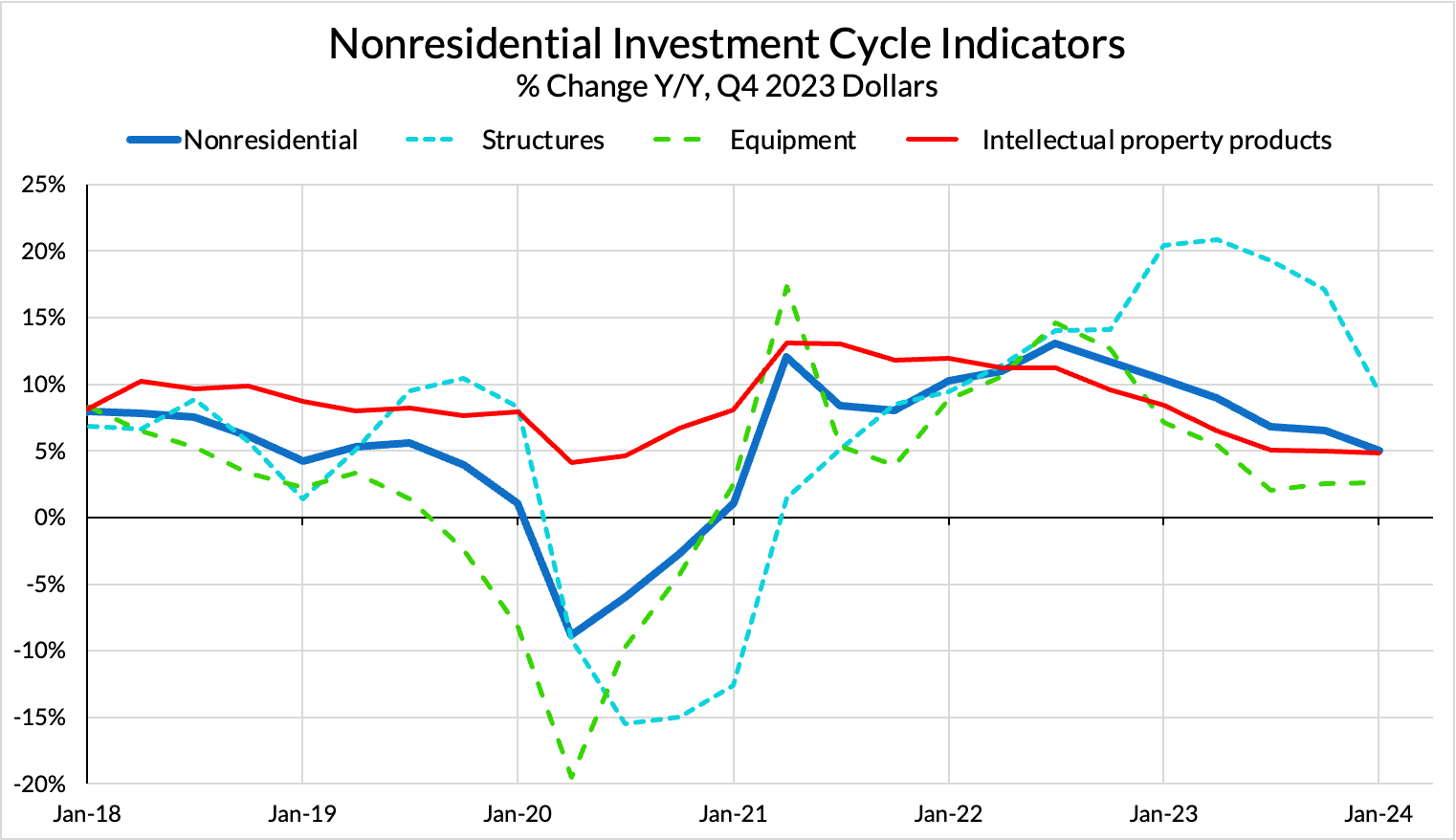

Within nominal Nonresidential investment, we see the growth slowdown is led by a significant fall in the growth rate of Structures investment. This is disappointing, as growth in Equipment and Intellectual Property investment continues to slide down year over year. Businesses may be slowing capex spend in line with higher interest rates.

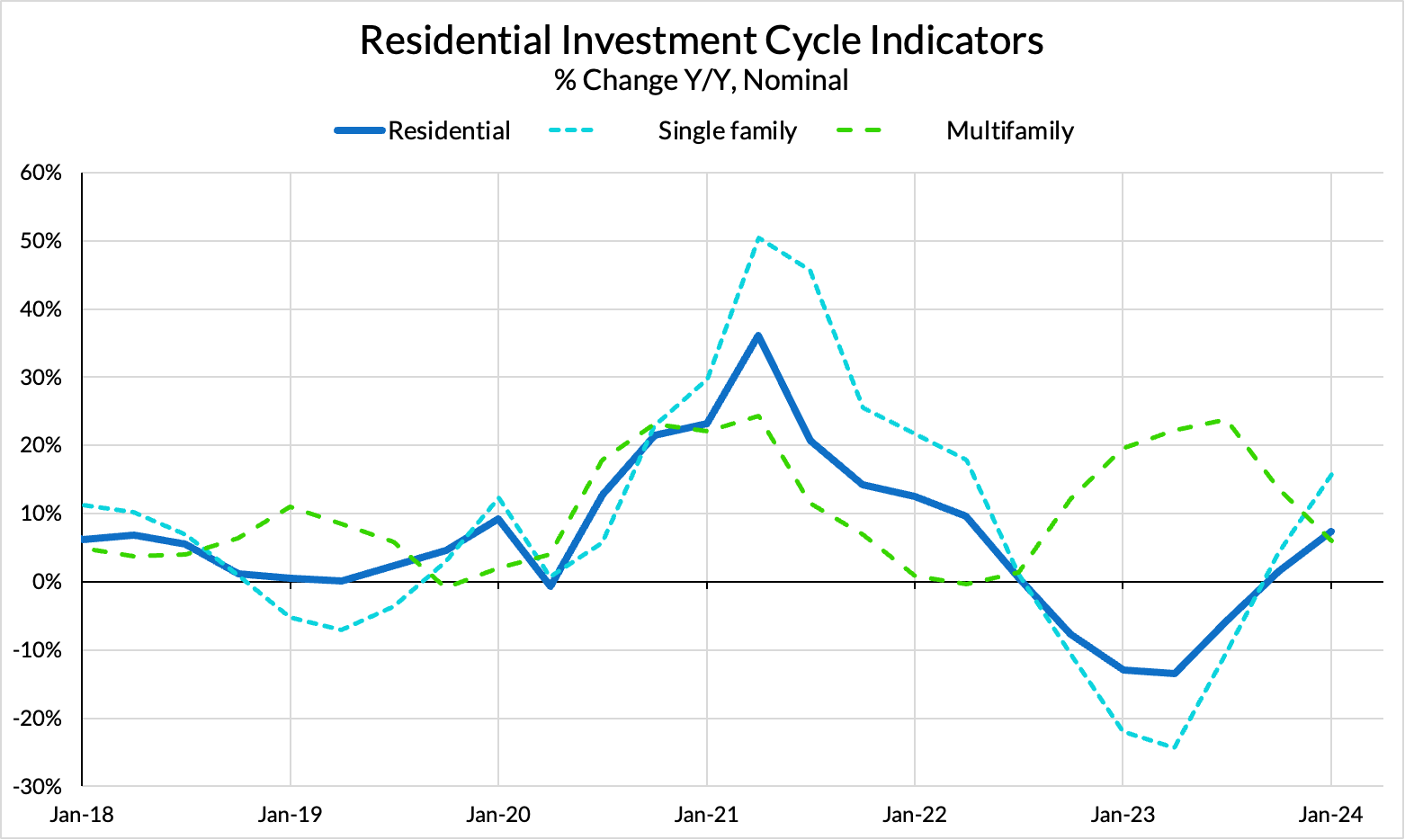

Growth in Residential investment has returned, but only after a long correction. Multifamily Residential Investment growth slowed substantially as many have raised warnings about the impact of interest rates on the pipeline of new projects, especially as indicated by the fall in multifamily housing starts.

Inflation-Adjusted Cycle Indicators

The inflation-adjusted investment picture looks somewhat weaker than the nominal, but is accelerating on rising Residential investment and waning measured inflation.

We see the same basic pattern in inflation-adjusted Nonresidential investment as in nominal, with the caveat that Equipment investment growth has been negative more recently in inflation-adjusted terms than nominal. Despite the falls in the relevant price indices, we see a comparable fall in the growth rate of structures investment.

Inflation-adjusted Single-Family Residential investment looks better than nominal, but Multifamily looks worse.

Fixed Investment Heatmaps

Despite the slowdown this quarter as manufacturing construction spending reaches a plateau, the strongest year over year growth remains in Manufacturing Structures. As a share of GDP, this category is at all time highs. Nominal intellectual property investment is also near all-time highs as a share of GDP. Most other categories are about midway between their largest and smallest all time shares of GDP, providing some confirmation to the interpretation that no single sector is driving continued growth in an outsized manner.

We see the strongest quarter-over-quarter growth in Computers and Peripheral Equipment, likely a consequence of decisions by a range of companies to capitalize on the possibility of large language models by investing heavily in a range of new tech hardware.

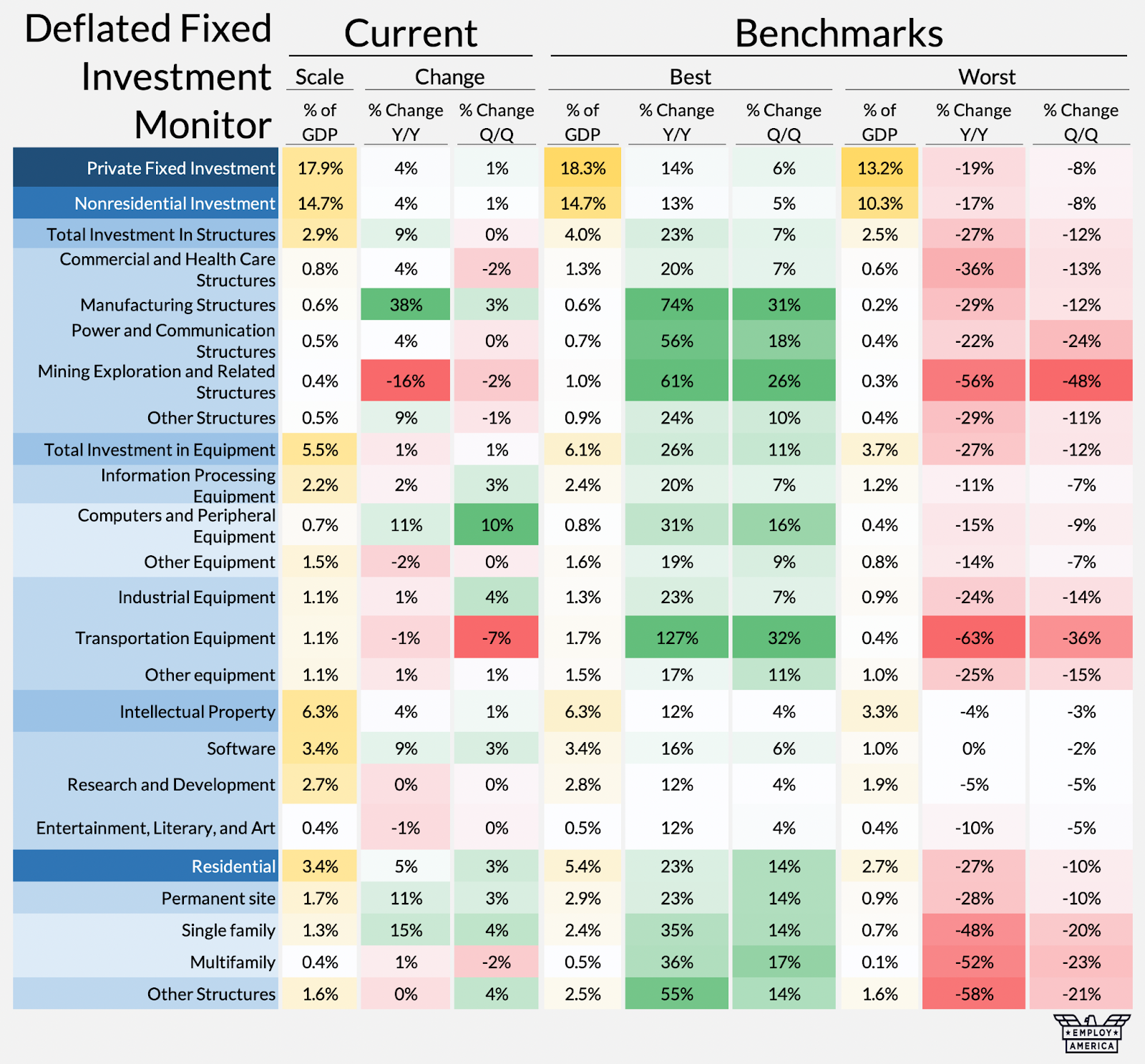

The picture looks much the same after adjusting GDP and Fixed Investment for inflation. Interestingly, inflation-adjusted Intellectual Property investment is at an all-time high as a share of GDP. In fact, almost every sub-component of Intellectual Property investment is at or near its all-time high as a share of GDP. The relative growth picture looks largely the same after adjusting for inflation, with Manufacturing Structures and Computers and Peripheral Equipment leading.