This is the third piece in the Contingent Supply series, which looks at the operational requirements, financial needs, and economic opportunities involved in using the SPR to stabilize oil markets. Our earlier pieces assessed the SPR in our current moment and examined whether the SPR has the ability to meaningfully impact crude oil prices. This piece describes how the DOE can structure a facility to most effectively maximize domestic oil production, ideally with the sale of put options to provide producers the most upside potential and risk mitigation.

Introduction

The Biden Administration has signaled an intent to structure Strategic Petroleum Reserve (SPR) replenishment in order to provide the insurance and stability necessary to stabilize oil prices and investment. In our preferred strategy, the Department of Energy (DOE) would sell put options directly to producers through a facility designed to incentivize net additional domestic production. By providing producers with the option to sell at a given strike price, the sale of put options would be a powerful form of price insurance for producers. That insurance would give them the certainty necessary to justify increased investment amidst an uncertain economic outlook and historically high oil price volatility. Rather than refilling the reserve in an ad-hoc, arbitrary manner, our proposed put options facility would align SPR acquisition with the state of the crude oil market while increasing our energy security.

To be clear, this strategy should not be the sole method of acquisition. It should be one critical tool amongst several to meet the objectives and procedural requirements of the SPR’s governing statute, specifically to minimize “the impact of… acquisition upon supply levels” and maximize domestic oil production, thereby reducing “vulnerability to a severe energy supply disruption.”

As this would be a new undertaking, reasonable questions have emerged. Is this a risky “financialization” of the Federal Government’s authority? Does DOE have the staff expertise necessary to implement this facility? Further questions arise about design and logistics: On what basis would producers bid? How would bids be evaluated? How should the options be structured? What happens if the SPR is overwhelmed with delivery requests?

Given the pressing need to develop a long-term acquisition strategy, it is our intent to answer these questions. In today’s installment, we will lay out the design of our proposed put-writing facility while grounding these choices in the statutory language which governs the SPR. Our subsequent piece in our “Contingent Supply” series will tackle the logistical challenges emanating from our proposal.

The Plan

Our goal is to design a facility that can effectively achieve the objectives and requirements of the SPR’s governing statute (and regulations while adapting to changes in oil markets and financial markets. Outside the Federal Reserve and the Department of Treasury, agencies do not typically interface with modern financial markets. Nonetheless, the policy goals we seek can largely be achieved within the SPR’s existing competitive bidding process.

As it stands, the DOE uses a competitive bidding process when acquiring crude for the SPR. Following a market analysis (required by 10 CFR 626.4), the DOE announces a solicitation, receives bids from interested producers (or intermediaries), and rewards bids on a price-competitive basis.

Our proposed facility would replicate the major steps of the existing competitive bidding procedure. The first step is conducting a market analysis to reduce the negative effects that could arise from market participation. As this process is ongoing, the decision to sell put options could arise from several factors including low SPR inventory, low private inventories, high or volatile prices, an uncertain production outlook domestically and internationally, or the existence or potential of ongoing supply disruptions. In addition to conclusively determining the need for the use of a put options facility, the DOE could obtain information through the market analysis that is necessary for implementation of the facility. This would include an analysis of bottlenecks to market investments, a breakeven analysis for the industry, analysis of specific methods of production in specific regions, and the availability and affordability of price insurance in financial markets. Given that DOE is already required to assess relatively technical factors like “market volatility” and “futures market differentials” – assessing our proposed factors should be well within the expertise of DOE staff.

The next step after the market analysis is an initial solicitation, where – as required by 10 CFR 626.5 – the SPR would announce its intent to acquire petroleum through the sale of put options, along with the requisite information about the bidding process. The process would then slightly diverge from existing procedures. Rather than a single process of bids and rewards, our facility would employ a two-stage Dutch auction process, breaking a single competitive bidding process into two competitive bidding processes. In the first, following solicitation, companies would submit “Initial Bids for Participation,” including the volume of put options sought and any other information necessary to select participants for the auction. The DOE would competitively “award” companies by selecting them for participation in the auction process. In the final stage of the auction process, DOE would award put option contracts to producers. Following completion, the only operational challenges should be fundamentally logistical and not financial.

Stage 1: Solicitation and Initial Bids

Once the need for a put facility has been demonstrated, the SPR would begin the process of acquisition by submitting an initial public notice of the SPR’s intent to acquire petroleum through the sale of put options, as required by 10 CFR 626.5. The solicitation should be similar to previous solicitation notices and could include an announcement for all auctions in a given acquisition cycle.

The solicitation notice would specify the period over which options could be exercised, strike prices at which options would be offered, the price and quantity of puts, and the strike prices at which they would be offered. For example, if the ultimate acquisition goal was as many as 240 million barrels of oil within a 12 month time horizon–the solicitation may aim to conduct auctions at a monthly frequency, with five auctions in a given month (corresponding to five different strike prices, e.g. $80, $70, $60, $50, and $40), ideally benchmarked to domestic industry breakeven costs. This would amount to 4 million barrels of put options available at each strike price, and 20 million barrels of put options available each month. The precise spacing of strike prices should be determined by balancing the logistical costs associated with managing SPR delivery against the information and price discovery benefits (the options surface).

The initial solicitation notice would also be an ideal place to locate any environmental requirements that the DOE may wish to impose as a condition of purchasing puts from the SPR. The best interpretation of 42 U.S.C. § 6240(b)(5) implies a broad construction of the competition objective, encompassing considerations beyond price and quantity. Given the growing trend towards certifying production within the US industry to achieve environmental goals, the decision to screen and appropriately reward bids that support this form of ‘environmental competition’ would be strongly justified on policy grounds and under existing statutory authority. Justified policy priorities of DOE have been reflected in the solicitation notice, for example, limiting an acquisition to producers with 5,000 employees or fewer.

Finally, but most importantly, for evaluating which bids would be selected for the final stage of the auction, producers would be required to submit a proposal demonstrating how the put option would translate into production of additional (uninsured) barrels. Their proposal would include the number of barrels of put options sought (at various strike prices if they wanted to participate in multiple auctions), and the quantity of barrels from the marginal well-pad that would be brought online as a result of the put options sought. Other conditions for participation could include submission of existing (pre-notice) capital plans and eligibility requirements – such as requiring a demonstration that “initial bid” is credible in the context of their submitted existing capital plans and the company’s untapped production potential, with a certification of accuracy and subject to independent review from an auditor or other independent third-party entity. The solicitation would also include information on transferability limitations (e.g. the rights of first refusal). With these requirements set in the solicitation, producers would then have a reasonable period of time to submit their initial bids.

Stage 2: Evaluation of Initial Bids and Auction Selection

Next, the SPR would evaluate the submissions in the manner necessary to target the sale of put options to producers whose purchase will most increase oil production. These plans must pass tests for credibility, both by an independent third-party entity and by staff at the DOE, and be subject to a good faith or reasonable efforts standard.

Among the credible bids, producers would qualify for the final stage of the auction process based either on (1) a sufficiently superior count of additional uninsured barrels associated with their put option bid (ie--the number of marginal barrels added from the put purchase), or (2) the ratio of uninsured barrels to put options sought (insured barrels). These two ranking schemes offer complementary approaches for maximizing production gains from both smaller and larger producers. The cutoffs for these two ranking schemes should be set transparently. Cutoffs should be rationally based on ensuring that there are a sufficient number of unique participants and a sufficient number of bids (in excess of the put options offered) to ensure a competitive and efficient auction process. Here, it would be necessary for DOE to consult with external experts in auction design to determine how to set the right cutoff.

While the evaluation of these two metrics would be a new practice for the DOE, the metrics are no less objective and quantified than the prices with which the DOE is used to reviewing bids. No special expertise would be required to distinguish between bids. Evaluation of the credibility of the bids would be a new undertaking, but supplemented by the requirements outlined in the initial solicitation. For example, many producers would be able to verify their pre-existing capital plans through third parties. Public companies and private companies alike share their capital plans with a host of external parties including investors and banks. Relying on legally enforceable certification would provide considerable confidence to DOE that companies would be highly disincentivized to submit fraudulent documentation or plans. Staff at DOE (or external auditors contracted by the DOE) could evaluate the credibility of bids based on alignment with previous capital expansions and the credibility that existing assets have untapped potential.

Stage 3: Dutch Auction Based On Option Premium Bids

Finally, the SPR runs a Dutch auction to determine the price at which the available options will be sold, and to which firms. In a Dutch auction, all bids are submitted at once. The full offering is then sold at the highest price at which there is a buyer for every contract issued. Running the auction this way ensures the maximal benefit to the SPR as a buyer, while ensuring the process is not a simple giveaway to oil companies. To ensure sufficient participation, the option premium could be subject to a capped upside price for the option premium. As conditions evolve and greater comfort with the process is achieved, the cap could be raised for subsequent auctions–an additional benefit to spreading auctions over a longer period of time.

The final outcome of the auction would be determined on the basis of the option premium price, with tiebreakers going to the producers capable of contributing to the largest number of uninsured barrels that would ultimately be brought to market.

Now, this has all been fairly abstract, so let’s work through a quick example of how this facility would look in action.

Example

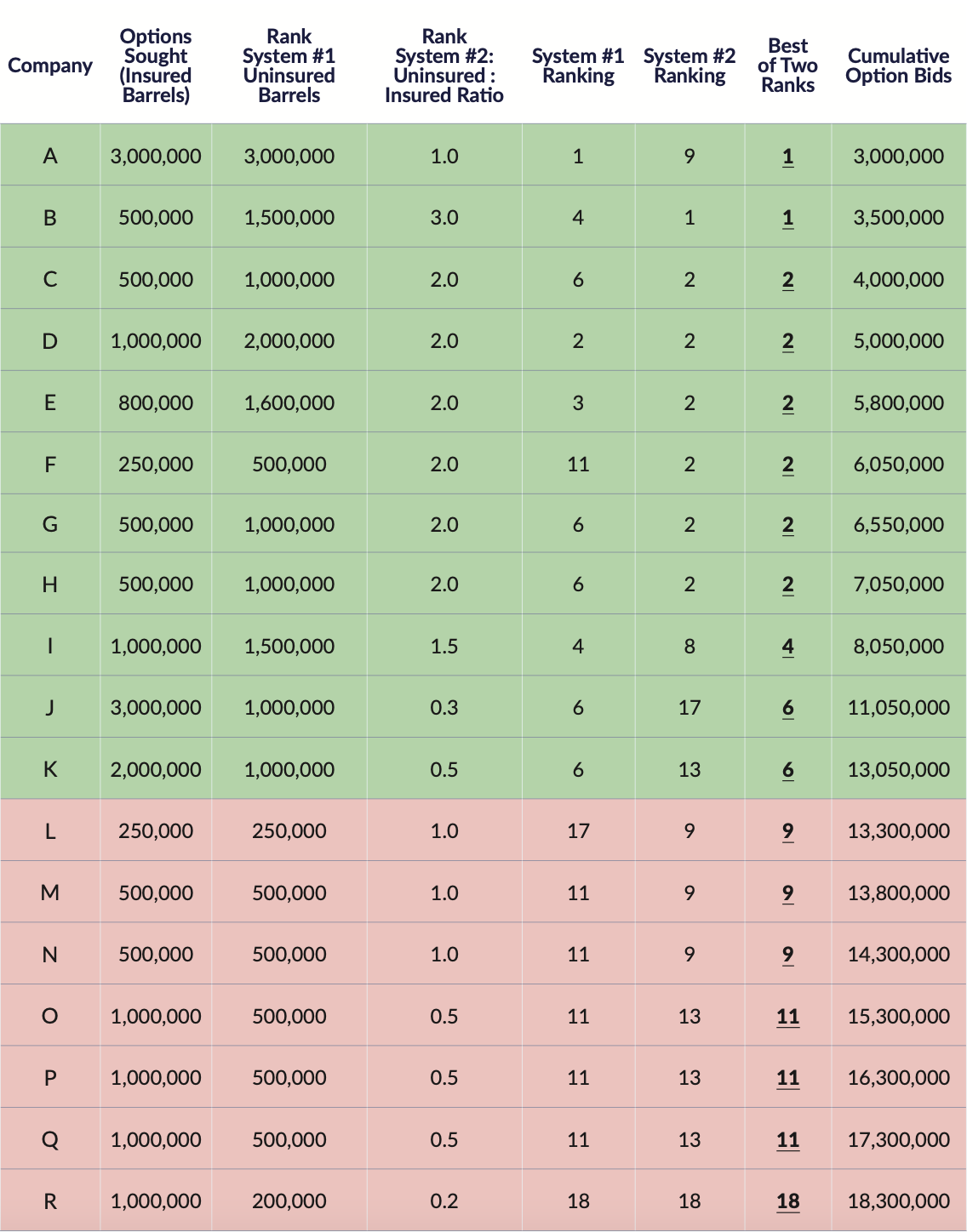

Let’s start with an auction for 5 million barrels worth of puts at a strike price of $65, with 18 different companies bidding. After the initial round of solicitations, we have the following set of bids.

The first step for the DOE is to make sure that it accepts enough first round solicitations to make sure that there will be competitive bids for all of the offered option contracts in the final auction. Given this set of initial bids, the stage 3 Dutch auction would require at least 12 unique bids for at least 10 million cumulative barrels of SPR storage. In this case, the top 12 bids (green) advance to a final-stage Dutch auction.

Using the best ranking between Ranking Systems #1 and #2 (the first ranks by the number of uninsured barrels attached to the initial bid, the second ranks by the ratio of uninsured to insured barrels), Companies A through K are among the top 12 and account for a little more than 13 million barrels of put option bids. From here, qualified participants submit their bids for the price on the option premium.

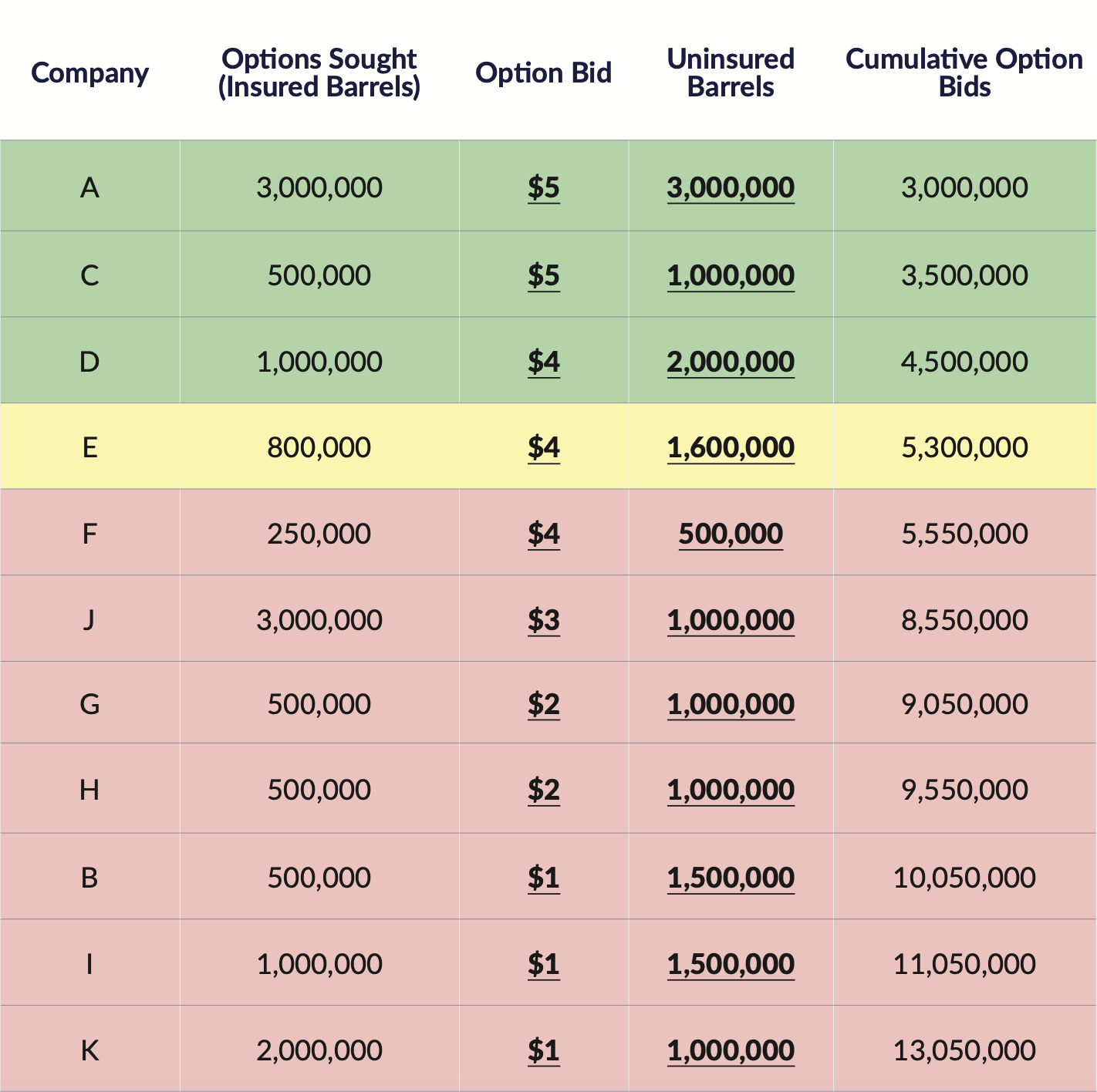

A $4 option premium clears the entire allotment of put options offered in this auction. Despite bidding $5 per barrel of put options, Companies A and C will only pay $4. When there is a tie – as between companies D, E and F in our example – where issuing the total volume of put options demanded would exceed the allotment, the number of uninsured barrels attached to each bid becomes pivotal. Company D would win the full 1 million barrels of put options it bid, since awarding those would still leave another 500 thousand barrels to allocate. Since 500 thousand barrels is still lower than the number of put options Company E bid, Company E would only receive 500 thousand barrels of put options. Company F scores the poorest in terms of uninsured barrels and would not win any of the options offered in the auction since Company E already received only a partial remainder of its bid.

This facility does not need to be complex, but it does need to be transparent. Clear communications about how the SPR operates in the context of the fossil fuel industry will be politically indispensable. Equally important is the precedent this arrangement sets for the structure and possible uses of other possible Strategic Reserves in the future, especially as we plan for the resource-intensive climate transition.

Conclusion

As the Biden Administration considers actions to lower oil prices (particularly in wake of the recent OPEC+ production cut), it can and should make every effort to boost domestic oil production. If the recently proposed rule is finalized, the DOE has an opportunity to create and design an acquisition facility at the SPR to do just that. Offering producers the chance to purchase put options from the DOE would provide producers the necessary price insurance to justify new investment, and could be designed to reward those producers who can bring the maximum number of new barrels online, all with only slight changes to the DOE’s existing competitive bidding procedures. It would be a worthwhile undertaking.