This is the second piece in our Contingent Supply series, which looks at the operational requirements, financial needs, and economic opportunities involved in using the SPR to stabilize oil markets. We argue that despite common misconceptions, the SPR is more equipped than any time in its history to stabilize the price of oil. The potential production impact of a well-calibrated SPR refill program could be comparable to the scale at which OPEC attempts to influence global supply-demand balances.

Despite falling oil prices, the energy crisis is not over yet. In the medium term, an isolated Russia may “shut-in” some of its existing oil production in response to pending sanction policies, already-implemented sanctions, private sector “self-sanctioning,” or “strategic” efforts from Vladimir Putin to increase his leverage by cutting production. If this comes to pass, we are likely to see significant gaps in global oil supply in the medium term, likely leading to sudden and sharp price increases. Furthermore, against a backdrop of falling oil prices and recession fears oil producers have been reticent to expand investment. The Biden Administration should announce a plan to prevent extreme oil price spikes in the event of sudden, near-total loss of Russian supply to global markets.

Fortunately, three factors make the Administration more equipped than at any time since the creation of OPEC to address this risk. First, following the development of shale extraction methods, the US has emerged as the world's leading oil producer. Second, increased storage capacity of the Strategic Petroleum Reserve (SPR) is available to meaningfully affect oil markets. Last, the Department of Energy’s (DOE) groundbreaking proposal to allow the SPR to more flexibly acquire oil should allow the Administration to manage its domestic oil production and storage to blunt the unique tail risks latent in today’s energy picture.

The time has come to use the SPR to stabilize oil markets and domestic oil production by providing price insurance to domestic oil producers through the sale of put options. Put options from the SPR would serve as a “production insurance cushion,” and could coax additional investment from US producers, while buffering industry against the risk of price crashes in the event of oversupplied conditions. By doing so, the administration can head off the possibility of disorderly oil price spikes caused by Russian production losses in the medium term (in addition to other factors like increased Chinese demand).

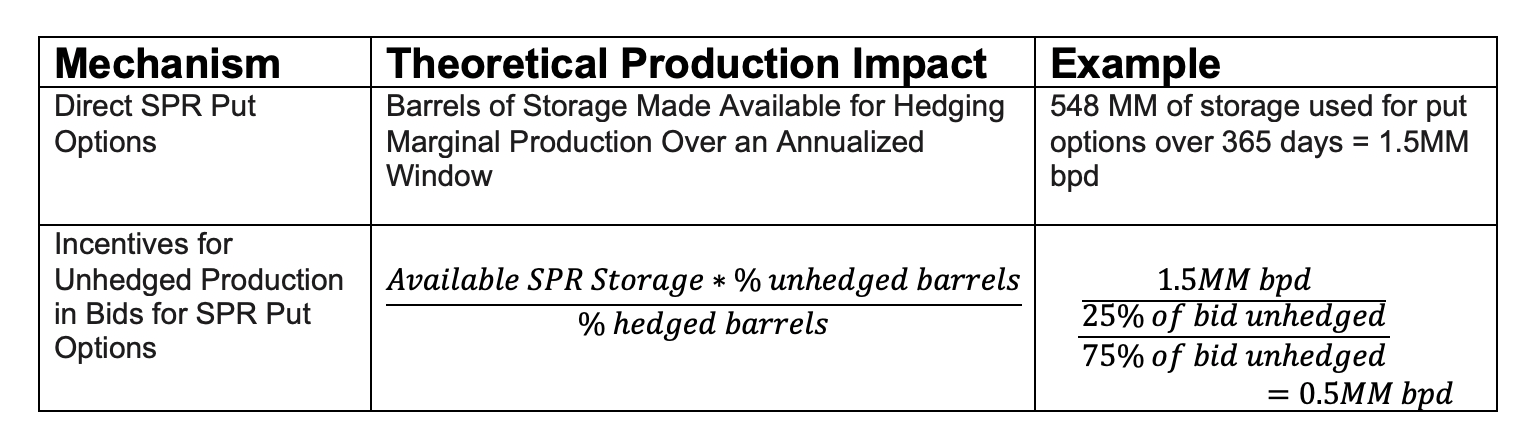

We estimate that a well-designed refill program could reasonably catalyze as much as 1 million barrels per day (bpd) of annualized additional US production. If additional releases free up 548 of the 714 million barrels of the SPR’s authorized storage capacity, the SPR would be able to use that storage space—along with the proceeds from SPR releases—to acquire oil by selling put options to industry. If we assume this storage space was made available for price insurance over a rolling 1-year period, 548 million barrels could mechanically translate into a 1.5 million bpd annualized production insurance cushion.

At these quantities of acquisition and new production, our capacity as a “swing” could be comparable to that of OPEC in terms of control over global supply and demand. For decades since its creation, the SPR’s “strategic asset” was oil in storage. But now, since the US leads production globally, the true “asset” is not the quantity of crude oil stored in the SPR—it is the presence of available storage that increases the ability of the SPR to structure oil acquisition in ways that manage severe price volatility.

The Oil Production “Multiplier”

In order to maximize the effectiveness of the available space, the facilities must be designed and managed with care. In short, put options could be sold through sequenced auctions in a manner that separates financial settlement from physical settlement, thereby working around the physical capacity constraints that limit the speed at which the SPR can be refilled (450 thousand bpd). Future pieces will elaborate the structure of these facilities in further detail.

Proper calibration of the strike prices of the options sold in these auctions could incentivize producers to leave 17-25% of the production in their bids unhedged (depending on the strike price of the put option and their internal breakeven). Although this estimate rests on some reasonable – even conservative – assumptions, it could imply a 20-33% multiplier to the quantity of production hedged through the auction of put options. By including both hedged and unhedged production, our suggested program could theoretically yield an additional 1.8-2.0 million bpd over an annualized window of time.

Of course in practice, such an increase would run into considerable mitigating factors that would dilute these estimates in the short-run, including supply chain bottlenecks (as acutely witnessed this year) and administrative challenges to targeting marginal production. But even with that in mind, one could reasonably assume an increase of 500,000 to 1m bpd. This is a large enough volume to meaningfully impact the price of oil and successfully curb the scale of sanctions-related Russian supply risks.

Why The Oil “Multiplier” Matters

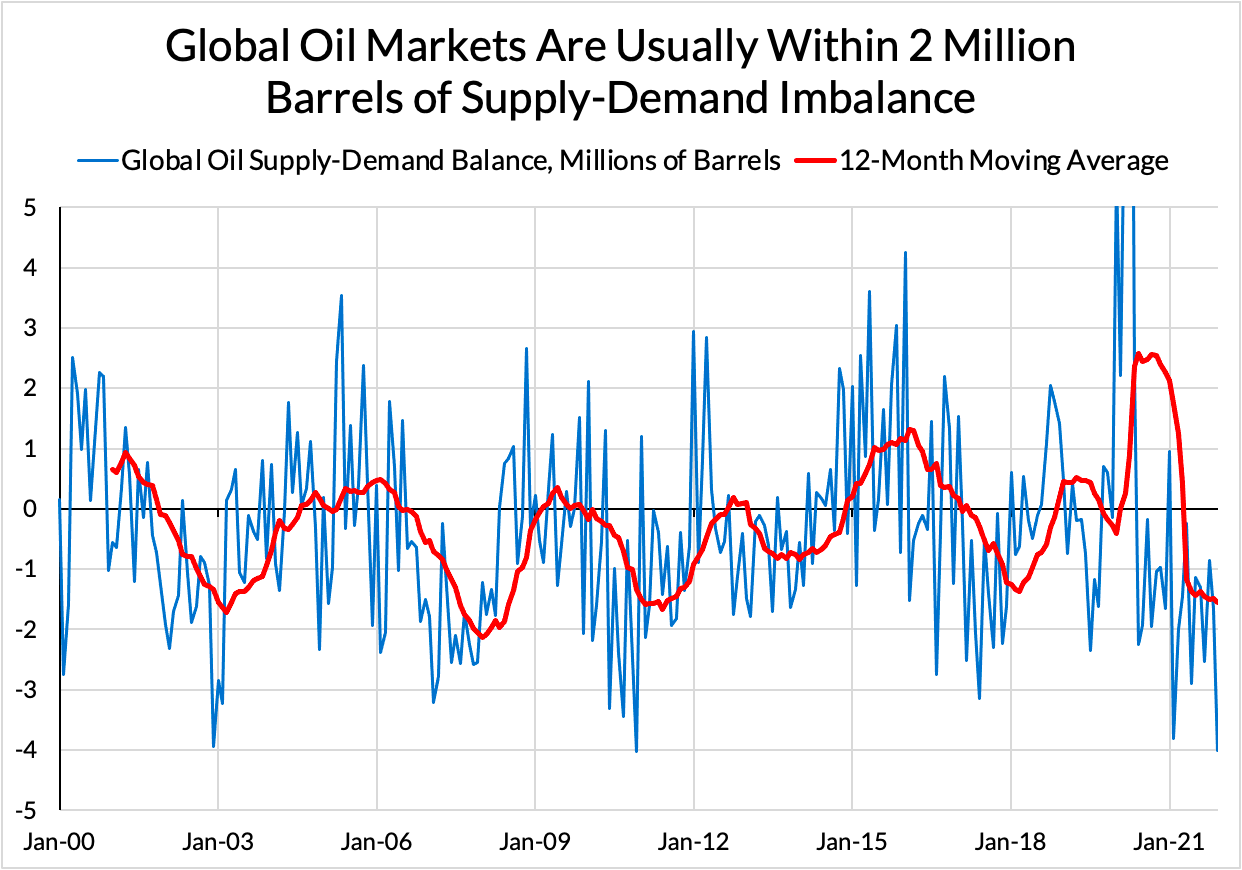

A common criticism against utilizing the SPR to constrain price volatility is that it is a drop in the bucket in a market that produces around 80 million barrels per day (mbpd). This criticism regrettably misses a major point. The overall size of the market or volume of production does not drive prices. Price is driven far more by the size of the gap between global supply and global demand. Over the past two decades, that delta has been highly correlated with crude prices.

Therefore, the price impact of a particular action is about the marginal production (or loss) and its impact on that global supply-demand delta. The more aligned the marginal production (or marginal acquisition into storage) is with the imbalance between supply and demand, the stronger the price impact.

Although this will not allow the US to pick and choose oil prices, it will have more power than at any point since the creation of OPEC. This is because the emergence of the United States as the world’s leading crude oil producer, a more flexible toolkit to acquire petroleum, and the significant available storage following the series of mandatory and discretionary releases over the past decade, each increase our discretionary capabilities to affect the price of crude oil. The SPR could have as much as 300-500 million barrels of available storage by 2024 given expected releases.

Our substantial proven reserves provide considerable capacity to ramp up production. This is particularly true in light of the diversity of basins from which short-cycle tight oil extraction is feasible and the depth of know-how within domestic industry. And in the context of historical supply-demand imbalances and their attendant price effects, the SPR’s authority can be quite meaningful. In the past two decades, the supply and demand imbalance—at their most stretched—has amounted to approximately 2 mpbd. For more than 90% of that same period, the imbalance was lower than 1 mbpd, including several periods when the price rose higher than $100 per barrel. Even the ability to cut a 2 mbpd delta to a 1 mbpd delta would have significant price effects.

These swing numbers are substantial relative to the price highs and lows over the previous two decades. In the first and second quarter of 2008, when the price had risen to a historic high, demand outstripped supply by about 2 mbpd. A marginal production increase of 1mbpd (or a release of equal size) could have alleviated nearly half of the imbalance. Alternatively, when the price of oil fell below $40 in 2016, supply outstripped demand by just over 1mbpd. If the SPR had the available storage it does today, it could have pulled a considerable amount of supply off the market, avoided gratuitous crude oil consumption, and promoted greater industrial and investment stability. With nearly 365 million barrels in available storage, the SPR already has considerable runway to acquire and store over a period without reaching the storage capacity limit of 714 million barrels.

The DOE’s recently proposed rulemaking also increases the DOE’s flexibility and power by enabling the separation of financial settlement from physical settlement. It would be well-within the power of DOE to, in a supply-abundant environment, purchase 1mbpd (perhaps even more). This would effectively pull those barrels off the spot market, while spacing out physical settlement (delivery) in a manner that aligns with the SPR’s logistical intake capabilities to ensure the facility is never overwhelmed.

Conclusion

There are implementation and governance risks that will dilute the capacity to reward marginal production and boost aggregate US production. Input and labor shortages are already weighing on the industry’s investment intentions. And of course, the ability of OPEC to engage in a price war looms. These are real challenges that hinder our ability to manage price volatility. In spite of these challenges, our ability to impact the price of oil is at its highest point since the creation of OPEC. Flexing that power begins with the DOE implementing a program to provide price insurance to producers.

This program can and should be implemented in a manner that is aligned with offsetting the risk of Russian production losses, thereby avoiding disorderly declines in global oil production. In the event that supply does overshoot demand, the DOE would become a contractual buyer of crude oil. The DOE would effectively take production off the market, thereby mitigating the risk of a deep crash in oil prices and a needless surge in crude oil consumption and greenhouse gas emissions. This is exactly the kind of state-contingent production that is well-aligned to resolve the risks we face today.

Given the risks of the situation and the latent power of the SPR, the Administration should take steps to begin the implementation of this policy today. By stabilizing oil prices at a level acceptable for both producers and consumers, the SPR has the ability to smooth the inflation outlook in the medium term while stabilizing energy and gasoline costs for Americans. Finally, this policy will ensure the economic viability of our existing foreign policy commitments and decarbonization investments in the longer term.

Many thanks to Rory Johnston of Commodity Context for his valuable comments and assistance with this piece.