Summary

Since the passage of the Inflation Reduction Act, efforts to secure the supply of energy transition commodities have intensified considerably. The Biden Administration has announced prizes, research and development initiatives, and loans for recovery projects to improve the U.S. supply chain for critical minerals. Other advanced economies are taking action: Canada has announced an ambitious critical minerals strategy and the European Union briefly considered stockpiling critical minerals. These activities are at least partially a response to China’s aggressive strategy and continued dominance in the supply chain. Recently, the US and allied nations have floated the idea of a “buyers club” to secure supply of critical minerals.

Across nations, the agency or agencies tasked with executing the obligations such a club would have a number of design questions to answer including what products to target, how to price the products, and how to match government authorities to the financial realities of commodity markets. We consider these questions in a continuation of our Contingent Supply series, exploring how a critical minerals club (and the executing agencies of member governments) could undertake our SPR approach to boosting production of a highly volatile commodity, lithium. The boom and bust cycles of lithium investment and mine development have helped drive shortages and ultimately, hindered the transition to green energy. The first piece described why storing spodumene would be a worthwhile endeavor for a lithium strategy. This piece describes the importance of selecting the right location for spodumene reserves.

Overview

The US should play a leading role in efforts to secure a more resilient decarbonization supply chain by working to create a buyer’s club for critical minerals. As we’ve previously written, affordable hedging options for producers require the creation of liquid market benchmarks. Without these price benchmarks for private actors to coordinate around, policy designed to crowd in private investment will face significant headwinds.

In our last piece, we showed how the lithium precursor spodumene is a natural choice for a market benchmark. Like crude oil, it is comparatively easy and affordable to store, it is relatively simple to grade compared to other lithium compounds (which makes high volumes easier to handle), and the production cycle is short.

Yet as important as deciding what to store is, we must also decide where to store it. In determining the location for such reserves, answering a few key questions can provide important insight. Geology tends to cluster geographically--and commodities infrastructure has historically been designed around this simple geological fact. For publicly-backed reserves to both manage price volatility and support the creation of liquid benchmarks, they need to be situated in a manner that minimizes costs for producers and consumers to deposit and withdraw from those stocks. Successful buffer stock strategies rely on easily accessible storage locations for the underlying commodity to actually remain liquid at benchmark prices. Poorly-placed reserve storage can quickly increase the costs, difficulties, and variabilities involved in using benchmark-linked commodity supplies, reducing the degree of liquidity associated with the benchmark price.

The importance of this cannot be minimized. Given the costs associated with delivering crude to the Strategic Petroleum Reserve’s caverns in a short time window, bid prices came in considerably higher than the WTI benchmark price in its most recent pilot acquisition. To properly shape a market, public infrastructure must be directly connected with the pathways used by that market.

Furthermore, the location is critical for private market participants as well: the more divorced the benchmark’s location is from the producer’s reality, the less likely it is that the producer can use that benchmark to hedge its investments in production. For example, CME launched a lithium hydroxide future in mid-2021, but producers and consumers in North America and elsewhere have tended not to use it for hedging, because it is based on prices for delivery to China, Japan, and South Korea. Therefore, the location of a benchmark’s underlying storage facility is an important policy design decision.

Why Doesn’t West Texas Intermediate Settle in Texas?

What can existing commodity benchmarks teach us about how to locate the spodumene storage facilities necessary for a successful price benchmark?

Over the past few decades, the most important US crude benchmark has been West Texas Intermediate (WTI), first offered by the New York Mercantile Exchange (NYMEX) in 1983. Somewhat counterintuitively however, WTI contracts settle in Cushing, Oklahoma, rather than in a Texas hub (like Houston). NYMEX selected Cushing because of its considerable storage capacity (the world’s largest onshore oil storage facility), its proximity to production, and its existing infrastructure to affordably transport crude oil. Via Cushing’s pipeline network, crude can travel from the vast West Texas oilfields to the refining networks of the both Midwest and the Gulf Coast. The lesson is simple: for producers and consumers to trust the benchmark price, they have to be able to move commodities in and out of the benchmark’s location quickly at transparent and affordable costs.

The key here is that in addition to the ability to store significant quantities of the commodity, a benchmark can only become liquid if the cost to transport is transparent, relatively low, and unconstrained. When selecting the location of a storage facility that would serve as the basis for a benchmark spodumene contract, policymakers (in concert with exchanges) should prioritize locations near existing production that have high-quality (and low-cost) infrastructure to transport. For a non-fluid bulk commodity in an international context (like spodumene), this primarily means access to maritime and rail networks. Here are a few potential locations that might make sense for storage reserves in a US-led critical minerals club.

Canada

A spodumene reserve in Quebec would suitably meet the requirements of proximity to production and existing transport infrastructure. For example, a storage facility in Montreal or Quebec City would be worthwhile. Northern Quebec has at least five high-volume spodumene mines in production, including one that just recently commenced production. As the feasibility studies for these mines state, the producers plan to either export the spodumene via the Port of Montreal, or to send the spodumene to processing facilities in Quebec City or Montreal (last year, Rio Tinto announced an “industrial scale” lithium refining pilot plant near Montreal).

The mines are located near major, well-paved roads that can accommodate the transport of bulk commodities all ultimately connected to Canada’s major rail network as well. For example, the James Bay Mine is:

“accessible all year-round via the paved Billy Diamond Highway which allows oversized haul trucking to and from site, including the town of Matagami... [which is] connected to the Canadian National Railway network, allowing future production to be railed to various locations in North America or any port along the Saint Lawrence River for international shipment.”

The connection to the rail network offers pathways for transport throughout North America, and perhaps as importantly, to Europe, as shipping via the Port of Montreal is the shortest direct route to Northern Europe and the Mediterranean from North America.

United States

The most appropriate place to locate a spodumene storage reserve would be North Carolina. The US Geological Survey estimated that three deposits contain 426,600 metric tons of lithium, potentially enough lithium to supply batteries for over 50 million electric vehicles. The largest spodumene project is owned by Piedmont Lithium, and Albermarle also has existing assets that are producing spodumene in the area. Situating the storage facility near the “tin-spodumene belt,” would be beneficial as the area is accessible by road and rail: the Piedmont facility is directly accessible by several state highways, CSX railroad, in close proximity to two major national highways, and four major ports, Charleston, Wilmington, Savannah, and Norfolk.

The connection to ports would allow the shipping of the spodumene internationally, and the interstate connectivity is particularly useful in the context of the domestic investments in the battery supply chain announced following passage of the Inflation Reduction Act. North Carolina is situated nearby many of these investments, including a $1.3bn lithium processing facility announced by Albemarle in South Carolina, and a $600mm processing facility announced by Piedmont in Tennessee, which it currently plans to use to process its spodumene sourced in Quebec and Ghana.

Given the efforts to build out the US battery supply chain domestically, situating a spodumene reserve in North Carolina near production, existing infrastructure, and processing facilities would be an important measure to build resilience and insulate the domestic electric vehicle industry from international supply chain vulnerabilities.

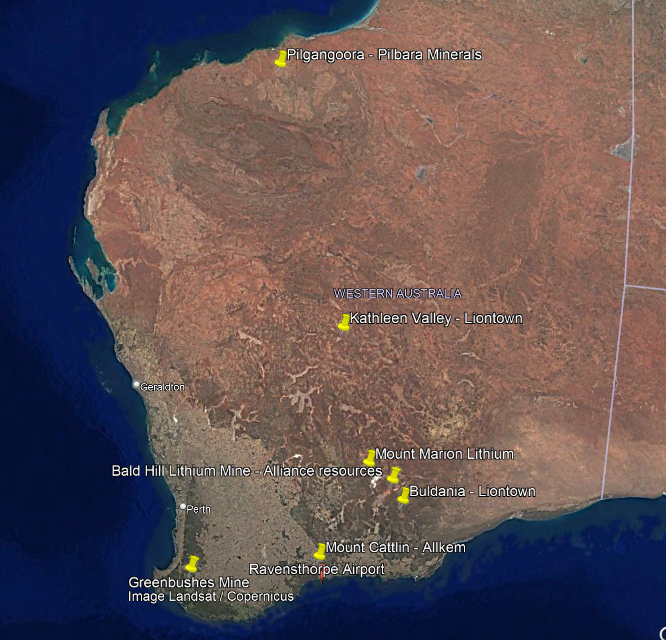

Australia

Western Australia would be a good location for a storage reserve, as it is home to Australia’s largest producing spodumene assets. Selecting a specific location is easier than Canada or the US because Australia already has a deep infrastructure network for delivery to port for its spodumene production--so there is no need to reinvent the wheel. Three ports in the state already take delivery of spodumene for exports. The Greenbushes mine is the nation’s largest producing asset (co-owned by Albemarle, Tianqi Lithium, and Independence Group), and ships its product directly from the Port of Bunbury. Other major producers ship from the ports of Esperance and Hedland.

A spodumene reserve in Western Australia is a good case example of how Australia, Japan, and South Korea would be well served by the approach of a critical minerals club well-suited to fill the broader goals for allied nations in a critical minerals club. South Korea and Japan are two nations hoping to build out their electric vehicle production capacity and limit their reliance on China. Australia is a major producer of lithium, but highly dependent on China which, according to a report in 2021 from the Western Australia government, imports over 85% of Australian lithium. This poses significant risk to Australian miners in the event of market interruptions (as witnessed during the late 2010s boom and bust cycle) or from geopolitical conflict. A storage reserve in Western Australia could help build regional resilience, and at little additional cost since these ports already ship the vast majority of their product to China (our internal calculations indicate that shipping from Western Australia to Japan rather than China would add less than two days at sea). And any of the ports within Western Australia could work -- given very low bulk dry shipping costs as a share of spodumene cost (less than 0.25% at today’s prices), each port would allow delivery and storage terms with minimal “slippage” due to logistics.

Brazil

As the US and the EU consider a critical minerals club, Brazil would be a worthwhile partner to include. In addition to its mineral wealth, Brazil has a new leader advocating for expanding commodity production while pushing for more responsible mining practices and higher royalties for the government. Brazil would also be a strong candidate for a spodumene reserve facility, specifically in or near the state of Minas Gerais.

Minas Gerais has two major spodumene mines, the Mibra mine owned by AMG, and the Grota do Cirilo mine, owned by Sigma Lithium, which is the largest hardock deposit in the Western Hemisphere and just received its permit and should begin production “within days.” As a major iron ore production area, Minas Gerais has extensive shipping infrastructure that could be especially relevant to European markets (though it would also be low cost to move Brazilian spodumene to reserves in North Carolina or Canada due to this port capacity and low shipping costs). The Minas Gerais mines are also connected by national highways with the ports of Vitória and Ilhéus.

Locating a storage reserve near the Port of Vitória may be particularly worthwhile. AMG has launched an export route out of the Port of Vitória specifically for spodumene, and is also building its own hydroxide refinery in Europe. There have been numerous announcements for new European lithium refining capacity by Ensorica, Northvolt as well. Either way, by capitalizing on existing and germinating infrastructure, Brazil could be a critical partner in building supply chain resilience by building a spodumene reserve.

Conclusion

Good public policy should support sustainable investment and price stability in the energy transition commodities sector. The model is the approach we have advocated for to utilize the purchasing power and storage capacity of a public asset like the Strategic Petroleum Reserve to offer affordable hedging options for producers to minimize investment risk and stabilize prices over the long-term. A US-led critical minerals club would be well-positioned to execute this strategy. Key to its design would be building the storage capacity necessary to weather price volatility and to support the creation of new benchmarks that can crowd in private investment.

As we’ve seen with the SPR, the location of these facilities is an important design decision. The location of the SPR caverns increases delivery costs and ultimately leads to a higher acquisition price than the WTI benchmark would indicate. Looking at the nations that could make up a critical minerals club, including IPEF nations like Canada and Australia, but also incorporating the EU and other major producers, like Brazil, we identified four potential locations.

These locations – Quebec, North Carolina, Western Australia, and Minas Gerais – are well-situated to serve as reserve locations and delivery points for financial benchmark indices. Most spodumene is already moved by heavy bulk from Australia and Canada. Both countries have ready port access and the capacity to build reserves for storage for a critical minerals club. For the United States, production from North Carolina could provide some security as well as storage at the Port of Wilmington both for domestic production and imported product storage for physical delivery into contracts. Minas Gerais is both a spodumene production hub and a suitable point for delivery to the EU given existing and developing infrastructure.

The heart of successful industrial policy is in the details. Even the siting of reserves is economically relevant to their ability to achieve their stated goals. Keeping the private sector building at the rate our planet needs requires a stable benchmark price for spodumene, and that stable benchmark price requires the relevant storage facilities be sited in sensible locations relative to the mining and refinement of spodumene which can nonetheless easily address global markets.