By Skanda Amarnath

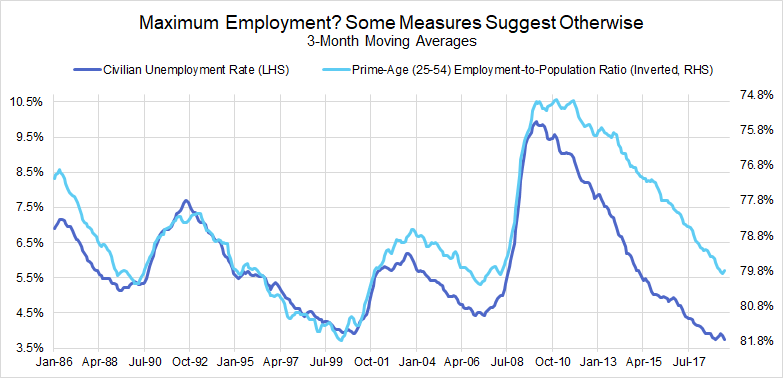

The prime-age employment-to-population (PA EPOP) ratio is better than the headline (U-3) unemployment rate as a barometer of labor utilization. Canada shows us that even when PA EPOP is pushed to new highs, wage and price acceleration does not necessarily follow or persist. It is time we rethink the interactions between labor markets and inflation.

Employment-to-population (EPOP) ratios measure labor utilization more robustly than unemployment rates.

The Fed’s approach to policymaking and communication should reflect this reality. It claims to be looking at alternative measures of labor market slack, but in practice, they serve mostly as secondary and tertiary supplements.

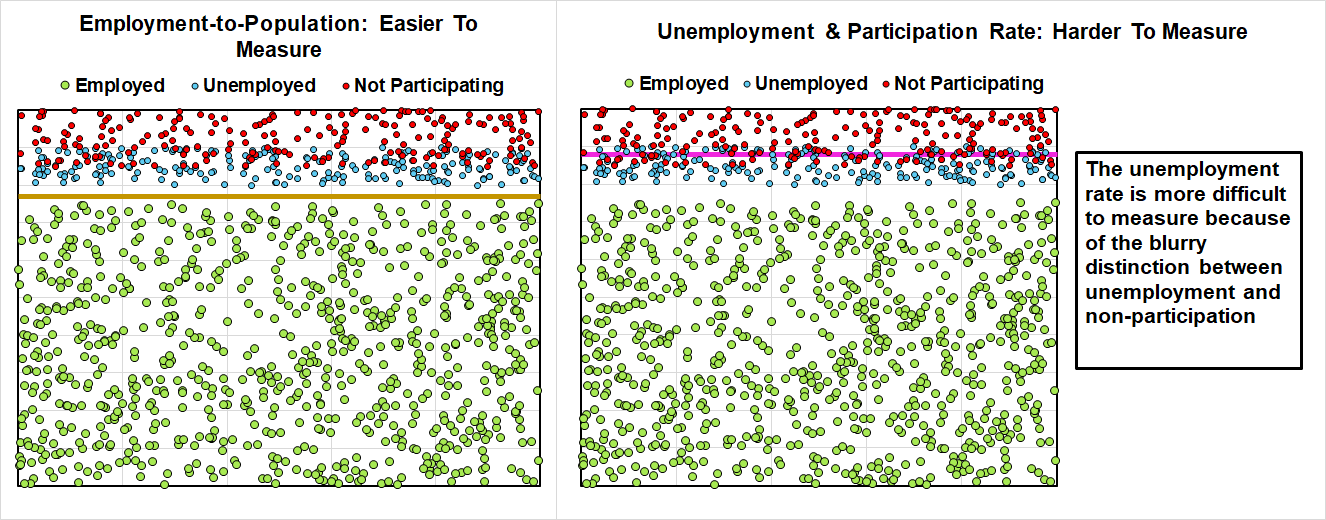

Ahn & Hamilton (2019) highlight a core problem in the Current Population Survey (CPS), which is used for calculating the headline (U-3) unemployment rate.

- The CPS does a poor job of distinguishing between those who are not participating in the labor force and those who are participating but unemployed. This blurry distinction likely leads to persistent but time-varying underestimation of the labor force participation rate and the unemployment rate. (Figure 4)

- The CPS can more robustly distinguish between who is employed and who is not employed. As a result, EPOP ratios are a more robust starting point.

The challenge with the headline EPOP ratio is that there are acyclical demographic trends that also require adjustment.

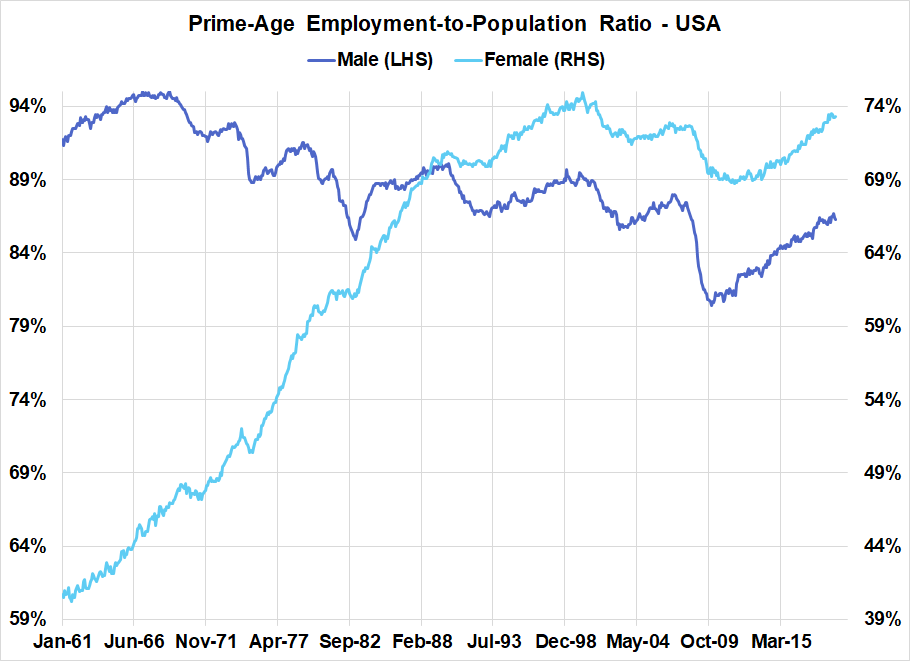

- To adjust crudely, EPOP for prime-age cohorts (25–54) would remove the major acyclical trends related to schooling, which mostly affects those younger than 25, and retirement, which mostly affects those older than 54. More granular adjustments are also feasible using the CPS.

- Prime-age EPOP would have been a less helpful measure during much of the 1960s, 70s, and 80s due to the systematic rise in female employment.

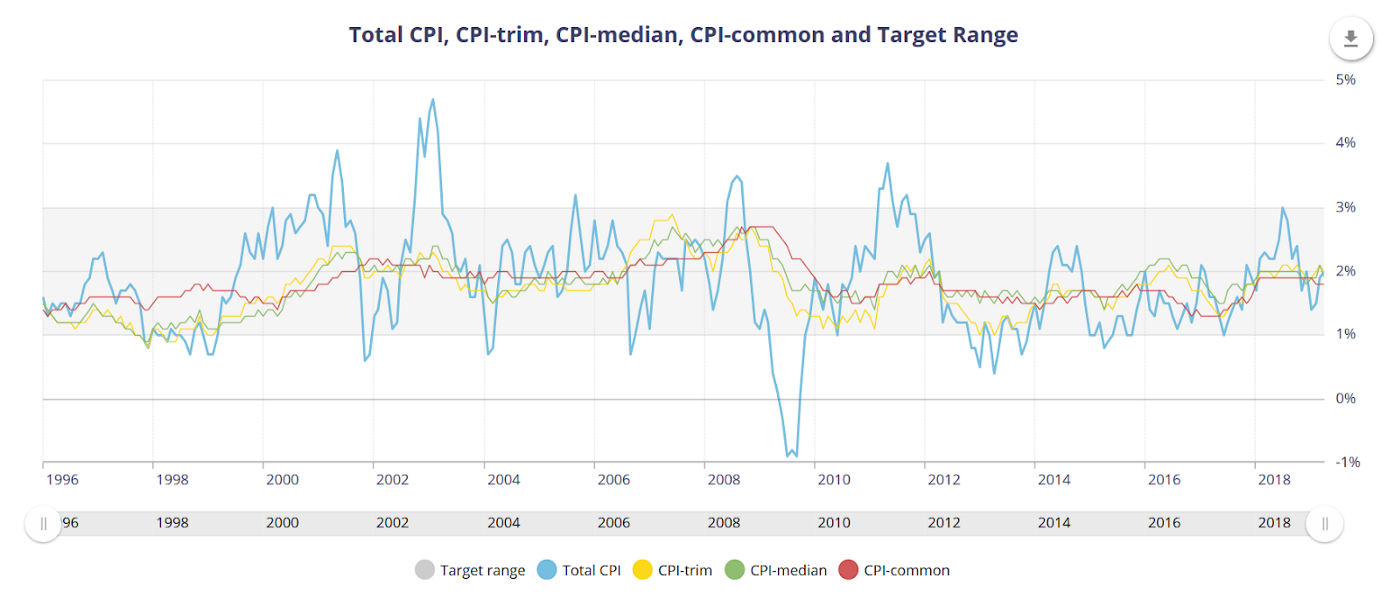

Canada’s prime-age EPOP has been historically elevated, but accelerated pressures on wages and prices have not materialized as of yet.

Under modern macroeconomic frameworks, inflation is supposed to be largely a function of expectations, which we cannot measure directly, and the relative level of labor utilization (or the “output gap”). The simplified logic underlying this idea is that as labor grows more scarce, businesses will be more likely to raise wages and prices.

To many, the puzzle now is why we have not seen higher inflation in the presence of low unemployment. One common view is that we are not measuring “true unemployment” correctly. While PA EPOP should address most of these measurement issues, Canada shows us that even this explanation fails to hold up under closer scrutiny. We might have to acknowledge that even the best measures of labor utilization will serve as an an incomplete assessment of whether, in the context of price stability, maximum employment has been achieved.

Not only is Canada’s prime-age EPOP above the US, but it is currently at a new all-time high relative to its own history! Nevertheless, Canada has seen little in the way of sustained inflationary pressures.

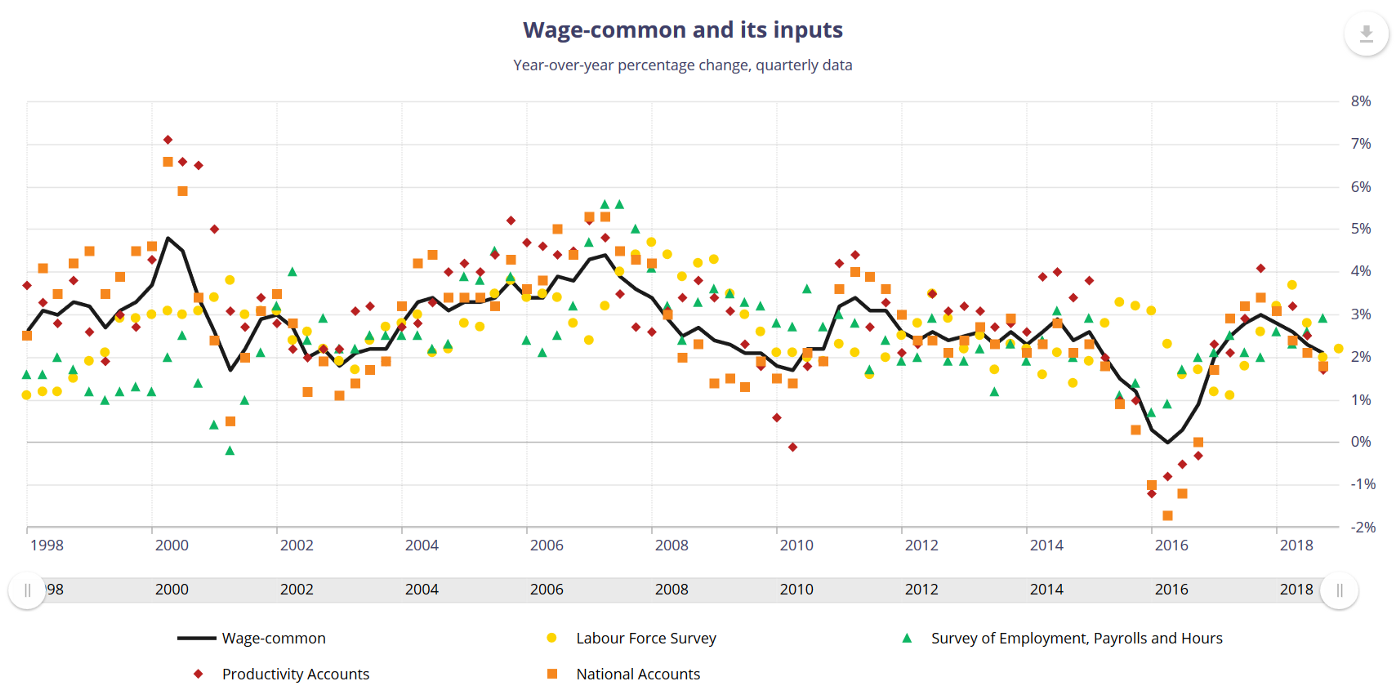

We have not even seen anything resembling sustained wage acceleration either.

Time to rethink model specification!

It is easy (and virtually unfalsifiable) to claim that the rate of unemployment or prime-age employment is simply very different from what we previously assumed. Canada has pushed both measures to such an extreme and yet the conventional approach is still failing to offer useful results.

- The common answer we hear is that the Phillips Curve is so flat that inflation expectations are all that matter for determining inflation outcomes, and that labor markets have become virtually irrelevant. However, such a claim fails to explore other potential explanations for how labor markets are relevant aside from the level of labor utilization.

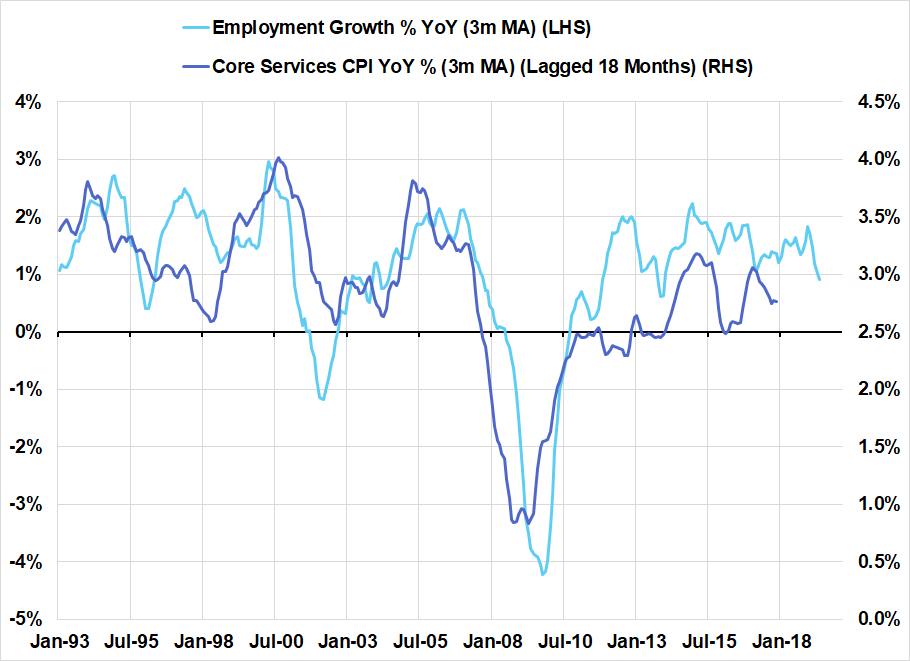

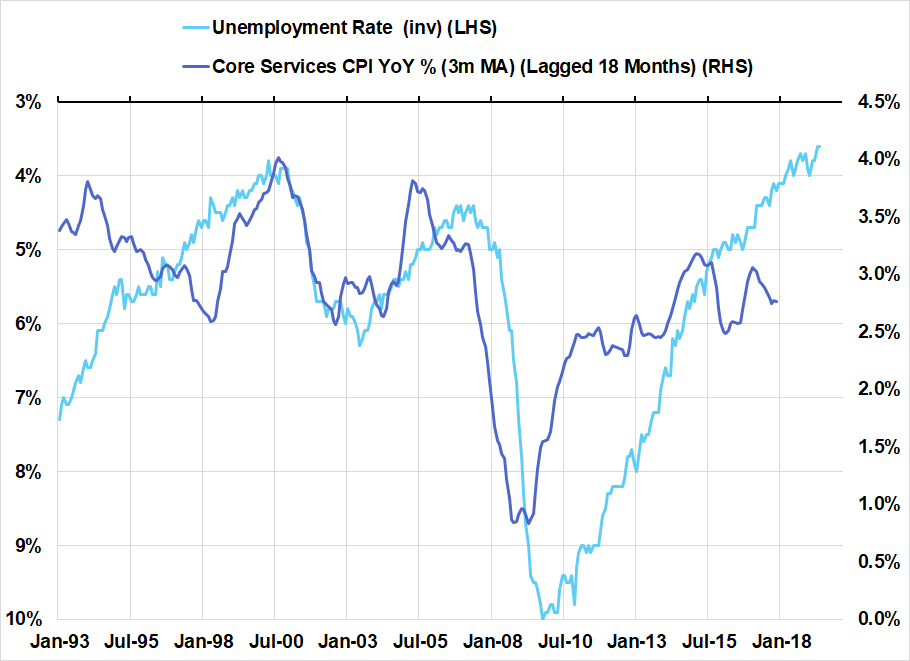

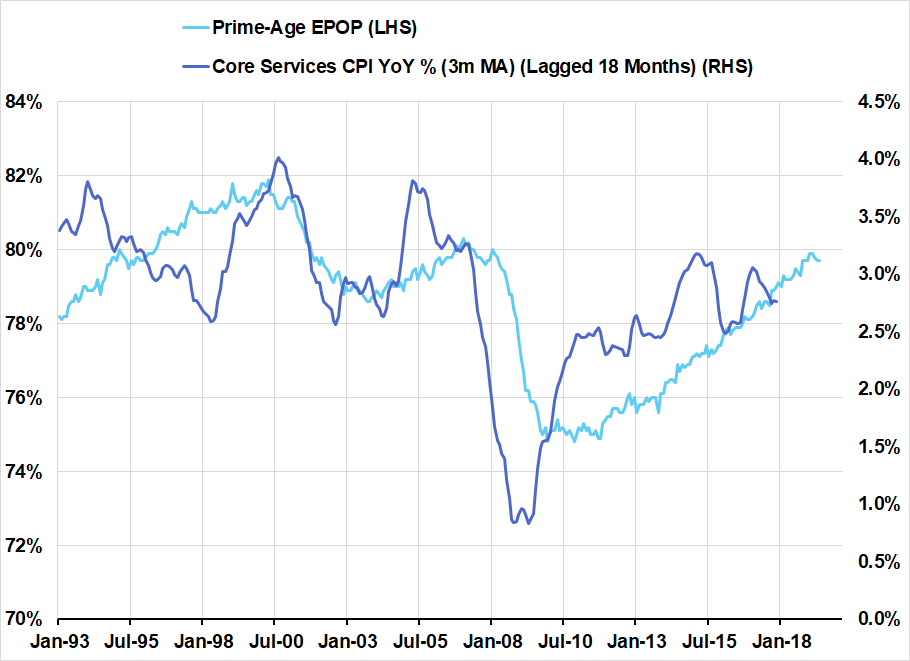

- For example, what if it is the change in labor utilization that matters for price stability, and not solely the level itself? If that were the case, then labor utilization would only be constrained in terms of speed, not in terms of destination. In other words, it doesn’t matter where you are on the road. It might only matter how fast you are going!

- After accounting for the lag in inflation, it appears that major segments of inflation are more correlated to the change in labor utilization than the outright level. There is more work to be done here, but if you would like some initial food for thought…

Concluding Thoughts

There are good and not-so-good reasons to focus on the prime-age employment rate. If you are trying to measure labor utilization while adjusting for the appropriate acyclical factors, the prime-age employment rate is an excellent starting point. If you’re expecting inflation to show up once a high PA EPOP ratio has been achieved, Canada’s current set of outcomes suggests otherwise.

Some in the dismal science might be disheartened to learn that Phillips Curve dynamics are even less evident in economies with historically high levels of labor utilization, but we prefer to take a more optimistic view. At least in the near- to medium-term, labor markets in the US and probably even Canada have scope to be more inclusive without triggering sustained acceleration in prices.