Inflation

The economy, as we all know, is mainly made up of goods and services that people buy and sell. This is an intuitive divide: when you pay for something – whether you are a business, household, or government – it’s either an object or an action, and its prices are based on the cost of providing the good or service plus some markup. Most of inflation forecasting is arguing over the cost of inputs or the level of the markup. When costs or markups change, prices change and we see inflation (or, rarely and historically disastrously, deflation).

Usually, indexes of goods inflation are taken as indicators of the cost of materials and upstream equipment, while indexes of services inflation are usually taken as indicators of the cost of labor. Goods inflation is then traditionally seen as an indication that the economy is “overheating” due to demand outstripping supply, while services inflation is seen as an indication that wages are “too high.” The intuitive justification here is the idea that, since services are usually rendered by workers, labor probably makes up the bulk of unit cost of an arbitrary service. We can see an example of this in the Fed’s recent (and possibly temporary) reliance on “Core PCE Services ex-Housing” as a measure of inflation due to underlying wage-pressure. Despite this, we have good reason to believe this intuitive rule of thumb may not provide good guidance in the near future. There are several places where the price of services is likely to be substantially dependent on the prices of goods involved in furnishing those services.

Food

As anyone who has been to a restaurant recently can attest, increases in the prices of food commodities can quickly pass through to food services and food away from home. Although the Food At Home category is substantially more volatile than the Food Away From Home category, we can see in the data how shifts in the prices of food commodities can lead to shifts in the prices of food services.

Each time food prices jump, we can see a lagged and dampened response in Food Away From Home. Given the substantial elevation in food commodity prices, there is good reason to believe prices in the latter category will drift upwards for some time in response to the spike in food commodity prices.

Transportation Services

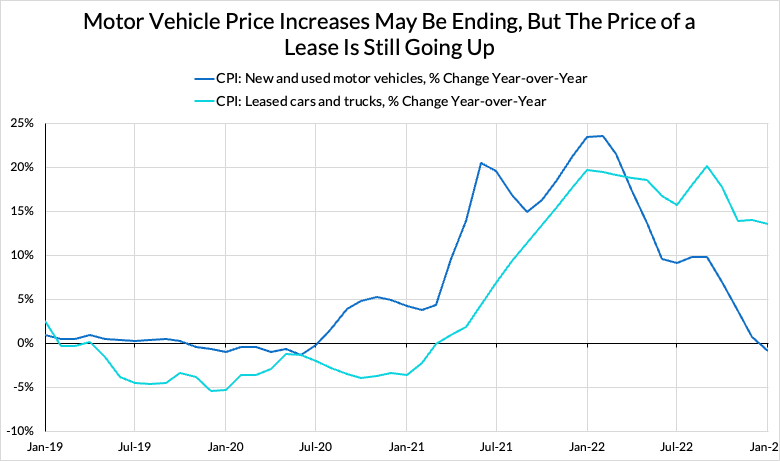

We see a similar dynamic in different parts of Transportation Services as well. The price of cars, and car parts, play a major role in the cost of leased vehicles and vehicle repairs, even though the latter two categories are technically services. Leased and rented cars and trucks often have price exposure to new and used vehicle markets in a variety of ways.

A similar dynamic obtains for motor vehicle parts and motor vehicle repairs. Although each is a comparatively small portion of the overall CPI index, the co-movement in the two series is instructive.

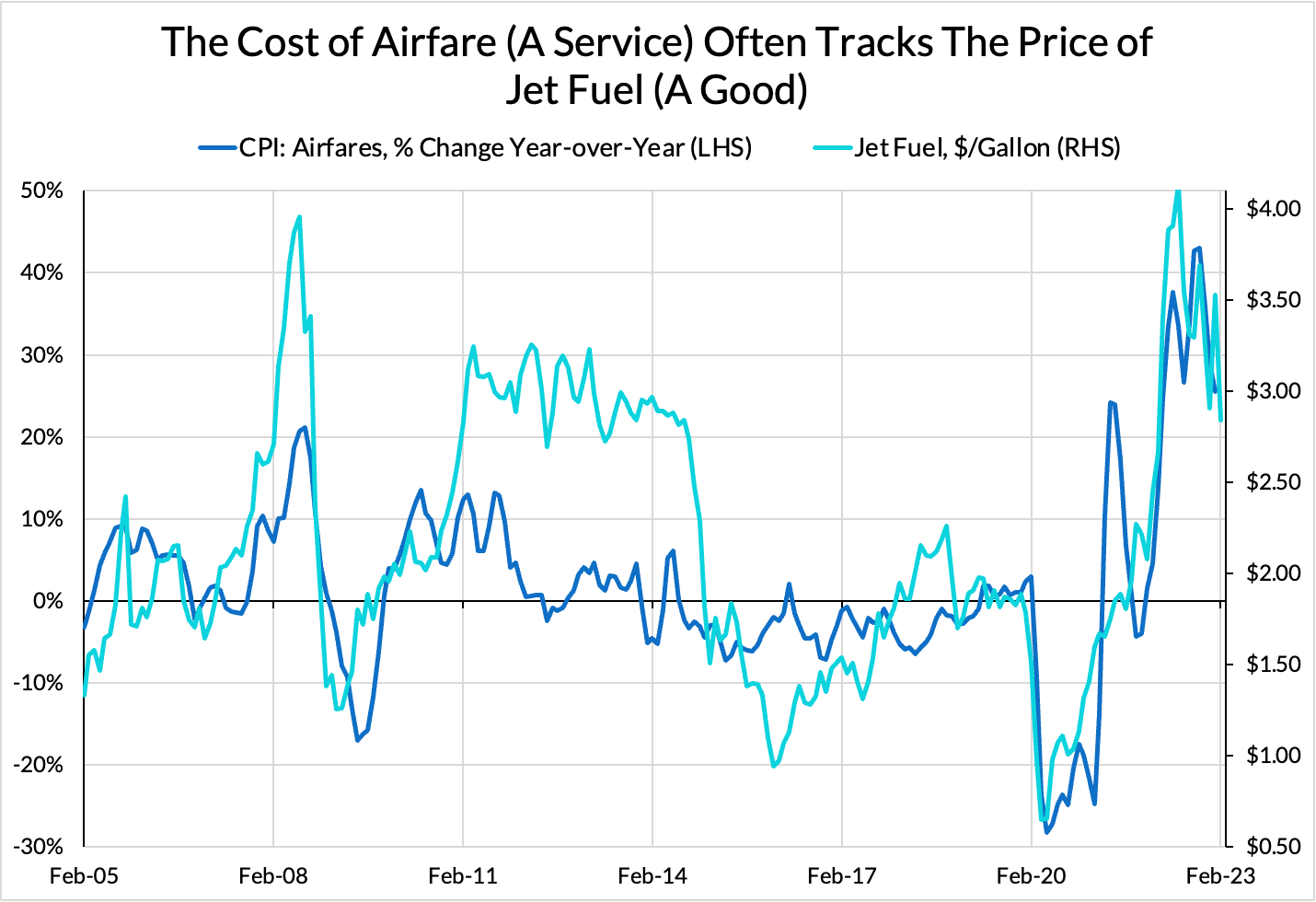

We are likely to see the same dynamic in airfares as well: rising prices for commodity inputs driving up service prices.

Energy

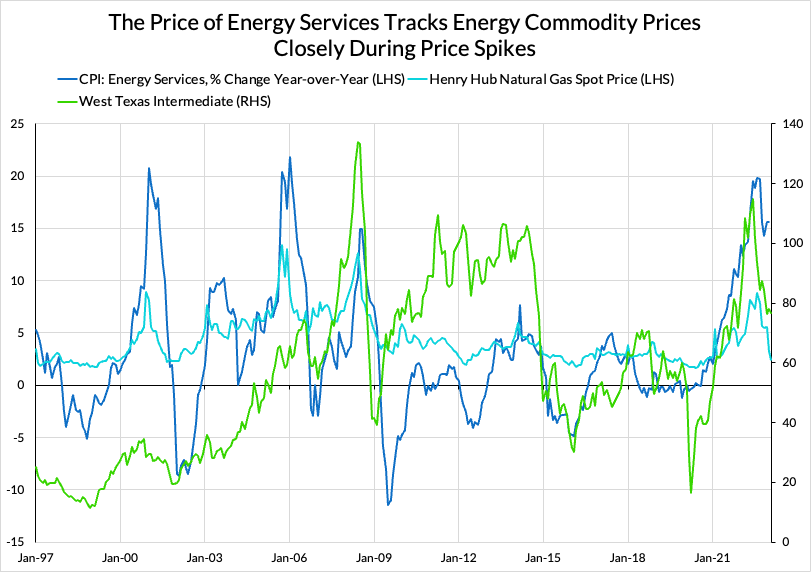

Energy commodities play a key role in determining the price of energy services, for the simple reason that energy services are almost always produced by burning energy commodities. Luckily these movements are tending in the opposite direction from the two above – towards disinflation – but the basic premise of services prices being determined by goods prices holds here as well.

We should be wary of attributing all strength in service prices to labor costs. Ignoring this dynamic may lead one to believe that we need to see dramatic labor market corrections for inflation to come down, which may not be true, but will be costly for everyday Americans. Simple heuristics like “goods = materials costs, services = labor costs” should come with a “buyer beware” warning in this period of economic dislocation.