Industrial Policy

The following was originally presented as “Towards Macroprudential Fiscal Policy” at the Coordinating the Supply Side: Creating a Systemic Industrial Policy for the 21st Century conference put on by the Berggruen Institute in December 2022. In light of recent discussion about the scope, aims, and variety embedded in industrial policy, we at Employ America are republishing this talk with the goal of reorienting discussions of industrial policy around the question of securing full employment and low inflation while managing a large industrial economy.

In the aftermath of the pandemic, we are seeing new momentum behind industrial policy as an approach to managing the American economy and guiding the development of productive capacity. Speaking in my capacity as an economist for a full employment focused think tank, Employ America, this situation has the potential to be a watershed for developing new and more effective full employment policy. Over the pandemic, prices spiked as tangled global supply chains led to shortages, frictions, and the simple unavailability of certain goods. Looking beyond the pandemic, an industrial policy approach seems to be the most effective way to address the climate transition. Achieving the level of investment required to decarbonize and electrify our economy will likely require something more than the everyday operation of capital and commodity markets.

“Industrial Policy” is an incredibly broad umbrella, with a range of historical implementations from France’s Dirigisme to Japan’s MITI to China’s Special Economic Zones to the Marshall Plan and countless others. Unlike many other economic discourses, attempts to develop trans-cultural or trans-institutional accounts or models of industrial policy have been rare in recent years. Much of the following relies on an older developmentalist tradition that runs from Alexander Hamilton to FDR to Albert O. Hirschman, each skeptical of “the market” in their own ways. What ties each of these approaches together is that they had clear — often developmentalist — goals, and that they concerned the method by which the government made or sponsored investments in physical capacity while helping manage markets towards realizing publicly-defined economic goals. In most cases, Industrial Policy programs were reasonably long-lived, lasting from 20 to 50 years. For projects that long, it can be helpful to start with a map.

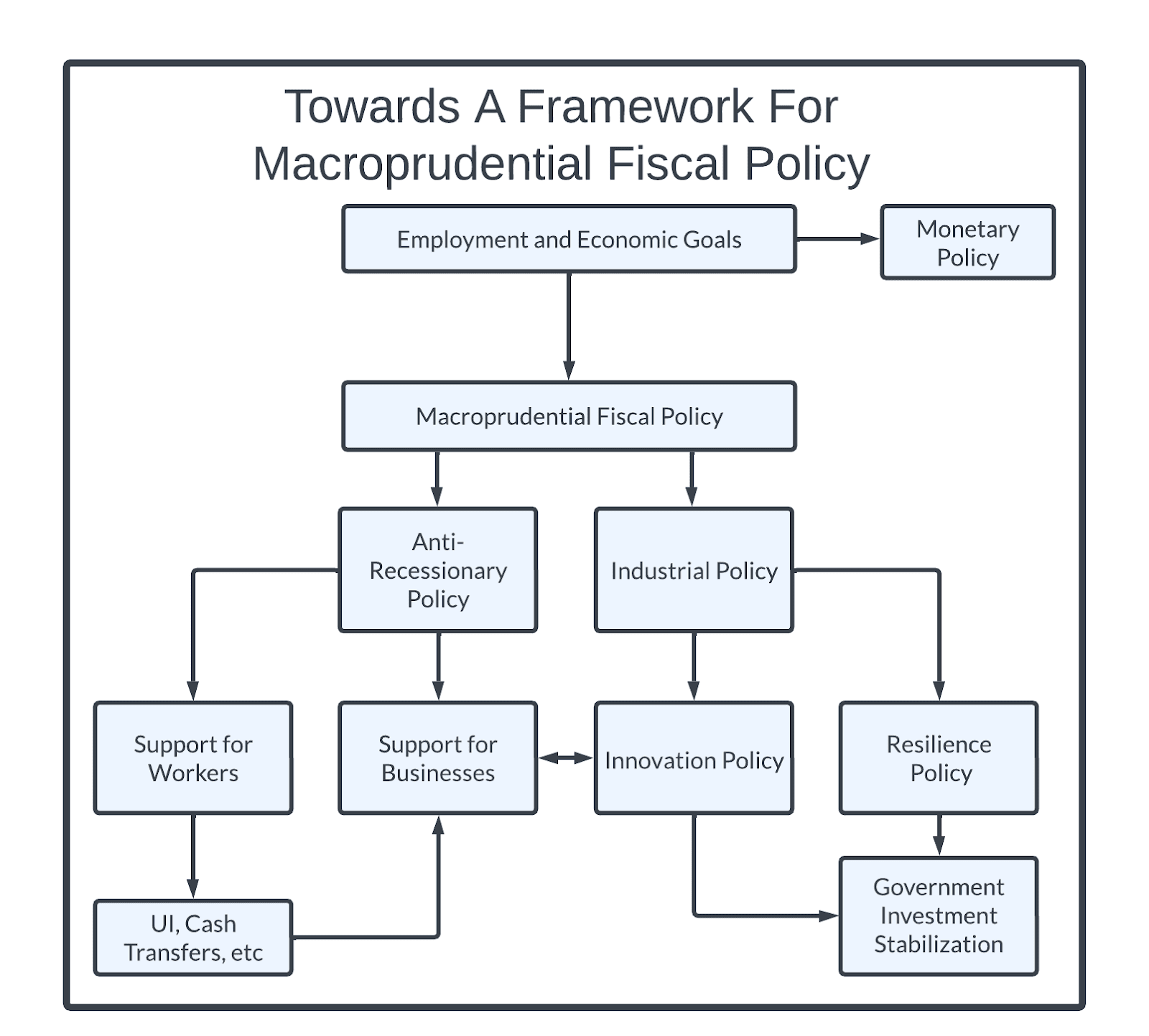

My goal today is to lay out the broad architecture of the macroeconomic aspects of one possible approach to a mature Industrial Policy. In order to clear the ground for a New American Industrial Policy discourse, I am going to try to group the main macroeconomic functions of successful industrial policy into a handful of simple dualisms. These dualisms all rely on an idea borrowed from central banking: the idea of “macroprudential” policy. For central banks, macroprudential monetary policy is a collection of regulations and interventions to secure the stability of the financial system as a whole, rather than any particular financial institution. By way of analogy, the goal of macroprudential fiscal policy ought to be the stability of aggregate investment and the productive structure of the economy as a whole, rather than any particular firm or sector alone. The analogy is obviously inexact, but as an analytical lens, it has proven helpful to my thinking while working on industrial policy proposals for semiconductors, energy, and other sectors, so I would like to share it in the hope it helps others.

There are two sides to macroprudential fiscal policy: anti-recessionary policy and industrial policy. These two strategies are often assumed to be linked — with infrastructure investment programs often rolled out as immediate solutions to recessions — however the role of each will be much clearer if we separate the two. We learned in the aftermath of the 2008 crisis that “there is no such thing as a shovel-ready project.” Years passed between the passage of the American Recovery and Reinvestment Act and the first paychecks going out to Americans working on the project. However, this is not a criticism or failure of industrial policy.

Anti-recessionary policy acts on the demand side to secure the labor market, making sure that when Americans lose jobs, businesses do not also lose customers. These policies functioned extraordinarily well over the pandemic, as Pandemic Unemployment Assistance, extended Unemployment Insurance, the Child Tax Credit, and a number of other programs ensured that the bulk of our economy could weather an otherwise-massive negative shock to demand. Anti-Recessionary policy must quickly and directly intervene on the demand side during downturns to keep Americans solvent and spending. This is something that industrial policy cannot do.

Instead, industrial policy acts on the supply side — although in truth the goal is to act upstream of immediate “supply,” by operating on “capacity,” or the ability of firms and supply chains to scale up supply in response to an increase in demand. Through slow and steady support of specific investment projects, industrial policy can guide the macroeconomy as a whole, at the level of both sectoral composition and the direction of innovation. This guidance can be used to produce a wide range of outcomes, from ensuring the availability of lithium to domestic car producers to ensuring the availability of key components for semiconductor and other electronics production.

Together, anti-recessionary policy and industrial policy comprise an entire macroeconomic toolkit. Anti-recessionary policy is fast and simple, industrial policy is slower and more difficult. Were we to be operating from this framework prior to the pandemic, we likely would have seen substantially less economic disruption, as businesses would have remained confident in the scale of the government response to the pandemic recession. Not for nothing that a few percentage points of year-over-year inflation are still downstream of the decision by automakers in the early months of the pandemic to cancel their outstanding orders of key semiconductors with a view towards an extended 2008-size downturn. They learned their lesson well — so much the worse for the rest of us that it was not the right lesson.

So, what are the goals of the kind of mature, macroprudential industrial policy the American economy needs? There are essentially two kinds of goals: goals where industrial policy acts alone, and goals where industrial policy acts to reinforce the efficacy and sustainability of anti-recessionary policy.

Industrial Policy has always played a critical role in the development of new industries and new capacity. A changing economy will need a changing set of inputs. Right now, the strategy for developing new inputs is for them to become increasingly expensive, luring new producers into the market. However, this strategy is fraught with pitfalls and obstacles. As today’s geopolitical situation evolves, industrial policy must be ready to take the economy where it needs to go to meet future challenges at every step of the supply chain.

Achieving the climate transition will also rely heavily on the kinds of programs traditionally associated with industrial policy. Addressing climate change will require an incredible volume of investment in both mitigation and adaptation. A recent Bloomberg BNEF pegs this investment need at over 170 trillion dollars between now and 2050. Securing this level of investment without leveraging the balance sheet space of the American government is simply not plausible.

Industrial policy and anti-recessionary policy are both key to the goal of Capacity Maintenance. A major lesson of the pandemic has been that the US economy is not in a position to smoothly transition from foreign production to domestic production. This is a problem. Successful industrial policy should ensure that sufficient spare capacity is maintained for robust anti-recessionary policy to be deployed without the threat of excess inflation as the recovery proceeds.

Additionally, much of the capacity shed in the US economy was shed during recessions that were met with an insufficient demand-side response. During these contractions, key sectors like housing, semiconductor production, and automobile production hemorrhaged workers and physical capacity. We are still seeing the scars from these losses today. Proper and timely deployment of anti-recessionary policy of the scale undertaken in response to the pandemic could plausibly have prevented some of this capacity loss, making today’s job easier for industrial policy.

Another core goal of industrial policy is the stabilization of the level of investment across the business cycle. Fluctuations in the level of investment — whether during a recession or not — can have outsized impacts on employment at both the aggregate and sectoral levels. These fluctuations also hamper the development of the capital stock, leaving us with a less-complex and less-resilient economy than we could otherwise have.

The final goal for mutually-reinforcing macroprudential fiscal policy is the achievement of full employment without excessive inflation. In any recovery — even if capacity is preserved — demand often ramps up faster than supply, as newly-employed workers spend their wages. The inflation this has produced over the pandemic recession cycle has led some to question whether the dramatic fiscal supports were “worth the inflation.” With proper capacity maintenance, ramping up supply to meet demand on the way out of a recession will happen faster, stalling inflation even as labor markets continue to strengthen. This is at variance with much conventional economic wisdom, but after the dramatic policy success of the pandemic there are no good reasons — moral or economic — to allow the system to stabilize itself through unemployment.

Now that we’ve worked through the principles, what is the state of play today?

There are currently three large proto-industrial policy acts with staffers feverishly working on implementations: the Inflation Reduction Act, CHIPS and Science, and the IIJA. Each of these programs address different problems, but have similar pitfalls: not enough data, not enough coordination. However, the development of solutions to these issues is still possible, depending on how these programs are implemented.

Effective and durable industrial policy will require us to change how the state “sees” the market. Often, industrial policy is derided for “picking winners” or being overly influential at the microeconomic level. Yet, the microeconomic level is not the appropriate one on which to make or evaluate macroprudential policy. New data and tools need to be developed for the US Government to understand the role and impact of Industrial Policy. This may mean annual and more granular input-output tables, more granular labor and price statistics, or more unified categories of economic activity to provide a more properly synoptic view. With this data, the government will have a clearer picture of the issues facing the economy in the near future, allowing them to better bargain with partners in industry, while also targeting investment and labor market policy more appropriately.

My hope is for this little exercise in thinking through a possible structure for industrial policy leads to more effective conversations between those working on the macroeconomic side and those working on other, more qualitative, aspects of Industrial Policy.