The coronavirus shock will lead to a dramatic spike in the unemployment rate. But even this surge could understate the true labor market damage from the virus. This is because:

- the emergency unemployment insurance benefits passed as part of the CARES Act temporarily relaxed the eligibility requirement that workers be actively looking for work; this will cause at least some of the labor supply response to be along the non-participation margin rather than the unemployment margin; and,

- some of the labor market response will be among workers who are still working but are involuntarily part-time. In the latter case, even looking at workers part-time for economic reasons may still prove insufficient, as households reducing hours due to coronavirus-related issues may cite a reason besides the economy for reduced hours, such as health or family care.

I introduce a broad labor market underutilization metric I call “NPOP” to better capture the future effects of the virus shock. NPOP incorporates any American not working full-time or voluntarily part-time.

Former Fed Chair Janet Yellen once said that if she had to pick only one indicator of the labor market, “the unemployment rate is probably as good a one as I could find.”

The unemployment rate — the share people with or looking for a job who are out of work — is indeed an economic metric par excellence. It mirrors much of the behavior we see other datasets; in economic jargon, it captures a lot of cyclical variation. And it does this while also being reasonably meaningful in its own right to non-economists.

No one doubts at this point that the unemployment rate will ultimately spike sharply thanks to the coronavirus. It may not start surging until the April data released next month, but some independent forecasts have it eventually exceeding the 26% peak reached during the Great Depression.

But even when it does rise, the unique circumstance of the coronavirus may prevent the unemployment rate from capturing the full breadth of the economic damage.

Unemployment misses people who drop out of the labor force, and workers who don’t have the hours they want.

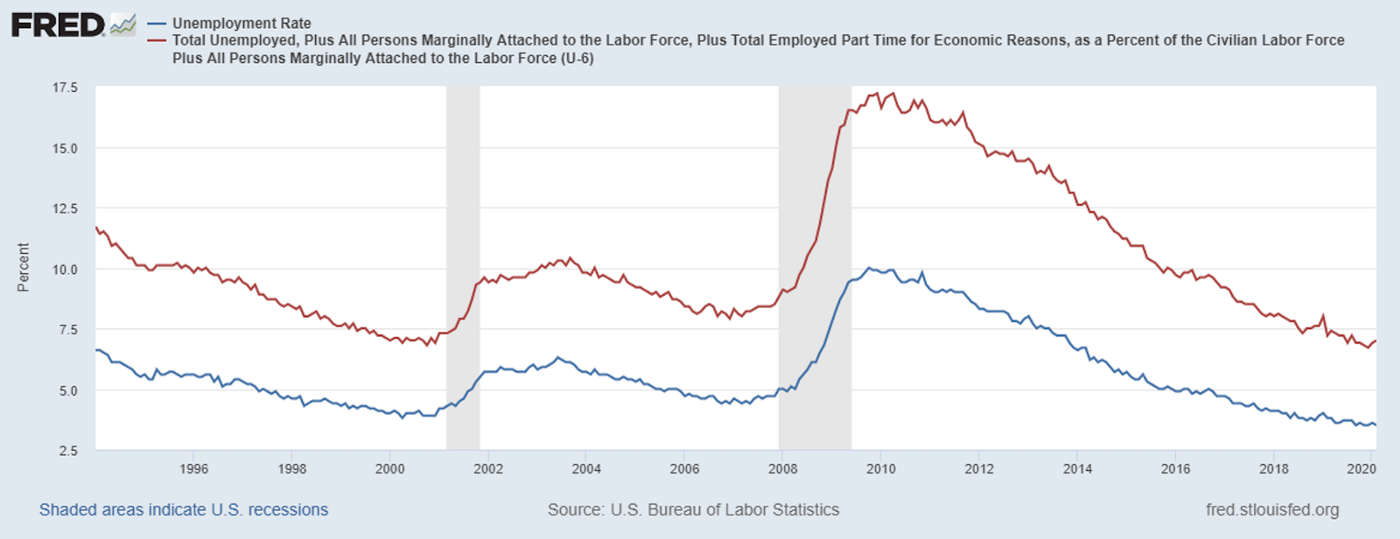

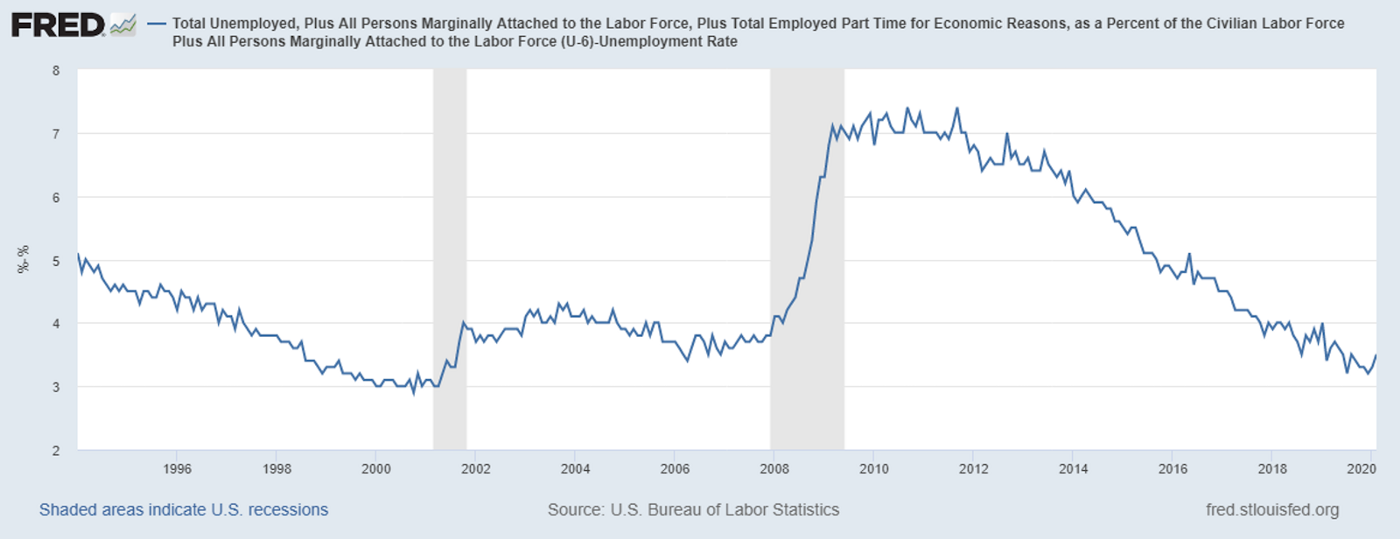

This is akin to the issues with the unemployment rate during the post-2009 recovery. The unemployment rate was not exactly a Pollyanna metric for much of this time: it peaked around 10% late in 2009 and only fell slowly thereafter. But even then, it left out key Americans who were hit hard by the recession. Frustrated Americans who gave up looking for work and left the labor force entirely — whom economists call “nonparticipants” — are not counted as part of the unemployment rate. Nor are Americans who are still employed but getting less than full-time hours thanks to the soggy economy; these workers are “part-time for economic reasons.”

As well as the unemployment rate captures the essence of the labor market, nonparticipants and workers part-time for economic reasons turned out to be a larger-than-usual piece of the economic pain after 2008, which made the unemployment rate in this cycle less comparable to past recessions and recoveries.

To be clear, this doesn’t make the unemployment rate “wrong” or “fake”; it’s very real. It just means that the unemployment rate may understate the economic damage in an extraordinary circumstance where disproportionately more pain is felt among the populations it doesn’t capture.

2020 may shape up to be similar to the post-2009 recovery. Again, the rise in the unemployment rate will tell most of the story of the coronavirus. But key parts of the pain will also be missing.

This time though the reasons will be a bit different than the recovery, for two reasons.

Not as many workers losing their jobs may show up as “unemployed” this time around.

First, not everybody losing work in this crisis will meet the definition of “unemployed” in the Current Population Survey (CPS), the source of the unemployment rate. One major reason is that a key incentive to look for work is not present over the next few months: the CARES Act temporarily relaxed the requirement that workers receiving unemployment insurance be actively looking for a job. It also added a flat $600 per week benefit to regular state UI benefits for four months; this will put UI close to or even modestly above 100% wage replacement for some workers.

Congress did this for a perfectly justifiable reason: it would be counterproductive to public health, to say nothing of obtuse to economic reality, to expect workers to find and take another job while the coronavirus is forcing businesses to shutter and families to stay indoors.

The likely impact of this policy in the data will be that a larger-than-normal share of people who leave employment over the next several months will show up as nonparticipants — that is, not actively looking for work — rather than unemployed.

Some existing labor market metrics attempt to incorporate some nonparticipants. The U6 rate, for example, is broader than the headline unemployment rate, in part because it adds in workers who aren’t actively looking for a job any more but say they want one and have looked for one over the past year. But some laid-off coronavirus workers may not have looked for a job over the past year, keeping them from being counted in the U6 rate too.

Many workers will keep their jobs but have their hours cut, and they may cite a factor other than the economy.

The second reason has to do with part-time work.

As with the Great Recession & recovery, the coronavirus shock will likely cause a sharp rise in the number of Americans who are part-time but want full-time work.

During the post-2009 recovery, economists typically accounted for this by measuring the number of workers part-time for “economic reasons”. These are Americans who work part-time but want full-time hours, and cite “economic reasons” — lack of demand or lack of available full-time jobs — as the reason they cannot get the hours they want. And in fact, the U6 rate also incorporates these workers.

But this time around Americans may more heavily cite a broader array of reasons beyond just “economic” ones — such as child care or health — for their low hours. So workers “part-time for economic reasons” — and measures that incorporate them like U6 — may still exclude other important people in this economic catastrophe.

Why not prime-age EPOP?

Many economists including myself have been fond of using the prime-age employment-to-population ratio (or prime-age EPOP) as a better measure of labor utilization in the post-2009 recovery. Prime-age EPOP has some attractive features, such as its tight correlation with wage growth. And I have little doubt prime-age EPOP will fall in the months ahead. But I also worry that the coronavirus shock will have a larger-than-normal effect on hours and the elderly, two margins that prime-age EPOP doesn’t capture.

Of course if the economic pain doesn’t disproportionately fall on these groups, it may turn out that any of the standard measures — the headline unemployment rate, U6, prime-age EPOP — end up summarizing the coronavirus shock quite well. But a priori I see blindspots in all of these measures that could potentially miss the story.

Introducing NPOP: a broad labor underutilization measure

Capturing the full extent of the coronavirus shock to the labor market will be difficult. It requires a broader metric than is currently published that covers all of the following:

- The unemployed

- Labor force nonparticipants

- The involuntary part-time, for any reason

To add to challenge, we will likely need a metric that captures all ages, given the unique sensitivity of older populations to the coronavirus. But that makes any metric harder to compare over time because it will be more prone to demographic effects from an aging population.

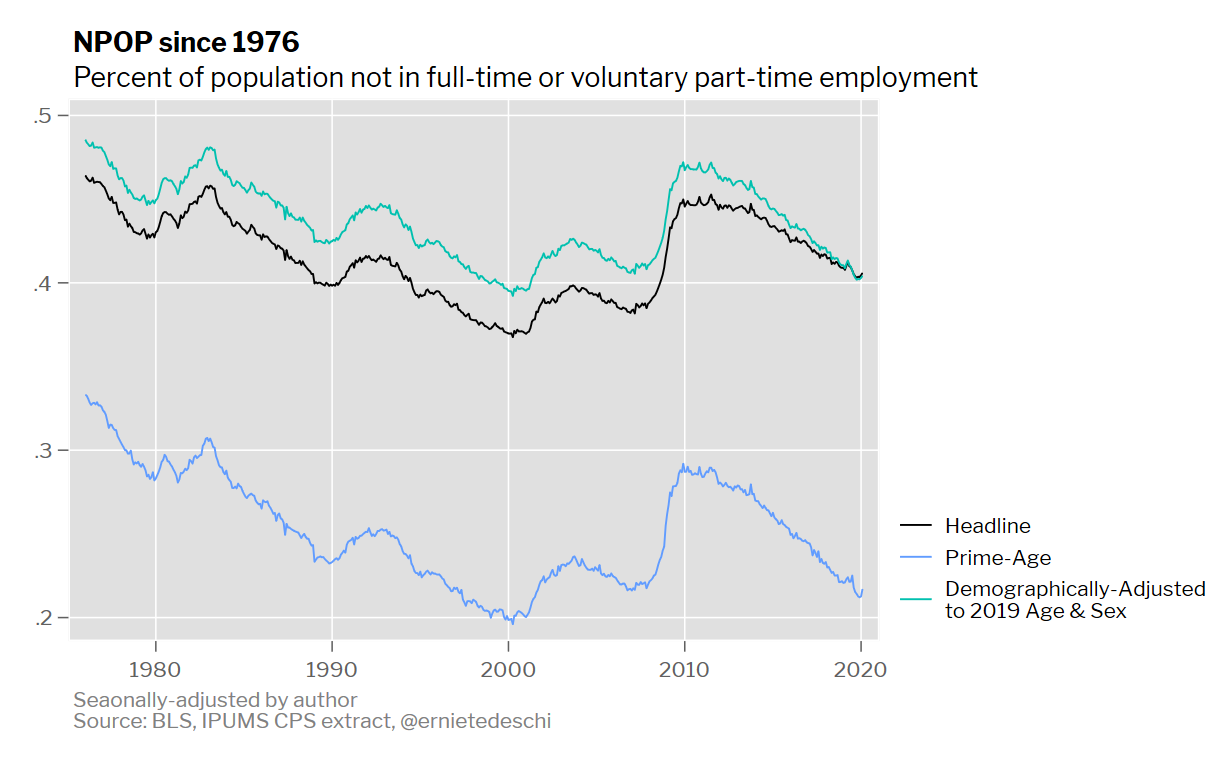

My proposed solution to this puzzle is a measure I’m calling “NPOP”. NPOP here is the percent of the total population that is either 1) unemployed, 2) not in the labor force, or 3) involuntarily part-time for any reason. Looked at differently, it measures the share of the population that is not employed full-time or voluntarily part-time. So NPOP is a much broader measure of labor underutilization than U3 or U6.

For very short-run changes, like the next several months, this headline unadjusted NPOP is likely sufficient. But over longer periods of time, NPOP isn’t apples-to-apples. That’s because the American population is aging, which means that we’d expect NPOP to naturally rise even in a healthy labor market.

One way to address this is to just look at NPOP for Americans age 25–54, which I’ve added below. But if seniors are hit disproportionately by the coronavirus, then just focusing on prime-age Americans may miss the full picture. So I’ve created a “demographically-adjusted NPOP” series that controls for changes in the composition of the population by sex and age over time. This adjusted series is more appropriate for longer-term comparisons.

As you can see, in all cases, we are going into the coronavirus shock with NPOP that was low but not quite back to levels consistent with the hey days of 2000.

In the end, the coronavirus shock will be a painful experience for many Americans. While many will show up as unemployed, many will not. A thorough assessment of the economic damage should keep as wide a perspective as possible going forward.

____

Methodology

“NPOP” is the share of Americans who are not full-time or voluntarily part-time employed, calculated from the basic monthly CPS microdata. In the IPUMS Basic CPS Extract, full-time and voluntarily part-time employed Americans are coded as:

EMPSTAT between 10 & 12

and either

- WHYPTLWK equals 0, 1, 70, or 80, or

- UH_WANTFT_1 does not equal 1

“Chained NPOP” uses a Fisher ideal index to chain the NPOP series based on 5-year age and sex cohorts. The resulting chain-weighted series is based to 2019. The advantage of a chain-weighted index is that the choice of base period does not affect the underlying behavior of the adjusted series.

All series are adjusted for changes in the CPS beginning in January 1994, so that all months are on a post-1994 basis.

All series are seasonally-adjusted using X-13ARIMA-SEATS.

Ernie Tedeschi is a policy economist and the Head of Fiscal Analysis at Evercore ISI, a macro advisory firm. He is also an occasional contributor to The Upshot section at The New York Times. Previously, Ernie was a Senior Advisor and Economist at the US Department of the Treasury. His research interests include the federal budget, monetary policy, and labor markets. You can follow him on Twitter at @ernietedeschi. The analysis here is solely his own.