That the current round of inflation has hit the poor harder than the rich has become a common refrain. Rent, food and energy - categories of consumption that make up a disproportionate share of the household budgets of low-income Americans, and which the Fed itself often acknowledges little control over - have seen dramatic price increases. Commentators across the ideological spectrum have argued that inequality and the need to protect the poor justifies a more hawkish path for monetary policy.

What these arguments miss is the fact that – as we outlined – interest rate policy primarily slows consumer spending and consumer price inflation by being able to slow down the labor market first. If tighter monetary policy is to slow inflation in the short term, it will likely do so primarily by denying jobs, paychecks and raises to the very same lower-income workers hardest hit by inflation.

To take these arguments to their logical extreme, the Fed may even be able to raise measured “real wages” by causing such a deep recession that oil prices collapse, but that deep recession will also lead to disproportionate job loss among those with lower income and wealth. The whole thing recalls an old quote from a US Army major during the previous significant round of inflation: “it became necessary to destroy the village to save it.”

Inflation and the Poor

It is true that poorer Americans have faced a budget squeeze as the inflation of the past eighteen months has proceeded. CPI-based measures of the cost of rent have increased at a pace of 4.4%, while food and energy have seen eye-popping increases of 7% and 27% respectively. Even after adjusting for the relative importance to inflation for each component, these are still stark price increases.

It is also true that these consumption segments make up a greater proportion of the budgets of poor households than richer households. By itself, this suggests that the poor have indeed faced a disproportionate share of cost of living increases relative to the rich.

As the charts show together, these inflation-sensitive components make up 35% of the budgets of the poorest 10% of households and less than 15% of the budgets of the richest 10%. That these components account for almost half of headline inflation shows how unequally the impact of inflation affects different income groups.

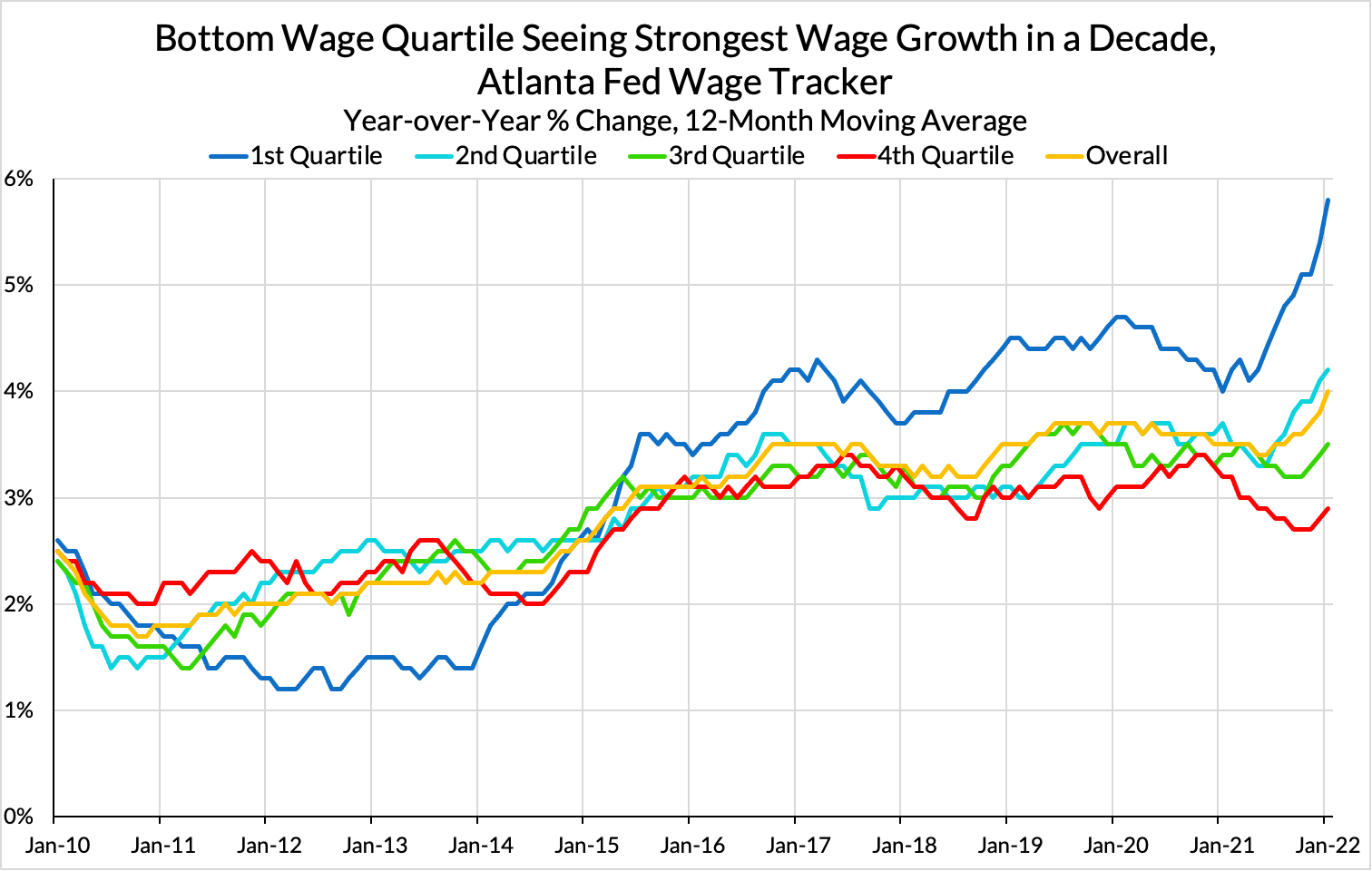

However, as we walked through in detail, the mechanism by which the Fed has any effect on these prices likely operates primarily by slowing down the labor market. Tighter labor markets support marginalized workers' ability to find employment and exercise bargaining power over the terms of that employment. Already we see a compression in the wage distribution and shrinking employment gaps that suggest a better labor market for low-income workers.

Even though there are multiple measures of wages, no measure is without flaws, including the generally superior Employment Cost Index and the Atlanta Fed Wage Tracker. Analysis from Dallas Fed economists Joseph Tracy and Sean Howard along with Cleveland Fed economist Robert Rich suggests that wage gains–as measured in the Establishment Survey’s “Average Hourly Earnings” measure–have likely been understated by composition bias: Real Wages Grew During Two Years of COVID-19 After Controlling for Workforce Composition. As we warned earlier, real wage measurement is a messy business that deserves a more careful and cautious discussion

Inflation by Income Decile

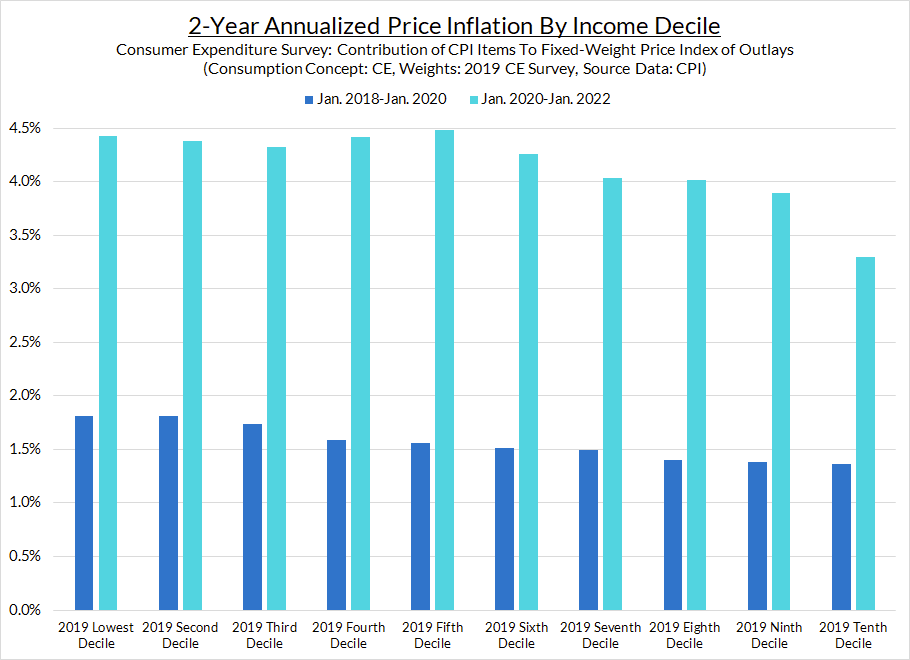

The best way to get a sense of how measured inflation has been different for different income groups would be to compute the CPI measure by income level. The BLS is in the process of developing experimental CPI measures by income quartile but as this paper from Josh Klick and Anya Stockburger illustrate, there are a number of complicating factors associated with constructing such indices. As a quick-and-dirty approach to figuring out how cost of (desirable) living has evolved for households in different income levels, we work from simple fixed-weight price indices using the expenditures shares in the 2019 Consumer Expenditure (CE) Survey by income decile. These measures will naturally be inexact: the CE Survey is an important input for the CPI’s weighting scheme, but cannot by itself provide apples-to-apples comparisons against CPI or PCE measures. The CE survey uses slightly different classifications and different aggregation approaches that limit the granularity of available data, increasing the error bars on all of our estimates of inflation by decile.

The issues with imputing indices from CE data do matter. Differences in aggregation classification and in the universe of measured transactions between the CE Survey and PCE and CPI data may over- or under-weight certain kinds of consumption. For example, the rich spend more on transportation, but it’s the poor who disproportionately bear the brunt of higher transportation fuel costs. At the same time, financing and insurance payments, as well as imputed consumption–consumption a household enjoys but does not directly pay for–are complicated to properly account for using the CE Survey. There is no current cash expenditure for these consumer goods or services; the debt service payment for your house or your car reflects the cost and payment of already-purchased capital and is thus excluded from CPI. If debt service payments were included, lower interest rates would thereby lower more components of inflation.

Since the categories and classifications underlying the various datasets involved do not exactly line up, this analysis may and likely will be subject to correction and revision regarding the classification of each CPI component within the CE survey. We will provide a transparent record of corrections and revisions as necessary, but the likely sources of error should not alter the major takeaways.

Caveats aside, this analysis further suggests that the burden of inflation is disproportionately borne by the poor. Although this was true both during and before the pandemic, the problem has become more acute. As noted above, much of this disproportionate burden can be attributed to higher food and energy prices. Motor vehicle expenses – maligned throughout 2021 for their contribution to elevated inflation – also play a substantial role, but more neutrally across the income distribution.

As the chart makes clear, inflation during the pandemic has been substantially higher for all income deciles, but the impact on the highest income deciles is noticeably weaker. While we have made note of the differential impact of inflation on the rich and poor, what the charts above suggest is that the greatest change in inflation rates has happened for middle-income households. This may lead to some salient political dynamics, especially given the contribution of gas prices to current inflation readings.

In plain english, wages are probably rising faster than inflation for low income households. While inflation dynamics have been meaningfully dispersed across income deciles (approximately 1-1.5%), wage compression dynamics are likely even more dispersed across incomes. Subsequent iterations of the Consumer Expenditure Survey should help provide clarity in this murky area of economic measurement.

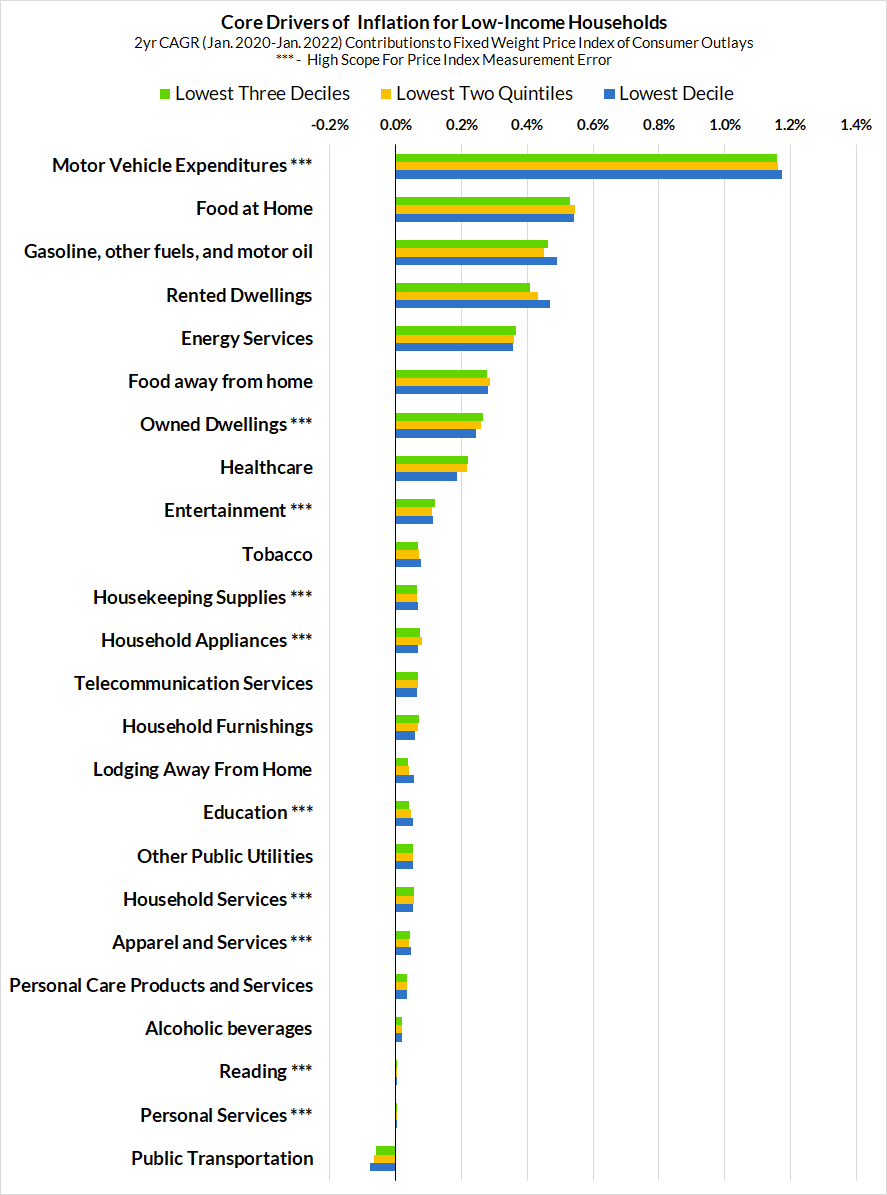

When we look at the composition of this higher measured inflation for low-income households, we see the same few categories mentioned above: food, energy and rent.

When viewed as a spread between the highest and lowest groups of income deciles, food and energy are the main drivers of why lower income households are facing a disproportionate inflationary burden currently. Food and energy prices are precisely the set of prices that the Fed systematically seeks to “look through” both because of their volatility and because of the Fed’s limited ability to influence these prices. Food is less volatile and less sensitive to global commodity prices than energy but the local variation in both sets of prices have substantial proximity to global supply, overseas demand, and geopolitical risk dynamics. One can quibble about the appropriate scope of exclusion from inflation, but from the lens of causality and noise-filtering, it is sensible for the Fed to strip out such price changes from their preferred real-time measures of inflation.

If the goal of restraining inflation is to improve the lot of low-income Americans, weakening the labor market is quite a perverse mechanism. The dislike for inflation – especially for highly visible or necessary goods and services – is understandable. No one likes paying more for things. However, interest rate policy primarily works to lower inflation by cooling off the labor market first and foremost. Interest rate hikes may have a role to play in restraining inflation, but that role should not be presented as one which also straightforwardly improves the well-being of the poorest Americans. The Fed has a mandate for price stability, but we shouldn't fool ourselves into thinking that disinflationary rate hikes are making standard of living outcomes more equal.

This does not mean, as some have suggested, that inflation is not a serious issue. Lower-income households likely have come out ahead – after accounting for transfers and wage compression dynamics – yet that fact is understandably obscured by the uncertainty created by higher price volatility in staple goods and services. As mentioned before, these goods make up a larger proportion of household budgets the further down the income scale one goes.

It only becomes more important to take inflation seriously when we are thinking through the kinds of policies required for the US economy to run at or near full employment. To ensure the political sustainability of tight labor markets, there must be better policy tools for addressing price pressures among the kinds of high-salience necessities. The Fed and the rest of the administrative state currently have limited discretionary policy tools capable of ensuring that supply and demand dynamics remain reasonably balanced both over the short- and the longer run. The compromise that has characterized the post-2008 policy environment – permanently low demand, low investment, and slow wage growth – should not be seen as viable or somehow welfare-maximizing either. As we saw during the pandemic, this approach has left our economy lacking resilience to a wide array of supply chain shocks and vulnerabilities, all while keeping a generation of Americans out of employment, particularly within communities that are more economically marginalized.

The Fed has a legislated mandate that spans stable prices and, for that reason alone, inflation must be encompassed in any Fed framework. But if the goal is to fight inflation with a view towards improving the living standards of low-income and marginalized Americans, we are going to need to develop better tools than interest rate hikes.