Labor Market Recap December 2022: Last Month’s High Earnings Were Wrong

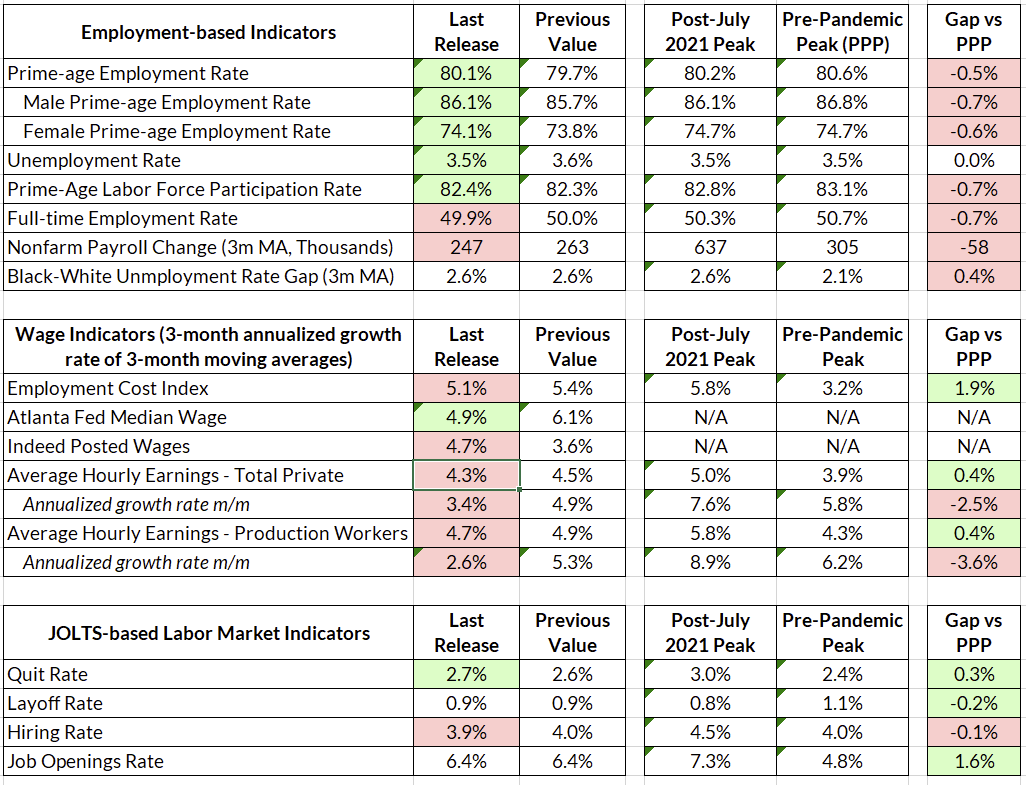

New data from December shows a labor market that remains strong all-around even as wages have begun to decelerate. The unemployment rate ticked down from 3.6% to 3.5%, while prime-age employment increased from 79.7% to 80.1%. The establishment survey continued to show growing employment, but at a slower rate, with business reporting 247,000 workers added in December.

Many economists and policymakers have focused on average hourly earnings, the growth rate of which was 3.4% (annualized) in December, since the Fed’s anti-inflation mission is now centered on the role of higher wages in elevated core services ex-housing inflation. As we stressed last month, and in our post about the Indeed Wage Tracker, many have placed too much weight on initial average hourly earnings reports, which are often subject to substantial revisions. Relying exclusively on this metric risks creating an unreliable narrative about the trajectory of wage growth.

In fact, the biggest news is not actually the softer wage data from the most recent month, but rather the revisions to previous months. As we suspected, last month’s hot wage growth was indeed a fluke. The annualized growth rate of average hourly earnings in November 2022 were revised downwards significantly from 6.8% to 4.9% for all workers, and from 8.5% to 5.3% for production workers in particular. Average hourly earnings are now clearly on a downward trend.

The December data tell a clear story: it’s time for the Fed to back down to 25 basis points at the February meeting. Even as employment remains strong, wage growth shows signs of decelerating. It doesn’t look like they need to break the labor market to tame inflation.

The Fed will be happy to see that average hourly earnings came in soft this month, at a 3.4% annualized monthly growth rate. The real story, however, is in the revisions to previous months. With every release of the monthly average hourly earnings data, there is always a reason to say “this is just one month in a noisy series, let’s wait.” However, because survey collection rates for the past three months rebounded from an exceptionally sparse November report, we learned much more information in the release: average hourly earnings growth wasn’t just decelerating in December but also substantially revised downward in October and November.

At this point, average hourly earnings have been on a downward, albeit bumpy, trajectory since July 2022. It’s clear that Powell is paying attention to this report:

If you look at wages, look at the average hourly earnings number we got with the last payrolls report, you don’t really see much progress in terms of average hourly earnings coming down. Now, there may be composition effects and other effects in that. So we don’t put too much weight on any one report. These things can be volatile month to month.

Jay Powell, December 14th, 2022

Powell, now you have your “progress,” and it’s been sustained for several months at this point.

A recurring theme in Jay Powell’s statements throughout 2022 was that the Fed wants to see wage growth fall to a point “consistent with” 2% inflation. The focus on wages has intensified as the Fed has turned its focus to inflation in the core services ex-housing category. In a speech at Brookings in November, Powell expressed concern that high nominal wage growth would lead to higher costs, and therefore prices, in these services.

Because wages make up the largest cost in delivering these services, the labor market holds the key to understanding inflation in this category.

Jay Powell, November 30th, 2022

While we agree with Powell that the Fed’s tools operate on inflation primarily through the labor market, we have a very different view on how that works. The primary reason why the labor market matters for inflation is not wages alone, but rather gross labor income, which is a combination of both employment and wages.

Gross labor income growth has been decelerating since early 2022. This is also around the same time that market rents began decelerating, which makes sense as rents are typically paid out of labor income flows and not financed. This was true even as wage growth continued to accelerate, because employment growth, which was nearing its pre-pandemic levels, had started to slow.

Over the course of 2022, prime-age employment growth fell and is now at essentially zero or slightly falling. The slowdown in employment growth is, itself, disinflationary because of its impact on labor income and demand. The sustained decline in growth in average hourly earnings portends a slowdown in 2022 Q4 ECI, but even if ECI moves sideways, the stagnation and fall in employment levels should reduce the growth rate of GLI by 1.5 percentage points in 2022 Q4 relative to 2022 Q3.

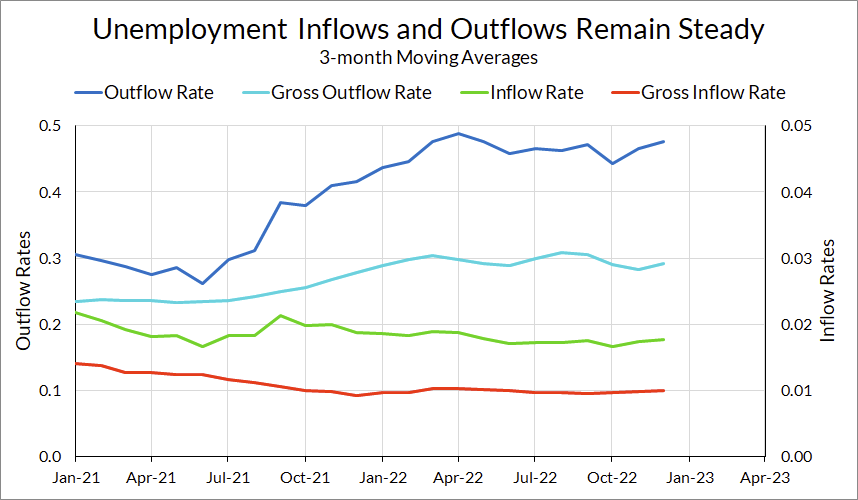

Like last month, we are keeping an eye on labor market flows. Fortunately, we have three ways of assessing labor market flows (see last month’s post for details). First, the household survey shows unemployment inflows holding steady. Meanwhile, unemployment outflows continued a slight upward trend over the past few months.

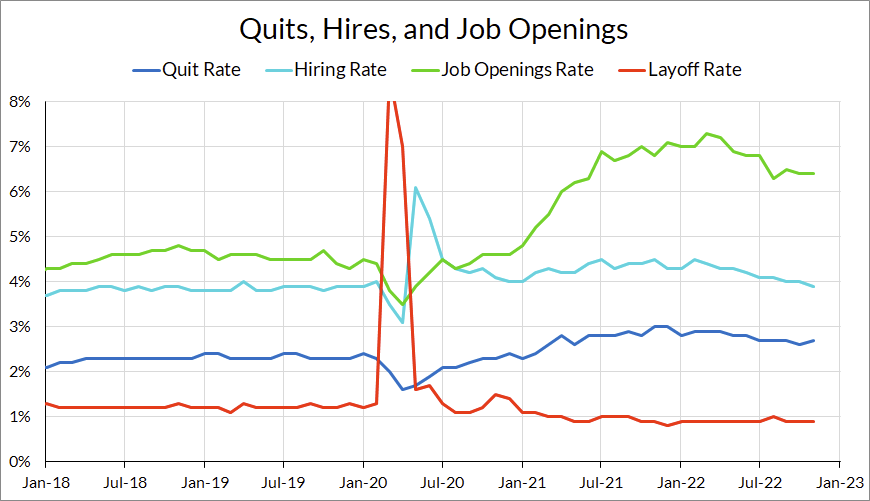

The JOLTS shows a similar story, although the hiring rate in JOLTS has been falling much more reliably than the unemployment outflows in the household survey. The hiring rate, at 3.9%, is now below its pre-pandemic highs.

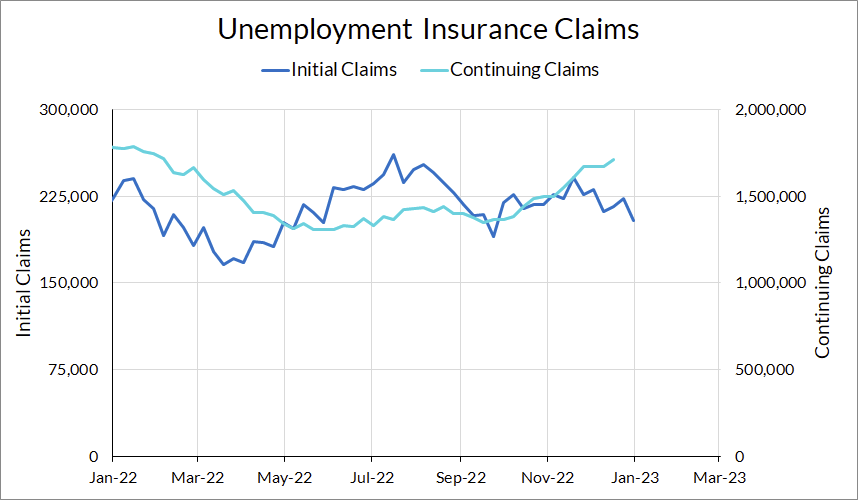

Finally, there is the evidence from the unemployment claims data. Initial claims—which should be indicative of people being laid off—fell over December, while continuing claims—which are indicative of people getting hired out of unemployment—continued to climb.

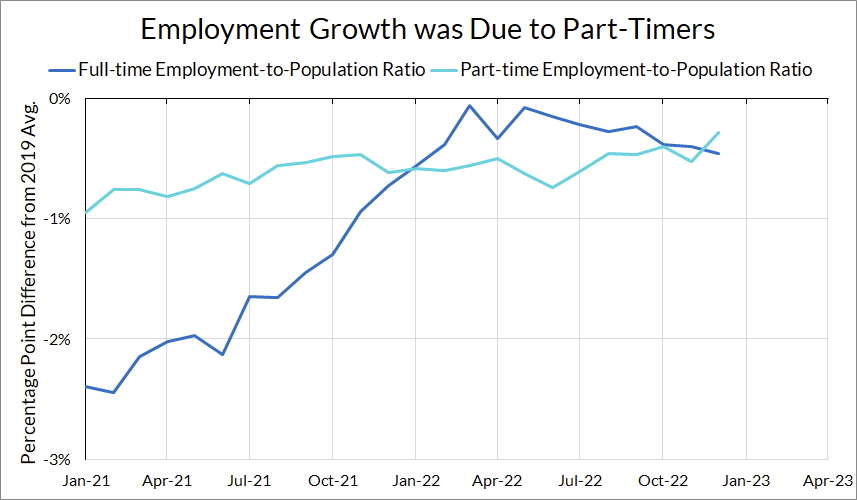

If there is one cloud in this otherwise bright day, it is that the increase in employment in the household survey appears to be entirely due to an increase in part-time employment. Full-time employment actually fell slightly, continuing the gradual decline we’ve seen since May 2022.

That increase in part-time work also appears to be matched by a similar uptick in the fraction of the population reporting that they are working part-time for economic reasons.

I don’t want to be alarmist, as the increase in this figure is well within the normal range of month-to-month variation. We’ve yet to see a sustained increase in this figure, which happens at the beginning of recessions. However, it should shade down one’s evaluation of the headline increase in employment this month.

The December 2022 data continues the trend we’ve seen over the past few months. While the month-to-month data is somewhat bumpy, the trend over the last half of 2022 is clear: the labor market has remained strong, with utilization levels high even as wages decelerate towards more normal growth rates.

However, the full effects of Fed policy have yet to hit, and the major question in 2023 will be whether or not the Fed will succeed in breaking the labor market when it’s not necessary. So far, the signs have not materialized—let’s hope it stays that way.