The Indeed Wage Tracker Shows Wage Deceleration. The Fed Should Pay Attention.

The Fed says that the labor market needs to cool in order to bring inflation down. A key part of the case for maintaining the current pace of rate hikes is built on high measures of wage growth. Jay Powell cited the last average hourly earnings figure as one sign that the labor market isn’t cooling fast enough, arguing that higher labor costs will feed into inflation. This is an important time for the Fed to be looking at the right measures of wages.

Indeed recently released a new measure of wages in the US, the Indeed Wage Tracker (IWT). Unlike most wage measures, which track wages paid to workers currently holding jobs, the IWT tracks wages and salaries advertised in job postings on Indeed. This wage measure provides a timely indicator of wage growth that accounts for composition issues and is highly relevant for thinking about the labor costs that firms face. Moreover, the strengths of the IWT highlight the flaws of other wage measures which tend to dominate the headlines.

More details about the methodology are available at Indeed, but in a nutshell, Indeed calculates the growth rate of median wages advertised in job postings (defined by title, region, and salary type), and reports the median of those growth rates. This methodology ensures that the IWT is less susceptible to the composition bias which taints wage measures like average hourly earnings. The use of advertised wages also means the measure is not thrown around by spurious movements in hours, which can affect crude measures of average hourly wages or earnings (which are calculated by dividing compensation by hours).

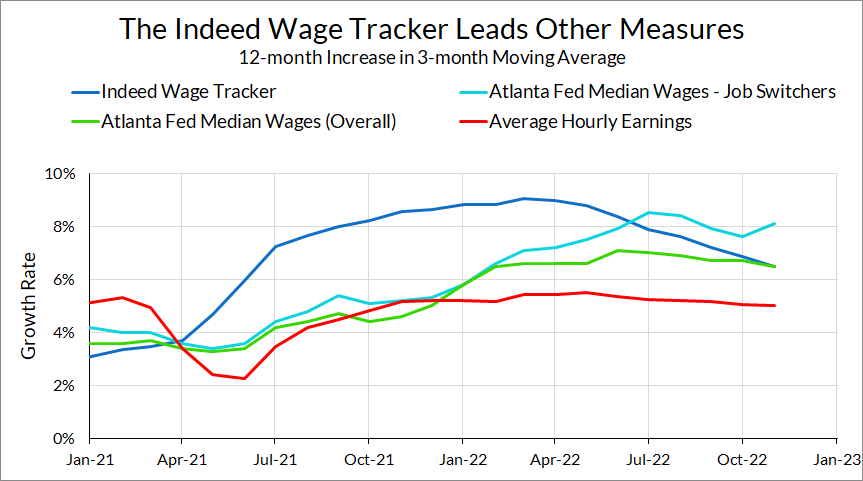

The IWT shows that the growth rate of advertised wages has been falling throughout 2022. In November the 3-month average of year-on-year-growth in posted wages was 6.5%, down from its peak of 9.0% in March, 2022 (the same month prime-age employment rates returned to 80.0% and leveled off).

Earlier on during the recovery, the increase in nominal wage growth rates showed up in the IWT before it showed up in other measures. This is a similar phenomenon to the recent trends in rental inflation, where market rents have been falling and portend a fall in measured rental inflation over the coming months. By similar reasoning, the deceleration in posted wages over the past few months suggests that we should see deceleration in traditional wage measures in 2023.

Perhaps more importantly, the IWT is also conceptually more relevant for some questions than measures of average wages. Some, including Jay Powell, have pointed to wages as an important determinant of services inflation because labor makes up a large portion of costs in that sector. For those concerned about wage pass-through into prices, average hourly earnings are the wrong measure of wages to be looking at.

In theory, the marginal cost of a firm is related to the marginal product of labor and the cost of the marginal unit of labor. In that second component, the wage that matters is the marginal wage, not the average wage. That is, the cost of adding an additional worker is more relevant to the firm than the wage paid to already-hired workers.

If labor were transacted in a spot market and wage rates were renegotiated frequently, then average and new hires’ wages might tell you the same thing. But in reality, due to wage rigidity and long-term labor agreements (formalized or otherwise), the wages of existing and newly-hired workers are not generally the same. Average wages and new hires' wages exhibit very different cyclical patterns. If one focuses solely on average wages, in part one is looking at remitted payments on wage agreements (implicit or otherwise) made in the past.

There are some caveats to the IWT, of course. A posted wage on a job forum is not itself a commitment, and the data is representative of the universe of jobs posted on Indeed, not the overall job market. But, it gets a lot of important things right and deserves more attention than other inferior wage measures (a more detailed dive into the good and bad of the methodology of different wage measures will be the subject of a future research report). Monetary policy should be forward-looking, and the IWT is telling us to expect a slowdown to show up in traditional wage measures over the next few months.