February Core-Cast: What February CPI Tells Us About The Fed's PCE Inflation Gauges

Core-Cast is our nowcasting model to track the Fed's preferred inflation gauges before and through their release date. The heatmaps below give a comprehensive view of how inflation components and themes are performing relative to what transpires when inflation is running at 2%. If you are interested in more timely access to this content following the release of data, feel free to reach out to us here to gain access to our Premium Donor distribution.

Most of the Personal Consumption Expenditures (PCE) inflation gauges are sourced from Consumer Price Index (CPI) data, but Producer Price Index (PPI) input data is of increasing relevance, import price index (IPI) data can prove occasionally relevant.

We still have critical data left outstanding for nowcasting the entirety of February PCE (including February PPI tomorrow), but today's CPI reading was quite consistent with what we previewed last Thursday: headline inflation was more neutral while core inflation still surprised to the upside. Lagged price revisions were due to push up Q1 inflation and it has. If there was not a rolling set of bank runs that the Fed had to step in and address, they would want to push for a 50 basis point hike. In light of the broader banking context, the choice is more likely to be between a pause and a 25 basis point hike.

The sectoral composition leans more heavily on reopening-sensitive in-person services and the ongoing "higher for longer" rent CPI dynamic. While there are some silver linings in this release, we still do not see the kind of broad-based goods deflation that would make us more optimistic about goods and services inflation in the near-term. And the coming rise of used cars inflation adds upside risk to March and April inflation releases. The Fed's claim that the labor market is at the root of services inflation is also not aging well; the labor market is cooling on most wage and wage-relevant statistics but it has yet to show up meaningfully in service prices.

For those interested in a deeper knowledge of the high-stakes dynamics (see the heatmaps below for how their scale to contribute to PCE):

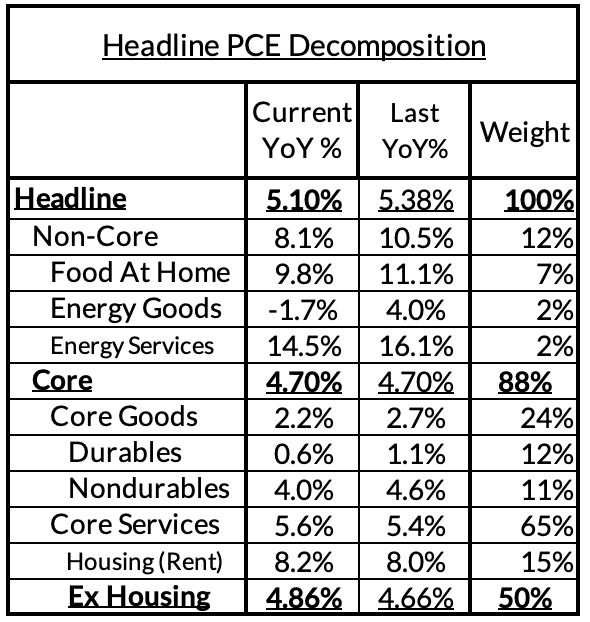

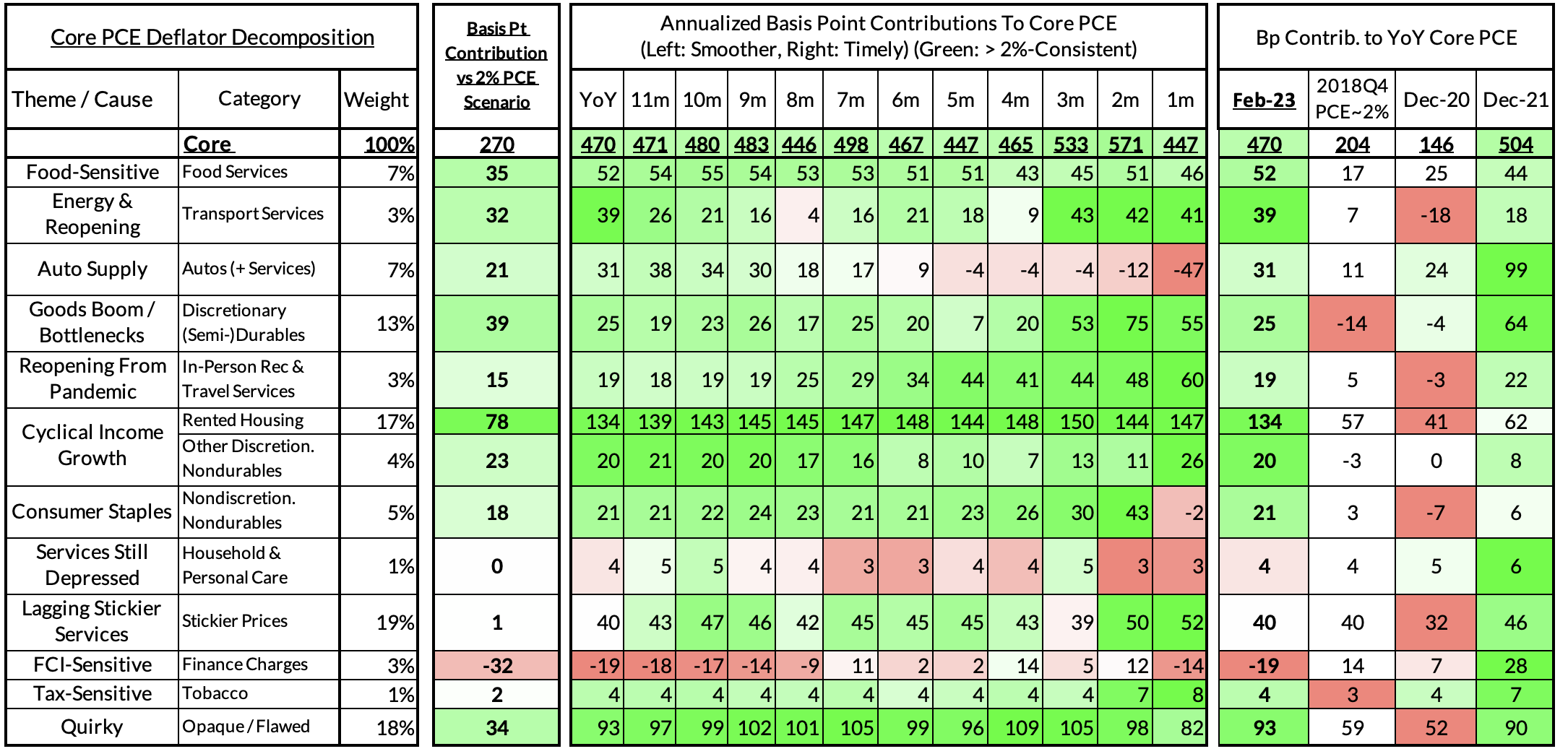

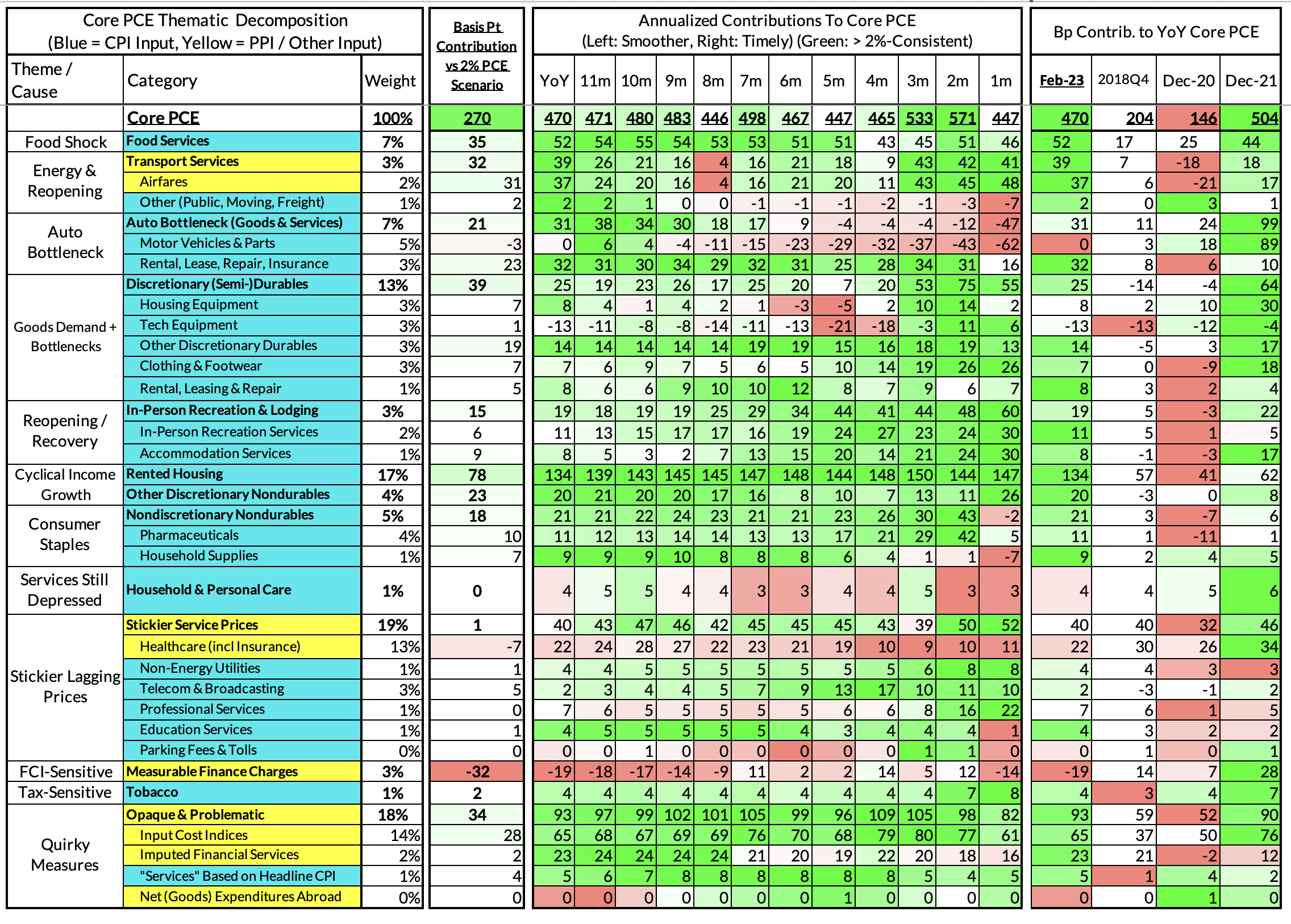

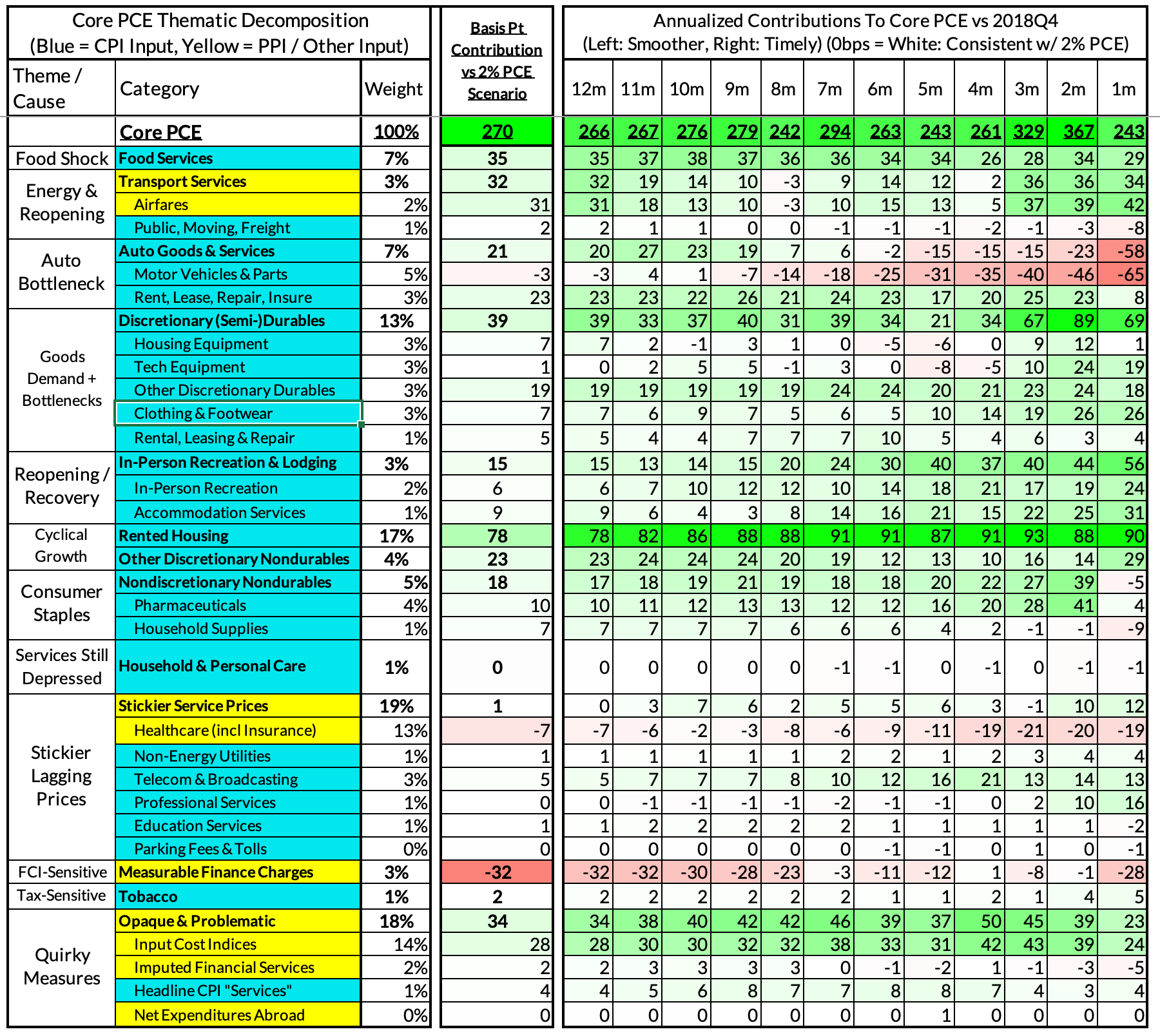

Right now Core PCE (PCE less food products and energy) is running at 4.70%, 270 basis points above the Fed's 2% inflation target for PCE. That overshoot is disproportionately driven by catch-up rent CPI inflation in response to the surge in household formation and market rents in 2021-22.

There are other contributors to the overshoot, some more supply-driven (automobile bottlenecks likely explain 21 basis points, while food inputs likely added 35 basis points to the overshoot) and some more demand-driven (in-person recreation and travel services adding 23 basis points to the overshoot) and some both (airfares are both reopening-sensitive and energy-sensitive, adding 32 basis points to the overshoot).

Looking through the detailed version of our heatmaps, you can get a sense for what's still left to play for: airfares, healthcare services, observed financial services, and a lot of opaque and problematic indices the BEA throws in. The first three are going to be determined by tomorrow's release; given the volatility of airfares, this could become a pronounced impact.

The final heatmap gives you a sense of the overshoot on shorter annualized run-rates. Right now we see February's monthly core PCE on track for a 243 basis point overshoot vs 2% (4.43% annualized growth). This estimate will inevitably shift tomorrow.

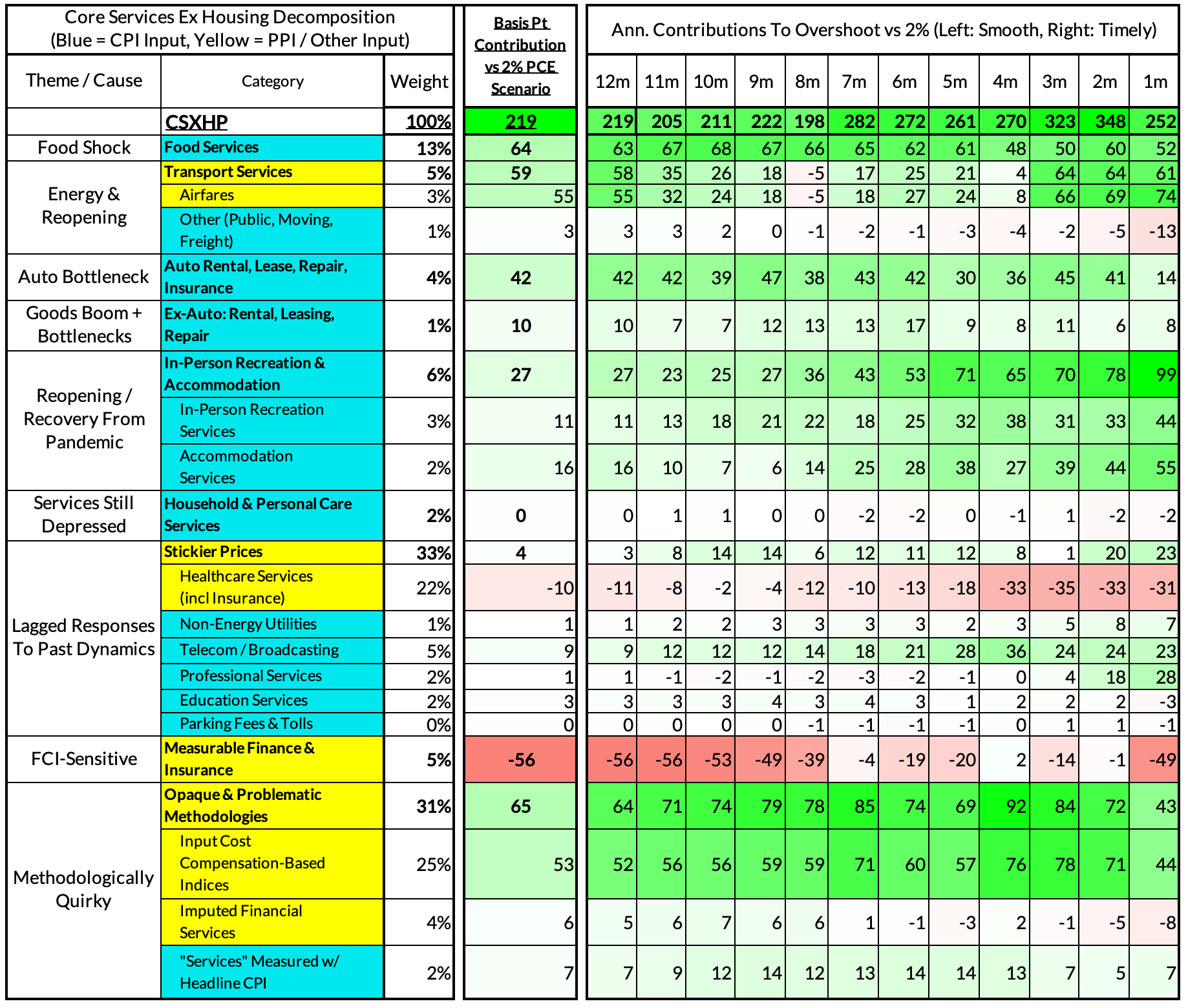

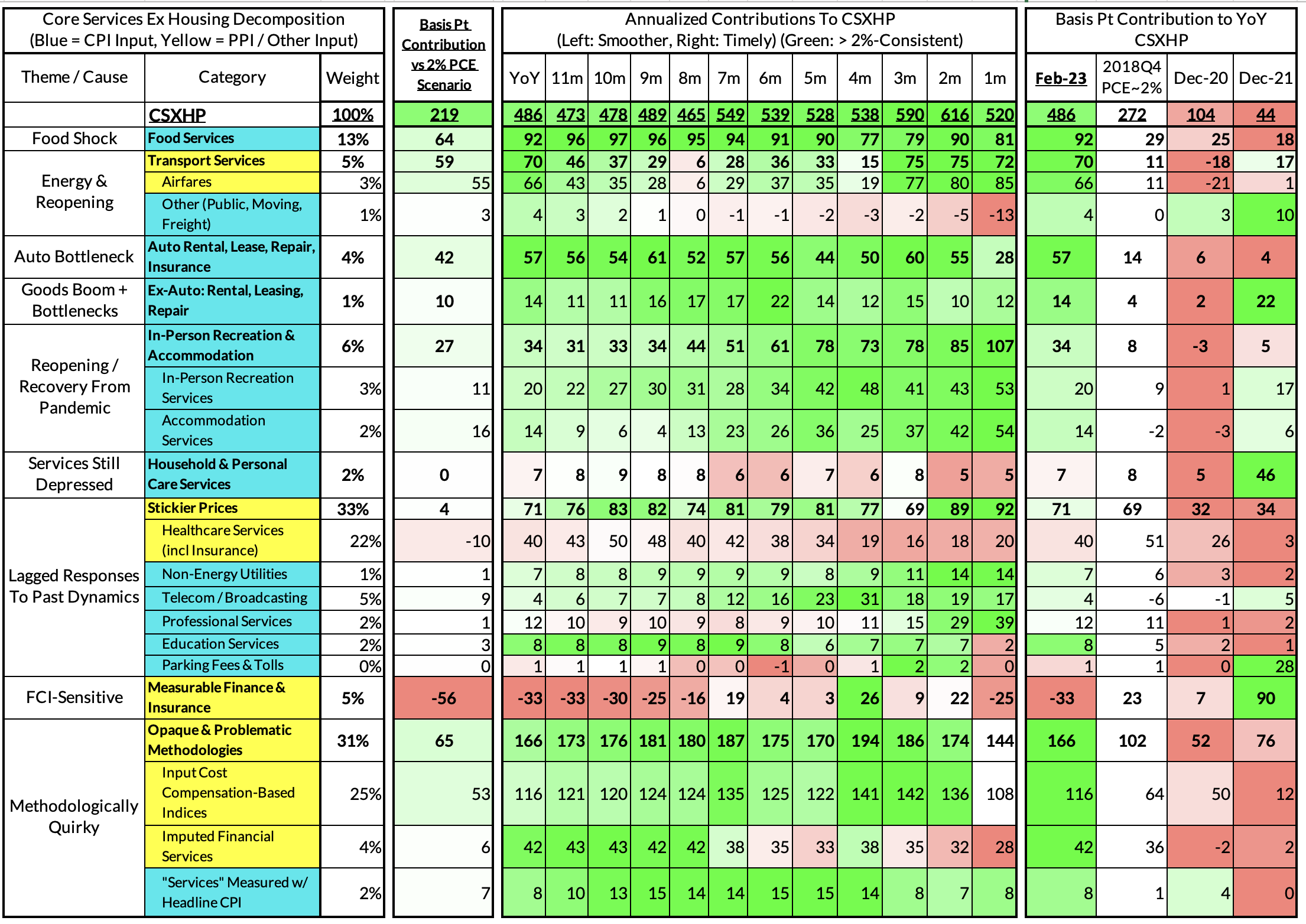

February's growth rate in "Core Services Ex Housing PCE" is on track to run at 4.86%, a 219 basis point overshoot versus the 2.72% run rate in this aggregate that coincided with 2% headline and core PCE.

The fundamental drivers of the overshoot are food services, airfares, motor vehicle services, and the ongoing boom in reopened in-person services. Motor vehicle services are starting to show some signs of abating but this may be a false dawn given the likely rise in used car values over the coming months. Airfares estimates will get updated after tomorrow, while food services should disinflate so long as food disinflation continues to sustain.

As for tomorrow, financial services present some upside risk relative to our nowcast model, and the BEA's opaque input cost indices also have scope to outperform our model.

The monthly reading for Core Services Ex Housing is currently on track to still look hot over Q1 though less so in February relative to January (for the same set of reasons we flagged ahead of time). We do not see the Fed backing off their hawkish inflation posturing if financial conditions and banking conditions recover.