January Inflation Preview - Residual Seasonality & Stickier Services Pose Upside Risks

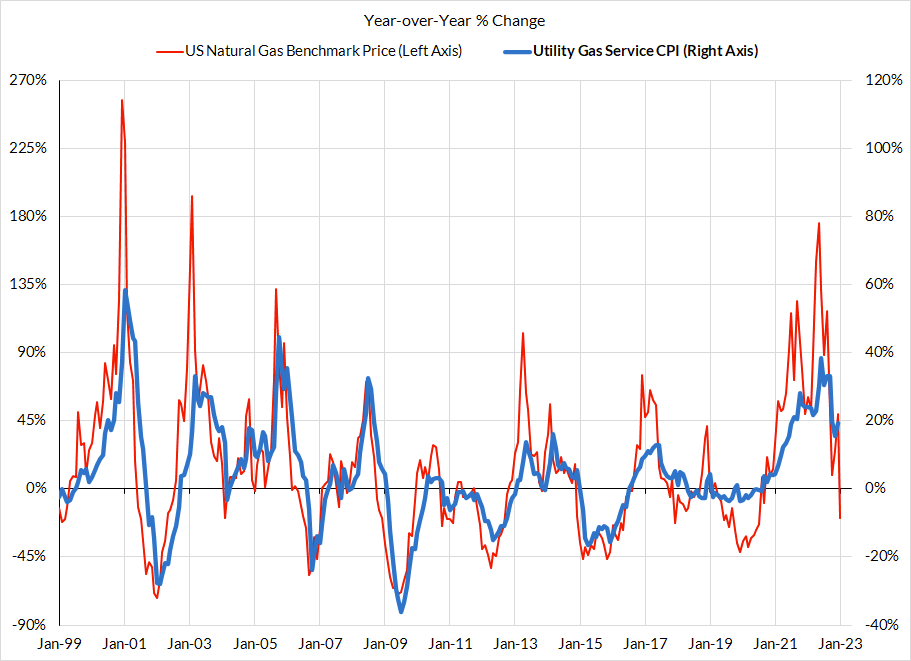

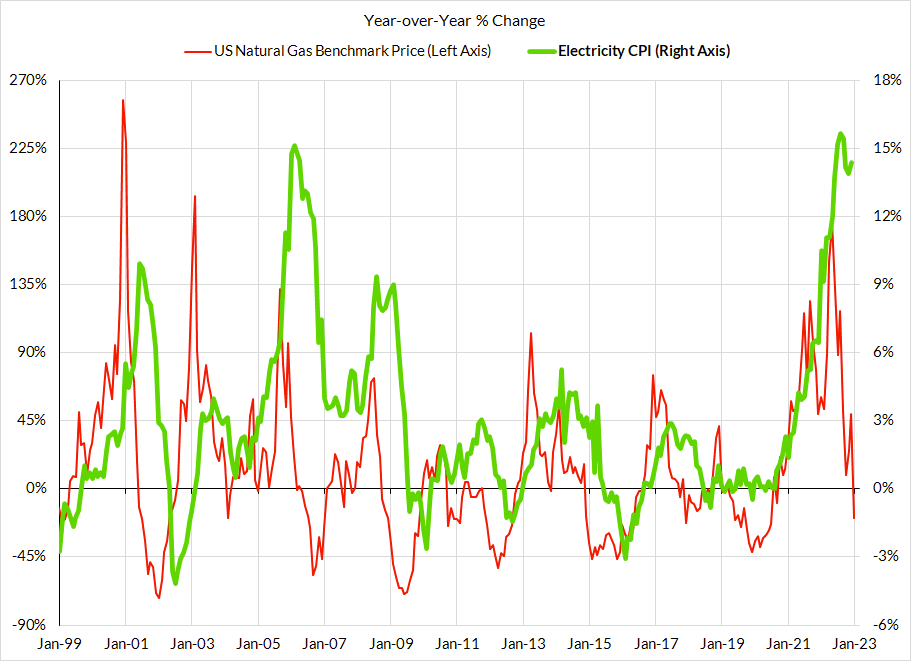

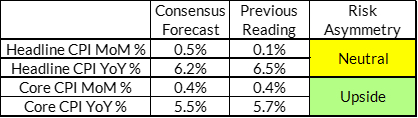

Summary: Relative to consensus forecasts, the risks for January & Q1 core inflation are now asymmetrically tilted to the upside (Jan core CPI ~ 0.4%). While we don't think the causes for upside risk are a sound basis for hawkish panic, the Fed would certainly be vulnerable to such a reaction as a result. As we noted in our February Fed recap, the FOMC clearly views 5-5.25% as a lower bound for the terminal Fed Funds Rate and such an upside surprise would only further cement the Fed's view here. Headline inflation risks are more balanced, thanks to declining benchmark natural gas prices and continued deceleration in food prices.

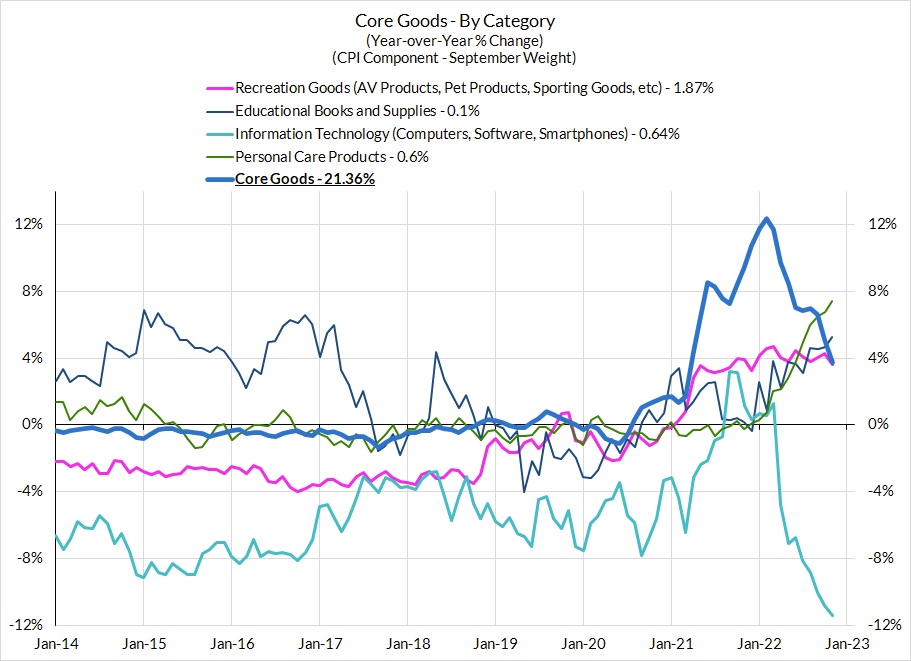

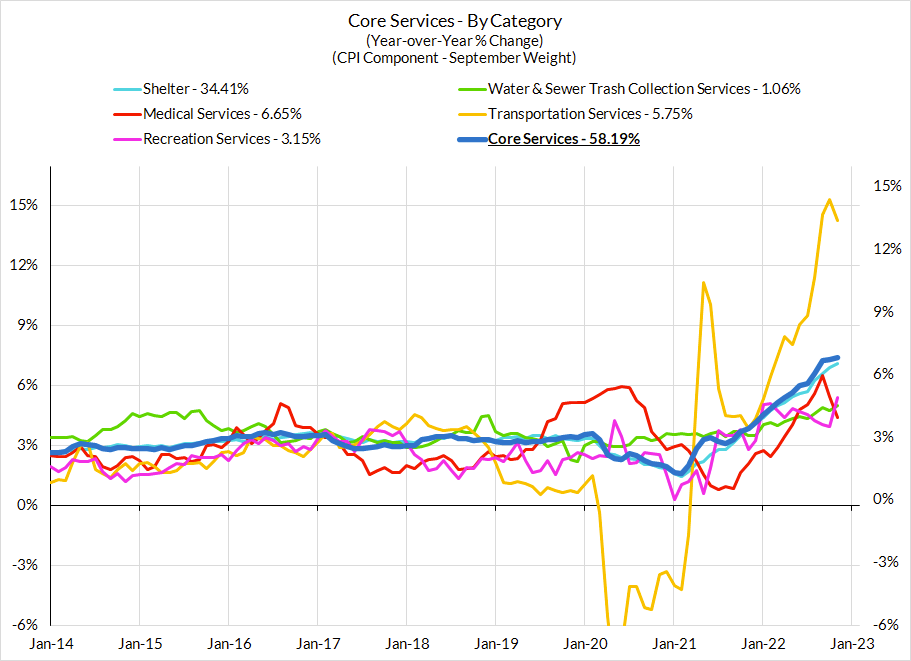

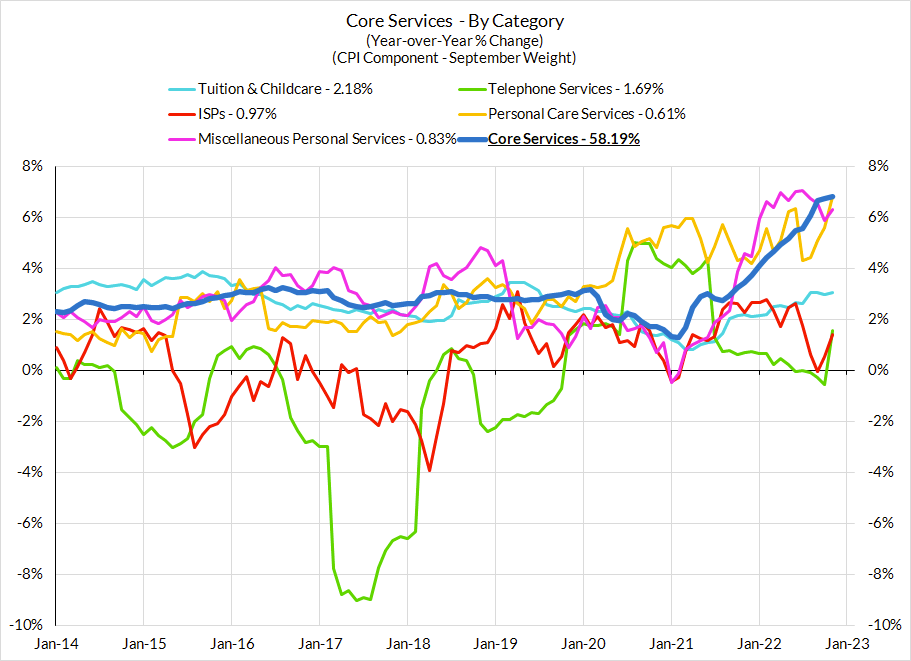

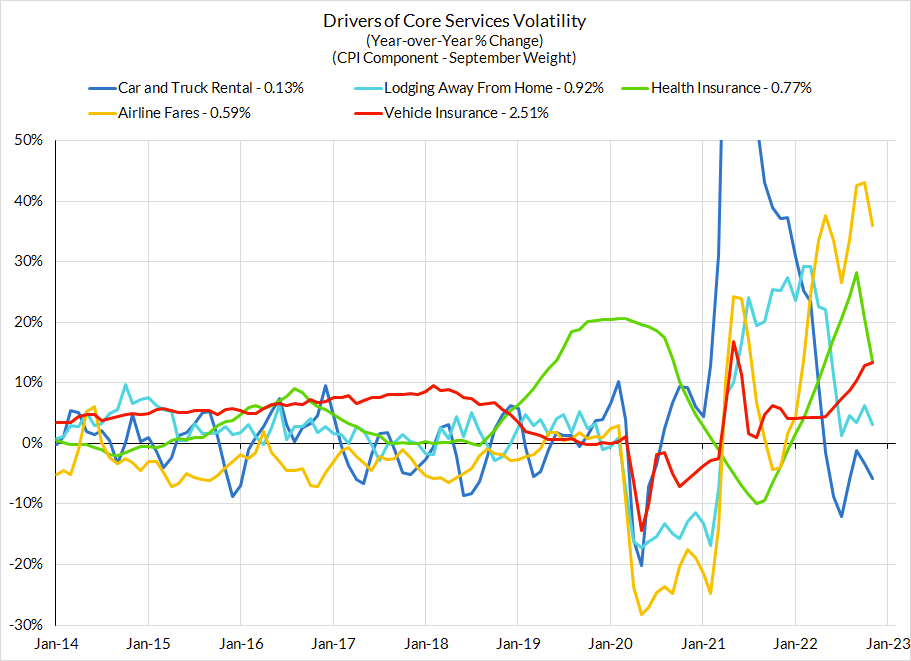

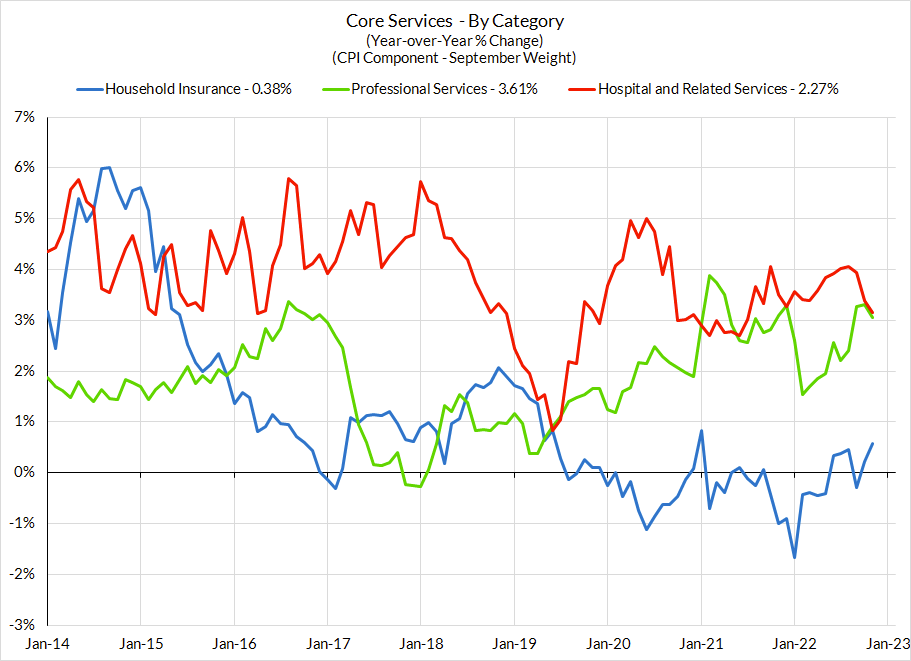

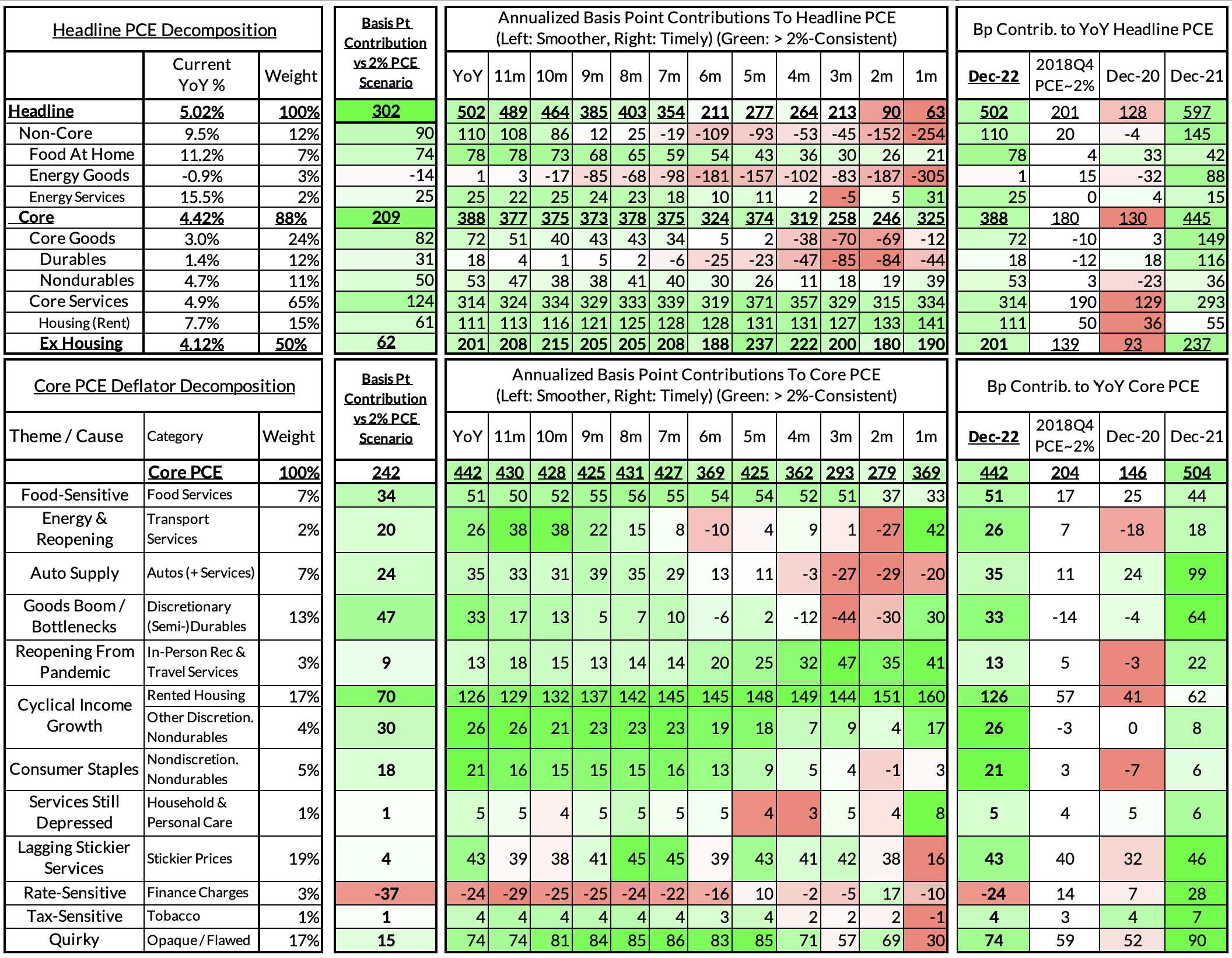

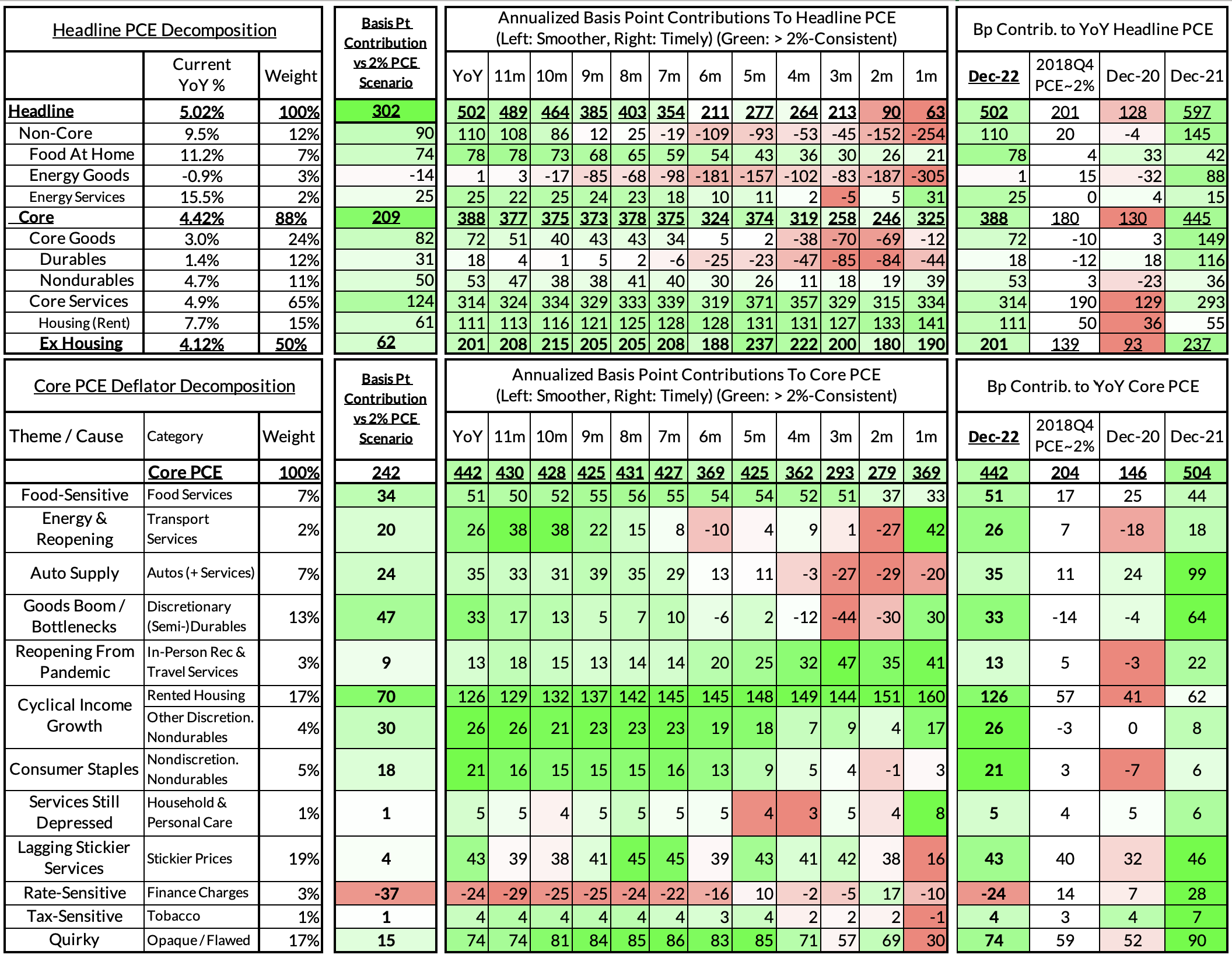

Key Dynamic: January (Q1 generally) is a time when firms with stickier and lagging service prices are more vulnerable to outsized price increases, especially when inflationary pressures were still elevated over the previous year. These upside core inflation risks are more pronounced for PCE than for CPI. The increases this month should still be softer than what we saw in January 2022 (0.7% core CPI increase) and thus result in declining year-over-year inflation readings. Key categories for tracking this view: healthcare services (PPI), non-energy utilities, telecommunications, broadcasting, and professional services.

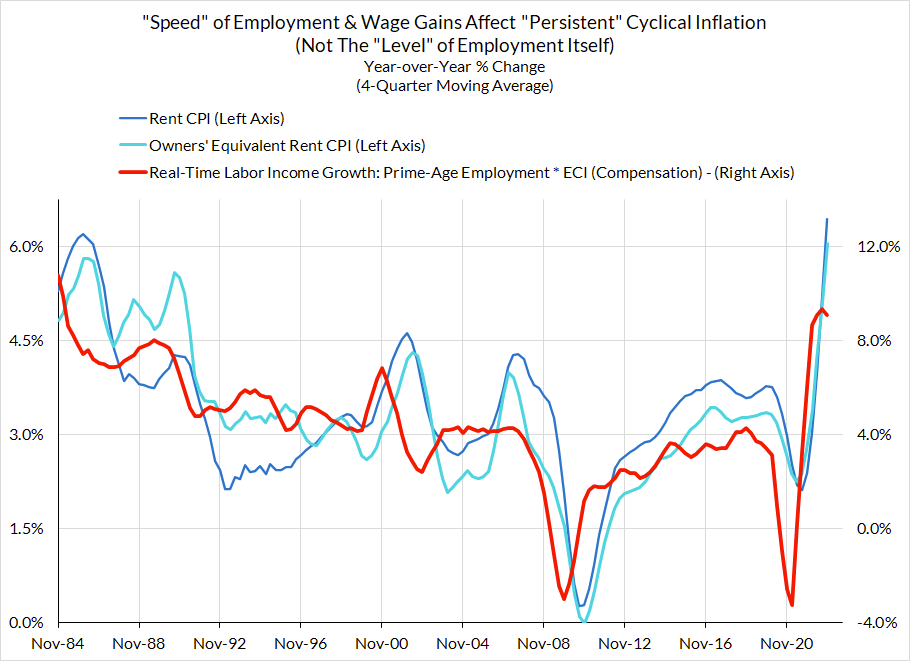

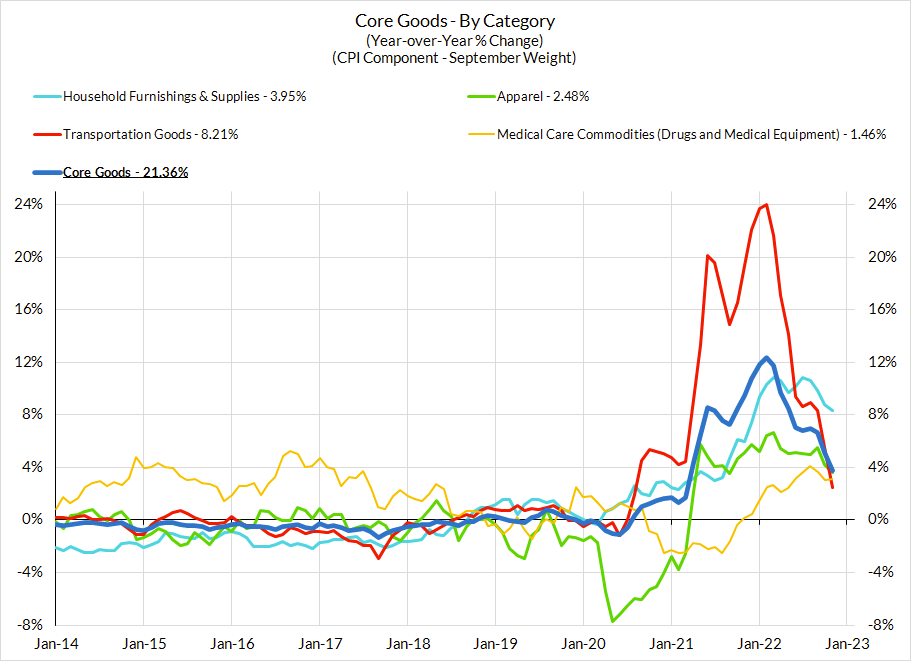

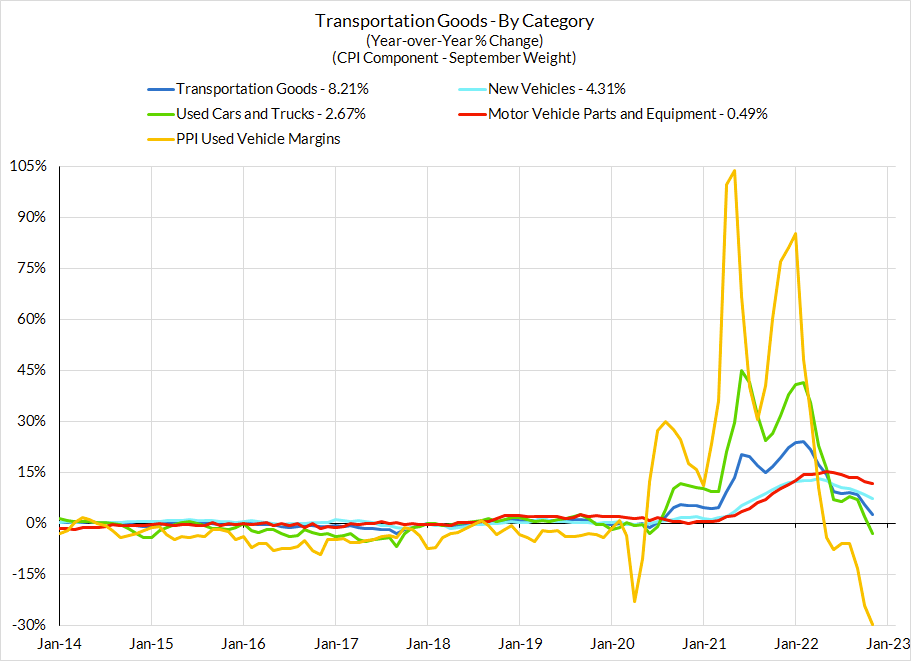

The More Likely Upside Scenario & Its Likely Policy Implications: In addition to stickier service prices, used cars are also likely to be less of a drag on core inflation prints in January than in Q4; they may even prove to be a source of upside in February and March. And while there is much hype about the implications of falling market rents, the CPI methodology involves a lot of smoothing and thus lags substantially; the recent run of rent CPI readings suggest more strength in Q1. Over the coming quarters, we expect slower job growth and wage growth to feed into rental CPI inflation, but that story is not likely to play out imminently.

Despite more signs of wage deceleration and more evidence presented that the Fed's alleged wage-price passthrough claims are weak, the Fed has continued its hawkish posturing. In the presence of upside inflation surprises in Core Services Ex Housing PCE, the Fed is more likely to follow through with expected tightening (2 more hikes) and threaten to go further (potentially hikes in June & July). The biggest concern for us is if this tightening push occurs amidst coincident labor market deterioration; thankfully such deterioration has not transpired as of yet.

The Less Likely Downside Scenario & Its Implications: Our 4-6 quarter outlook is one of substantial disinflation, but here are some plausible disinflationary dynamics that could materialize sooner than we now pencil in:

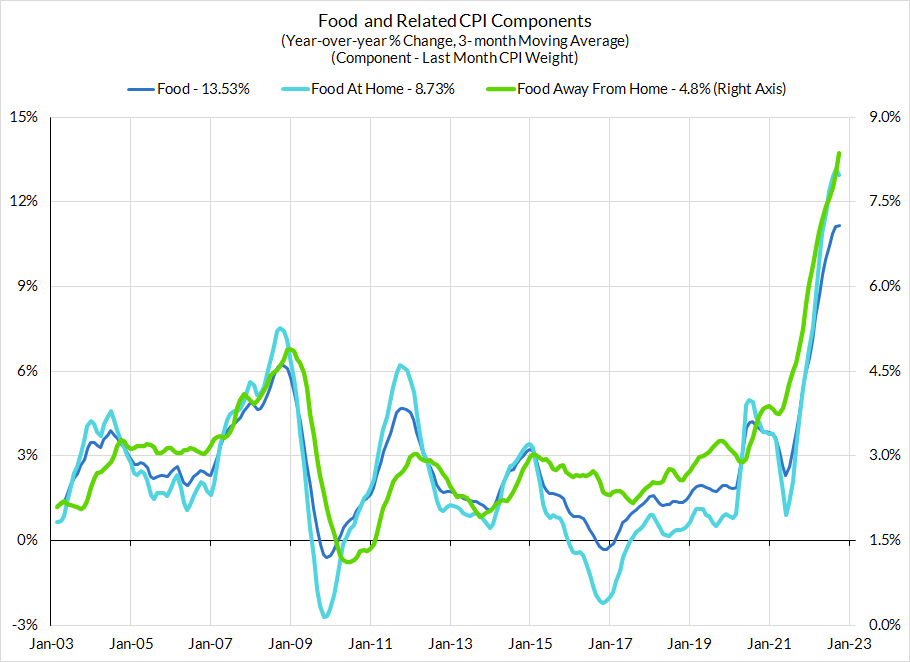

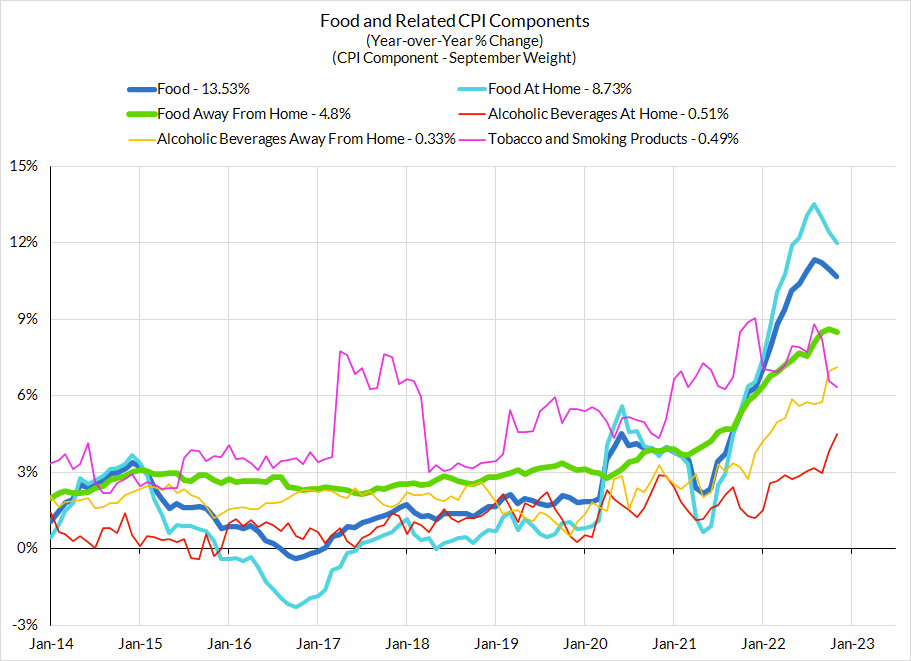

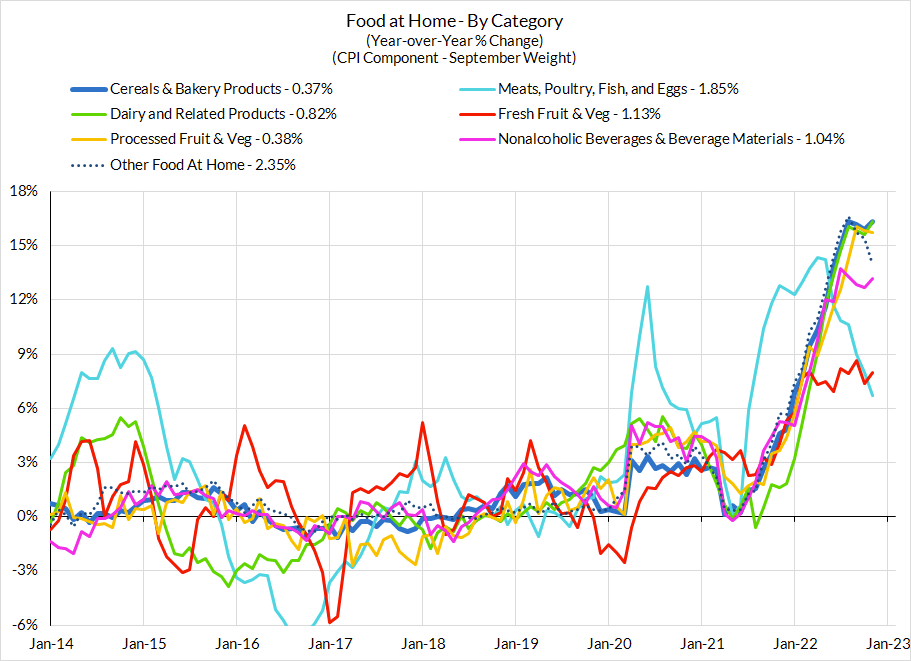

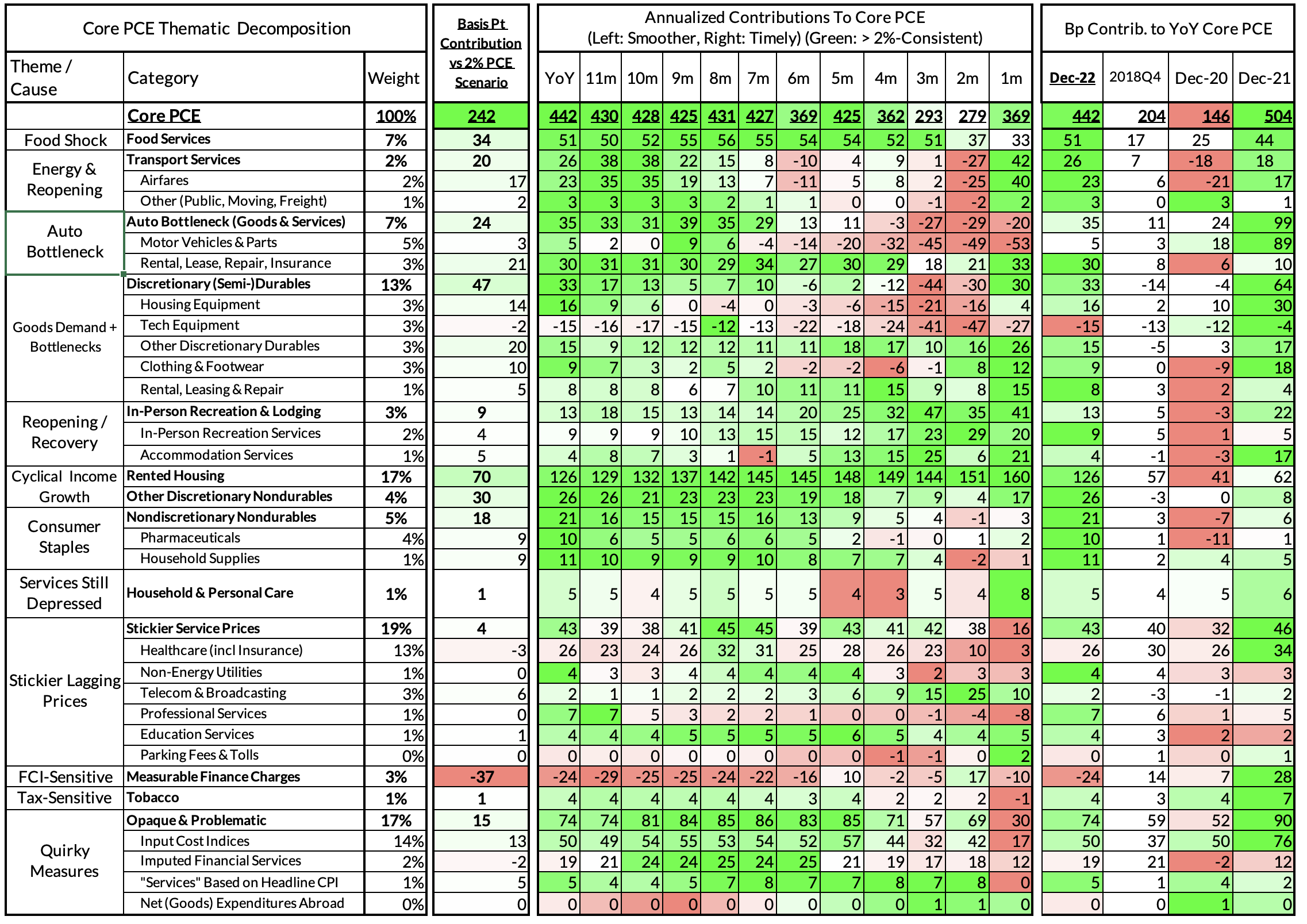

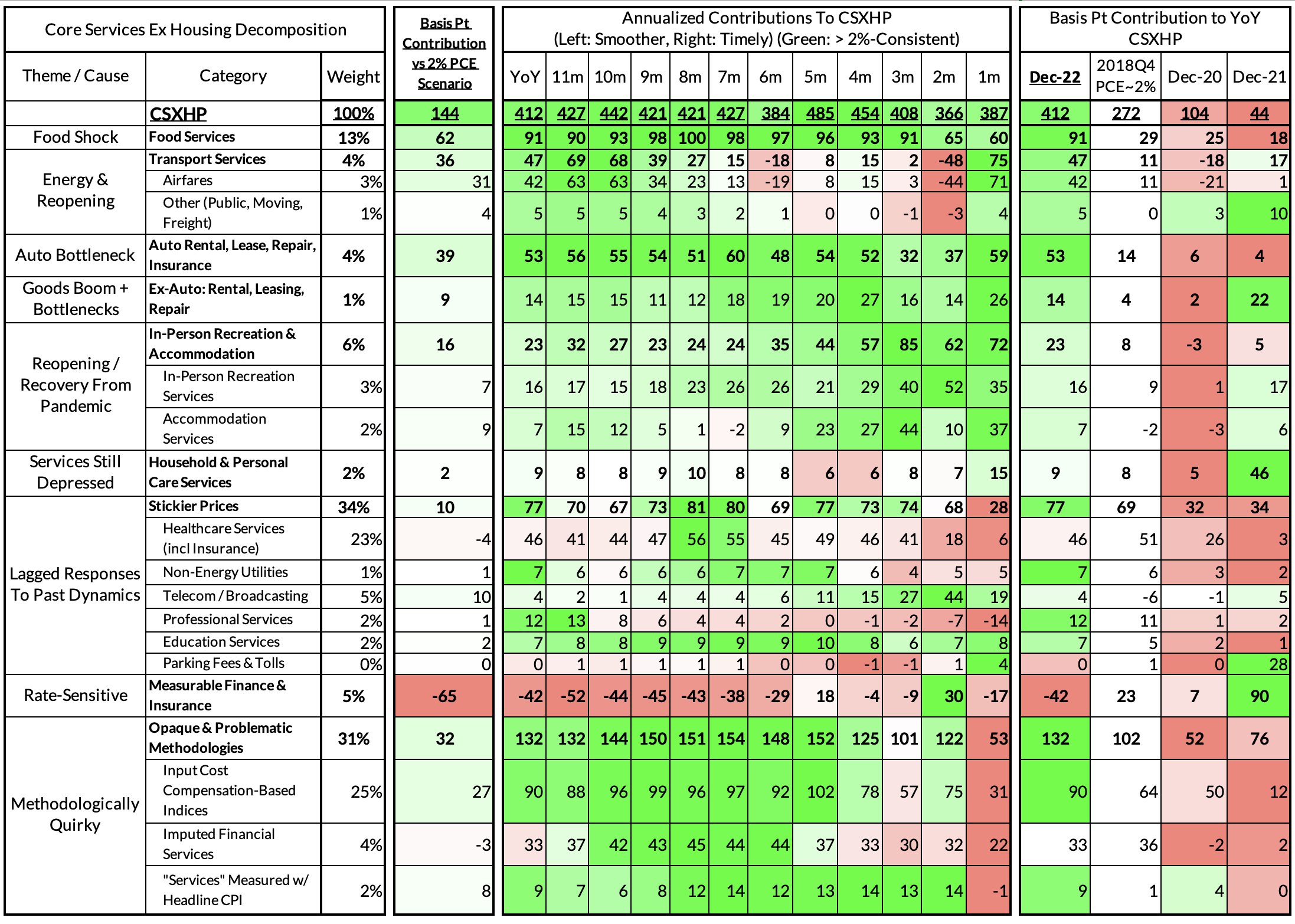

Final Note: Is The Most Important CPI Component To Fed Policy Outside Core CPI? Keen observers will know that food services are not included in core CPI but are included in core PCE. Food services takes even more importance in the Fed's "Core Services Ex Housing PCE" aggregation. But the dirty secret about food service prices is that they are highly connected to "food at home" prices that are excluded from both core CPI and core PCE. If food at home prices continue to decelerate as they have in the past few months, we expect food service prices to follow (with some lag).