A soft landing consensus for CPI? The forecasting consensus is sticking close to its November predictions, with a 0.3% increase expected for core CPI (falling from 6% to 5.7% year-over-year) and -0.1% for headline CPI (falling from 7.1% to 6.5% year-over-year) for December. A print in this range would continue a trend begun in July of last year, where monthly rates of inflation have been – on average – consistent with a 2-3% annualized rate of CPI inflation. However, it will take most of the next six months for year-over-year CPI inflation to clearly reflect that stabilization, owing to the eye-watering prints during last summer’s energy crunch.

We think this downside consensus view is reasonable, and we even see a downside skew in the balance of risks for core inflation in December. But despite this benign expectation, there are more than enough countervailing dynamics that can deliver an upside surprise in the December data. Lags within CPI component methodologies are a substantial source for upside risk. Although many of the price movements may be slowing down more rapidly in real-time data (e.g. apartment rents, used cars), they can take more time to feed into CPI data. Food prices also risk running hot for supply-driven reasons, and have underappreciated spillover effects on "core" measures of inflation.

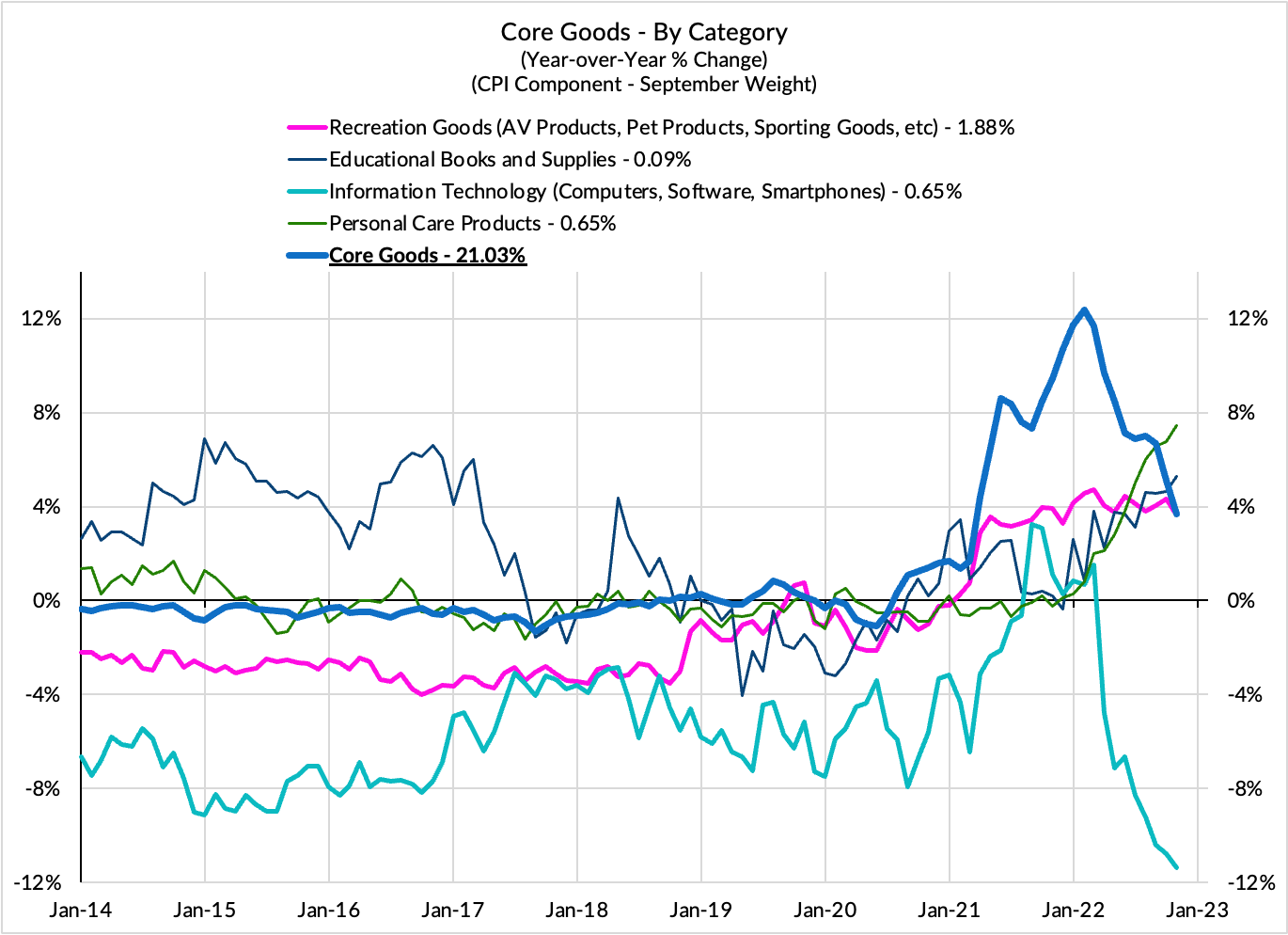

We see downside risks in a wide range of CPI components, as do many other forecasters. The combination of excess inventory due to pandemic over-ordering and usual post-holiday season discounting will likely contribute to disinflationary pressures in a number of markets, especially apparel, household furnishings & supplies, audio, video, and information processing equipment, and other discretionary durable goods.

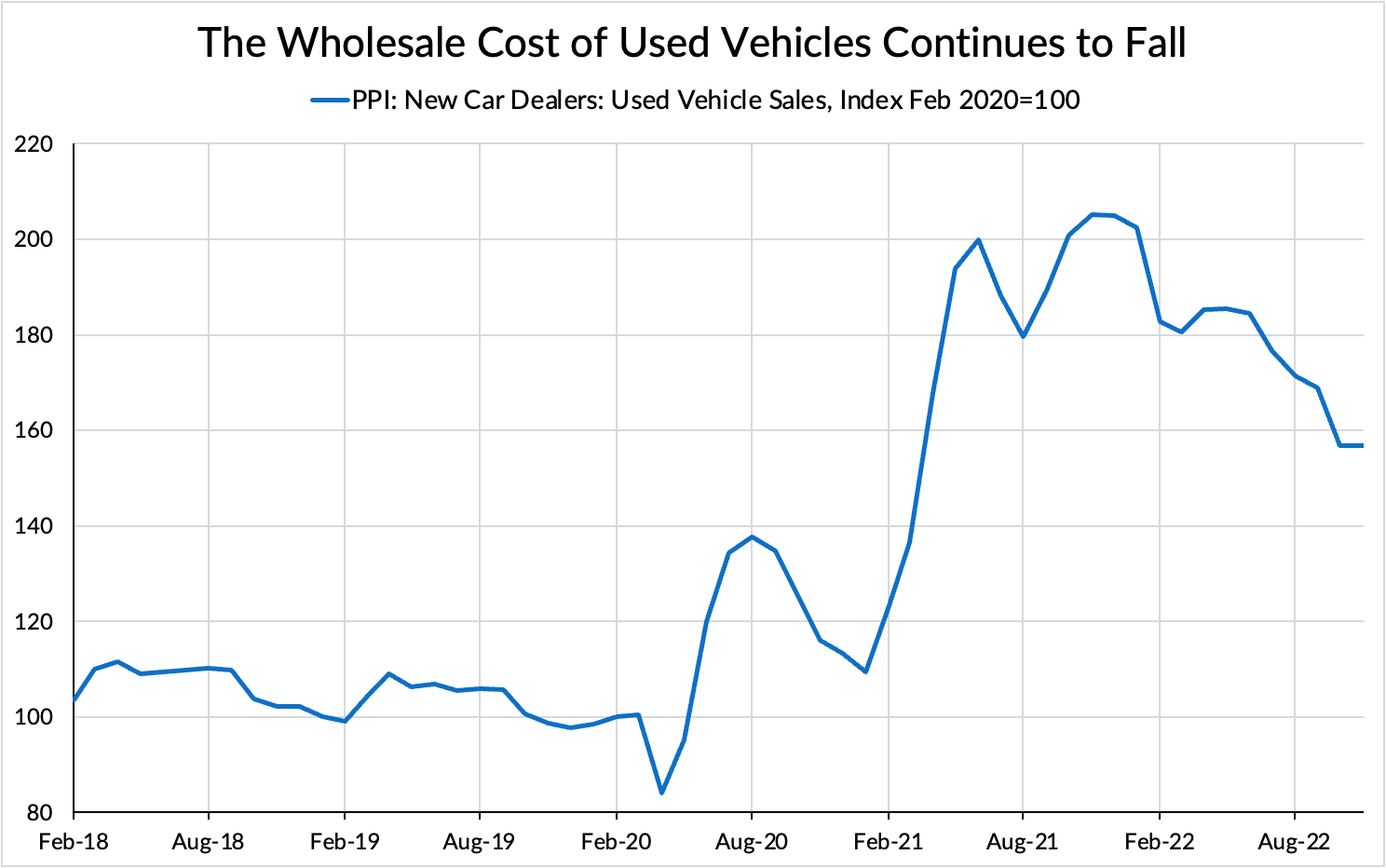

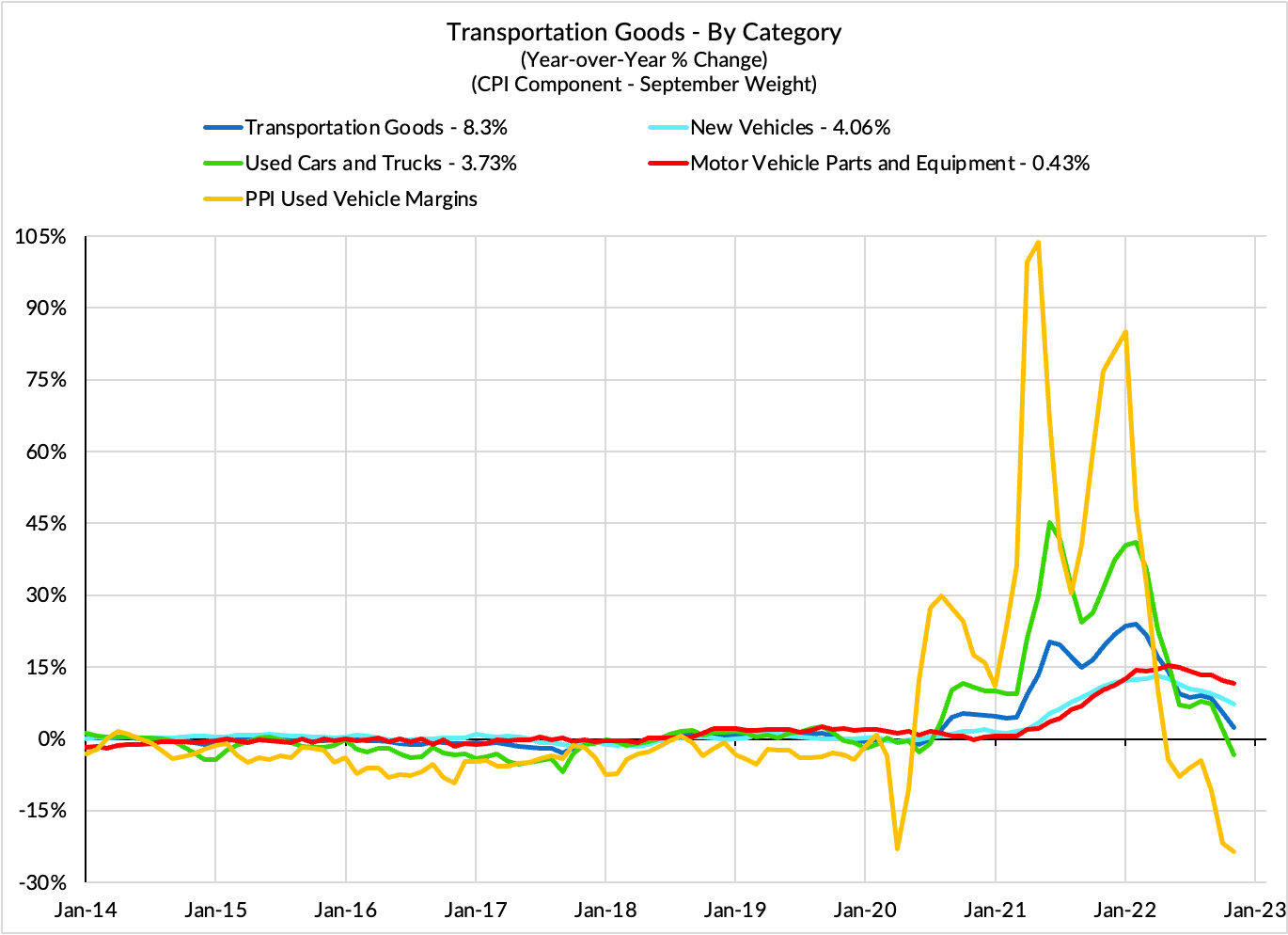

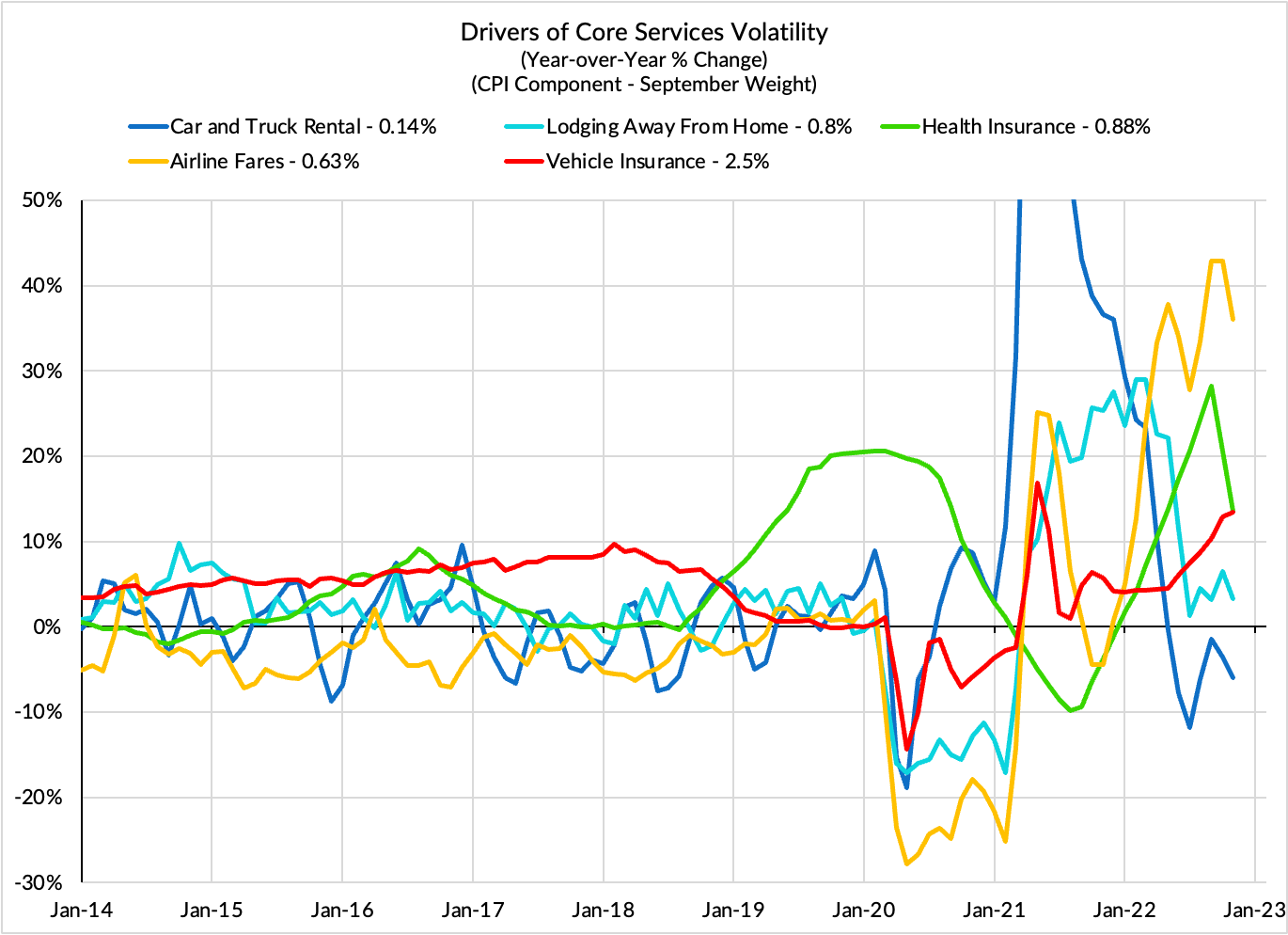

However, all of these dynamics are at least somewhat baked into consensus and there is a chance that the inflation impact of holiday discounting takes more time to fully feed through into CPI. Such an outcome would make a stronger case for price declines in upcoming months given the fundamental reality. Goods and logistics markets are continuing to normalize as supply chain snarls are progressively resolved. This is especially welcome in the automobile components, which has seen substantial declines in high-frequency and wholesale price indicators, but which is taking more time to fully show up in the associated CPI components. Automobile services deceleration should kick in soon as well, as the broader stabilization in international supply chains feeds through to the cost of automobile repair, maintenance, insurance, rental, and leasing.

Health insurance should also provide a substantial drag on headline and core CPI readings (but not PCE), owing to some substantial idiosyncrasies in how the BLS calculates the price of health insurance. As Omair Sharif detailed on this recent episode of Odd Lots, health insurance had been a large and consistent source of inflation upside in 2022. Thanks to the same methodological quirks and some updated data, it should provide noticeable disinflation until October of this year (though marginally less disinflation than what we saw over the previous two months).

Now, all of these dynamics are relatively well-understood and well-predicted. More interesting is the question of how an upside surprise could happen (even though not our base case), and what that upside surprise would mean, based on its source.

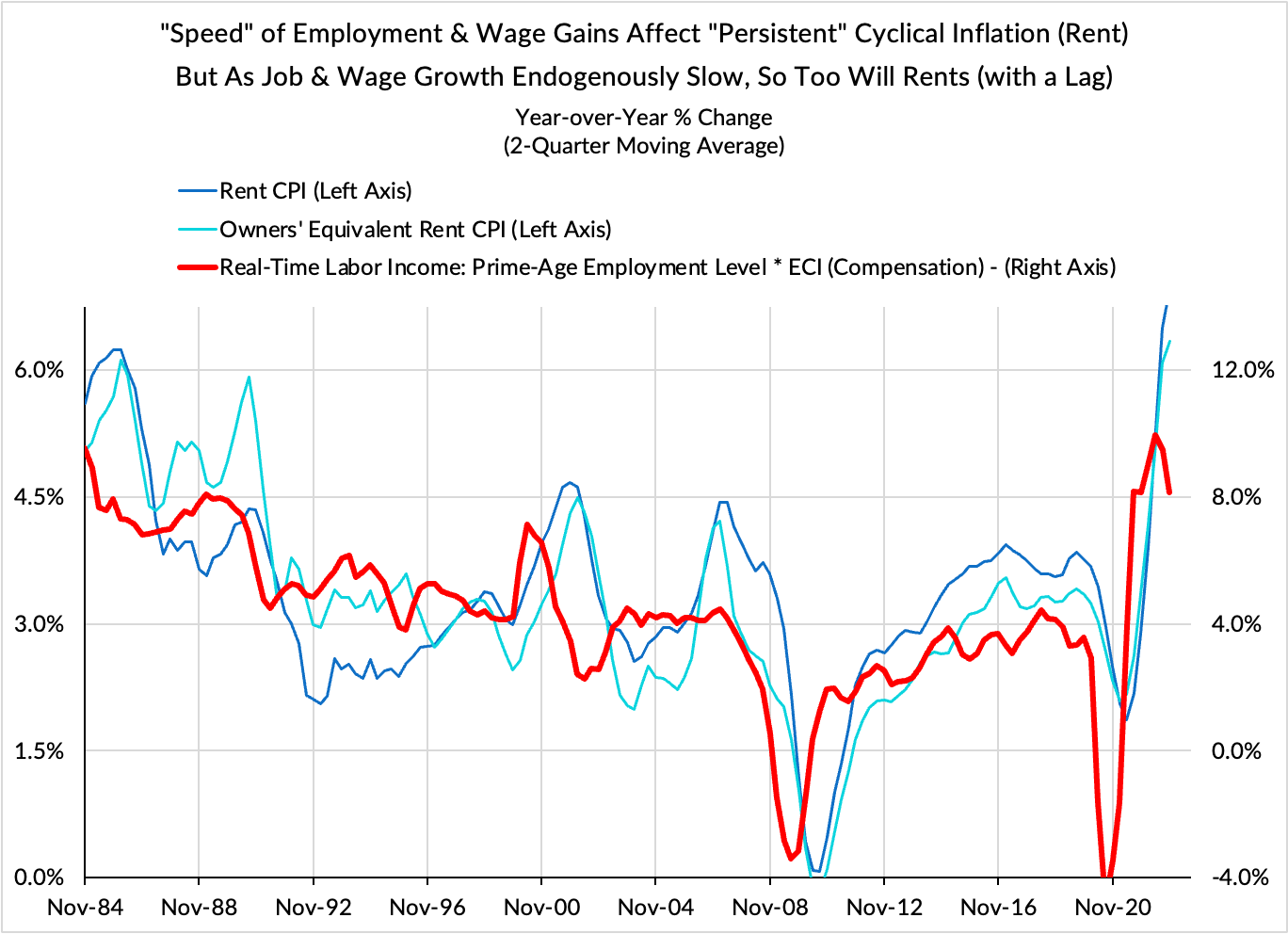

Across-the-board price increases in services tend to follow periods of strong economic growth, but with long and variable lags. In rents, we have long flagged this dynamic with respect to labor income growth. Though wage and employment growth are now decelerating, past gains may still contribute to currently measured rent and OER CPI increases. Certain prices with less exposure to changes in the cost of labor may also update further as we round out the calendar year. Though no one would seriously claim that Netflix prices its subscriptions based on its labor costs, streaming services have seen periodic price increases since the onset of the pandemic. A similar situation can obtain for Cable, Satellite TV and Radio, ISPs, and Telecommunication Services more broadly. In each of these situations, it is not clear that an upside surprise communicates much about the forward path of inflation; it seems better explained as a lagged response to rapidly cyclical recovery in incomes and consumption (which is now endogenously cooling).

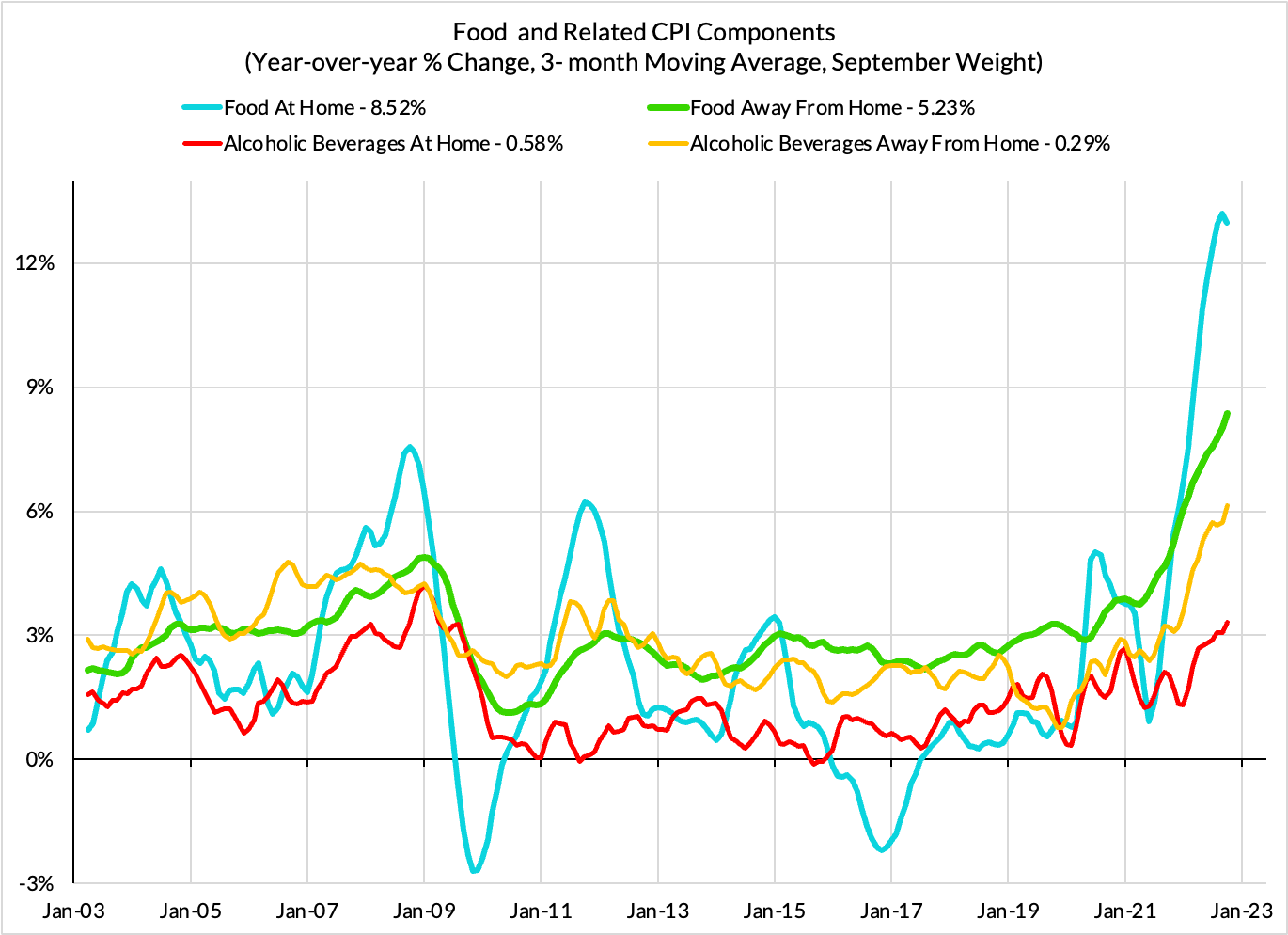

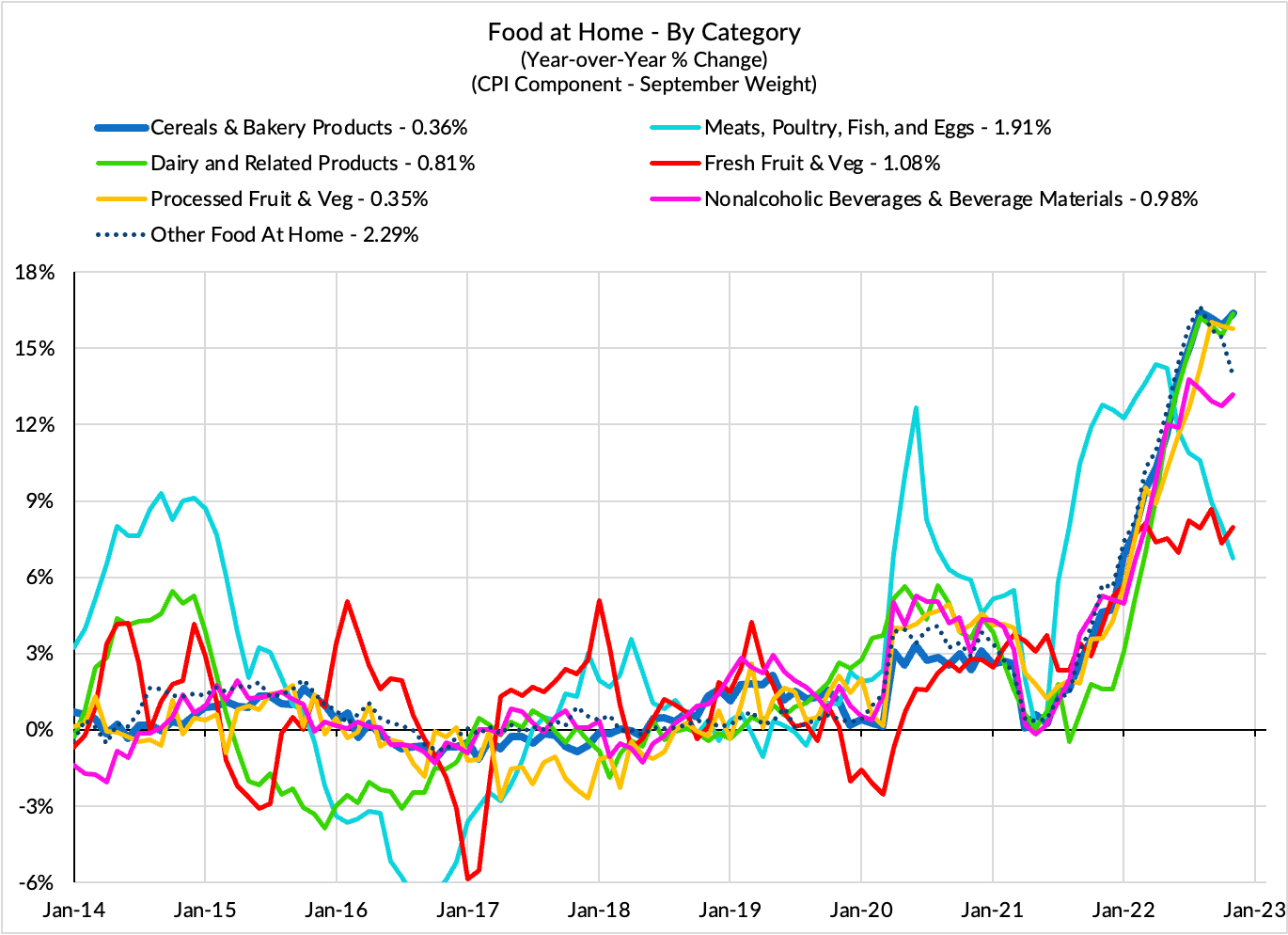

An unexpectedly hot headline CPI print driven by food-adjacent prices is also worth flagging. Food services fall outside of core CPI, but are counted within core PCE. Chair Powell is implicitly hyping up the role of wage growth in food services prices, but empirically, food services is also very sensitive to the same factors shaping grocery store prices (Food At Home). Alcohol, on the other hand, falls outside of core PCE but within core CPI; it also tends to track food price dynamics, but with a lag. Although most food prices slowed their acceleration in the November 2022 CPI, the supply situation for a number of food categories remains fragile, and this alone creates upside risks for prices in December. Just see the effect of the avian flu outbreak on egg prices across the country.

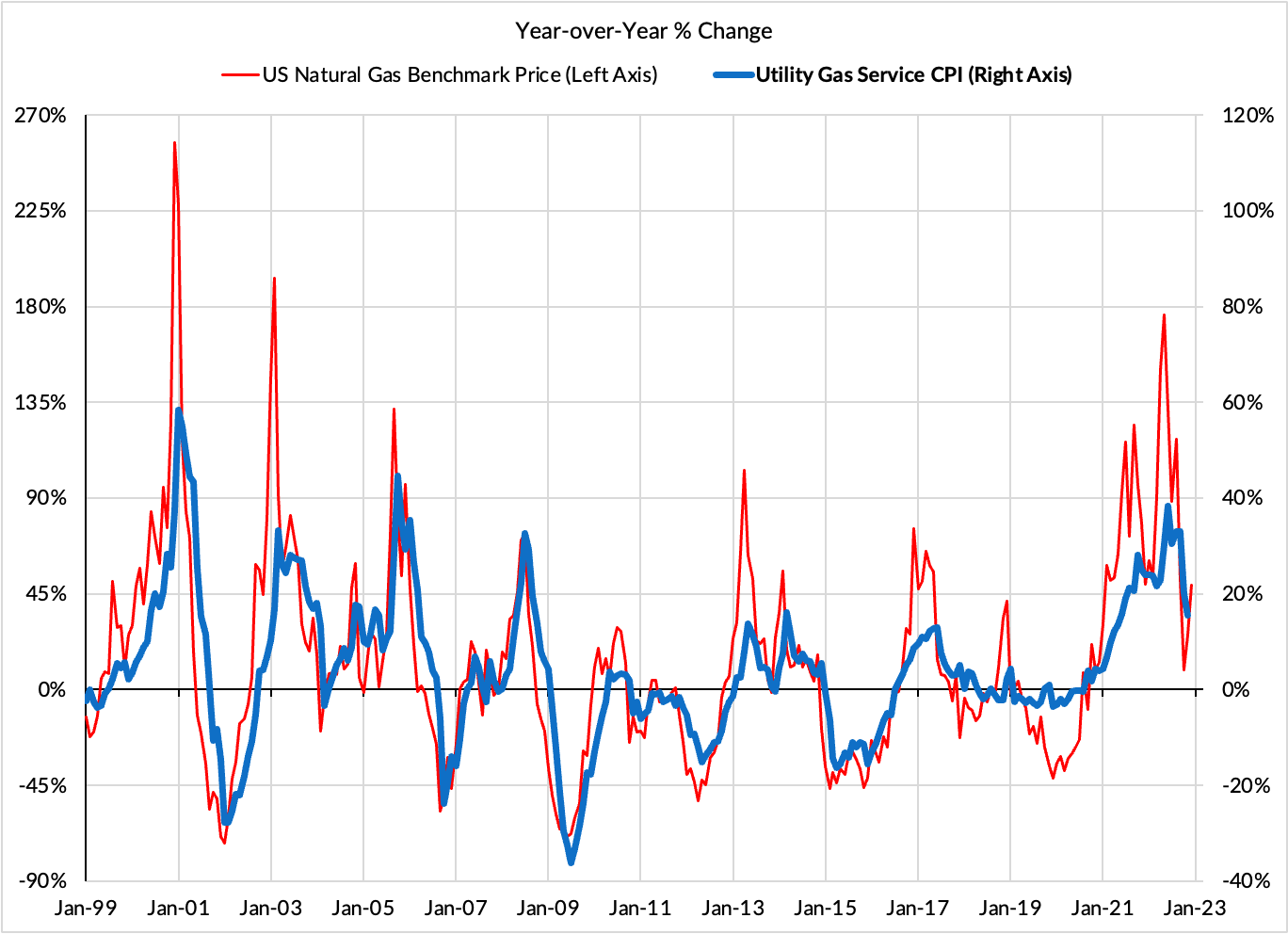

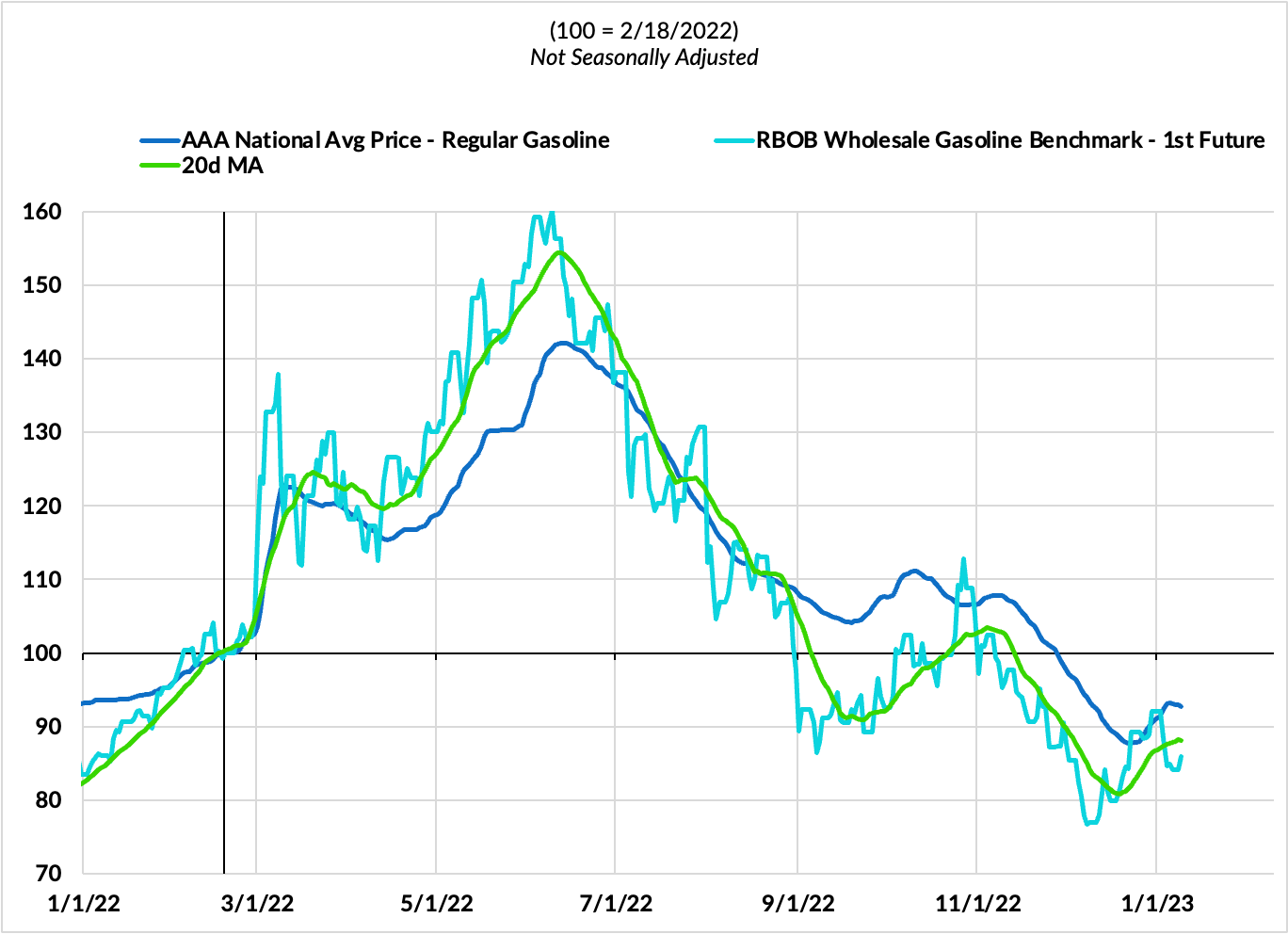

As for the energy components of non-core inflation, the trends are getting more encouraging. Gasoline prices further declined from November to December and home heating costs should benefit from the fall in natural gas benchmarks. Electricity prices should also benefit from the decline in natural gas prices, but these prices tend to be revised with a longer lag and may still reflect upside dynamics that materialized earlier in the 2022 calendar year. Headed into 2023, electricity prices should show more signs of stability and disinflation (vs a hot 2022).

On the whole, we understand the optimism about inflation reflected in the forecasting consensus, but do see several factors that could lead to unexpected (and unwelcome) outperformance.

Charts

Energy

Food (and Core-Affected Food Components)

Housing

Core Goods

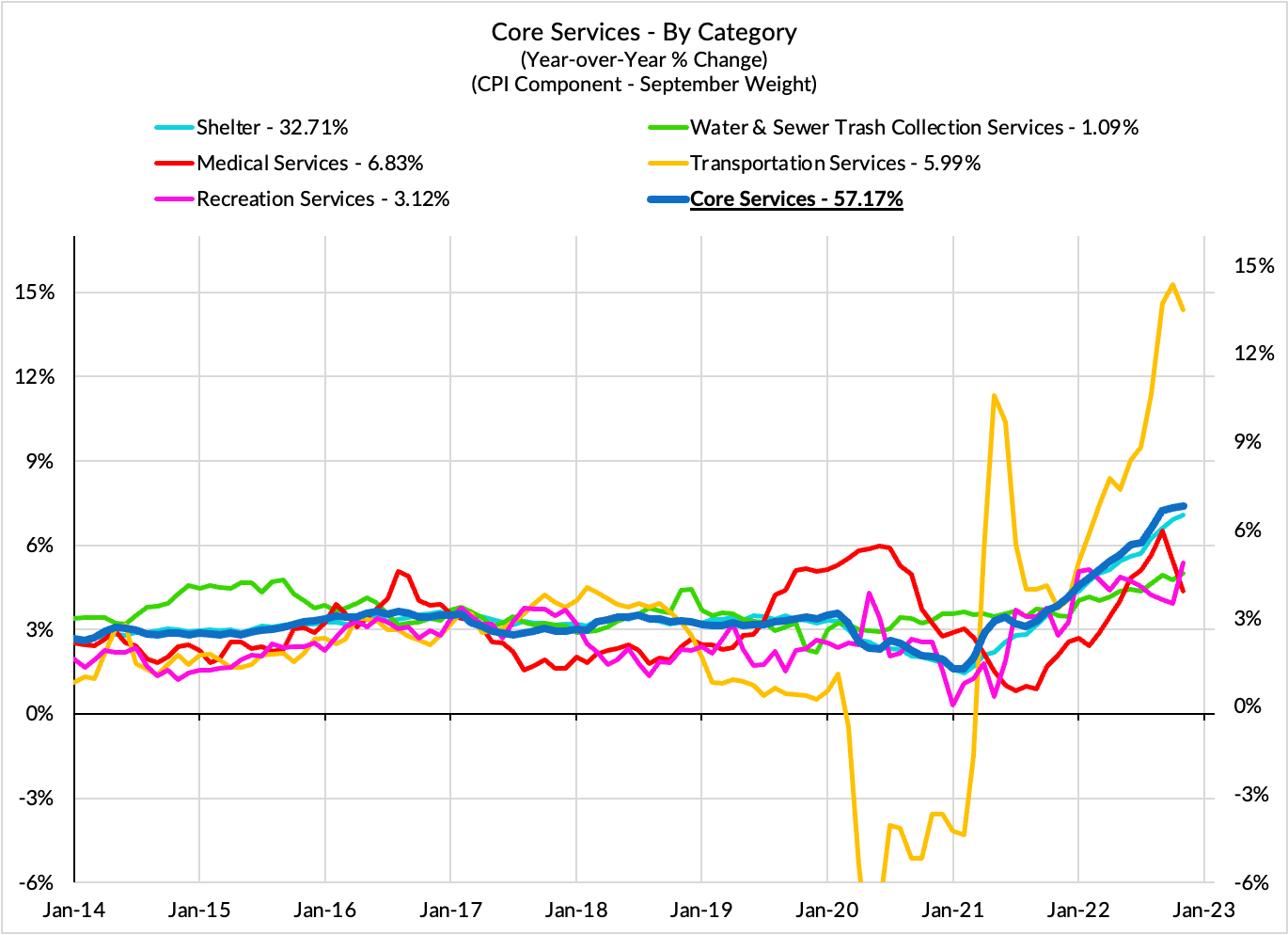

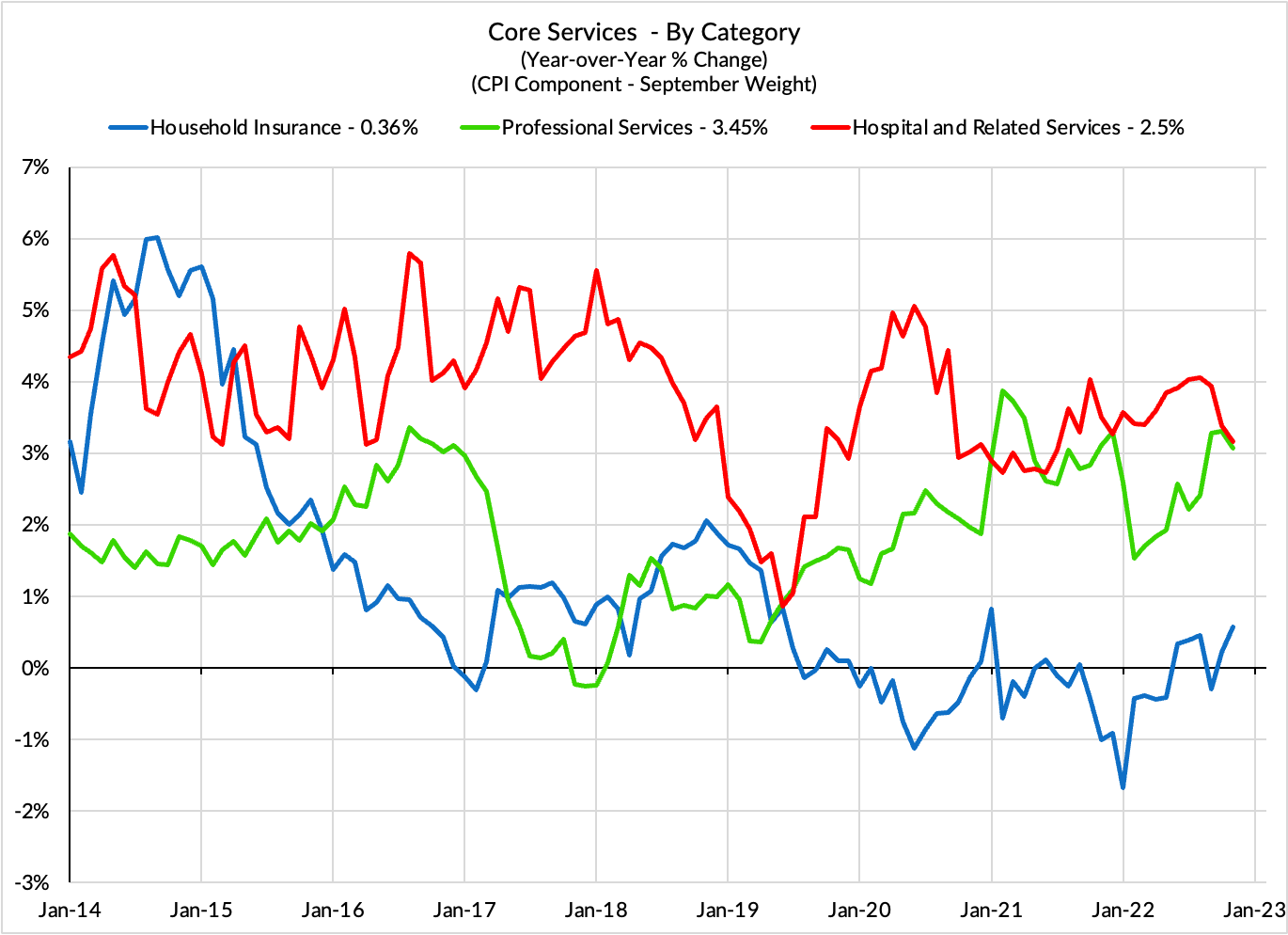

Core Services (Ex Housing)

Past Inflation Previews and Commentary

- 2/12/21: The Good, The Bad, and The Transitory

- 10/27/21: Offsetting Persistent Inflationary Pressures With Disinflationary Healthcare Policy

- 11/8/21: Q4 CPI Preview: What Will Hot Q4 Inflation Tell Us About 2022 Dynamics?

- 12/9/21: November CPI Preview: Planes, Constraints, and Automobiles: What to Look For in a Hot November CPI Print

- 2/9/22: January CPI Preview: Calendar Year Price Revisions Skew Risks To The Upside in January, But The Balance of Risks May Shift Soon After

- 3/9/22: Feb CPI - Short Preview: Inflection Points - Headline Upside (Putin), Core Downside (Used Cars)

- 4/11/22: March CPI Preview: Managing The Endogenous Slowdown: Transitioning From A Rapid Recovery To Non-Inflationary Growth

- 5/10/22: April CPI Preview: Subtle Headline CPI Upside, But Core PCE Should Reveal More Disinflation

- 6/9/22: May Inflation Preview: Peak Inflation? Not So Fast, My Friend. Upside Surprises Loom Large

- 7/12/22: June Inflation Preview: Lagging Consensus Catches Up To Hot Headline, But Relief Nearing…

- 8/8/22: July Inflation Preview: Finally, Fewer Fireworks

- 9/9/22: August Inflation Preview: Can Used Cars & Gasoline Overcome The Rest of The Russia Shock?

- 10/12/22: September Inflation Preview: Timing The Goods Deflation Lag Amidst Hot Inflation Prints

- 11/12/22: October Inflation Preview: When Will We See The 'Real' Goods Deflation Materialize? Until Then, Rent Rules Everything Around Me

- 12/12/22: November Inflation Preview: The Goods Deflation Cavalry Is Coming, But OER Can Upset An Optimistic Consensus Tomorrow