Feb CPI Preview - A Regime Shift For Headline And Core Inflation

Journalists can pretty much pre-write their headlines given the spike in oil prices. Year-over-year headline inflation readings are set to make new highs, potentially breaching 8% based on the food and energy impulse from what we might call the "Putin shock" to key commodities.

At the same time, February should begin to mark some better news for "core" inflation relative to January; consensus (0.5% month-over-month) for February seems to be lagging realized inflation prints over the past 5 months but less tethered to the causes of that strong inflation patch we flagged. We noted that January had unique upside risk for reasons that materialized as we specified: a large subset of prices are only revised at the start of the calendar year, thus setting the stage for outsized impact. Perhaps there is reason to believe in a residual spillover effect for February, but the absence of this calendar-effect should reveal itself as a slower core inflation reading from the 0.6% month-over-month January print.

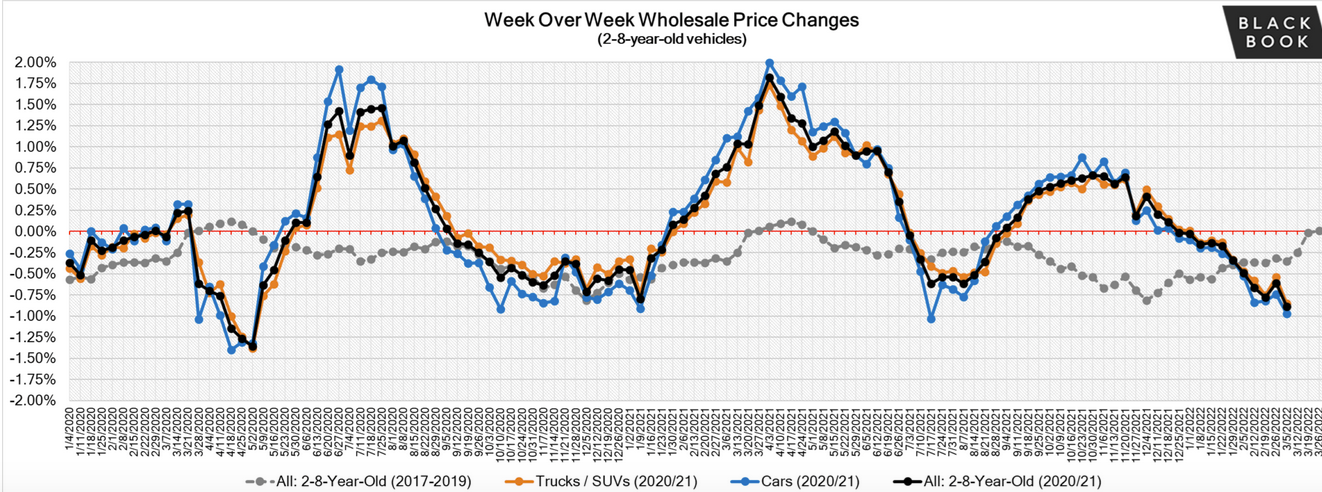

Core inflation in February should also begin to show some of the softness that is now growing more apparent in private used car price data. February is the peak month for wholesale used car sales, and the auctions this past month appear to be going poorly. The main driver here isn't the chip shortage; it is the dissipation of demand from rental car companies (who were buying back their liquidated fleets through much of 2021H2). Here's the latest data from Blackbook:

CPI data lags the Blackbook data by a couple months, and the Mannheim Used Vehicle Index a little less so, but both indicators are signaling some reprieve in from what was an exceptionally strong run in used cars CPI in 2021. We should see some of that reprieve show up tomorrow.

What we are dealing with now is an inflection point from one macroeconomic episode (the pandemic) to a new and very different episode (Russian commodity shock). Russia remains a linchpin producer of key commodities, most notably oil and gas but also base metals (e.g. palladium, nickel), agricultural commodities (e.g. wheat), and fertilizer. This shock is destined to hit the items that fall outside of "core" inflation measures (which exclude food and energy), but food and energy are generally consumed disproportionately by those at the lowest end of the income spectrum.

The net effect over the course of the year from this shock remains unknown, because the timeline of the shock (how long the war, sanctions, and self-sanctions last) is uncertain, but we can say a few obvious but still useful things.

Quick estimates of equity risk premiums suggest that there's more tightening of financial conditions than what expected rate hikes are reflecting. CDX indices also implying 100bps of HY spread widening.

— Skanda Amarnath ( Neoliberal Sellout ) (@IrvingSwisher) March 8, 2022

Warrants marginal caution from Fed (mkt pricing in ~6 hikes in '22) https://t.co/HZs8PmpAOl pic.twitter.com/UHMjUYoWju