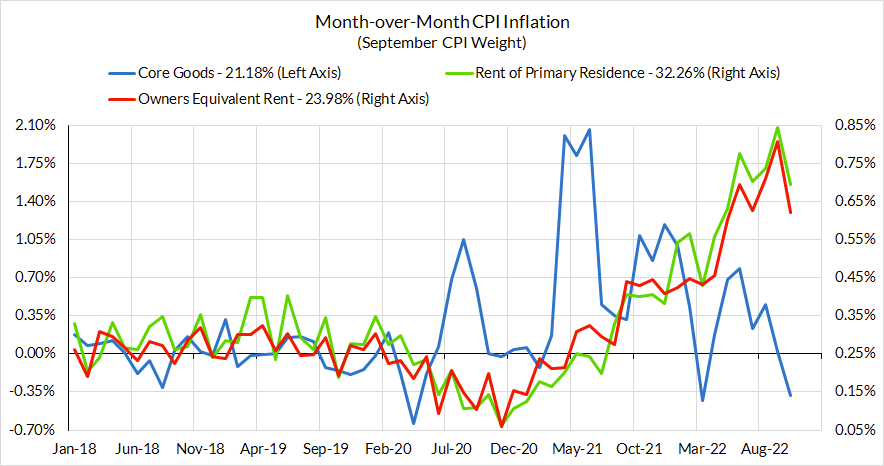

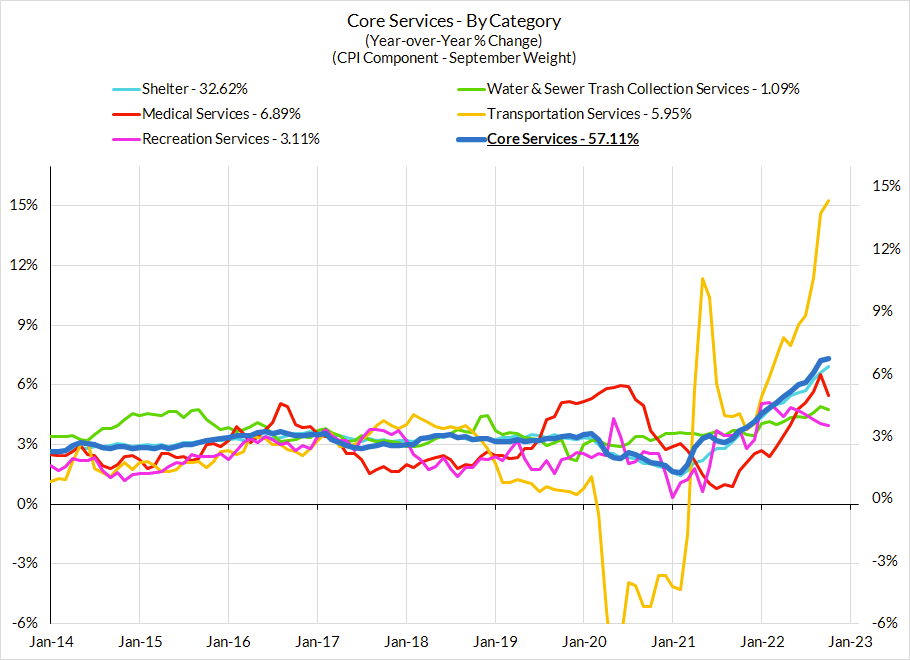

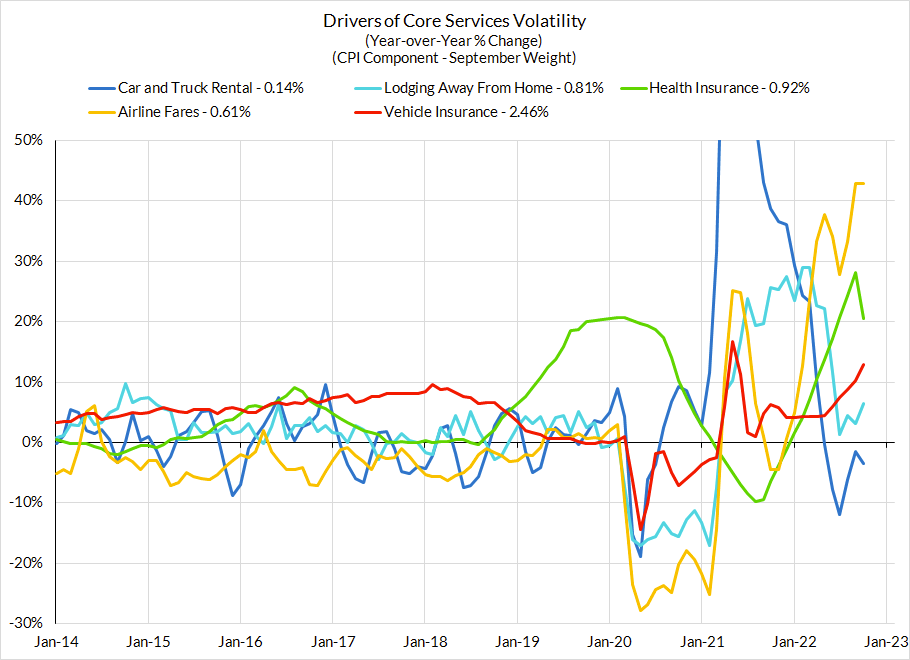

Not out of the woods yet on upside risks to monthly core CPI inflation:The forecasting consensus has shifted down from its 0.5% expectation for core CPI in October to a more optimistic 0.3% expectation in November. This seems to be mostly a reaction to the welcome core inflation "miss" last month, and is in large part justified so long as you're taking a longer view of the inflation outlook. But for the purpose of forecasting November CPI, the pace of deceleration in owners' equivalent rent from September (0.80%) to October (0.62%) seems at risk of some reversal. A return to rent and OER readings closer to September can still catch an optimistic forecasting consensus (for core CPI disinflation) offsides tomorrow (consensus year-over-year: 6.1% from October's 6.3%)

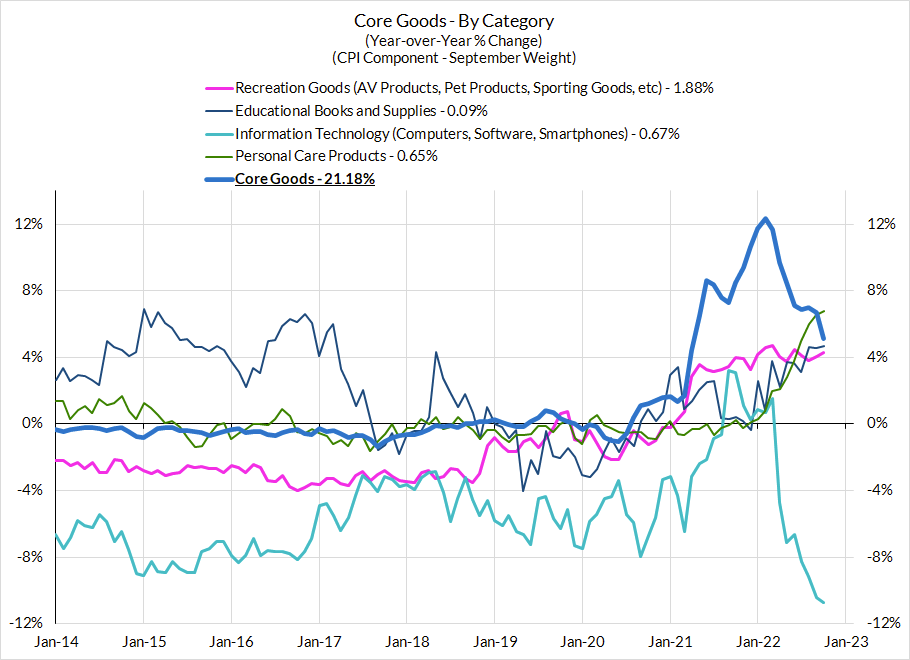

Reason for Optimism: Wholesale used car price declines for several months are only just beginning to properly feed into the retail-level CPI data; we should see further declines in November and December used car data. The fundamentals for supply are continuing to improve and are likely to put more pressure on new and used car pricing in 2023.

Reason for Optimism: We are seeing other core goods prices also begin to correct in Q4 based on firm-level commentary on bloated retail inventories and discounting. Holiday-season+January is primetime for the kind of aggressive inventory-clearing discounting that can drive more aggressive goods deflation over the coming CPI releases.

Reasons for Caution Tomorrow: Unfortunately, some of this well-placed optimism has to be countered by A) the risk of rent and OER CPI reverting to its September monthly growth rate, and B) the risk that the bulk of atypical discounting this holiday season takes place in December and January.

Non-core inflation is still facing cross-currents, but starting to tilt more favorably towards disinflation

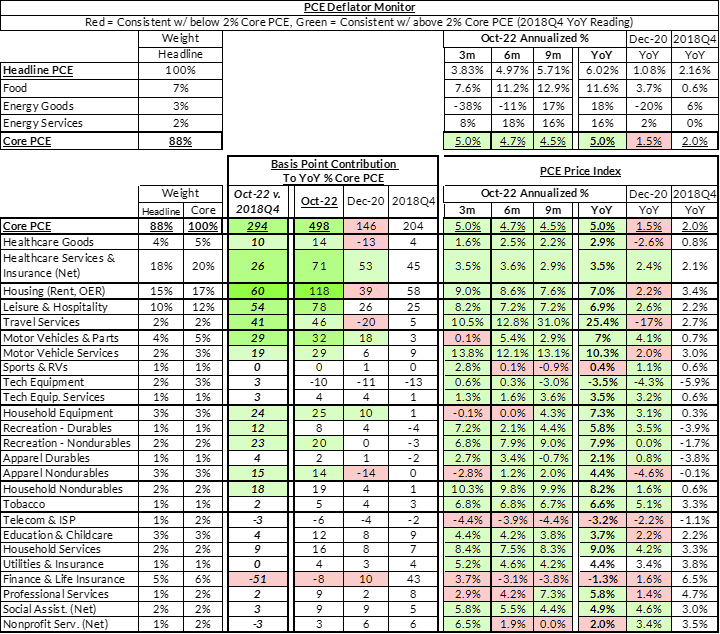

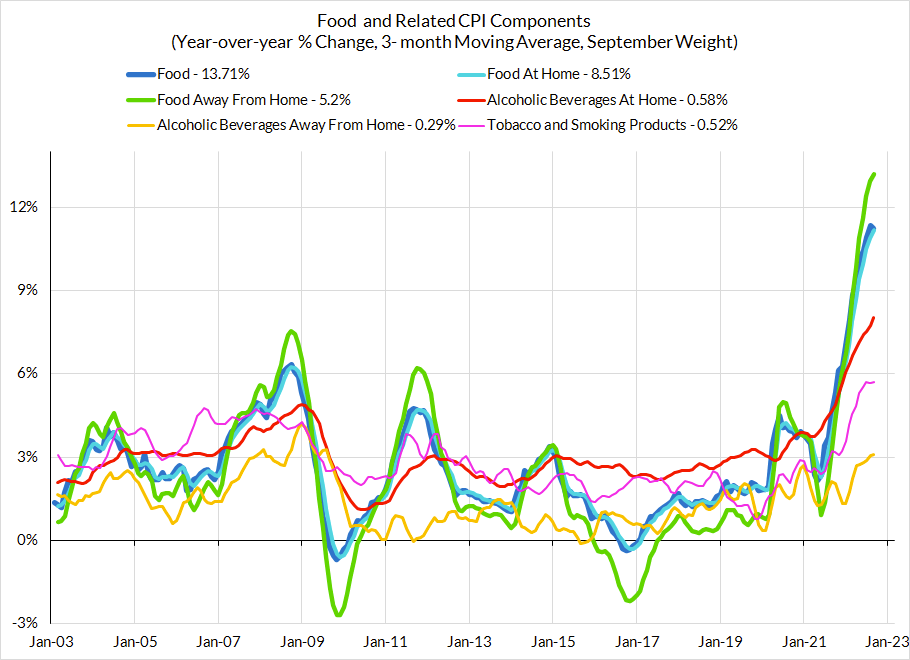

Upside risk: Food pricing is still likely to run hot for the time being as a number of cost-push shocks are still filtering through the data. Moreover, food at home CPI (which is excluded from "core CPI" and "core PCE") has a lot of bearing on the pricing of key components that are included in core inflation (food services are included in "core PCE"; alcohol is included in "core CPI"; tobacco and smoking products are included in both). Food "at home" prices showed some sign of deceleration in October but we will need to see more sustained evidence of progress, and it will take even more time to filter into core-sensitive categories like food services, which typically lag pricing trends at the grocery store.

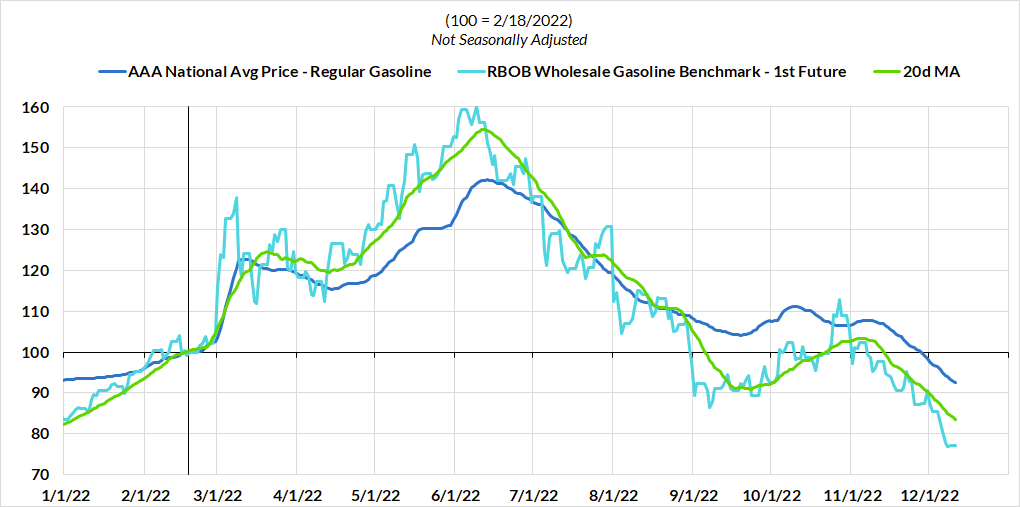

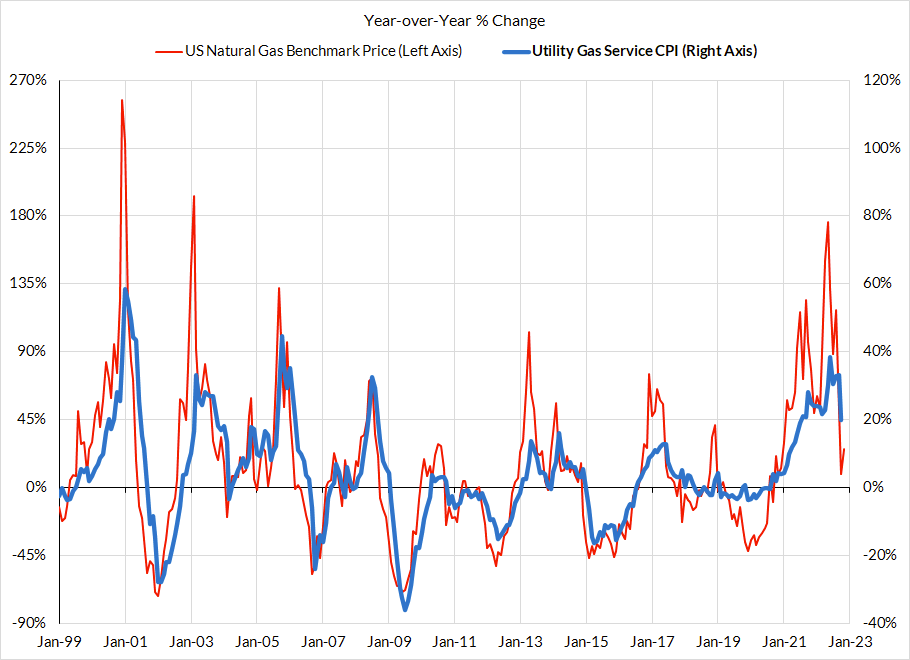

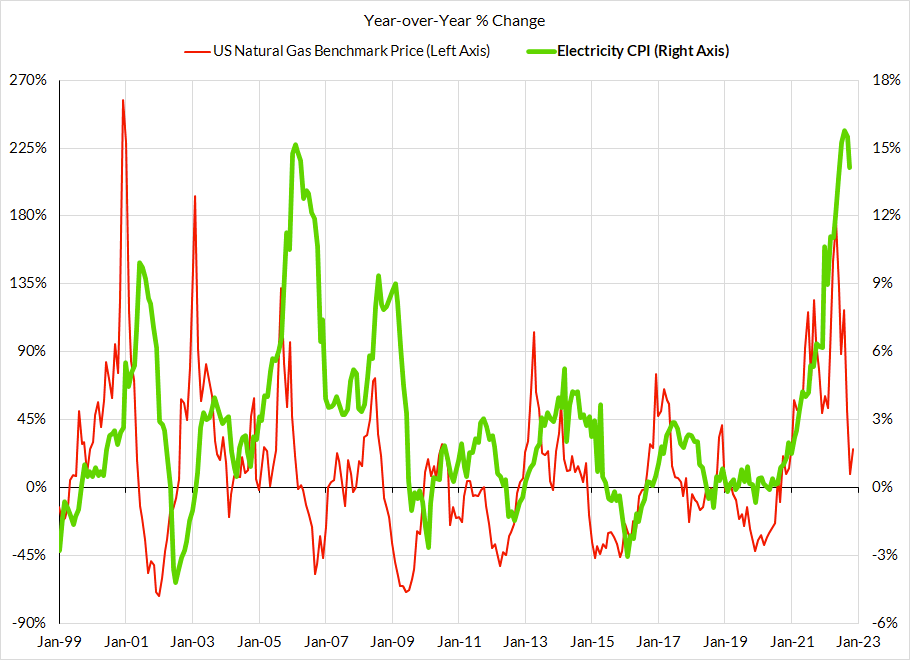

Downside risk: Energy prices are starting to give more reason for broad-based optimism, but there will be lags to how commodity price declines in gasoline and natural gas filter through to CPI. Refining margins and crude oil prices are both compressing in a manner that will—over the next couple months—filter through to retail gas station pricing. Utility gas service pricing should show some stabilization after declines in natural gas benchmarks from a few months ago. Electricity CPI tends to respond with a longer and more variable lag to natural gas prices but the longer-term outlook is improving here as well.