February FOMC Quick Recap: The (Recessionary) Projections of December Live On

Summary: Today's FOMC Statement and press conference shows high continuity with the thinking reflected in the December FOMC meeting. The Fed does not appear to be impressed by the deceleration in wage growth in 2022H2 enough to explicitly rethink the inflation, unemployment, or interest rate outlook right now. Two more hikes this year remains the Fed's base case (terminal Fed Funds Rate: 5-5.25%), with risks likely skewed towards more than two hikes.

Decision: Today's 25bp hike aligned with consensus and market expectations.

Rate Guidance: Despite the opportunity to show more open-mindedness about the path for interest rates over coming meetings, the FOMC is continuing to signal high confidence that at least two more 25bp hikes are needed.

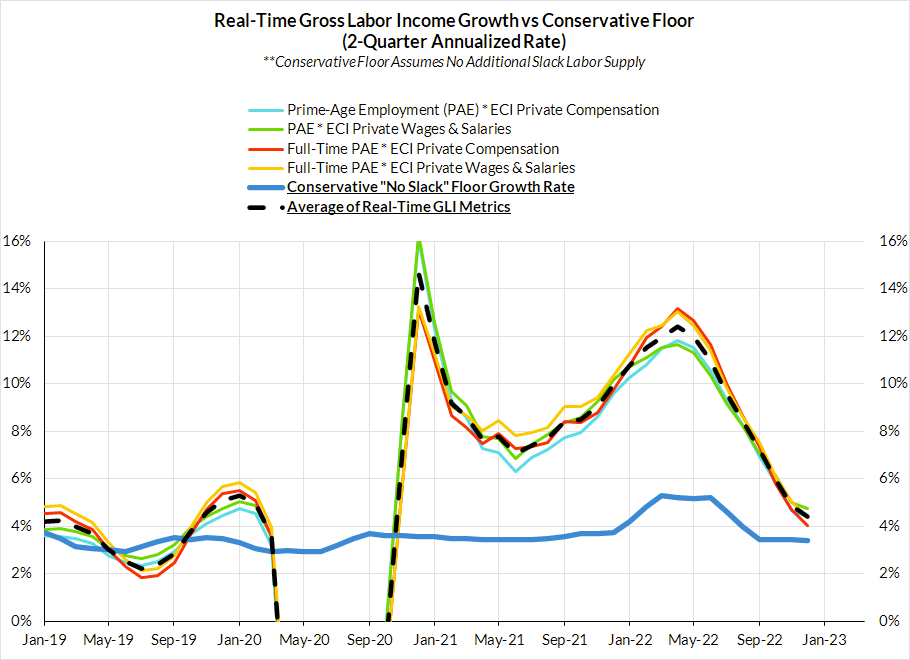

Chair Powell's Reasoning: We heard all of the major arguments we heard in December, but with the only surprise stemming from the elevated emphasis on goods disinflation over wage disinflation. The former only really got going in Q4, whereas ECI clearly shows sequential deceleration across both Q3 and Q4.

FOMC Member |

Latest Comments |

Comments as of Previous SEP |

|---|---|---|

Jerome Powell |

The Fed's tools work, and there is nothing wrong with our mandates. January 10, 2023 |

The Fed has been pretty aggressive, but it does not feel it appropriate to crash the economy and clean up afterwards. November 30, 2022 |

Lael Brainard |

More two-sided risks develop as we move deeper into restrictive territory and we're now in an environment where there are risks on both sides. January 19, 2023 |

Continued supply shocks may force central banks to tighten policy in order to manage risks. November 28, 2022 |

Michelle Bowman |

Allowing inflation to persist has far greater costs and risks. January 10, 2023 |

We are not seeing a significant impact on inflation reduction, they are still at high levels and i need to see our actions have an impact. December 1, 2022 |

Michael Barr |

It is a mistake to believe that changes in the pace of rate hikes indicate a shift in the Fed's commitment to a 2% inflation target. December 1, 2022 |

The Fed's policy rate will have to remain high for a long period of time. December 1, 2022 |

Lisa Cook |

Despite recent encouraging signs, inflation remains far too high and of great concern. January 6, 2023 |

Wage growth is above levels that are consistent with the Fed's 2% inflation target. November 30, 2022 |

Philip Jefferson |

Low inflation is critical to achieving long-term growth. November 17, 2022 |

Low inflation is critical to achieving long-term growth. November 17, 2022 |

Christopher Waller |

I favour a 25-basis-point rate hike at the upcoming meeting, followed by additional policy tightening. January 20, 2023 |

Rates still have a long way to go and will require increases into next year. November 16, 2022 |

President John Williams |

Us inflation remains too high, and the Fed has more work to do on rate hikes. January 19, 2023 |

The Fed has a long way to go with rate hikes. December 1, 2022 |