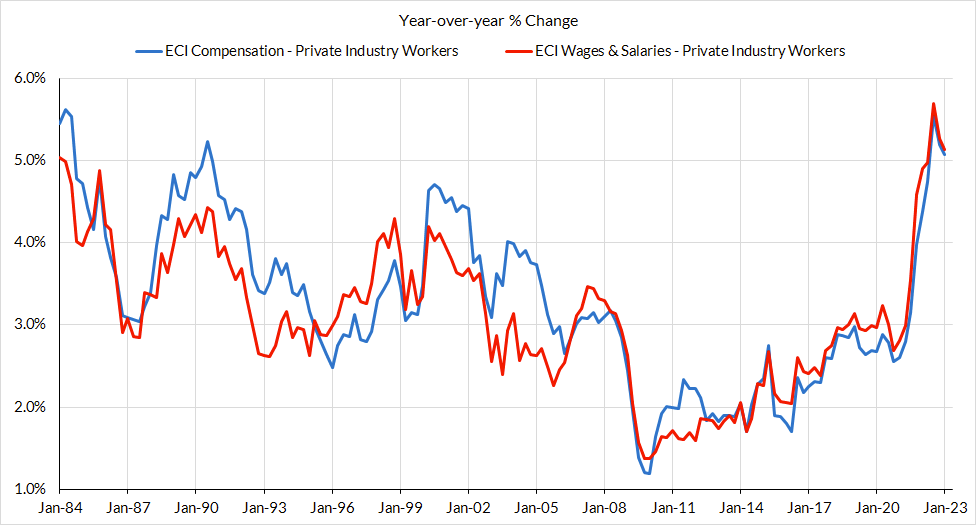

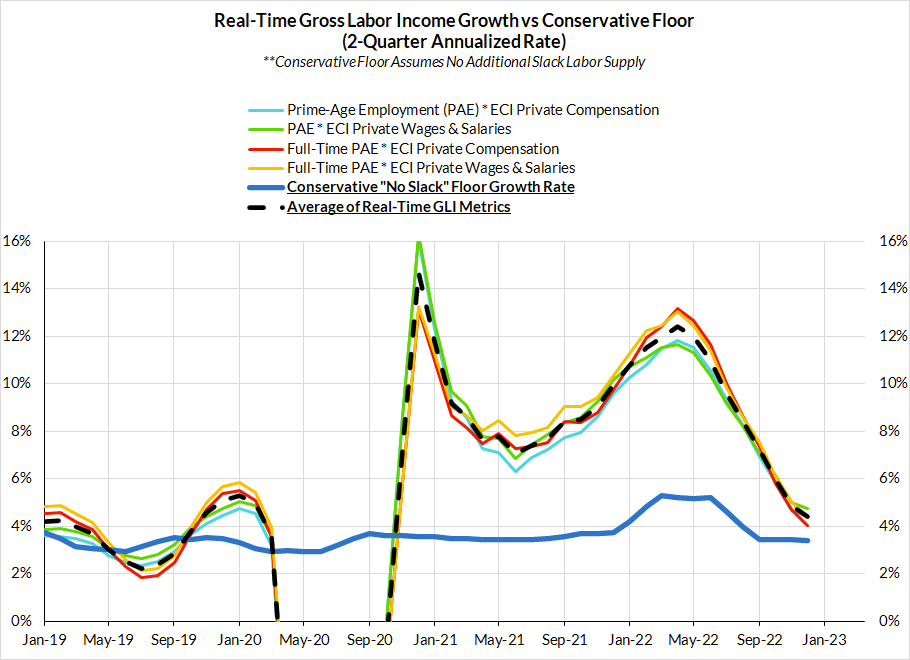

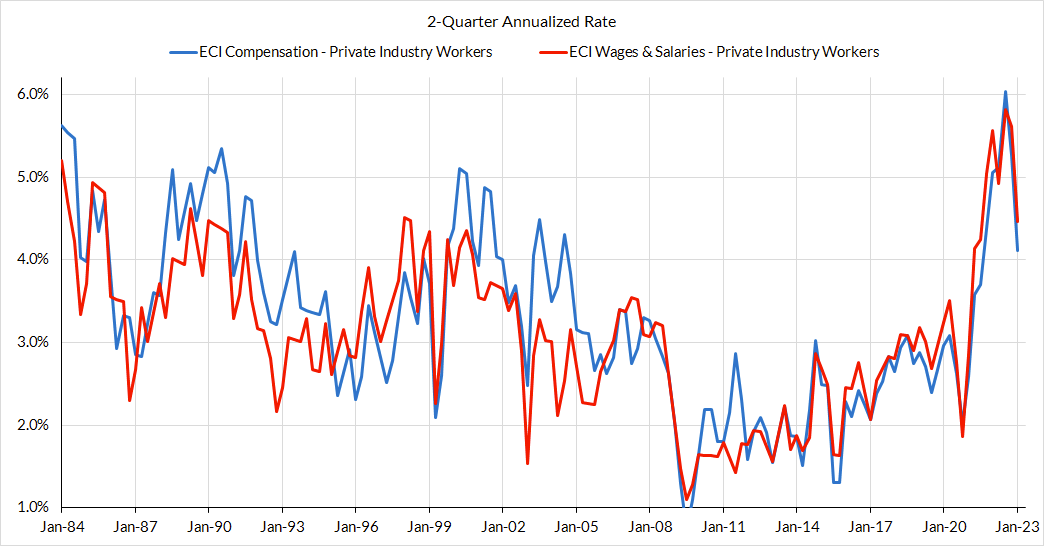

Wage growth slowed in Q4 faster than consensus forecasts–-at an annualized rate just over 4%. We already noted in our preview that this would be very consistent with what the other Q4 macroeconomic & wage data was signaling. The scenario poised to trigger a hawkish overreaction did not materialize. While nothing about inflation or wage growth is definitive at this stage, the Fed should take seriously the possibility that disinflation can materialize without recessionary rises in joblessness.

The link has been copied!