Too Many Eggs In One Basket: The Fragility of The Fed's Wage-Oriented 'Cost-Push' View of Inflation

The Fed is arguing that inflation is driven by the cost-push impacts of wage growth on service prices. This is a traditional view, but the pandemic recovery has been anything but textbook. In our view, the primary nexus is a demand-pull relationship. The core question for the Fed ought to be how gross labor income growth—that is, the cumulative effect of both job growth and wage increases—translates into nominal consumer spending growth. While wage growth plays a role in both views, the reason for the distinction is critical:

What should policymakers do if wage growth indicators are hot due to distortions, lags, or simple statistical noise, rather than underlying strength? Based on recent statements from Fed leadership, the only other dynamic that could get the Fed to rethink their tightening campaign is if a recessionary rise in unemployment has already materialized.

The Fed is relying on lagging and flawed dynamics to constrain their tightening efforts. This unnecessarily puts the labor market and the US economy at excessive risk of recession.

Since wage growth measures are subject to flaws and lags, the demand-pull view can be monitored more robustly than the cost-push view in real-time. More importantly, the non-wage data needed to force a pivot under the demand-pull view does not turn on first seeing mass joblessness. If the demand-pull view is right, then the Fed should be taking more seriously the disinflationary implications of slowing growth in employment, gross labor income, and consumer spending, all of which can be observed more reliably than wages and all of which are occurring already.

To address the premise of this piece, here's a run-down of the flaws across major wage indicators:

The Fed’s job is to interpret imperfect information in real-time. Every observed data point has some methodological flaw, but some data is more reliable for real-time purposes than others. But what do you do if a critical input for your causal view of inflation—whether cost-push or demand-pull—is unobservable?

The Fed is overly focused on the wage Phillips Curve. If nominal wage growth comes in strong—even if for ultimately faulty reasons—the Fed seems unwilling to settle for anything less than a recessionary rise in the unemployment rate. In their view, this is virtually the only way “to bring the labor market back into balance.” Perhaps a fortuitous, non-recessionary, reversion in job openings could provide Chair Powell enough relief to back off of an aggressive tightening policy. But even this kind of data is lousy and unreliable to lean on, for well-documented methodological and empirical reasons. The Fed is effectively taking a binary view: either ECI tracks down quickly or else the Fed will continue to aim for recessionary increases in unemployment.

For us, there is a healthier middle ground. There exists macroeconomic data other than wages that give us clues about the underlying trajectory of household income and spending growth (and by extension, wage growth too!).

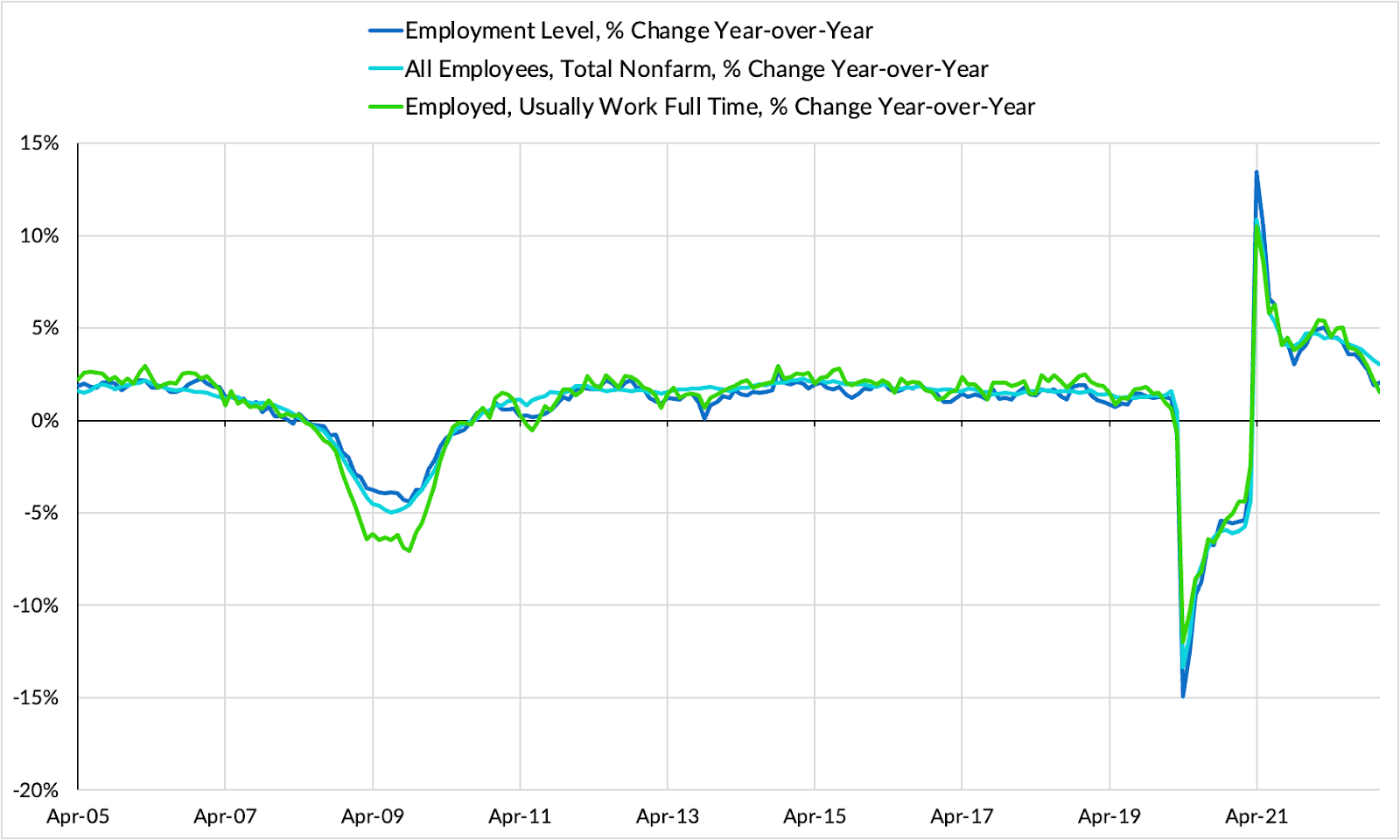

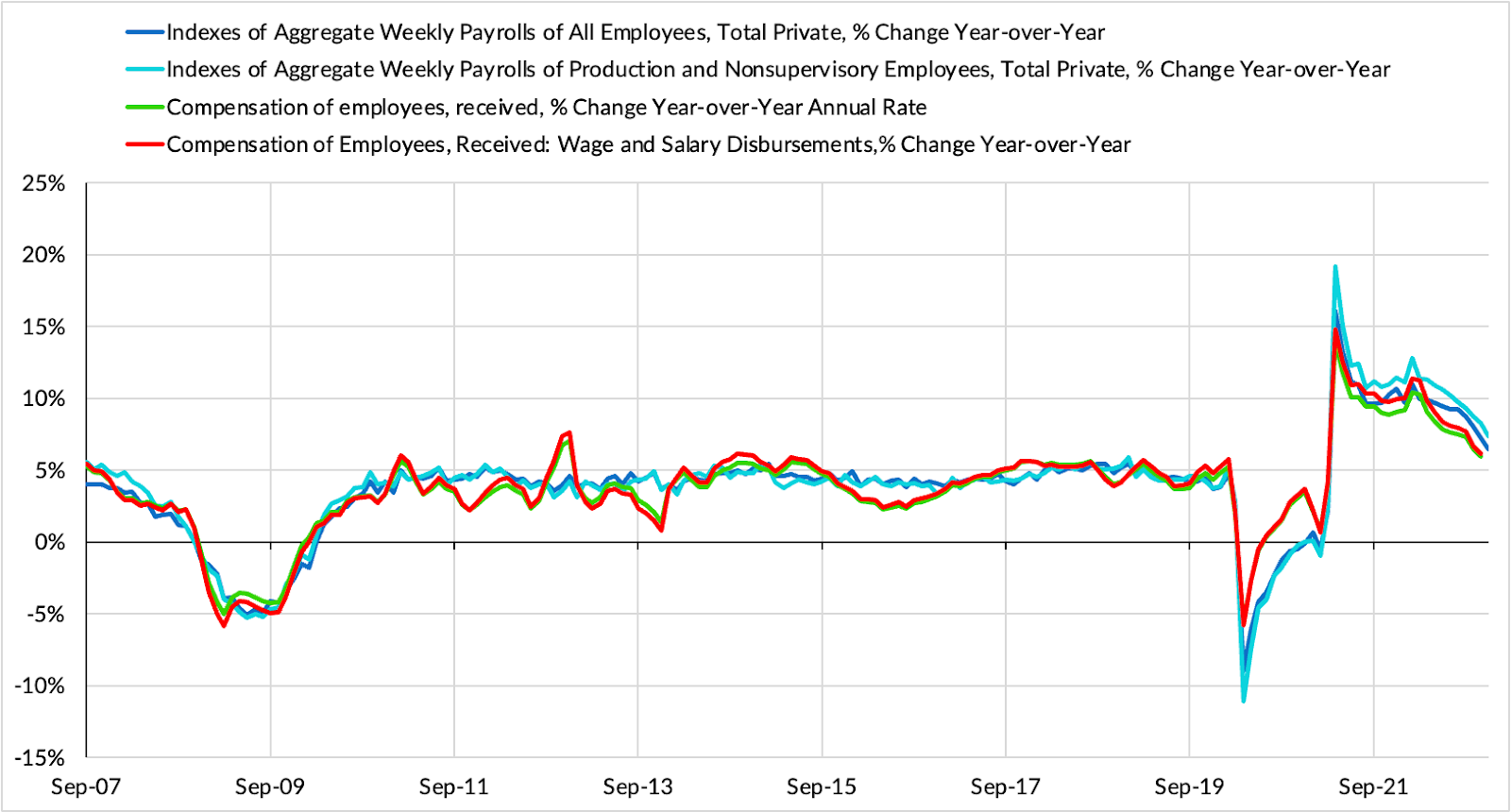

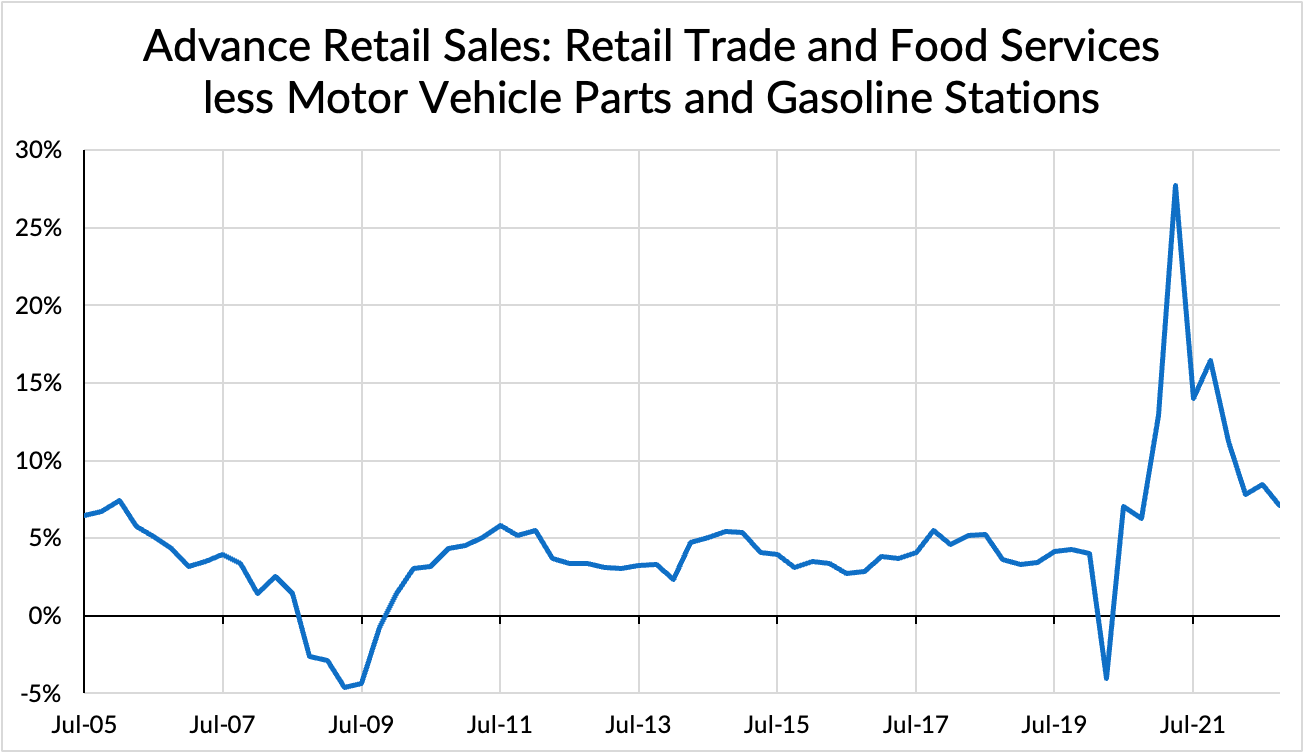

Right now the data from all three of these metrics are confirming a story of inflation cooling off through the demand-side labor market mechanism:

If these decelerating dynamics hold up and trend nominal growth reverts fully back to the pre-pandemic pace, inflation risks should be lowered correspondingly. For a permanent and meaningful regime shift to inflation trends, the pace of gross nominal income and spending growth almost necessarily should shift upward too. Perhaps some of these local trends reverse in the coming months and quarters, but the data is currently validating the idea that demand-side inflation pressures are already cooling. [The charts below are year-over-year growth rates and should ease further in the coming months and quarters given upcoming base-effects]