While layoffs are painful to workers, more attention needs to be paid to the threat of a rise in unemployment arising from a slowdown in hiring. In this report, we examine the important role that a fall in hiring rates plays during unemployment increases.

Earlier this month, we wrote about just how problematic the Fed’s projections of the unemployment rate are. The Summary of Economic Projections calls for an unemployment rate of 4.6% by the end of this year. It signals that the Fed is prepared to engineer a recessionary labor market, even while both wages and prices have cooled quickly over the last three months.

At the December FOMC press conference, Jerome Powell tried to downplay the pain that would arise from increasing unemployment this quickly:

…you can look at history, right? And history would, you know, would say that, in a situation like this, the declines in unemployment would be more meaningful, I think, than what you see written down there…

…vacancies can come down a fair amount. And we’re hearing from many companies that they don’t want to lay people off—so that they’ll keep people because it’s been so hard…

So the fact that there’s a strong labor market, you know, means that companies will hold on to workers. And it means that it may take longer, but it also means that the costs in unemployment may be less.

-- Jay Powell, December 14th, 2022 FOMC Press Conference

In other words, Powell is saying that a rise in unemployment driven by lower hiring instead of more layoffs would make this less painful than previous episodes.

Layoffs receive outsized attention in the media, relative to hiring. Layoffs, especially in the tech sector, have recentlygrabbedheadlines, even though the aggregate layoff rate remains low. Meanwhile, the hiring rate has declined substantially from its post-pandemic high and is now at pre-pandemic levels. While layoffs are painful to workers, more attention needs to be paid to the threat of a rise in unemployment arising from a slowdown in hiring. Tight labor markets are not only beneficial to workers because they are able to avoid unemployment. A long-term benefit of tight labor markets is that workers are able to move to better, higher-paying jobs over time; a slowdown in hiring threatens the ability of workers to accumulate skills and move up the job ladder.

In this report, we examine the important role that a fall in hiring rates plays during unemployment increases. While layoffs do often happen during recessions, they account for a relatively small amount of the rise in unemployment. Importantly, when hiring rates fall they do not return to pre-recession levels for a long time, while layoff rates fall back to normal levels relatively quickly. This slowed hiring rate, in turn, is why the unemployment rate remains elevated for many years after recessions.

Although Powell’s comments might seem innocuous, a hiring-driven increase in unemployment is the norm, not the exception, historically speaking.

Hiring Plays an Important Role in Recessions

A key feature of the labor market is that at any given time, there are large numbers of layoffs, hires, and quits. The unemployment rate is jointly determined by the rate at which unemployed workers find jobs and the rate at which workers separate from jobs into unemployment. During strong labor markets, hiring is strong relative to layoffs, so any workers that find themselves unemployed quickly find jobs, keeping the unemployment rate low. Conversely, during recessions, weak hiring slows the exit of workers from unemployment, keeping the unemployment rate high. Increases in unemployment can therefore theoretically arise from an increase in layoffs, decreases in hiring, or a combination of both.

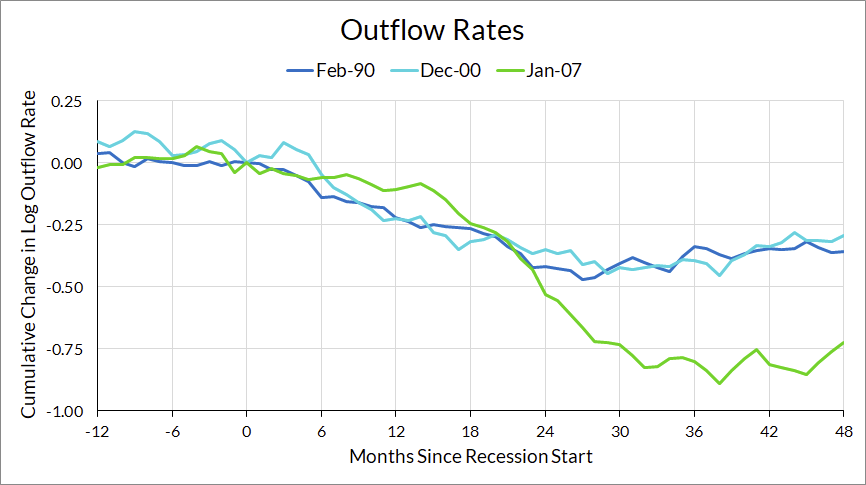

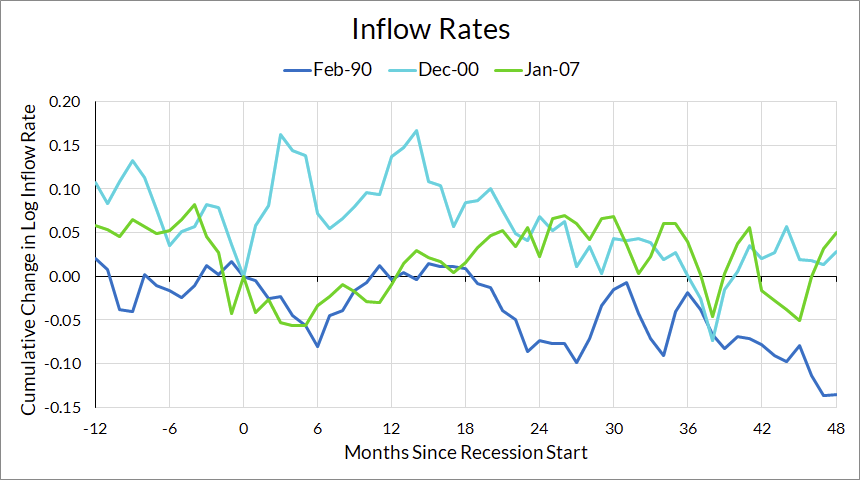

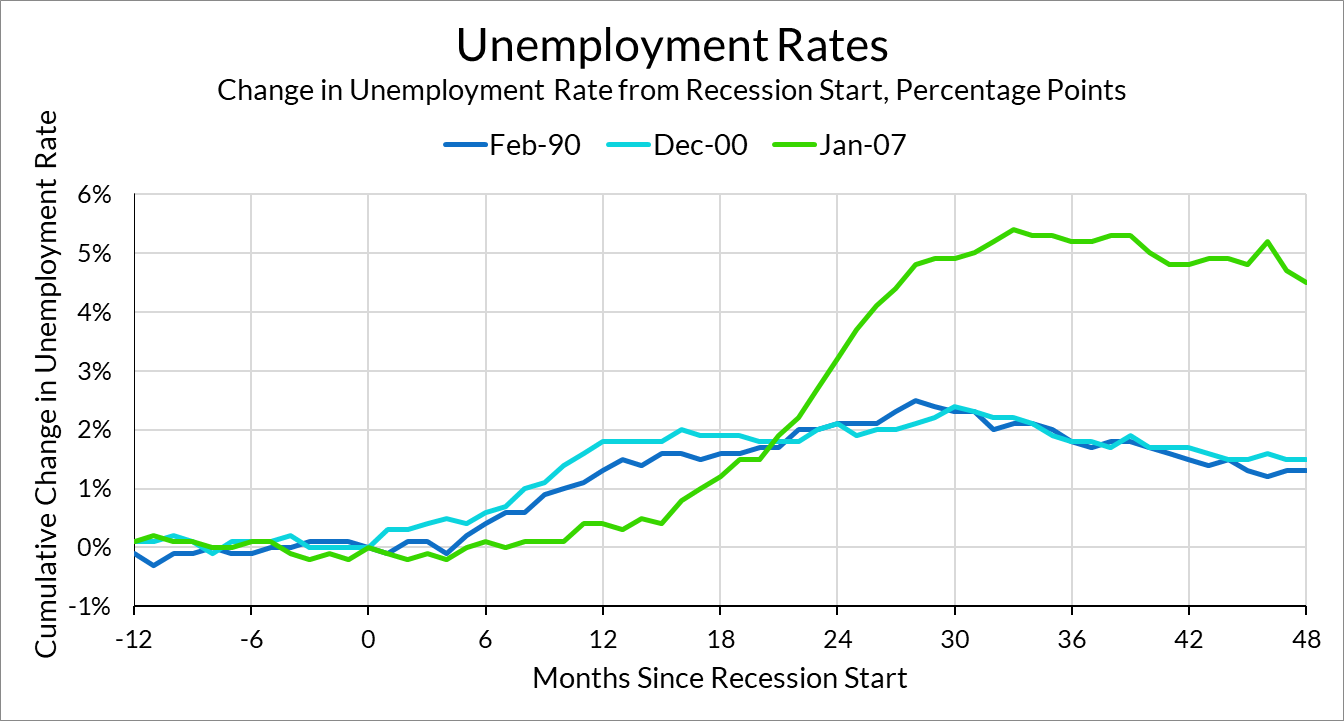

One data source to look at is the JOLTS, which asks firms how many quits, hires, layoffs, or firings there were in a given month. Importantly, these are observed economic flows, unlike job openings, which come from the same survey but can mislead regarding the actual willingness to hire. In both the 2000 and 2007 recession, hiring rates (hires as a percentage of employees) fell substantially and took years to recover, taking until 2005 and 2019 to recover, respectively. Meanwhile, layoff rates spike relatively early during both recessions but quickly return to pre-recession levels.

Nowadays, most eyes are on the JOLTS data. However, the historical utility of the JOLTS is limited since it began in late 2000. Going forward, the JOLTS data may also be less reliable as the response rate has declined from around 70% to 30% over the past decade. JOLTS data also only tells the story of hiring and layoff behavior from the perspective of firms, not workers, making it difficult to interpret the data in terms of worker outcomes. For example, JOLTS hires could be hires of either unemployed or already-employed workers, so the effect on unemployment is unclear.

For another perspective on labor market flows, economists have used methods from Shimer (2012) to measure labor market flows using the Current Population Survey (CPS) data. This method decomposes changes in the unemployment rate into changes in the “inflow rate”, the rate at which workers move from employment to unemployment, and the “outflow rate”, the rate at which unemployed people find jobs. The overall unemployment rate is determined by the combination of these inflow and outflow rates.

Elsby, Hobijn and Solon (2013) show that the change in the unemployment rate can be approximately accounted for by changes in the log inflow and outflow rates. Below, I graph the cumulative change in the log inflow and outflow rates over the course of the three most recent pre-pandemic recessions.

Source: Bureau of Labor Statistics, Author's CalculationsSource: Bureau of Labor Statistics, Author's Calculations

Consistent with the JOLTS data, the CPS data shows that outflows from unemployment, rather than inflows into unemployment, play a larger role in the increase in unemployment during recessions. When unemployment inflow rates increase, they do so slightly and return to pre-recession levels relatively quickly. Meanwhile, unemployment outflow rates exhibit large declines and take years to recover to pre-recession levels. The slow recovery of hiring therefore is the reason unemployment takes years to recover after a recession.

Powell says that if the Federal Reserve’s unemployment projections are realized through lower hiring, the pain of that unemployment will be less costly than what history suggests. The historical record shows that hiring-driven recessions are the norm, not the exception. If the Fed manages to increase unemployment primarily through a reduction in hires, that would not be historically unique. A hiring recession is still a recession, and all recessions are hiring recessions.

Welfare Costs of Slow Hiring are Still Large

Powell says lower hiring would be "less meaningful" if not accompanied by layoffs. It is important to not downplay the costs of a recession from hiring. While a full accounting of the relative welfare costs of unemployment from layoffs versus reduced hiring is beyond the scope of this piece, the evidence shows that weak hiring is harmful to workers.

Tight labor markets are not only good for workers because they reduce unemployment. Tight labor markets lead to higher wages as unemployed workers find better jobs than they otherwise would and employed workers find more opportunities to move to higher-paying jobs.

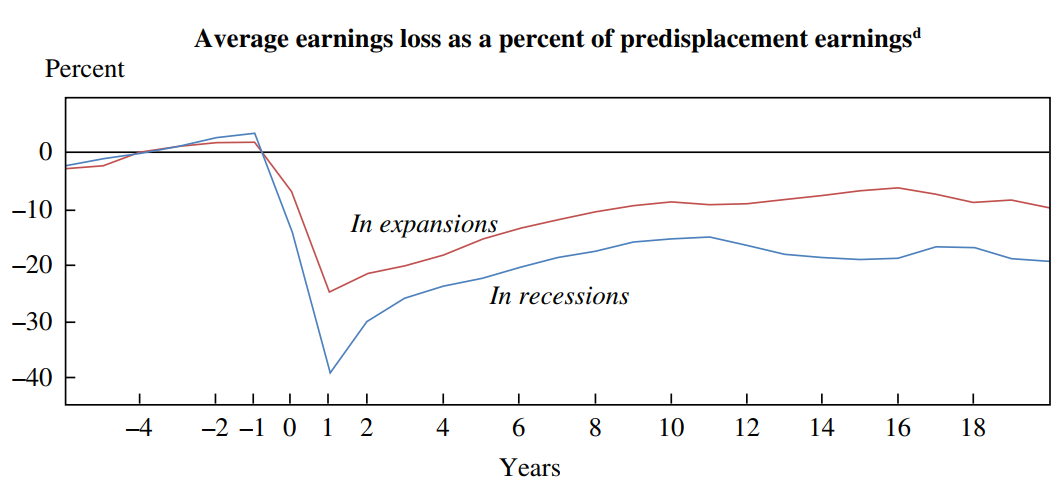

Strong hiring also reduces the pain of any layoffs that do happen. While getting laid off is a generally negative experience, the extent of the pain of getting laid off depends on the labor market at the time. If hiring rates are high, a laid-off worker can find a job relatively quickly with fewer, if any, losses in earnings. Davis and von Wachter (2011) study how the wage trajectories of workers affected by mass layoff events varies with the unemployment rate, and find that displaced workers lose far more earnings when the unemployment rate is high. The loss in earnings persists for over twenty years after displacement. Importantly, the bulk of the earnings loss is not due to lower employment rates but due to reductions in hours or wages, indicating that workers laid off during recessions are persistently employed at lower-paying jobs than if they had entered during expansions.

Additional evidence for the harm of soft hiring comes from Oreopoulos, von Wachter and Heisz (2012), who study how the employment trajectories of college graduates varies with the unemployment rate at the time of graduation. They find that the earnings of college graduates are lower when they graduate in times of high unemployment, and the effects persist for up to ten years. As with workers affected by mass layoffs, this difference is not solely attributable to differences in employment rates, which quickly reconverge within a few years. College graduates unlucky enough to graduate during high unemployment rates are persistently more likely to take jobs at smaller, lower-paying firms. The effects are highly unequal, with the largest earnings losses concentrated among graduates from schools and majors with generally lower-paid graduates.

Since layoffs generally come in short-lived waves, the persistence of higher earnings losses from workers affected by mass layoffs and college entrants during recessions is likely explained by the persistent weakness of hiring during recessions. As such, the inability of unemployed workers to find jobs during recessions deserves as much attention as the more visible layoffs.

This Time is Not that Different

With recent high-profile layoffs dominating the headlines, there will inevitably be an impulse to look to the aggregate layoff statistics, which are still low (although there are warning signs that this may change) to gauge the health of the labor market. While a spike in layoffs would indeed be worrying, the absence of such a spike does not preclude a painful recession. Historically speaking, recessions arise and persist primarily through a fall in the hiring rate. Policymakers, journalists and commentators should pay as much attention to what happens to hiring.

At the moment, hiring rates (as measured by JOLTS) have fallen quite a bit and have now returned to pre-pandemic levels. However, unemployment outflow rates have yet to fall, keeping the unemployment rate low. This implies that the job-switching churn we’ve seen during the pandemic has been normalizing.

However, if the Fed projections are realized, some combination of layoffs or slower hiring will necessarily occur. If this happens purely through hiring, the Fed may try to argue that this time is different, in terms of how much pain workers have to endure. In reality, increasing unemployment through lowering hiring largely follows the same playbook as previous recessions.

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.