Cost-Push or Demand-Pull? The Implications of *How* The Labor Market Affects Inflation

In the coming weeks, we hope to discuss in greater detail what kinds of labor market and inflation outcomes the Fed should be aiming for. Here is an initial layout of how some of our macroeconomic views tend to differ from senior Fed officials.

The Fed has increasingly gone back to its roots, embracing a cost-push Phillips Curve view of how the labor market primarily affects inflation. That view involves:

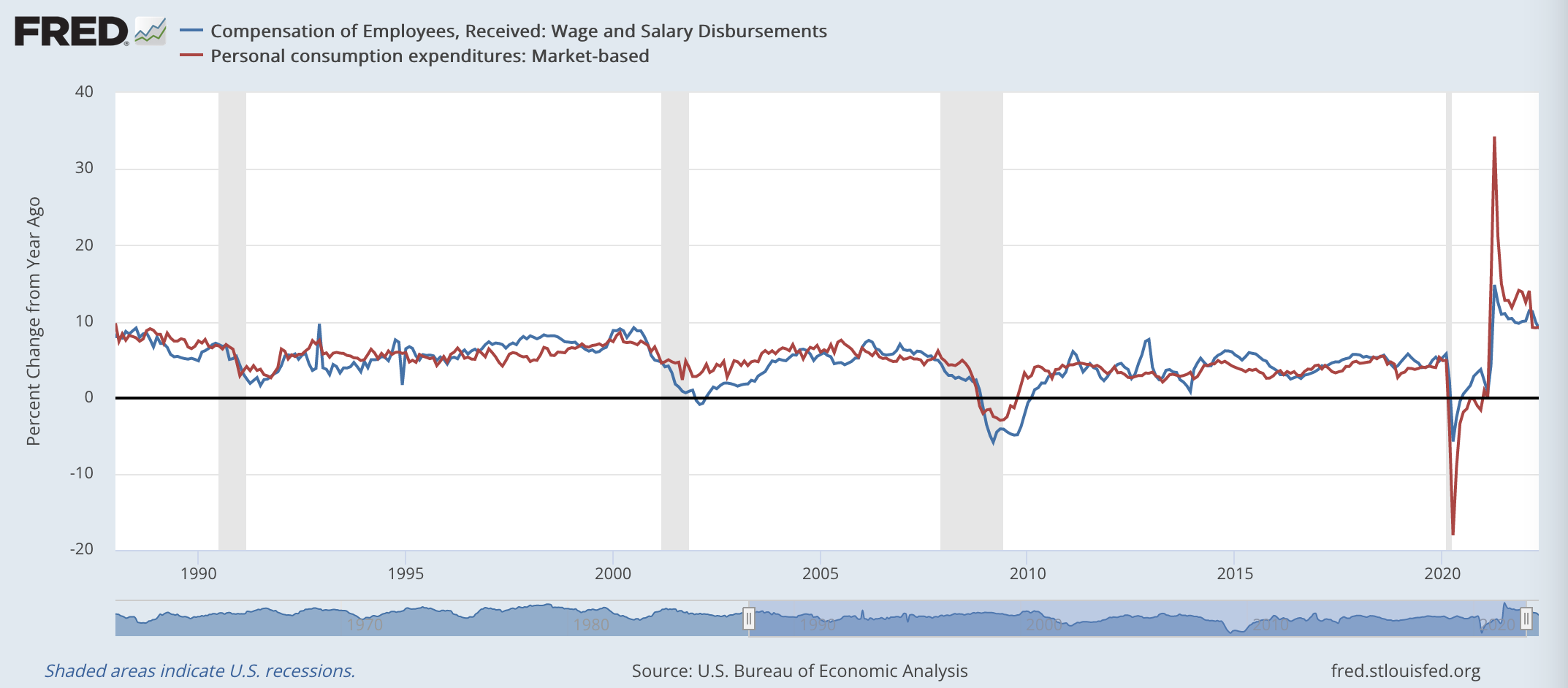

We are not denialists about the relevance of labor market conditions, but we subscribe to a different view of how the labor market primarily affects inflation, what we will call a demand-pull view. Labor incomes are the major and marginal funding source for household consumption. Stronger gross labor income growth—which is really just job growth plus wage growth—puts more demand-side pressure on aggregate nominal consumption growth. This in turn pressures consumer price inflation at the margin.

These two dynamics may seem like two sides of the same coin: complementary mechanisms that have equivalent implications for how the Fed should respond to labor market dynamics. But when it comes to how the Fed should react to incoming information under uncertainty, the two channels emphasize different sets of data for shaping the Fed's policy reaction function.

The Cost-Push Phillips Curve View: The Fed is clearly unsatisfied with job growth merely slowing. Fedspeak and Fed projections make clear they are aiming for higher unemployment within the current calendar year, at a scale which would only be consistent with outright job loss. Why? Under a static Phillips Curve model of wage growth, the pace of nominal wage growth is—to a first approximation—determined by the level of unemployment. Slower job growth should directly lowers gross labor income growth assuming fixed wage growth, but Phillips Curve models of wage growth make the alternative assumption.

The Demand-Pull View: Job growth has already been slowing this year; that much we know. If you're not so confident about what drives wage growth over time, and you think it might move somewhat independently of a static Phillips Curve model, then the consumption-decelerating effects of slower job growth are more compelling. Lower job growth translates into lower aggregate household income growth, and that should lower aggregate consumption growth.

Aside from the unemployment rate and wage growth, there are other measures of prices and other points of economic data worth tracking to see how the labor market may (or may not) be affecting the inflation outlook.

The Cost-Push Phillips Curve View: The Fed has explicitly embraced a new special aggregate of consumer prices, Core Services Ex Housing PCE. CSXHP is meant to be a proxy of for how labor costs feed into (allegedly) labor-intensive prices. The fact that it has mildly risen but used to be more inertial is now being offered as proof positive that the labor market has caused permanent damage to the Fed's aspirations of hitting the inflation target.

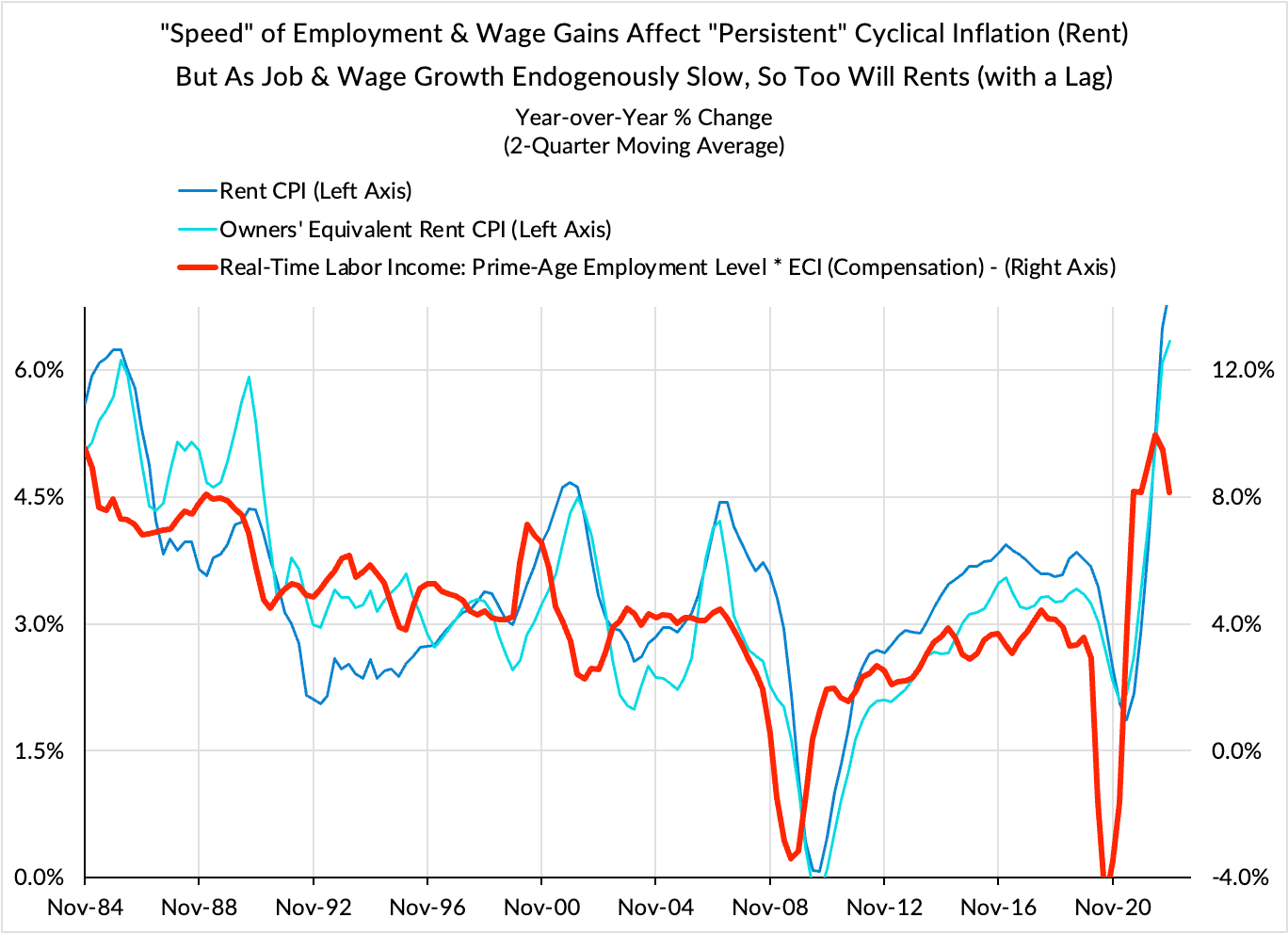

The Demand-Pull View: When the Fed first suggested looking through (rental) housing services inflation, most were probably heartened by the notion that the Fed would "see through" the lagged nature of the measure and show more policy flexibility. But in its full context, the Fed is making a more questionable policy judgment that housing services are not as sensitive to labor market conditions as other services prices. This claim does not hold up well empirically. Job growth and wage growth—when taken together—are excellent predictors of the trajectory of housing PCE inflation, especially since the inflation methodology smooths through some of the volatility associated with real-time market rent measures.

What we hope to find out in the coming months is the pace of labor income growth that is sufficient for bringing inflation down to more desirable rates. But that hope may go unrealized if the Fed is keen to aim for something much worse and act with sufficient speed and scale. Fed's view is leaning on 1) a misguided price aggregate, 2) a lagging measure (wage growth), and 3) a deeply unsettling goal for the unemployment rate.

Our own compass involves tracking data that is 1) more robustly sensitive to labor market conditions, 2) more timely (job growth, nominal consumption growth), and 3) more open to pathways that do not involve recessionary outcomes. Let's hope the Fed does not inadvertently foreclose the non-recessionary pathways that still could prove well within reach.