Q4 ECI Preview: Coincident Data Suggests Slowing, But Noise & Lags Risk Hawkish Overreaction

As we await the Q4 Employment Cost Index (ECI) release tomorrow (forecasting consensus: 1.2% QoQ, 4.9% CAGR; Q3: 1.2% QoQ, 4.8% CAGR), two key points to keep in mind.

Actual Economic Implications: A number of measures of nominal income and spending growth are already confirming a normalization back toward pre-pandemic growth rates. This basic fact should soften the urge to panic about the inflationary implications of an upside ECI surprise.

Fed Implications: The Fed's wage-cost-push view of inflation makes ECI a more high-stakes release now than it otherwise should be.

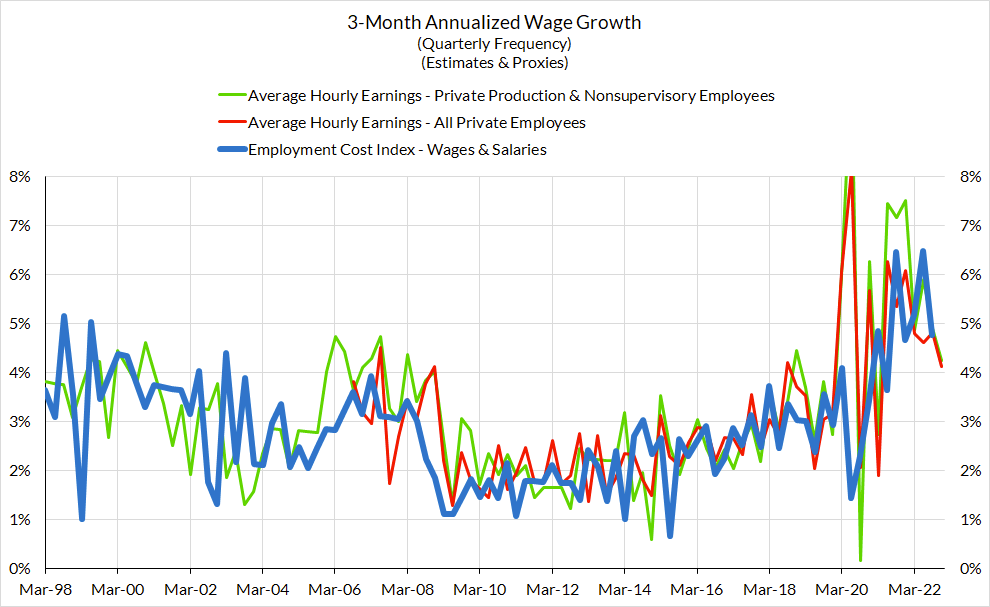

Tomorrow's Employment Cost Index number plays an outsized role in labor market assessments, both for the Fed and for ourselves (albeit for different reasons). Among the government-provided measures of wage growth, ECI has the fewest blindspots and biases for the purpose of real-time business cycle interpretation.

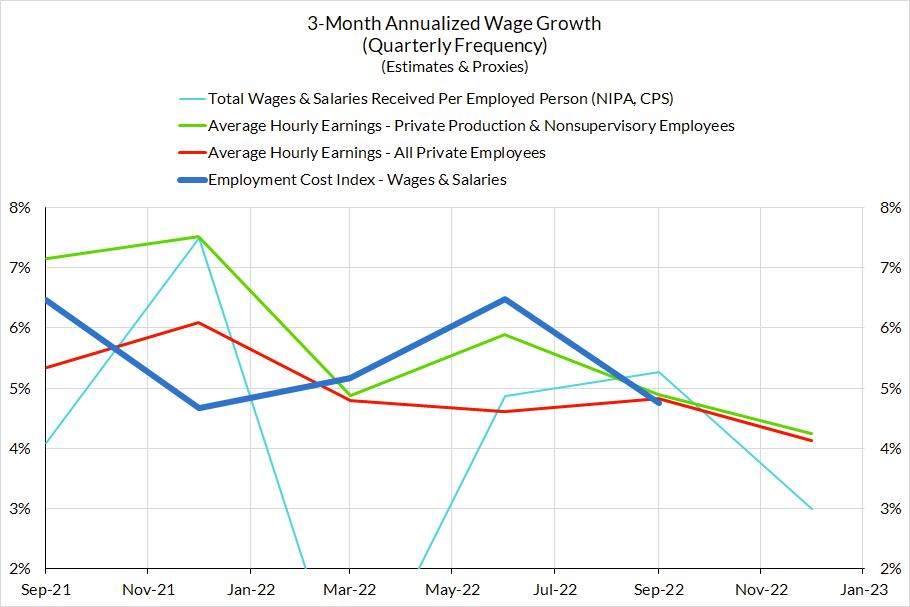

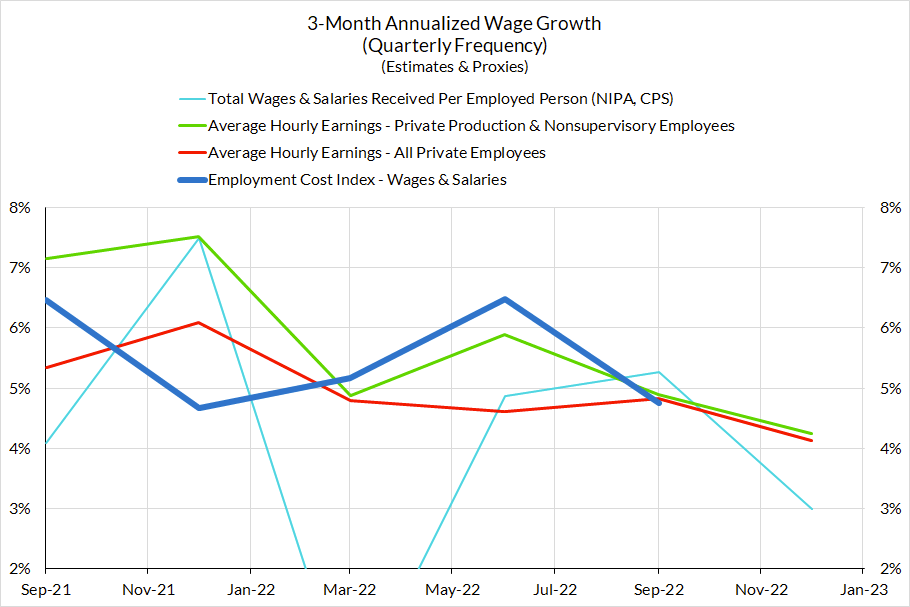

To start with, the data is generally showing a slowing pattern in Q4. Dividing aggregate labor income by total employment or hours worked is vulnerable to composition biases. These measures of "average wages" are far from optimal when making business cycle judgments, but these composition biases should be less aggressive for 2022Q4 (in comparison to periods of recession and rapid recovery). Taken at face-value, annualized ECI growth would be on track to decelerate close to 4.2% annualized in 2022Q4.

But the longer history of ECI give ample reasons for caution when engaging in such crude nowcasting heuristics. There can be substantial divergences between each of these measures in any given quarter.

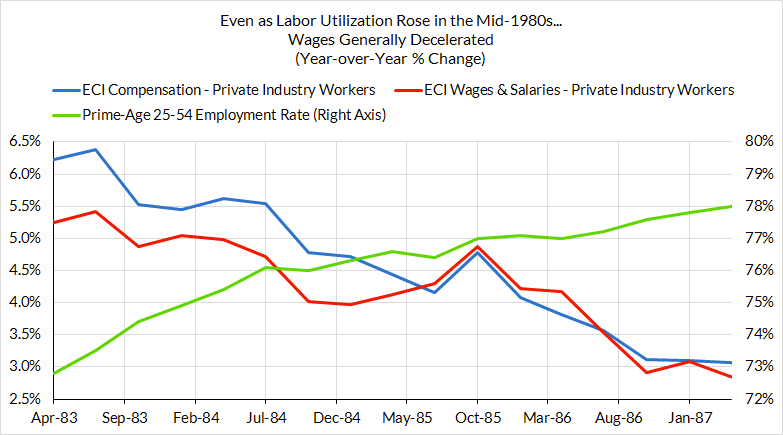

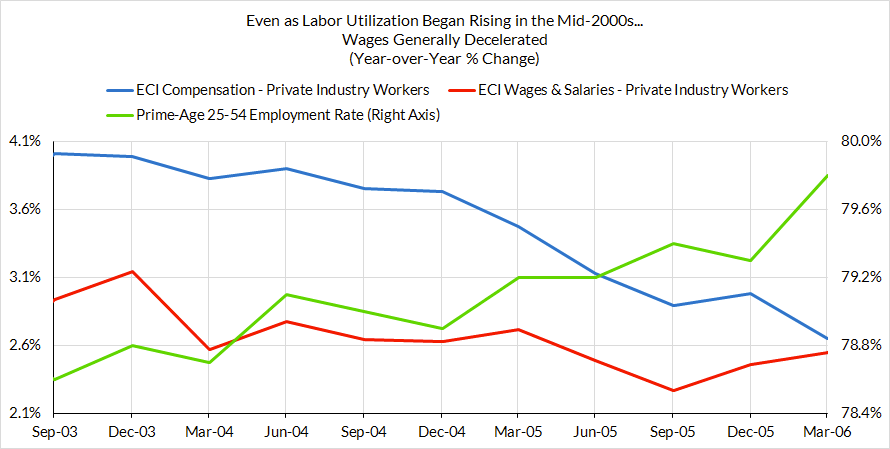

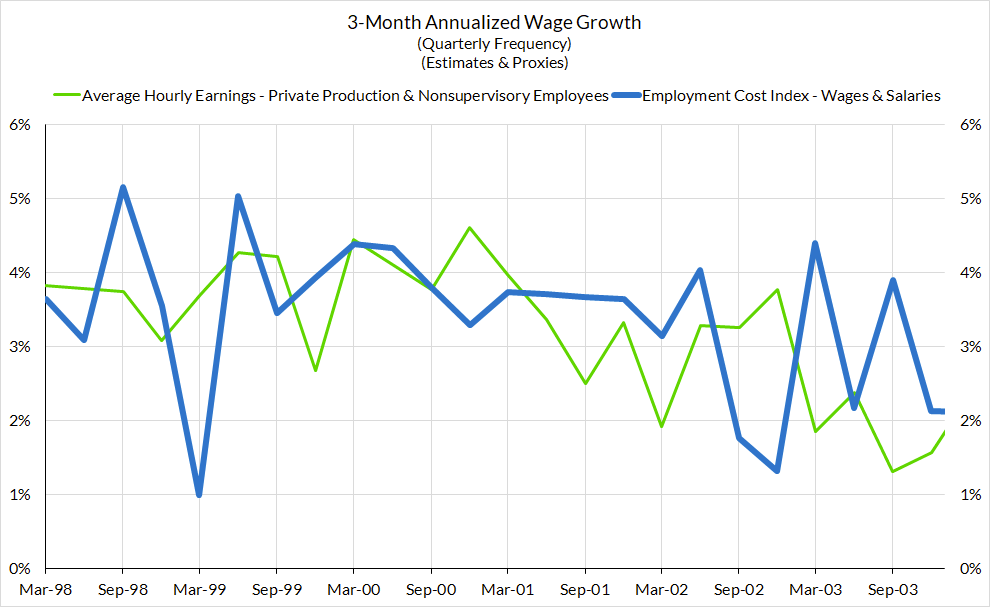

Look closely at the 2000-2002 period and you'll see that ECI growth was especially sticky in the face of underlying economic and labor market deceleration that was transpiring.

With all of these factors in mind, it is best to be prepared for surprises on both sides of the forecasting consensus. And the biggest risk stems from Fed misinterpretation and overreaction to an upside surprise.