February FOMC Preview: Will the Fed Update its Model of the Labor Market?

A lot has changed in the last six weeks.

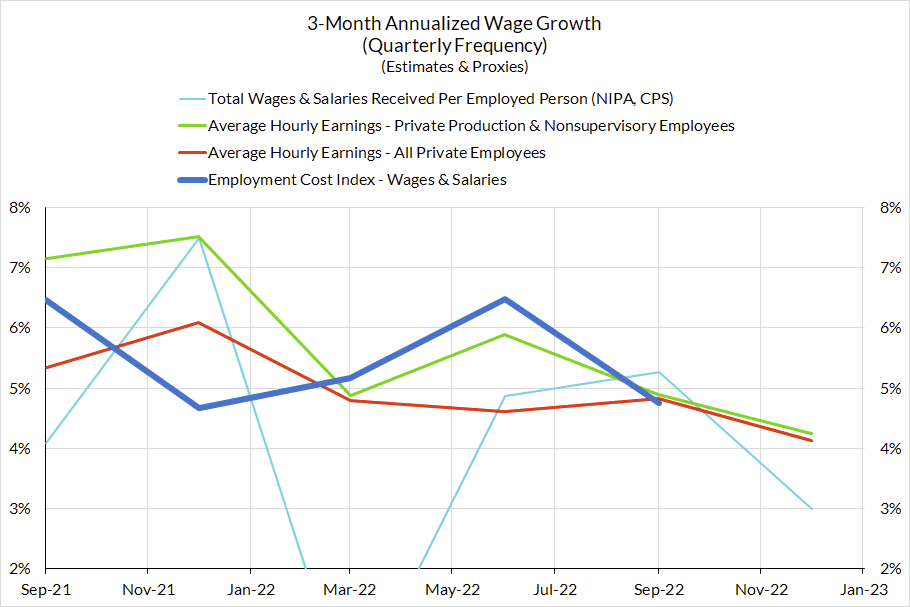

This week’s meeting coincides with a deluge of labor market data, and the Fed will see new data from the Employment Cost Index (ECI) release on Tuesday and JOLTS on Wednesday

We wrote previously about how the Fed’s December projections are consistent with them trying to engineer a recession. We think this is neither necessary nor desirable, but the Fed has been operating on a framework based on three faulty premises:

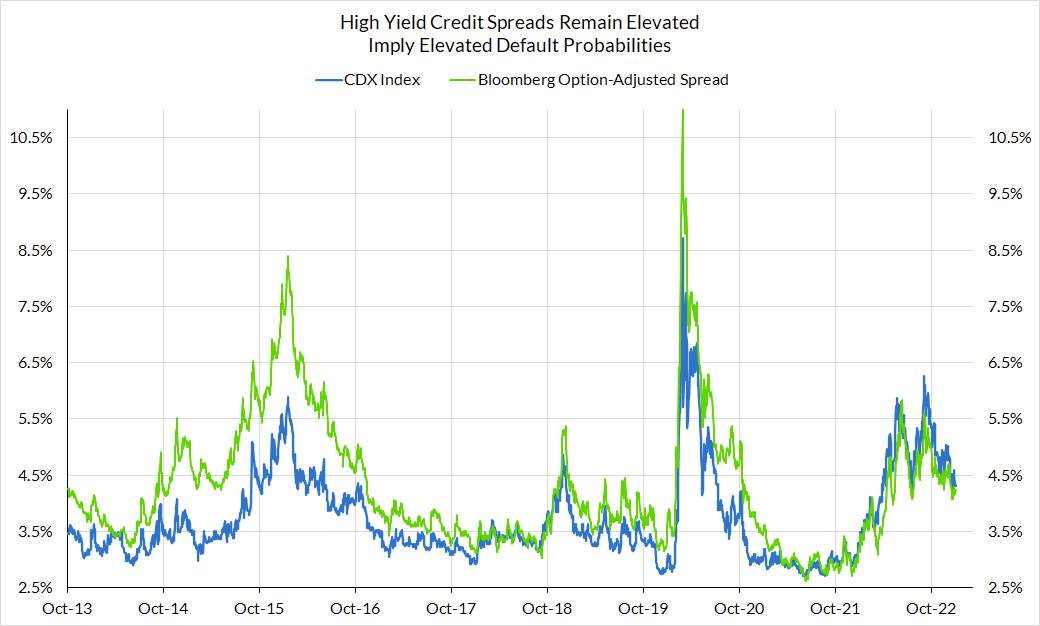

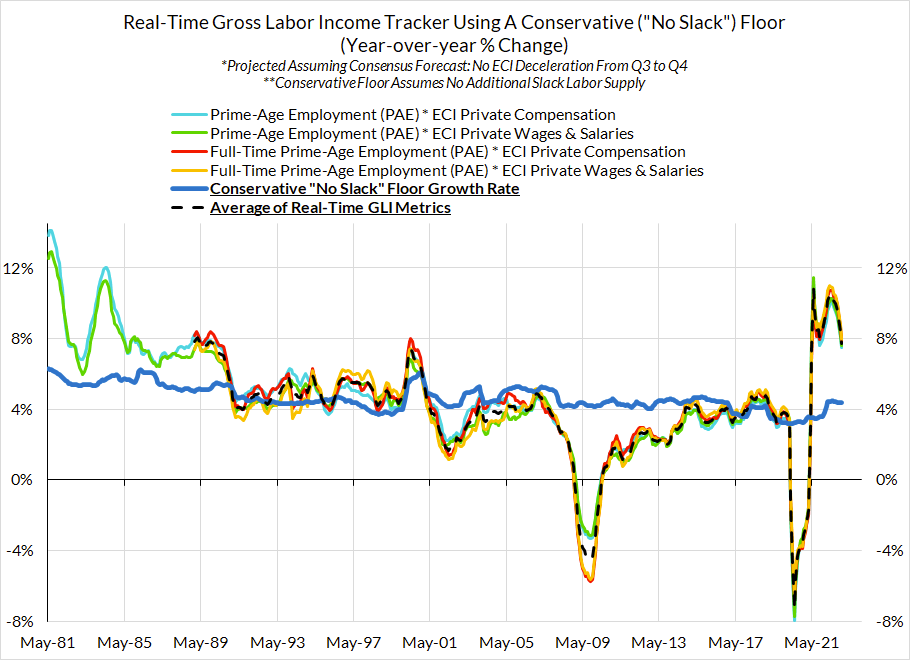

Since the last meeting, new data and revisions have shown that disinflation is possible even as the labor market remains strong, since labor income growth is slowing and returning to its pre-pandemic growth rate. We hope the Fed recognizes that it has been operating on a faulty model of the labor market’s relationship to inflation and adjusts accordingly by signaling that it no longer sees the above chain of events as the primary description of what drives inflation. Before the last meeting, we wrote that the risks to the outlook are “increasingly balanced.” Since then, the inflation-side risk has subsided substantially, and the Fed should look to loosen financial conditions accordingly.

FOMC Member |

Latest Comments |

Comments as of Previous SEP |

|---|---|---|

Jerome Powell |

The Fed's tools work, and there is nothing wrong with our mandates. January 10, 2023 |

The Fed has been pretty aggressive, but it does not feel it appropriate to crash the economy and clean up afterwards. November 30, 2022 |

Lael Brainard |

More two-sided risks develop as we move deeper into restrictive territory and we're now in an environment where there are risks on both sides. January 19, 2023 |

Continued supply shocks may force central banks to tighten policy in order to manage risks. November 28, 2022 |

Michelle Bowman |

Allowing inflation to persist has far greater costs and risks. January 10, 2023 |

We are not seeing a significant impact on inflation reduction, they are still at high levels and i need to see our actions have an impact. December 1, 2022 |

Michael Barr |

It is a mistake to believe that changes in the pace of rate hikes indicate a shift in the Fed's commitment to a 2% inflation target. December 1, 2022 |

The Fed's policy rate will have to remain high for a long period of time. December 1, 2022 |

Lisa Cook |

Despite recent encouraging signs, inflation remains far too high and of great concern. January 6, 2023 |

Wage growth is above levels that are consistent with the Fed's 2% inflation target. November 30, 2022 |

Philip Jefferson |

Low inflation is critical to achieving long-term growth. November 17, 2022 |

Low inflation is critical to achieving long-term growth. November 17, 2022 |

Christopher Waller |

I favour a 25-basis-point rate hike at the upcoming meeting, followed by additional policy tightening. January 20, 2023 |

Rates still have a long way to go and will require increases into next year. November 16, 2022 |

President John Williams |

Us inflation remains too high, and the Fed has more work to do on rate hikes. January 19, 2023 |

The Fed has a long way to go with rate hikes. December 1, 2022 |

FOMC Member |

Latest Comments |

Comments as of Previous SEP |

|---|---|---|

Evans (Chicago) |

We are likely to have a slightly higher peak to Fed policy rate even as we slow the pace of rate hikes. December 2, 2022 |

Following the September CPI, I view a policy rate of 4.5 to 4.75% as suitable for next year. October 19, 2022 |

Harker (Philadelphia) |

The worst of the inflation spike is likely past now....the time of super-sized rate hikes has passed. January 12, 2023 |

The Fed will raise rates for a while. October 20, 2022 |

Logan (Dallas) |

The process of cooling off the economy is just getting started. The FOMC must to everything in its power to restore price stability. November 10, 2022 |

|

Kashkari (Minneapolis) |

It is appropriate to continue interest rate hikes at least at the next few meetings until we are confident that inflation has peaked. January 4, 2023 |

My best guess is that the Fed can pause rate hikes some time next year. October 19, 2022 |

Bostic (Atlanta) |

Until inflation is on track to 2%, the Fed has to resist the temptation for rate cuts even if economy weakens. November 19, 2022 |

On speculation of rate cuts in 2023: Not so fast. October 5, 2022 |

Daly (San Francisco) |

No evidence of a wage price spiral. November 21, 2022 |

It is important that we slow our rate hikes. We will do a step-down, not to pause, but to 50 or 25 bps increments. October 21, 2022 |

Barkin (Richmond) |

It won't be easy to try to get demand back into balance, especially with household excess savings and fiscal stimulus. December 2, 2022 |

A more inflationary environment suggests tighter Fed policy. October 3, 2022 |

Mester (Cleveland) |

Fed rate cuts are not timed according to a calendar. December 16, 2022 |

We must continue to raise until we achieve positive real rates. October 11, 2022 |

Bullard (St. Louis) |

The current Fed policy rate is not quite restrictive; it should be at least 5%. January 12, 2023 |

If inflation begins to fall meaningfully in 2023, the Fed can maintain where it is at higher rate level. October 19, 2022 |

Collins (Boston) |

I think 25 or 50 would be reasonable; I’d lean at this stage to 25, but it’s very data-dependent. January 11, 2023 |

Inflation is most likely nearing or has already peaked. September 26, 2022 |

George (Kansas City) |

As the labor market softens, the Fed will face difficult communications and difficult choices. January 6, 2023 |

I am in favour of slower and steadier rate increases to allow time to see lags in our policy. October 14, 2022 |