As everyone is watching for signs of recession, some are warning that weakness in surveys like the ISM Manufacturing PMIs indicate an imminent recession. Since expectations play a major (and multi-faceted, as one can have expectations about all sorts of things) role in investment and employment...

The following is the type of analysis usually shared on our high-frequency descriptive analysis distribution exclusively for Premium Donors. If you are interested in supporting our content and would like more frequent access to pieces like this, please consider becoming an Employ America Premium Donor. You can start your 30-day free trial of exclusive bonus content here or contact us for more information.

As everyone is watching for signs of recession, some are warning that weakness in surveys like the ISM Manufacturing PMIs indicate an imminent recession. Since expectations play a major (and multi-faceted, as one can have expectations about all sorts of things) role in investment and employment decisions at the firm level, it’s important to understand how business leaders are thinking.

However, it’s also critical to put information about those expectations in proper context. We are not really in a “normal” business cycle position right now — the goal on some level should be to transition from the “No Landing” scenario to steady growth, rather than slide into an “inevitable” recession. With this in mind, it’s interesting that over the first half of the year, we have seen a growing disconnect between “soft” data on sentiment — whether business or consumer — and “hard” data on the money spent by firms and households on employment, investment and consumption.

On the one hand, nominal GDP is still growing, labor markets remain tight, and investment is steady as the Biden administration rolls out the first wave of industrial policy investments. On the other hand, the Fed has hiked more than 500bp in the fastest tightening cycle in decades while consumer and business confidence have dropped.

At the same time, supply chain snarls are sufficiently resolved for nearly all sectors — aside from certain semiconductors and electronic components — to report shorter lead times for inputs. Firms are also suggesting a strong intention to spend on capital investments now that the helter-skelter pandemic rush has ended and the post-pandemic uncertainty about the macro environment has begun to dissipate.

Overall, we may be seeing the beginning of a meaningfully new regime within macro — and in the structure of business’ responses to the macro environment. Where the fiscal response to the 2008 recession looks increasingly insufficient, the fiscal response to the pandemic seems to have jump-started firms’ beliefs about expected demand, and thus their attitude towards further capital investment.

ISM Services

Services are upbeat, and consumer spending is rising steadily. The sector is growing, with growing employment alongside anecdotes that suggest firms are still looking to expand. In the words of one survey respondent: “Finally able to fill some positions that have been open for some time.”

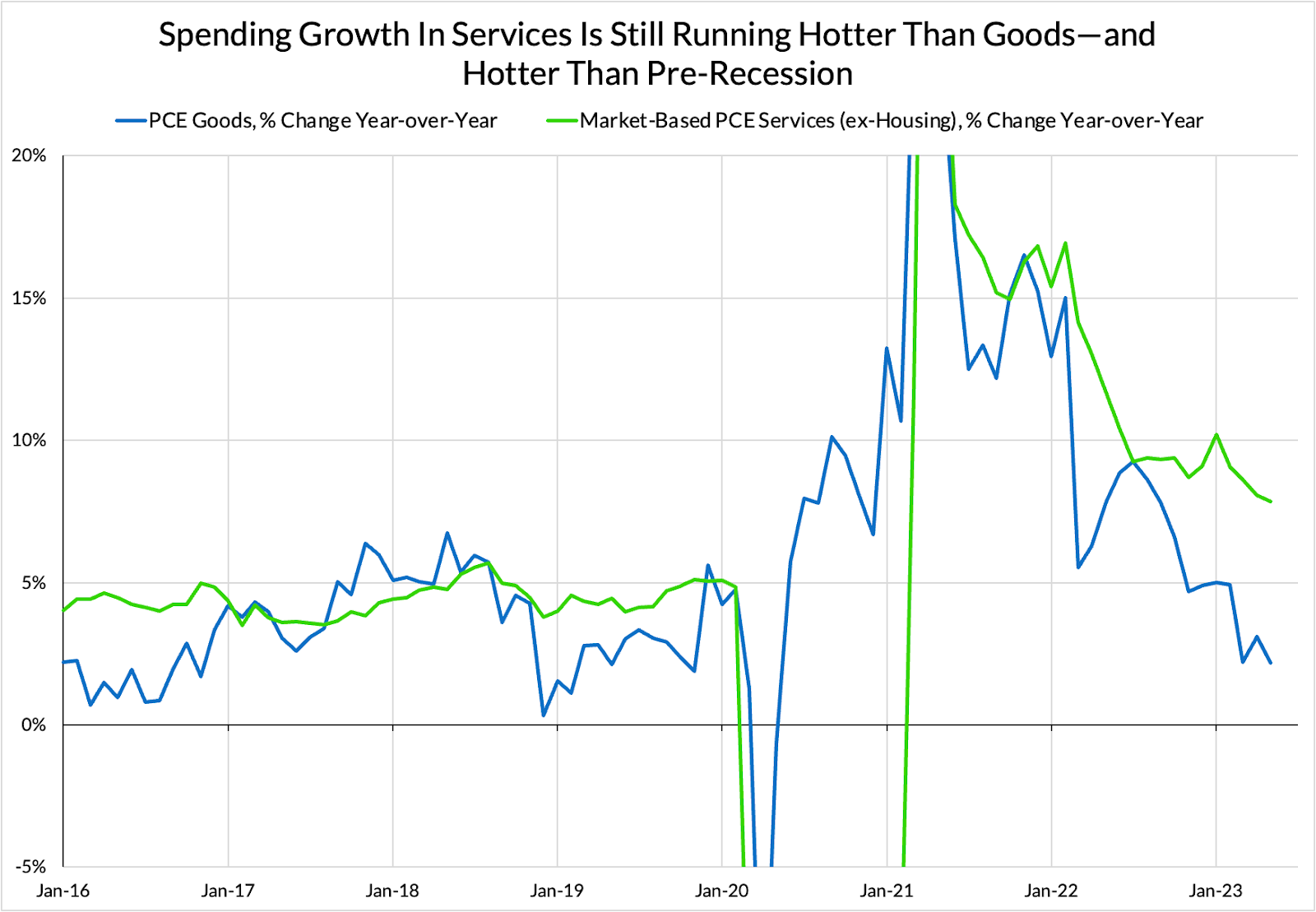

There is very little here to suggest we need to look closer at the recession question on the services side. But we see growth in goods consumption falling back to, and even below, pre-recessionary growth rates.

ISM Manufacturing

Here, the soft data suggests recession to many. Topline ISM Manufacturing PMIs are consistent with a substantial contraction, but the investment announcements keep coming even as companies continue to worry about a coming downturn.

In this past month’s Dallas Fed Manufacturing Survey, one respondent in the computer and electronics manufacturing industry went so far as to say “we intend to hire more people and embark. on a significant capital improvement project (including new building, new manufacturing equipment) so that we have capacity available as soon as the economy starts to recover after the recession that everyone is predicting.” Rather than seeing “a recession” as a reason to cut costs and lay off staff, firms are beginning to expect a “natural” recovery in demand that makes “a recession” a cheaper time to invest, build and grow.

A second contributing factor may be firms adapting to the expectation of demand-side “bullwhips” that the pandemic environment so frequently created. The traditional bullwhip story on the demand side is one where small changes in final demand can induce major changes in price, which then induce major changes in production. Once the demand shifts back down in this story, the firms which changed production are left high and dry as there is no longer demand to validate the earlier investments.

However, if the firms parcel out the tsunami of incoming demand over the pandemic into a deeper and deeper order book, they can continue to work at a steady pace even when those new orders begin to seriously dip. This is interesting too, because it suggests that the “bullwhip” effect may work itself out differently depending on how the supply side reacts.

Supply and Demand can move quickly — especially within specific sectors or product markets — but capacity can’t. Capacity especially couldn’t during the pandemic, when supply chain disruptions significantly constrained firms’ abilities to quickly scale up production. The situation was frequently even worse for capital goods producing industries which rely on large numbers of highly varied specific parts. Backlogs in one or two pieces were enough to put the entire production on pause for a wide range of manufacturers.

So firms aren’t necessarily facing the usual pre-recession position where worries are about the forward profitability of investments made during the bull run or in response to temporary bullwhip factors. In fact, they seem increasingly confident that demand will bounce back following any recession. Government spending and transfers to support incomes during the pandemic quickly becomes earnings for firms as consumers buy things, providing a balance sheet refresh alongside indication of stable demand. Because of this, one could read their current situation as one where the pandemic-era rush to restock on oversold consumer goods has ended, and firms are just now able to dust themselves off and begin investing in repairs and maintenance, which will be capacity and productivity-enhancing in the longer term.

The above story is consistent with the key points in recent PMIs, especially this past month. The slowdown in new orders was largely expected; the question is going to be how firms approach it.

Order backlogs are shrinking, but a simple dispersion index like the PMIs does not explain how much. We know there are still industries with months and years-long backlogs. To take one example at random, as of the start of the year, Airbus has roughly ten years worth of order backlogs at their current pace of production.

To take another, look at Class 8 Trucks. As I argued, despite worries in the spot trucking market, the sector as a whole was set up for robust continuing investment. That has played out, even as new orders have slowed dramatically. The backlogs drop in response, but they are deep enough that manufacturers are keeping their order books largely closed for the remainder of the year. That is not the mark of a demand-constrained environment.

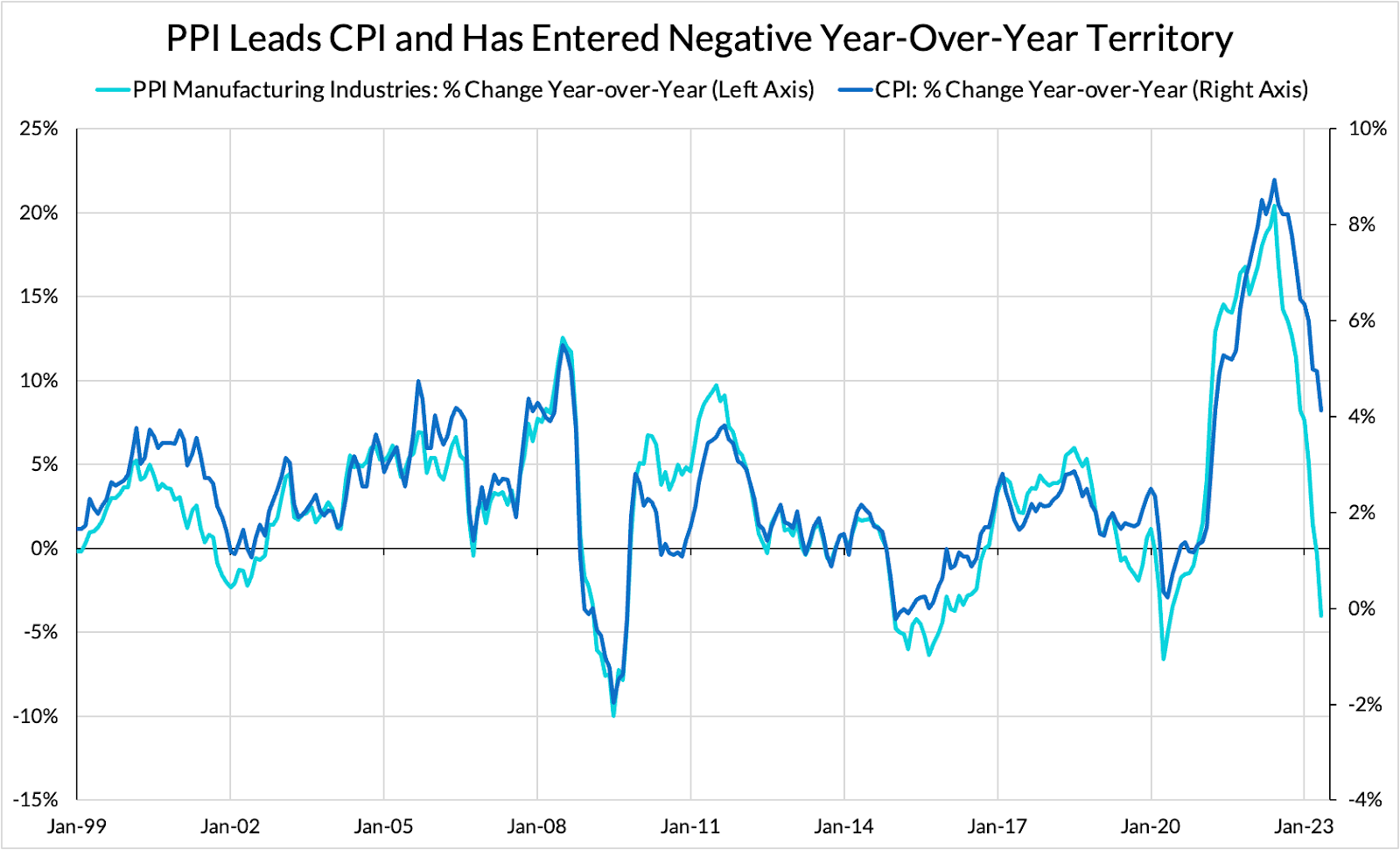

Also critical: input prices are down for every industry with the exception of Textile Mills; Nonmetallic Mineral Products; and Computer & Electronic Products. This tracks information we have been getting from the PPIs: producer prices are coming down.

This is good for a wide range of reasons.

It’s an indication that supply chains are healing.

A decrease in uncertainty about forward Cost Of Goods Sold is always good for businesses looking to ramp up production.

Mechanically, it will feed through to lower PCE price index readings, which are good for the Fed’s ability to achieve its inflation goals.

Falling or lower prices for upstream inputs are a key turning point for future falls in CPI measured prices, as the following chart suggests.

Manufacturing PMIs may seem downbeat, but they are not quite the harbinger of recession they would be expected to be during a more normal business cycle.

What This Might Mean

Employment and Investment may begin to detach from measures of business and consumer confidence in today’s environment. Maintaining a clear read will require more data and analysis than just sentiment indicators.

Despite the Fed’s apparent intent to hike rates until inflation falls, the supply side seems to be actively looking to learn the lessons of the brittle supply chains and physical capacity shortage and adjust to meet a higher level of demand. How firms adapt to a strong demand environment if rates remain elevated will be an interesting test of a wide range of theories.

Where the 2008 response was insufficient, and led to multi-dip recessions as liquidity continued to dry up despite interventions in the banking system, the pandemic response was sufficient to persuade firms of the viability of further capital investment. If this remains the case, expect to see a materially different macro environment with different dynamics compared to the ten years prior to the pandemic.

Even if private sector manufacturing slows in response to the still-strong expectations of recession, that may simply make more room for the Biden Administration’s industrial policy programs to take up capacity without bidding up prices.

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.