Quits vs. Openings: The Fed Needs To Choose Wisely

For months now, the JOLTS job openings have told a divergent story from other labor market indicators, such as quits, hires, and employment-based measures. This month’s data release is no different. While all labor market indicators show a strong labor market, the difference is one of magnitude: the job openings data point to a far tighter labor market. The ratio of job openings to unemployed is now 1.90, far above its pre-pandemic peak of 1.24. Meanwhile, the quit rate continued to fall and is now 2.5%, just off its pre-pandemic peak of 2.4% (even that may be overexaggerated). Hires, too, are near pre-pandemic levels.

The Fed has put a lot of weight on the job openings data. Throughout 2022, Powell consistently referenced the ratio of job openings to unemployed at FOMC statements. But, as quits started to fall more towards pre-2020 levels while job openings remained at very high levels, Powell began to deprioritize it:

We talk a lot about vacancies in the—vacancy-to-unemployed rate, but it’s just one, it’s just another data series. It’s been unusually important in this cycle because it’s been so out of line. But so has quits. So have wages. So we look at a very wide range of data on the unemployment—on the labor market.

Jerome Powell, November 2nd, 2022

Meanwhile, wage growth, while still high, has decelerated substantially over the latter half of 2022. This is consistent with the quits data, but not the elevated level of job openings.

At this point, the Fed needs to pick a side. Do they believe the job openings data, which suggest that there is some sort of structural shift in the Beveridge Curve that should lead one to believe that the “natural rate” of unemployment is substantially higher than before, and that we need to crush employment to bring the labor market “back into balance”? Or will they rely on the other labor market data, which have been pointing to a strong labor market that is steadily cooling?

We have written before that there are good reasons to distrust the job openings data. The first is conceptual; job openings, as measured by JOLTS, don’t tell the whole story. Crucially, they don’t contain any information about recruitment effort, which microevidence has shown to be a crucial determinant of actual hiring behavior.

Empirically, the strongest evidence for job openings came from the fact that the large increase in inflation in 2021 coincided with a similarly large increase in job openings. Some economists have looked to this phenomenon as evidence that job openings are the most relevant labor market indicator in the post-COVID economy. But, as we’ve written before, a reliance on the post-pandemic data to differentiate between job openings and quits is reliance on mere coincidence. Using pre-pandemic data only is highly sensitive to the specification of the empirical tests.

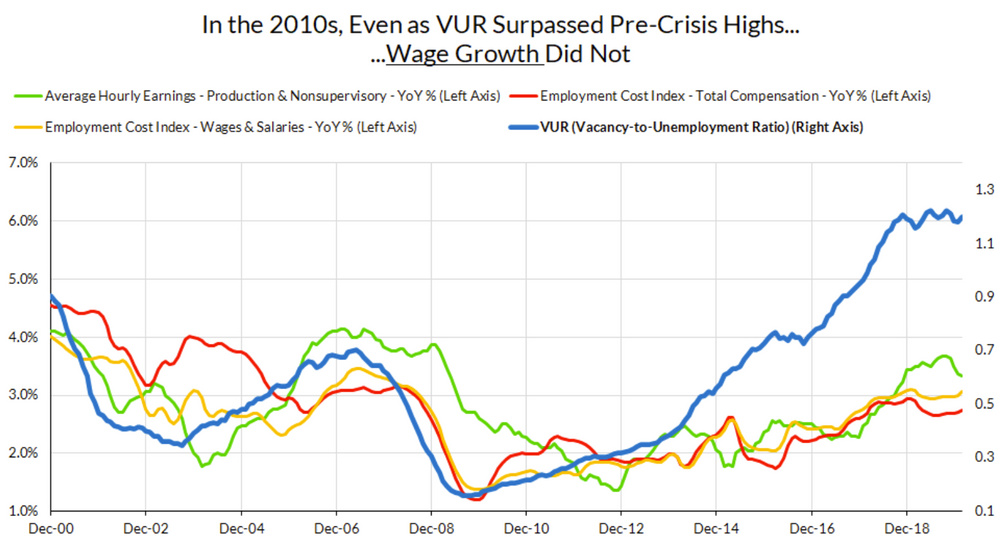

One need only look to recent history to see another example where job openings would have predicted runaway wage growth and inflation—the 2010s. After the Great Recession, there was an observed shift in the Beveridge Curve.

If the Fed is going to continue emphasizing the job openings data, they need to explain why elevated job openings are a problem today, but weren’t a problem five years ago. As Justin Bloesch has pointed out, there isn’t any corroborating evidence pointing to a decrease in matching efficiency. Meanwhile, there is a mounting pile of evidence that the labor market, while still strong, is cooling and heading back towards its less inflationary pre-pandemic state.