We are glad to see President Biden taking steps to alleviate the oil shortage, including domestic supply-side measures. Commodity shortages are a tricky issue that combine macroeconomic stabilization with geopolitical, physical capacity, and environmental constraints. As such, policy made in response must be able to address each of these sticking points. The Strategic Petroleum Reserve (SPR) release of 180mm barrels over the next six months has already induced some measurable declines in oil prices and specifically reduced the premium associated with the spot price of oil relative to prices for delivering crude oil further out in time (according to the current curve for futures contracts).

While we applaud the administration’s stated intent to use proceeds from the release to replenish the SPR in the future, more tangible action is necessary to get to the heart of why producers are holding back. The recent SPR action is a release – not an exchange – which means the Administration has yet to enter into contractual obligations that incentivize future oil production (to help refill the reserve). The problem is not just that there is an oil shortage driving spot prices up today. The real problem is that the spot price of oil won’t come down in the future without substantially more investment.

The value of an SPR release–which we conditionally welcome–is that it serves as an immediate funding source for the SPR to acquire future barrels of oil, thereby raising the incentive for domestic exploration and production companies (E&Ps) to invest today—all without requiring a fresh appropriation from Congress. The spot price of West Texas Intermediate–roughly $100–is still over 13% above the price of oil deliverable even just 1 year from now. Even on the narrow criteria of “making the taxpayer a tidy return,” the Administration’s optimal action remains the same: announce that it will enter into contracts to purchase future barrels of oil as soon as practicable. Simply waiting for the spot price to come down does nothing to guarantee that prices at which the SPR purchases oil will actually come down.

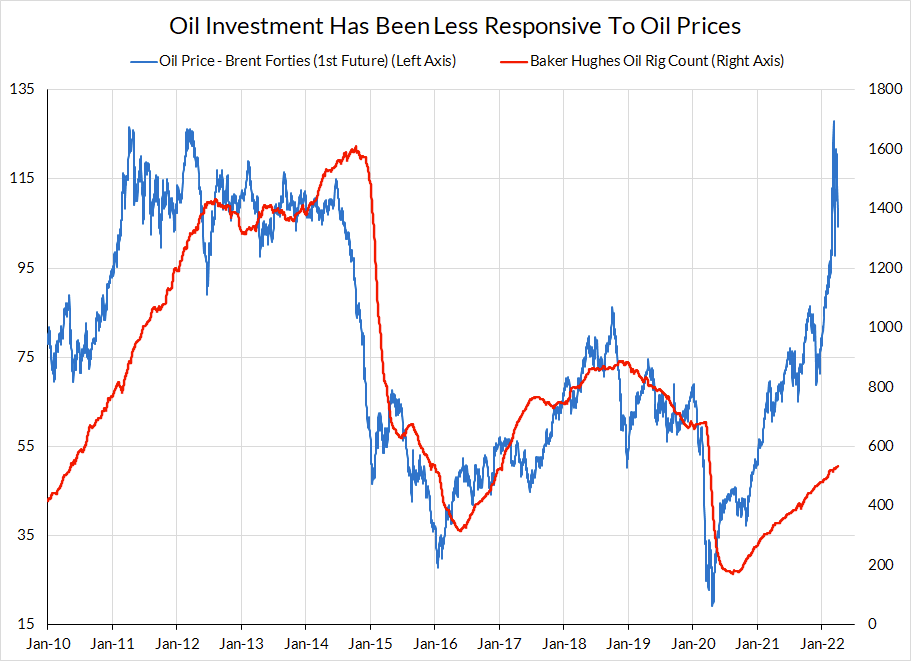

Since the development of fracking, oil has repeated the same boom-bust cycle multiple times: high prices draw investment, investment creates excess capacity, excess capacity drives down oil prices and those investments no longer pay off. The most recent crash was the most extreme, with oil prices turning negative in spring 2020 as demand collapsed early in the pandemic and OPEC members aggressively raised production. Investors have learned their lesson, and are making the rational and financially prudent decision to constrain investment. Many factors can impact investment decisions, but a large majority of executives have explicitly cited one factor over others to explain the stingy production response—“investor pressure to maintain capital discipline.” This means producers are adding less capacity than the current oil price would lead one to expect, as active rig counts reflect. As a consequence of this decision, oil prices are liable to remain higher for longer.

Ultimately, investors are looking out for shareholder interests. While shareholder interests can often be aligned with the interests of the economy at large, in this case there is a misalignment.

To incentivize E&Ps to make the necessary investments on a timeline that provides stabilization to the market, there is much more the Administration can do today to provide certainty. The Administration should make use of all of its tools in concert – as outlined in the original Employ America plan – to remove uncertainty and smooth returns for oil producers, ideally in exchange for catalyzing additional investment. The first step to enter into contracts for future barrels of production as soon as practicable. This would lock in lower prices, but more importantly, provide a critical source of guaranteed demand associated with new investment today.

While it might be tempting to only make such purchases at a later date when spot prices may have fallen, doing so would only make sense if the proximate constraint were time alone. One senior official has been quoted as saying, “the bottom line is we are committed to doing so [refilling SPR] …when prices come down.” The problem with this policy is that it risks assuming a reality–falling oil prices–that is far less likely to occur if the SPR does not initiate contracts for future barrels of oil. The most proximate constraint to greater domestic oil production is investment intentions. There is no good explanation given for why spot crude oil prices will simply fall further on their own, especially given the likely declines in Russian supply. If producers continue to invest slowly rather than all at once, spot prices may remain elevated and the Administration could end up losing substantial money on the deal as a whole. This would be an unnecessary embarrassment and may potentially dissuade future governments from acting to stabilize commodity markets.

While the Administration’s initial actions point in the right direction, they remain incomplete. A release from the SPR is an important plank in the overall program of bringing down today’s oil prices. Building on these successes by entering into acquisition contracts as soon as possible will support greater oil price stability over a longer time horizon. It would be complacent to claim victory; the SPR release is only the first step in a more comprehensive strategy.