Closing In On A Key Milestone For The Fed's "Maximum Employment" Forward Guidance

If the Fed wants to stay true to the "maximum employment" component of its forward guidance, and the "broad and inclusive" nature of that goal, it is imperative that their interest rate policy actions reflect a full recovery on both of these measures.

Friday's Jobs Report for November shows rapid progress in the quest to return to the pre-pandemic labor market. The prime-age 25-54 employment rate gained 0.5% in November alone and now stands just 1.5% below its 2019Q4 level and 1.7% below its peak monthly level. In the next two jobs reports, the momentum we see today together with upcoming seasonal factor revisions will likely narrow the remaining employment gap even further. This adds up to an impressive bottom line: the prime-age 25-54 employment rate may see a full recovery as early as 2022Q2!

Some commentators have claimed that the Fed's preconditioning of interest rate increases on the achievement of "maximum employment" has been a mistake and, by implication, that lower demand support, a slower recovery and a longer period of depressed employment rates would have been preferable. To American workers, that view might seem jarring. However, it is remarkably consistent with the consensus policymaking view during the previous three recoveries from recessions: a high tolerance for labor market stagnation and a low tolerance for any inflation risk that might stem from a rapid recovery in employment and output.

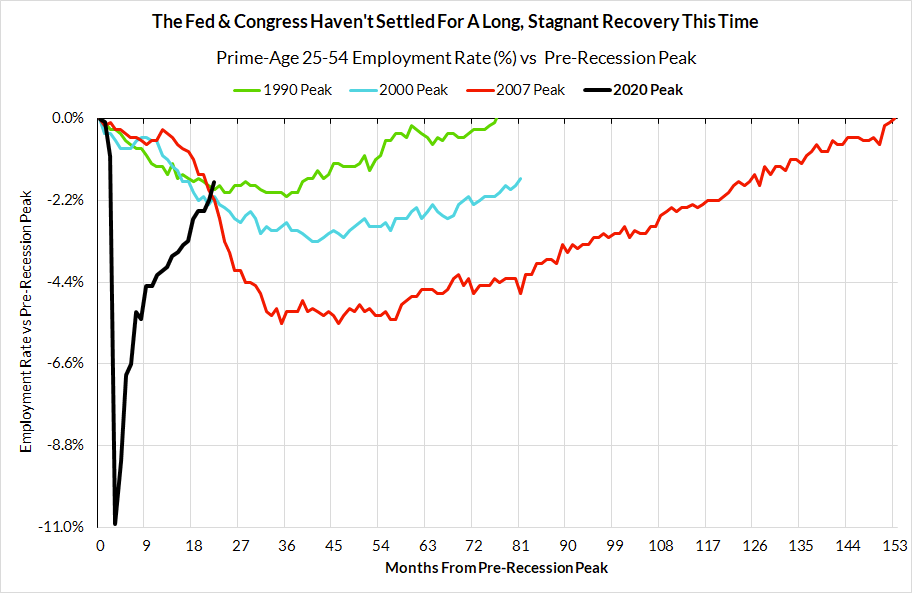

In those previous recoveries, the prime-age employment rate was still declining 22 months after the previous pre-recession peaks.

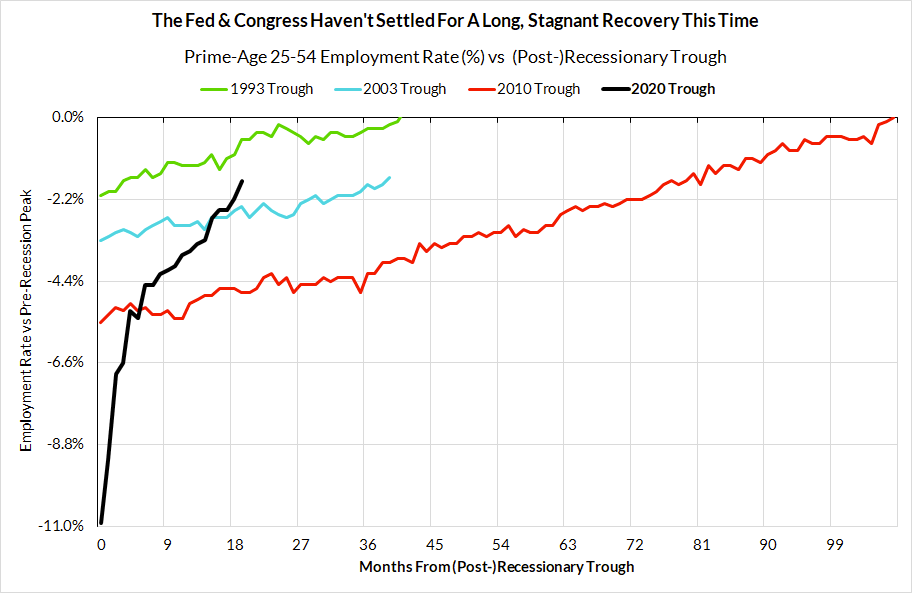

If comparing performance to the pre-recession peak seems unfair, it's worth noting that we see a similar story even if we evaluate the recovery from the trough of the prime-age employment rate. The three previous troughs occurred after the recession officially ended. This recovery is likely to be much faster than the previous three despite starting from a much deeper trough and the additional impediments that the pandemic imposed.

To understand the pandemic recovery, we have to put it into its proper perspective. Current fiscal and monetary policymakers have clearly outdone their predecessors and have shattered past excuses for why Americans should settle for a shallow and sluggish employment recovery. The Fed's commitment to avoiding interest rate policy tightening until maximum employment is achieved has played a pivotal role in creating financial conditions sufficiently supportive to achieve this goal.

In February 2021, Chair Powell noted that maximum employment is "a broad and inclusive goal" that spans more than just the one-dimensional and highly flawed unemployment rate. We agree and hope the Fed will choose multiple indicators to evaluate maximum employment that are robust to the measurement flaws that attend the unemployment rate.

Any committee assessment of maximum employment must include labor utilization measures that are robust to the excessively exclusive definitions of labor force participation in the Current Population Survey.

Ideally, the Fed would go beyond these two principles and lay out measures that better identify sources of cyclical inequity and marginalization. However, these two principles should be an unobjectionable starting point for thinking about a broad and inclusive measure of "maximum employment."

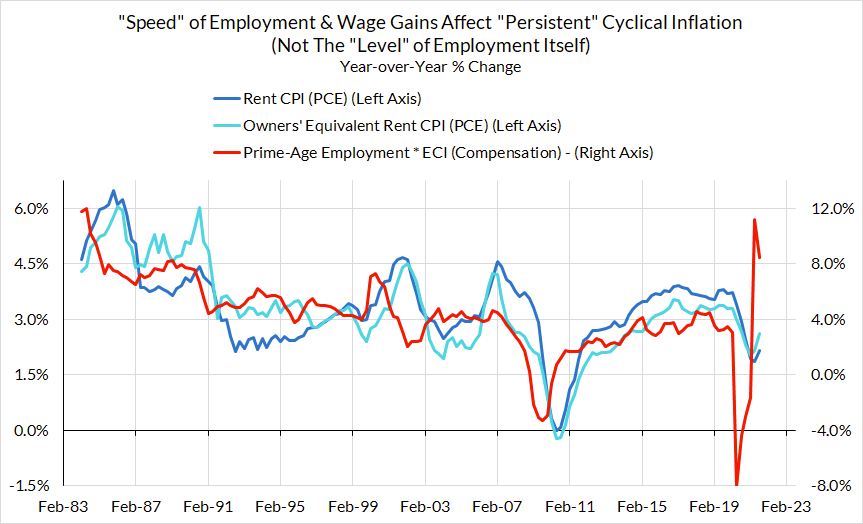

In the process of pursuing a historically rapid recovery in labor utilization, the economy is seeing evidence of a faster cyclical inflation recovery. As that historic pace subsides over the course of 2022, the inflationary pressure should subside as well. Although price inflation is currently very strong, it is likely that there still exists a pace of positive labor utilization gains consistent with the Fed's longer run inflation goals. The precise pace will, of course, be a function of the kinds of inflationary pressures the economy is experiencing over the course of 2022 and beyond.

But before the Fed seeks to slow the pace of the expansion through possible interest rate increases, the Fed's mandate and its credibility still require that it--at a bare minimum–support a full return to the pre-pandemic labor market, both in terms of wage growth and age-adjusted employment rates.

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.